Table of Contents

Overview

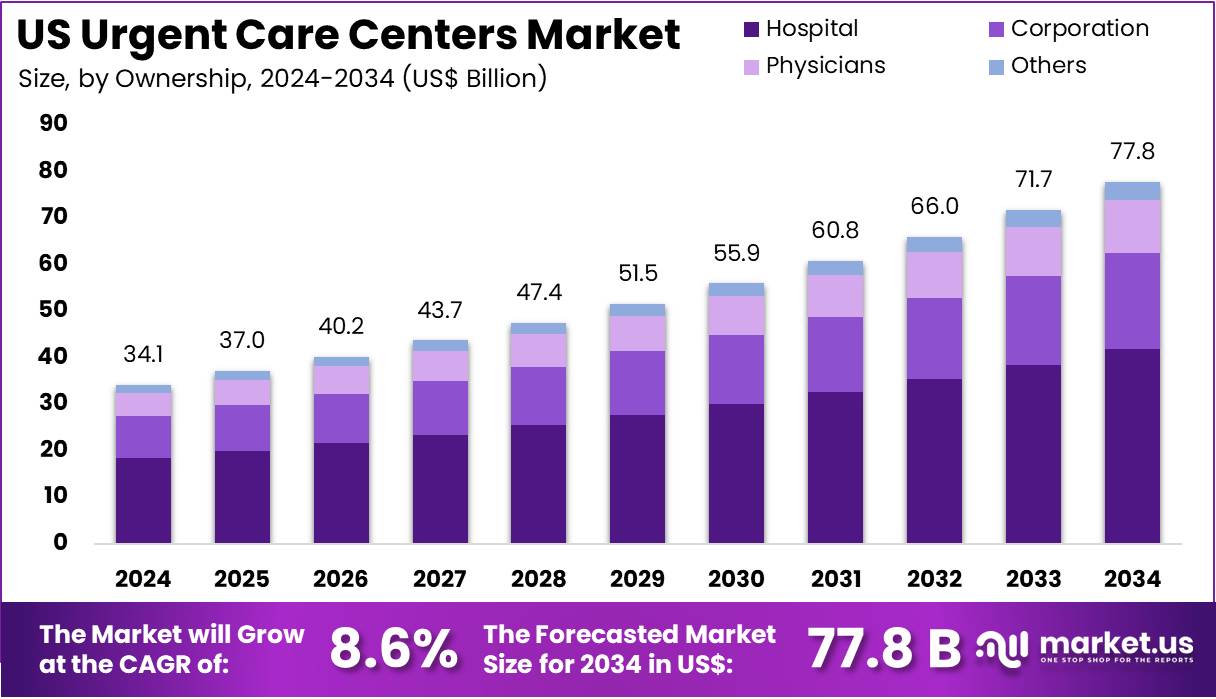

New York, NY – June 22, 2026 – The US Urgent Care Centers Market size is expected to be worth around US$ 77.8 billion by 2034 from US$ 34.1 billion in 2024, growing at a CAGR of 8.6% during the forecast period 2025 to 2034.

The United States urgent care centers market represents a rapidly expanding segment within the broader outpatient healthcare system, providing accessible, cost-efficient, and time-sensitive medical services for non-life-threatening conditions. These facilities bridge the gap between primary care physicians and emergency departments, offering walk-in treatment for illnesses, minor injuries, diagnostic services, and preventive care.

The growth of urgent care centers can be attributed to increasing demand for convenient healthcare access, rising emergency room overcrowding, and growing healthcare expenditure. A significant shift in patient preference toward on-demand care services has further strengthened market adoption. The sector is estimated to encompass more than 14,000–15,000 centers across the United States, with continued expansion driven by both independent operators and hospital-affiliated networks.

Services commonly provided include treatment for flu, infections, sprains, fractures, minor burns, occupational health services, vaccinations, and basic laboratory and imaging diagnostics. Extended operating hours, including evenings and weekends, have enhanced patient accessibility and reduced reliance on emergency departments for non-critical cases.

The market structure is moderately fragmented, with key players operating multi-site networks and leveraging digital health integration, online appointment systems, and telehealth services. The integration of electronic health records and value-based care models has further improved operational efficiency.

The continued expansion of insured patient populations, along with increasing awareness regarding cost-effective care alternatives, is expected to support sustained growth of urgent care centers across the United States healthcare landscape.

Key Takeaways

- In 2024, the US urgent care centers market generated revenue of US$ 34.1 billion and is projected to expand at a CAGR of 8.6%, reaching approximately US$ 77.8 billion by 2034.

- Based on ownership, the market is segmented into hospitals, corporations, physicians, and others. Hospitals emerged as the dominant segment in 2024, accounting for a 53.7% market share.

- In terms of application, the market is categorized into respiratory diseases & infections, general symptoms, injuries, and others. Among these, respiratory diseases & infections represented the leading segment, holding a 49.3% share of the overall market.

Segmentation Analysis

- Ownership Analysis: In 2024, the hospital segment accounted for a dominant 53.7% share of the urgent care market. This expansion has been supported by hospitals increasingly broadening access to non-emergency care services. By developing urgent care facilities, pressure on emergency departments has been reduced, leading to improved patient flow management. Faster and more cost-efficient care delivery has been enabled through these centers, strengthening patient preference for walk-in services for minor medical conditions. The continued focus on accessibility and service convenience is expected to support sustained growth of hospital-owned urgent care facilities in the forecast period.

- Application Analysis: Respiratory diseases and infections represented a leading 49.3% share in 2024. The high incidence of influenza, COVID-19, bronchitis, and allergic conditions has been a key growth driver. Rapid diagnosis and treatment services offered by urgent care centers have improved patient outcomes while reducing waiting times. The availability of quick testing solutions, including influenza and COVID-19 diagnostics, has strengthened the role of these centers in primary care delivery. Increasing awareness regarding early disease detection is expected to further drive patient inflow, particularly during seasonal outbreaks and epidemic cycles.

Emerging Trends

- Rising Demand for Convenient Care: Rising demand for convenient care is being observed as patients increasingly prefer fast healthcare services over long hospital waiting times. Walk-in urgent care centers are being chosen for minor injuries and infections, offering flexible, affordable, and accessible treatment options nationwide.

- Expansion into Specialized Services: Urgent care clinics are expanding services beyond basic treatment to include mental health counseling, pediatric care, and chronic disease management. On-site diagnostics such as X-rays and lab testing are offered, improving care coordination and enhancing patient convenience and clinical efficiency.

- Blended Care Models: Blended care models integrate urgent care and emergency services within a single facility to manage both minor and severe conditions. This approach reduces emergency department congestion, improves patient routing efficiency, and enables faster access to appropriate levels of medical care.

- Use of AI and Digital Tools: Use of artificial intelligence and digital tools is improving operational efficiency in urgent care centers. Automated scheduling, electronic check-ins, and AI-based triage systems reduce waiting times, streamline administrative tasks, and enhance accuracy in patient assessment and overall service delivery quality.

Use Cases

- Treatment for Common Illnesses and Injuries: Urgent care centers provide immediate treatment for non-life-threatening conditions such as infections, sprains, cuts, and minor burns. Walk-in access, on-site diagnostics, and rapid treatment reduce reliance on emergency rooms, ensuring timely and cost-effective healthcare for everyday medical needs delivery system.

- Follow-Up and Chronic Condition Support: Urgent care services extend support for chronic conditions such as asthma, diabetes, and hypertension, especially during flare-ups. They provide timely intervention when primary care is unavailable, helping prevent complications, reduce emergency visits, and ensure continuity of essential healthcare support services.

- Behavioral Health and Mental Health Access: Some urgent care centers provide behavioral and mental health services addressing stress, anxiety, and emotional distress. These facilities offer immediate consultations and short-term support, bridging gaps in specialist availability and improving access to timely psychological care for patients in need.

- Travel Medicine and Vaccinations: Urgent care centers support travel medicine needs and vaccination requirements, offering routine and travel-specific immunizations such as flu, tetanus, and MMR. They also provide consultations for international travel health preparation, ensuring convenient access for families and frequent travelers health services.

Frequently Asked Questions on US Urgent Care Centers

- What are US urgent care centers?

US urgent care centers are outpatient healthcare facilities designed to treat non-life-threatening conditions requiring immediate attention. These centers bridge the gap between primary care and emergency departments, offering walk-in consultations, diagnostics, and treatment services with extended operating hours. - What services are provided by urgent care centers in the US?

US urgent care centers provide a wide range of medical services including treatment for minor injuries, infections, respiratory illnesses, vaccinations, diagnostic imaging, laboratory testing, and occupational health services, typically delivered without prior appointment requirements. - Why is demand for US urgent care centers increasing?

Demand for urgent care centers in the United States is increasing due to rising emergency department congestion, growing patient preference for convenient healthcare access, higher healthcare costs, and expansion of insurance coverage supporting outpatient care utilization. - How large is the US urgent care centers market?

The US urgent care centers market was valued at US$ 34.1 billion in 2024 and is projected to grow at a CAGR of 8.6%, reaching approximately US$ 77.8 billion by 2034, supported by strong outpatient care demand. - What is the ownership structure of urgent care centers in the US?

The ownership structure of US urgent care centers is segmented into hospitals, corporations, physicians, and others. Hospitals dominate the market with a 53.7% share, driven by integrated healthcare networks and stronger operational and referral capabilities. - What is the future outlook for the US urgent care centers market?

The US urgent care centers market is expected to witness sustained growth, driven by increasing outpatient utilization, digital health integration, and expanding insurance coverage, alongside continued emphasis on cost-effective and accessible healthcare delivery models across the country.

Conclusion

The United States urgent care centers market is positioned for sustained expansion, supported by increasing demand for accessible and cost-efficient outpatient services. Growth can be attributed to rising emergency department congestion, expanding insured populations, and strong patient preference for walk-in care models.

Hospital-affiliated networks continue to dominate the market, while digital integration and AI-enabled systems are enhancing operational efficiency. Respiratory and infection-related cases remain the primary demand drivers. Over the forecast period, continued investments in infrastructure, service diversification, and blended care models are expected to strengthen market penetration and improve healthcare delivery outcomes across the United States healthcare ecosystem overall.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)