Table of Contents

Overview

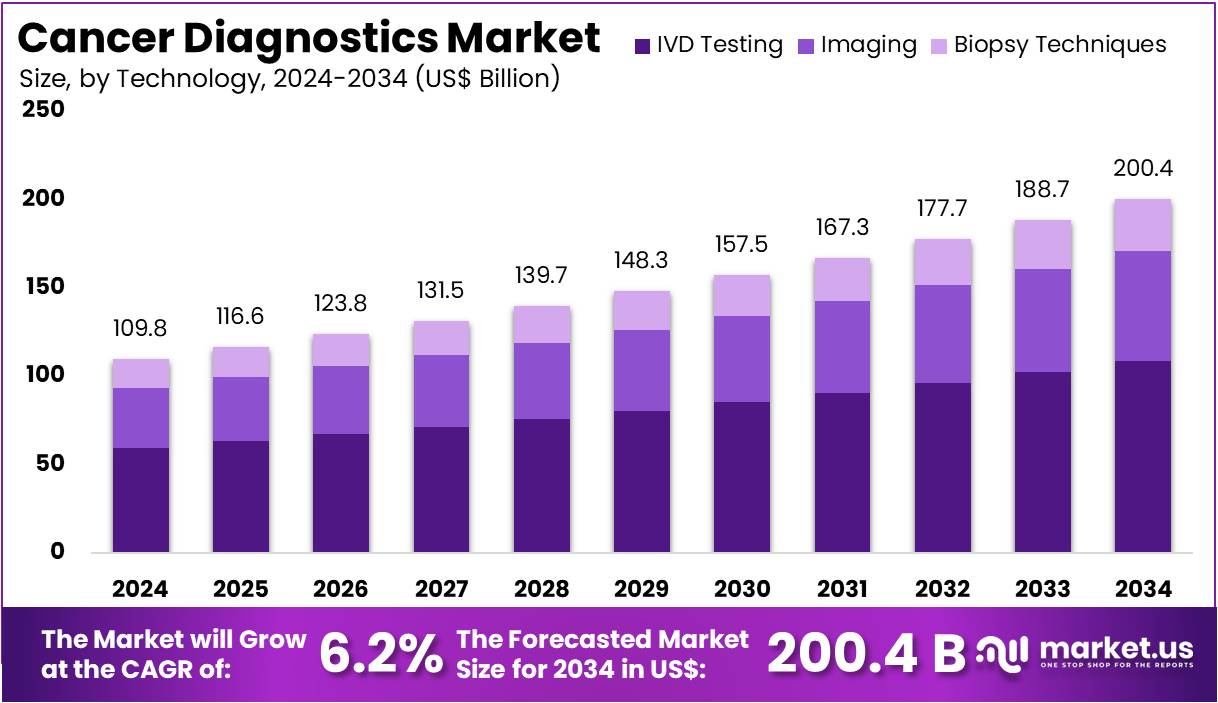

New York, NY – July 06, 2026 – The Cancer Diagnostics Market size is expected to be worth around US$ 200.4 Billion by 2034 from US$ 109.8 Billion in 2024, growing at a CAGR of 6.2% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 43.2% share and holds US$ 47.4 Billion market value for the year.

Cancer diagnostics refers to the range of tests and technologies used to detect, identify, and monitor cancer at different stages of the disease. These diagnostic methods play a critical role in enabling early detection, accurate diagnosis, treatment planning, and ongoing disease monitoring. Common diagnostic approaches include laboratory testing, imaging techniques, molecular diagnostics, genetic testing, biopsy, and pathology analysis. Advances in precision medicine and biomarker-based testing have significantly improved the accuracy and speed of cancer diagnosis, supporting personalized treatment strategies and better patient outcomes.

The increasing global burden of cancer, coupled with rising awareness regarding the benefits of early detection, has driven the adoption of advanced diagnostic technologies across healthcare systems. Continuous innovations in genomic sequencing, liquid biopsy, artificial intelligence-assisted imaging, and companion diagnostics are further enhancing the efficiency and reliability of cancer detection. In addition, government initiatives, cancer screening programs, and growing investments in oncology research are contributing to the expansion of the cancer diagnostics sector.

Healthcare providers are increasingly integrating advanced diagnostic platforms to improve clinical decision-making and optimize patient care. The demand for minimally invasive diagnostic procedures and rapid testing solutions continues to grow, particularly for breast, lung, colorectal, prostate, and blood cancers. As technological advancements continue to reshape oncology diagnostics, the cancer diagnostics market is expected to witness sustained growth, supported by increasing healthcare expenditure, expanding access to diagnostic services, and ongoing research focused on improving early cancer detection and survival rates worldwide.

Key Takeaways

- The cancer diagnostics market was valued at US$ 109.8 billion in 2024 and is projected to reach US$ 200.4 billion by 2034, expanding at a CAGR of 6.2% during the forecast period.

- Based on product type, the market is categorized into consumables, instruments, imaging instruments, and biopsy instruments. Among these, consumables accounted for the largest market share of 42.3% in 2024.

- By technology, the market is segmented into IVD testing, imaging, and biopsy techniques. IVD testing emerged as the leading segment, capturing 54.2% of the market share in 2024.

- In terms of application, breast cancer diagnostics represented the largest segment, contributing 30.8% of the total market revenue in 2024.

- Based on end user, the market is divided into diagnostic laboratories & imaging centers, hospitals & clinics, and research institutes. The diagnostic laboratories & imaging centers segment dominated the market with a 50.5% revenue share in 2024.

- North America maintained its leading position in the global cancer diagnostics market, accounting for 43.2% of the total market share in 2024.

Key Statistics of the Cancer Diagnostics Market

- Global Cancer Mortality (2022): Approximately 10 million people died from cancer worldwide, with nearly 70% of deaths occurring in low- and middle-income countries, largely due to delayed diagnosis and limited access to treatment.

- Global Cancer Incidence (2022): Around 19.3 million new cancer cases were reported globally, highlighting the growing demand for advanced diagnostic technologies.

- U.S. Cancer Burden (2023): An estimated 1.9 million new cancer cases and approximately 610,000 cancer-related deaths were projected in the United States.

- Age-Related Cancer Incidence: Cancer occurrence rises significantly with age, with adults aged 60 years and above experiencing incidence rates of roughly 1,000 cases per 100,000 population.

- Most Prevalent Cancer Types: Breast cancer remains the most frequently diagnosed cancer globally, while lung cancer continues to be the leading cause of cancer incidence and mortality among men.

- Cervical and Stomach Cancer Mortality: Mortality rates for cervical and stomach cancers remain substantially higher in countries with low Human Development Index (HDI) due to limited screening and treatment access.

- Liver and Pancreatic Cancer Outcomes: These cancers are associated with poor prognosis, with the majority of patients not surviving beyond five years after diagnosis.

- Colon and Esophageal Cancer Survival: Survival rates vary across countries depending on healthcare infrastructure and early detection programs, although outcomes remain relatively poor in many regions.

- Ovarian Cancer Survival: The estimated five-year survival rate for ovarian cancer remains close to 30%, reflecting the challenges of late-stage diagnosis.

- Cancer Mortality in India: The majority of cancer-related deaths in India occur among individuals aged 30–69 years, emphasizing the importance of early diagnosis within the working-age population.

Regional Analysis

North America dominated the global cancer diagnostics market with a revenue share of 43.2% in 2024, supported by a high cancer incidence, advanced healthcare infrastructure, and continuous innovation in diagnostic technologies. The growing adoption of molecular diagnostics, imaging systems, and in-vitro diagnostic (IVD) tests has strengthened early cancer detection across the region.

In the United States, more than 1.85 million new cancer cases were reported in 2022, while Canada estimated approximately 247,100 new cases in 2024, reflecting sustained demand for diagnostic solutions. Regulatory support has further accelerated market growth, with the U.S. Food and Drug Administration approving a significant number of oncology diagnostic devices and IVDs. In addition, strong investments by leading diagnostic companies and the increasing commercialization of precision oncology technologies continue to reinforce North America’s market leadership.

Asia Pacific is projected to register the fastest CAGR during the forecast period, driven by the rising prevalence of cancer, expanding healthcare infrastructure, and increasing awareness of early diagnosis. Countries such as China, India, and Japan are witnessing growing demand for advanced diagnostic technologies due to their large patient populations. Government initiatives promoting cancer screening, greater healthcare investments, and improving access to modern diagnostic services are supporting market expansion.

Furthermore, increasing adoption of molecular diagnostics, AI-enabled imaging, and liquid biopsy technologies, along with investments from global diagnostic companies, is expected to accelerate the region’s cancer diagnostics market growth over the coming years.

Emerging Trends in Cancer Diagnostics

- Personalized Cancer Vaccines: Personalized vaccines are advancing precision medicine by stimulating immune responses against patient-specific tumor characteristics, reducing recurrence risks and improving treatment outcomes.

- Multi-Cancer Early Detection (MCED) Tests: Novel blood-based diagnostic tests capable of identifying multiple cancer types simultaneously are improving early-stage detection and expanding screening opportunities.

- Rapid Treatment Delivery Methods: Innovations in drug administration, including ultra-fast injectable therapies, are enhancing patient convenience while improving healthcare system efficiency.

- Precision Oncology: Genomic profiling and molecular diagnostics are enabling individualized treatment selection, improving therapeutic effectiveness and minimizing treatment-related toxicity.

- Artificial Intelligence (AI) in Cancer Diagnostics: AI-powered technologies are enhancing image interpretation, risk assessment, pathology analysis, and clinical decision-making, resulting in faster and more accurate diagnoses.

- Regenerative Medicine Applications: Advances in stem cell therapies and tissue engineering are creating new treatment opportunities for cancers with limited therapeutic options, supporting future innovations in oncology care.

Key Use Cases of Cancer Diagnostics

- Early Cancer Detection and Screening: Advanced diagnostic technologies, including multi-cancer blood tests, facilitate earlier identification of malignancies, improving survival rates and treatment success.

- Personalized Treatment Planning: Biomarker testing and genomic profiling enable clinicians to develop customized treatment strategies that maximize therapeutic effectiveness while minimizing adverse effects.

- Monitoring Disease Progression and Recurrence: Liquid biopsy and circulating tumor DNA (ctDNA) analysis provide minimally invasive tools for tracking treatment response and detecting disease recurrence.

- Clinical Research and Drug Development: Cancer diagnostics support patient stratification for clinical trials, biomarker discovery, and the evaluation of targeted therapies, accelerating oncology research.

- Palliative Care Management: Diagnostic imaging and molecular testing assist in assessing disease progression, monitoring treatment-related complications, and optimizing supportive care strategies for patients with advanced cancer.

Frequently Asked Questions on Cancer Diagnostics

- Why is early cancer diagnosis important?

Early cancer diagnosis improves the chances of successful treatment by identifying tumors before they spread to other parts of the body. Timely detection supports less invasive therapies, enhances survival rates, reduces healthcare costs, and improves the overall quality of life for patients. - What are the major technologies used in cancer diagnostics?

Cancer diagnostics primarily utilizes in-vitro diagnostics (IVD), medical imaging, biopsy techniques, molecular diagnostics, liquid biopsy, and genomic sequencing. These technologies help physicians accurately identify cancer types, determine disease stages, detect biomarkers, and select personalized treatment strategies for patients. - What factors are driving the growth of the cancer diagnostics market?

The market is expanding due to the increasing global cancer burden, rising awareness of early detection, technological advancements in molecular diagnostics and AI-based imaging, growing healthcare investments, supportive government screening programs, and the increasing adoption of precision medicine. - Which product segment dominates the cancer diagnostics market?

Consumables represent the largest product segment because diagnostic tests require a continuous supply of reagents, assay kits, antibodies, and laboratory chemicals. Their recurring demand across hospitals, laboratories, and research facilities contributes significantly to overall market revenue. - Which region leads the global cancer diagnostics market?

North America holds the largest share of the global cancer diagnostics market due to its advanced healthcare infrastructure, widespread adoption of innovative diagnostic technologies, high cancer prevalence, favorable reimbursement policies, and strong presence of leading diagnostic companies and research institutions. - What is the future outlook for the cancer diagnostics market?

The cancer diagnostics market is expected to experience steady growth over the coming years, driven by continuous technological innovation, expanding cancer screening programs, increasing demand for personalized medicine, and greater adoption of minimally invasive diagnostic techniques such as liquid biopsy and AI-assisted diagnostics.

Conclusion

The global cancer diagnostics market is poised for sustained growth, driven by the rising incidence of cancer, increasing emphasis on early detection, and continuous advancements in diagnostic technologies. Innovations in molecular diagnostics, liquid biopsy, AI-powered imaging, and precision oncology are improving diagnostic accuracy and enabling personalized treatment approaches.

Strong government support, expanding screening programs, and growing healthcare investments are further accelerating market development across both developed and emerging economies. While North America maintains market leadership, Asia Pacific is expected to witness the fastest growth. Overall, the market will remain essential in improving patient outcomes, supporting timely interventions, and advancing global cancer care.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)