Introduction

According to Organic Packaged Food Statistics, Organic packaged food encompasses a wide range of products meeting strict organic farming standards, such as the USDA Organic certification in the United States or the European Commission’s regulations in the EU.

These foods feature ingredients from organic farms and are grown without synthetic pesticides, fertilizers, GMOs, or irradiation.

Packaging typically includes labels indicating organic certification, ensuring consumers of the product’s adherence to these standards.

While organic foods may offer nutritional benefits and align with sustainability and health-conscious consumer preferences, challenges like higher production costs and limited ingredient availability persist.

Nonetheless, the sector continues to grow globally, driven by increased consumer awareness and demand for natural, sustainable options.

Editor’s Choice

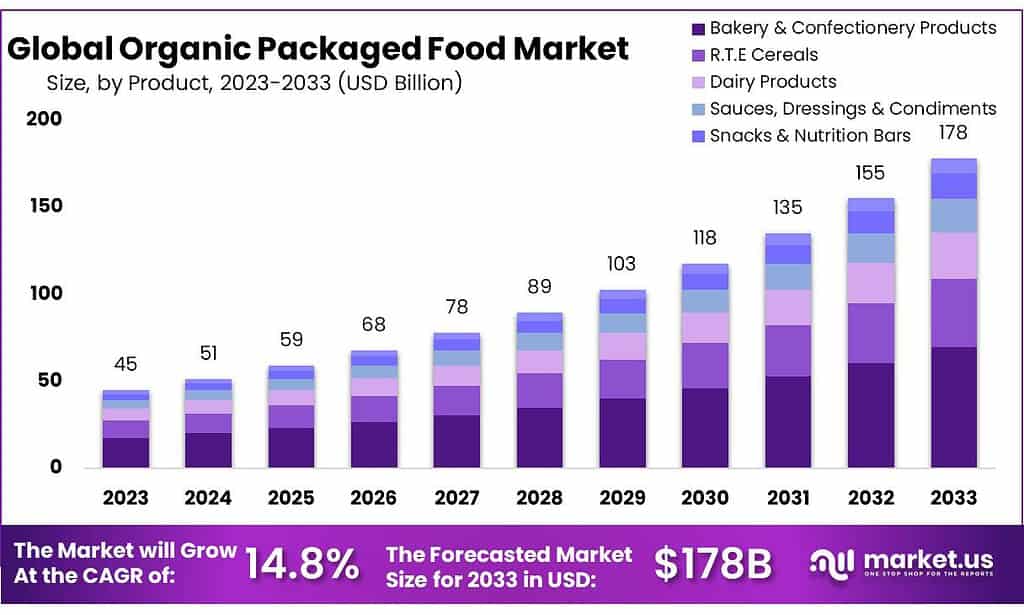

- In 2023, the global organic packaged food market revenue was recorded at USD 45 billion.

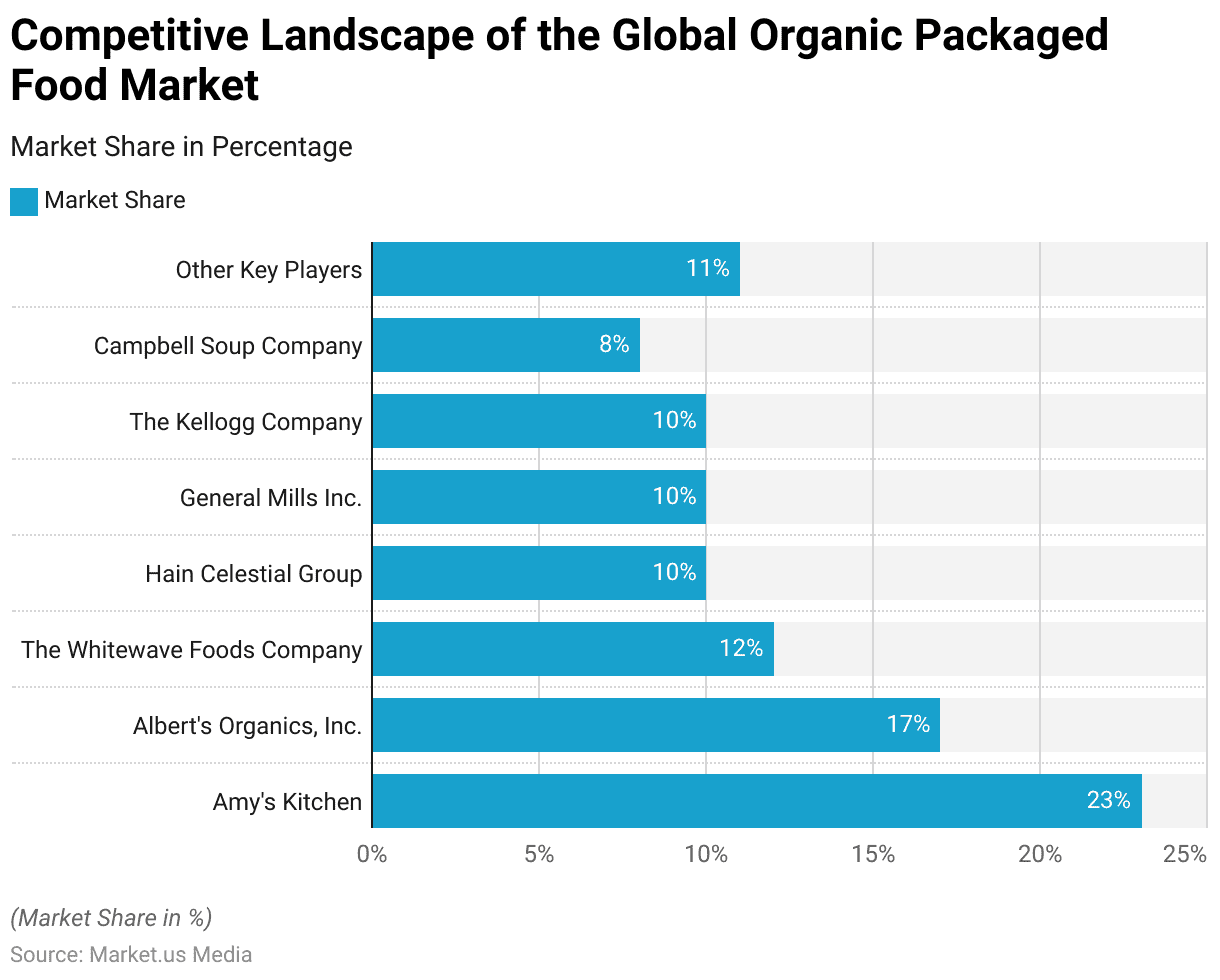

- In the global organic packaged food market, Amy’s Kitchen holds a leading position with a market share of 23%.

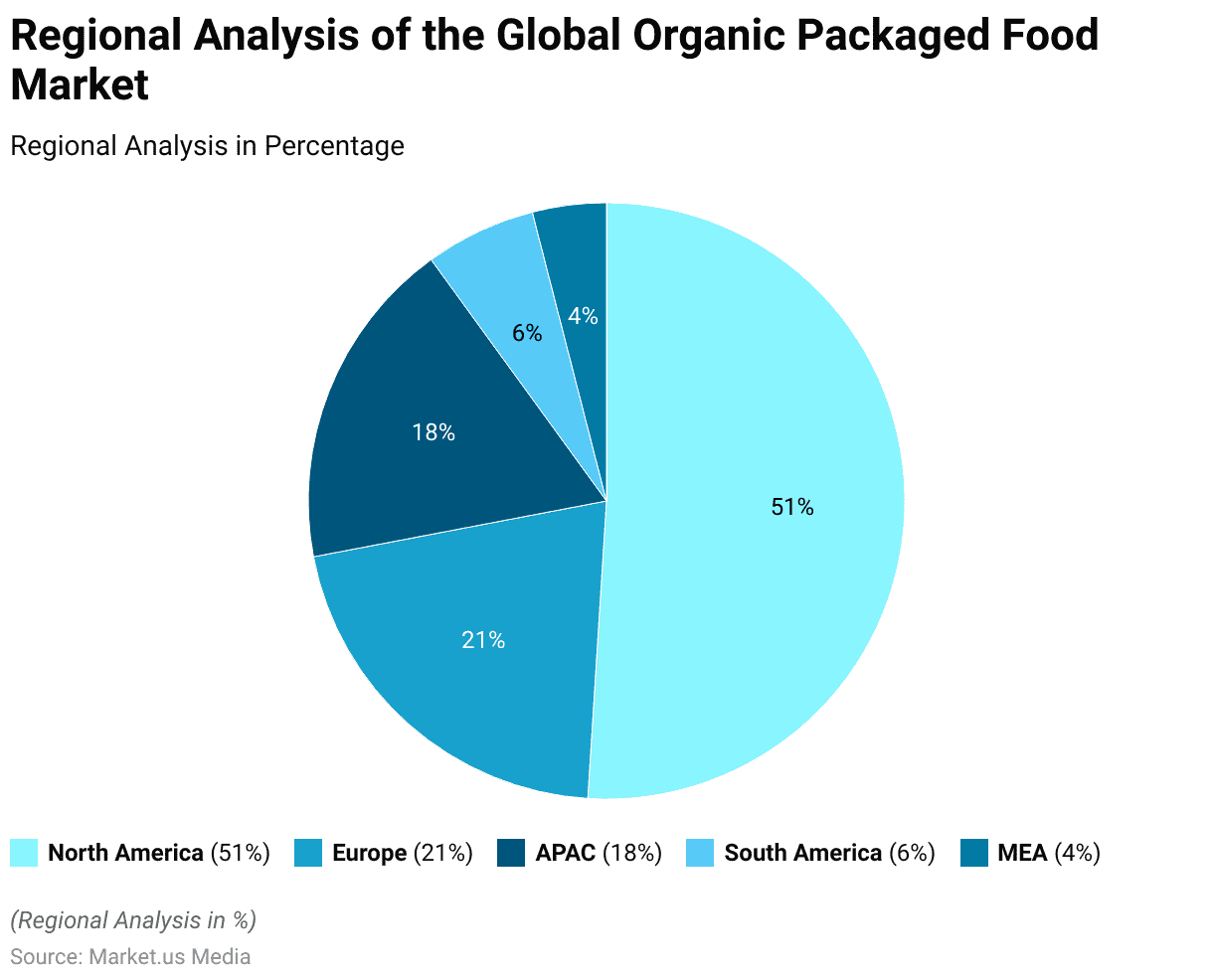

- The global organic packaged food market is predominantly led by North America, which holds a commanding 51.0% market share.

- In 2023, the leading organic food brands in the United States, ranked by brand awareness, showcased notable market recognition. Trader Joe’s led with a brand awareness of 72%.

- The COVID-19 pandemic saw a surge in demand for organic food, with sales soaring to USD 120.65 billion in 2020.

- The majority of Americans are opting for organic foods due to health concerns, with 55% believing organic fruits and vegetables are superior for one’s well-being.

- Approximately 72% of American adults consider the price difference between organic and conventionally grown foods when deciding whether to purchase organic.

Global Organic Packaged Food Market Overview

Global Organic Packaged Food Market Size

- The global organic packaged food market has exhibited substantial growth over the past decade at a CAGR of 14.8%.

- In 2023, the market revenue was recorded at USD 45 billion.

- The most substantial growth is projected for 2032, with an expected market revenue of USD 155 billion.

Competitive Landscape of the Global Organic Packaged Food Market

- In the global organic packaged food market, Amy’s Kitchen holds a leading position with a market share of 23%.

- Albert’s Organics, Inc. follows with a 17% share, while The Whitewave Foods Company accounts for 12% of the market.

- Hain Celestial Group, General Mills Inc., and The Kellogg Company each possess a 10% share.

- Campbell Soup Company captures 8% of the market, with other key players collectively holding an 11% share.

Regional Analysis of the Global Organic Packaged Food Market

- The global organic packaged food market is predominantly led by North America, which holds a commanding 51.0% market share.

- Europe follows with a 21.0% share, reflecting strong consumer demand in the region.

- The Asia-Pacific (APAC) region accounts for 18.0% of the market, indicating significant growth potential.

- South America holds a 6.0% share, while the Middle East and Africa (MEA) region captures 4.0% of the market.

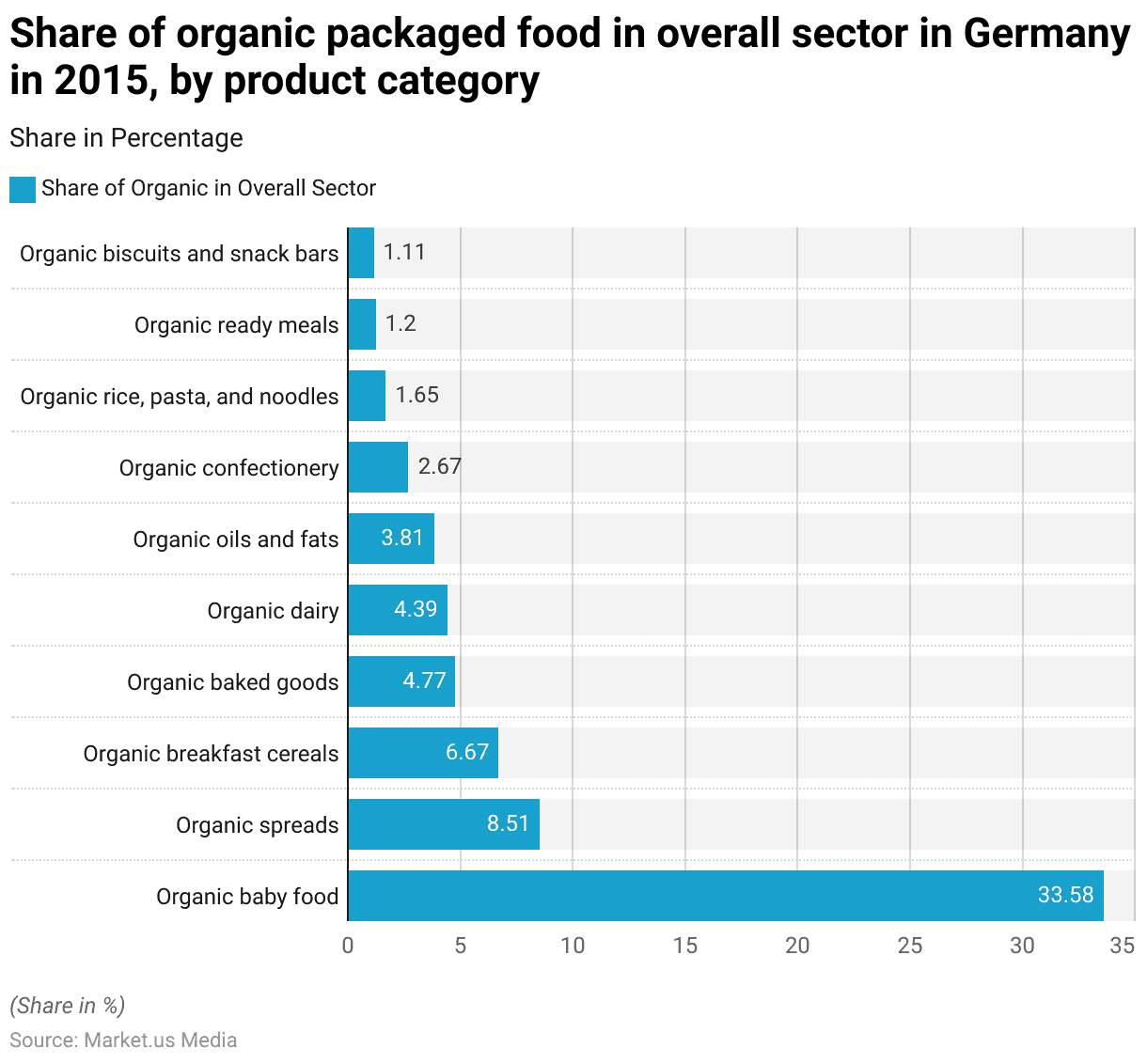

- In 2015, the share of organic packaged food within the overall sector in Germany varied significantly by product category.

- Organic baby food held the highest market penetration, comprising 33.58% of its overall sector.

- Organic spreads followed with an 8.51% share, while organic breakfast cereals accounted for 6.67%.

- Organic baked goods represented 4.77% of their sector, and organic dairy products constituted 4.39%.

- The share of organic oils and fats was 3.81%, and organic confectionery held 2.67%.

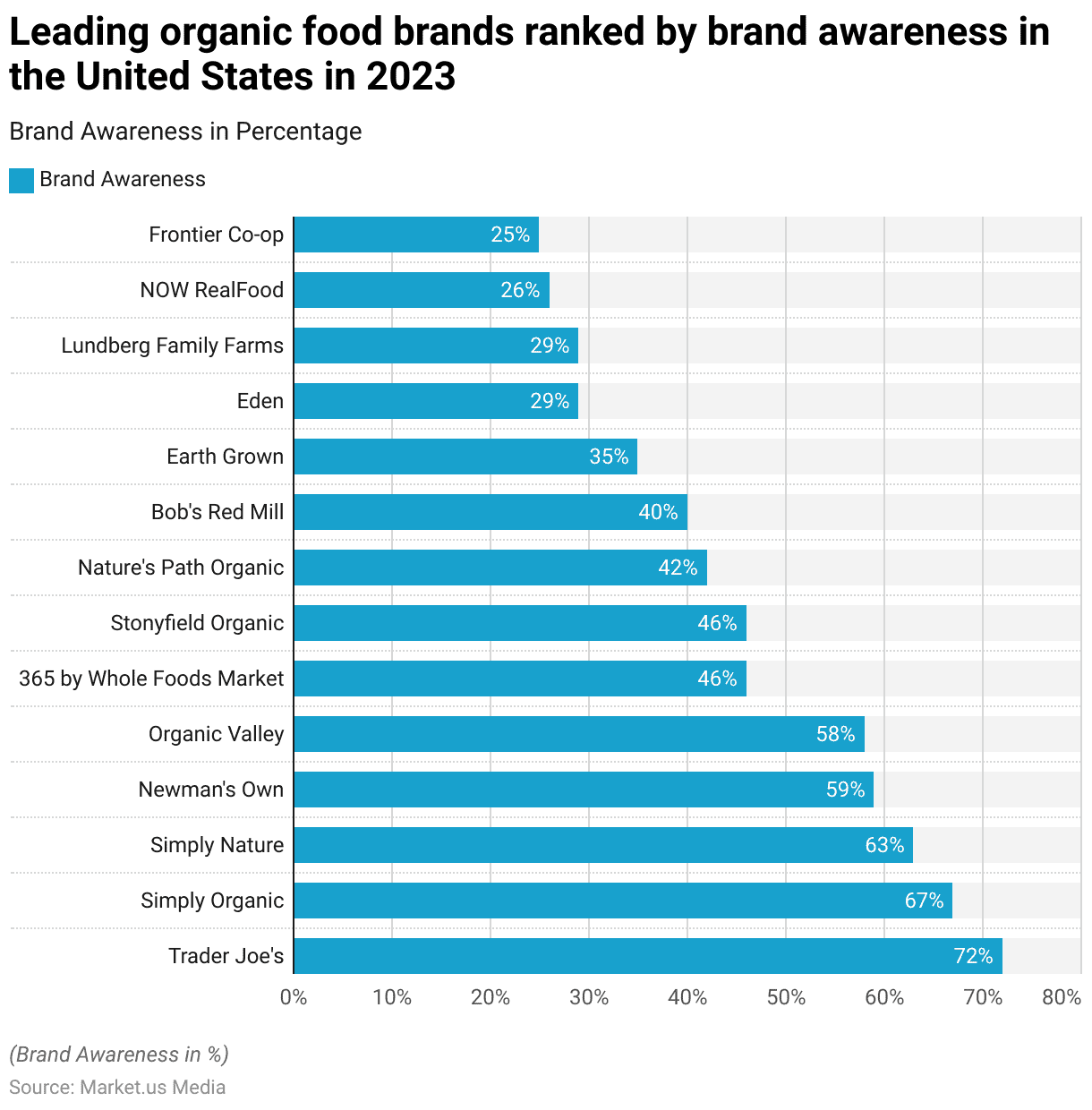

Leading Organic Packaged Food Brands – By Brand Awareness

- In 2023, the leading organic food brands in the United States, ranked by brand awareness, showcased notable market recognition.

- Trader Joe’s led with brand awareness of 72%, followed by Simply Organic at 67% and Simply Nature at 63%.

- Newman’s Own and Organic Valley were also prominent, with 59% and 58% awareness, respectively. Both 365 by Whole Foods Market and Stonyfield Organic achieved 46% brand awareness.

- Nature’s Path Organic was recognized by 42% of consumers, while Bob’s Red Mill had a 40% awareness.

- Earth Grown followed with 35%, and both Eden and Lundberg Family Farms had 29% awareness.

Global Organic Food Sales Statistics

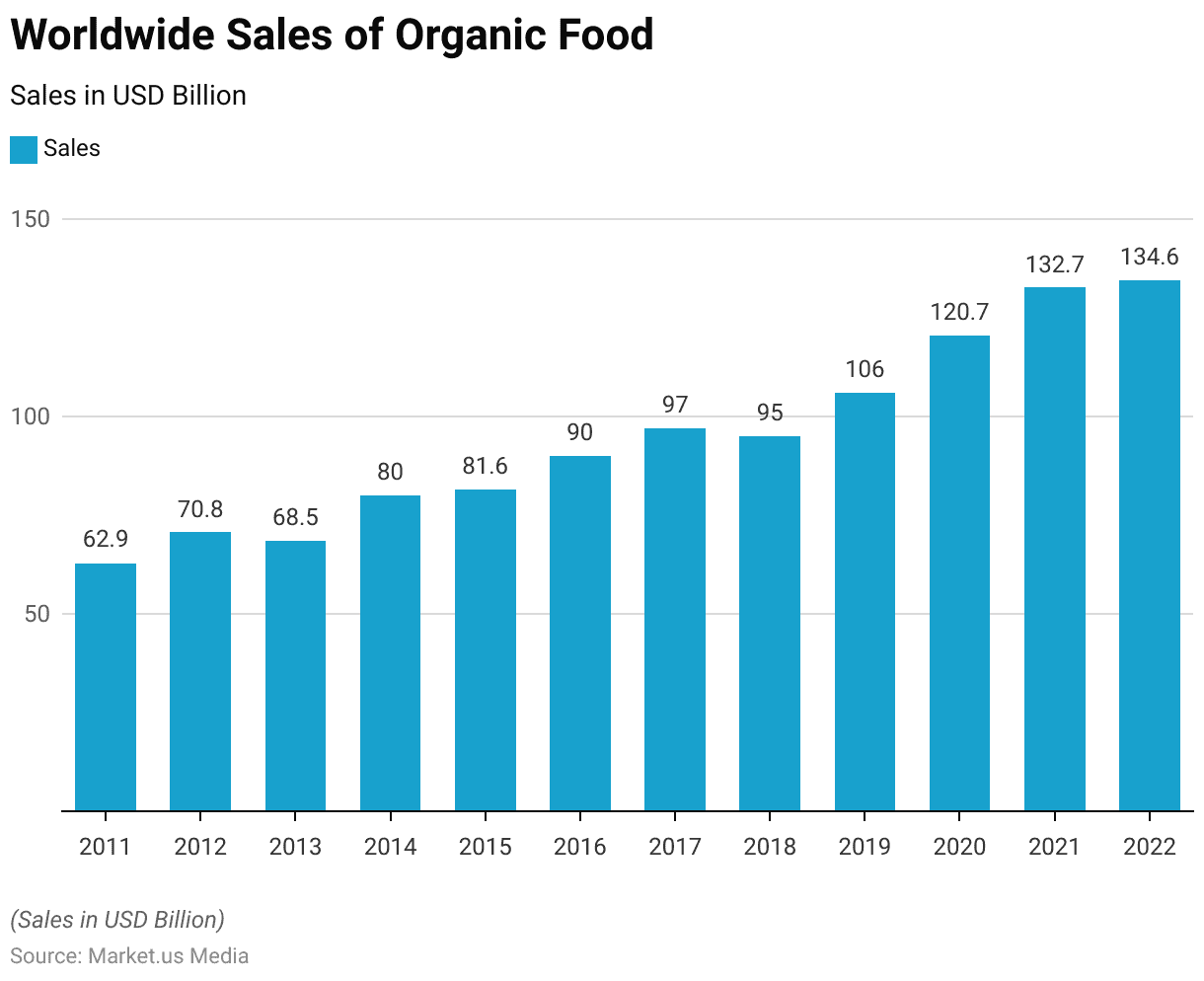

Worldwide Sales of Organic Food

- The worldwide sales of organic food have demonstrated a notable upward trajectory over the past decade.

- In 2011, the market achieved sales of USD 62.9 billion, which increased to USD 70.8 billion in 2012.

- Despite a slight dip to USD 68.5 billion in 2013, the market rebounded to USD 80 billion in 2014 and further to USD 81.6 billion in 2015.

- The COVID-19 pandemic saw a surge in demand for organic food, with sales soaring to USD 120.65 billion in 2020.

- This trend persisted in 2021, with sales rising to USD 132.74 billion, and in 2022, the market slightly increased to USD 134.6 billion, reflecting sustained consumer interest in organic products.

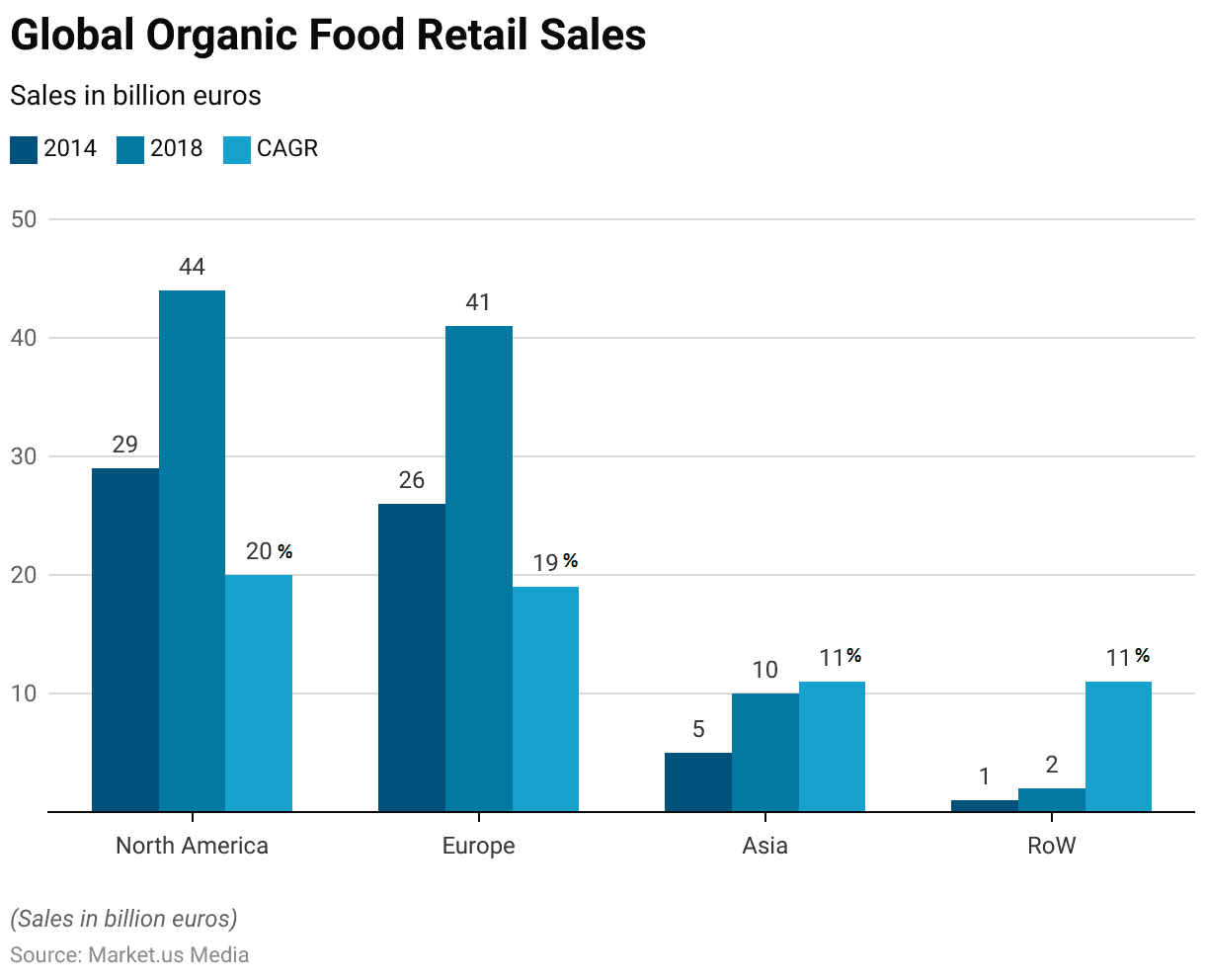

Global Organic Food Retail Sales

- Between 2014 and 2018, global organic food retail sales exhibited significant growth across various regions.

- In North America, sales increased from 29 billion euros in 2014 to 44 billion euros in 2018, reflecting a robust compound annual growth rate (CAGR) of 20%.

- Europe also saw considerable growth, with sales rising from 26 billion euros to 41 billion euros, corresponding to a CAGR of 19%.

- In Asia, the market expanded from 5 billion euros to 10 billion euros, achieving a CAGR of 11%.

- The rest of the world (RoW) experienced growth from 1 billion euros to 2 billion euros, maintaining a CAGR of 11%.

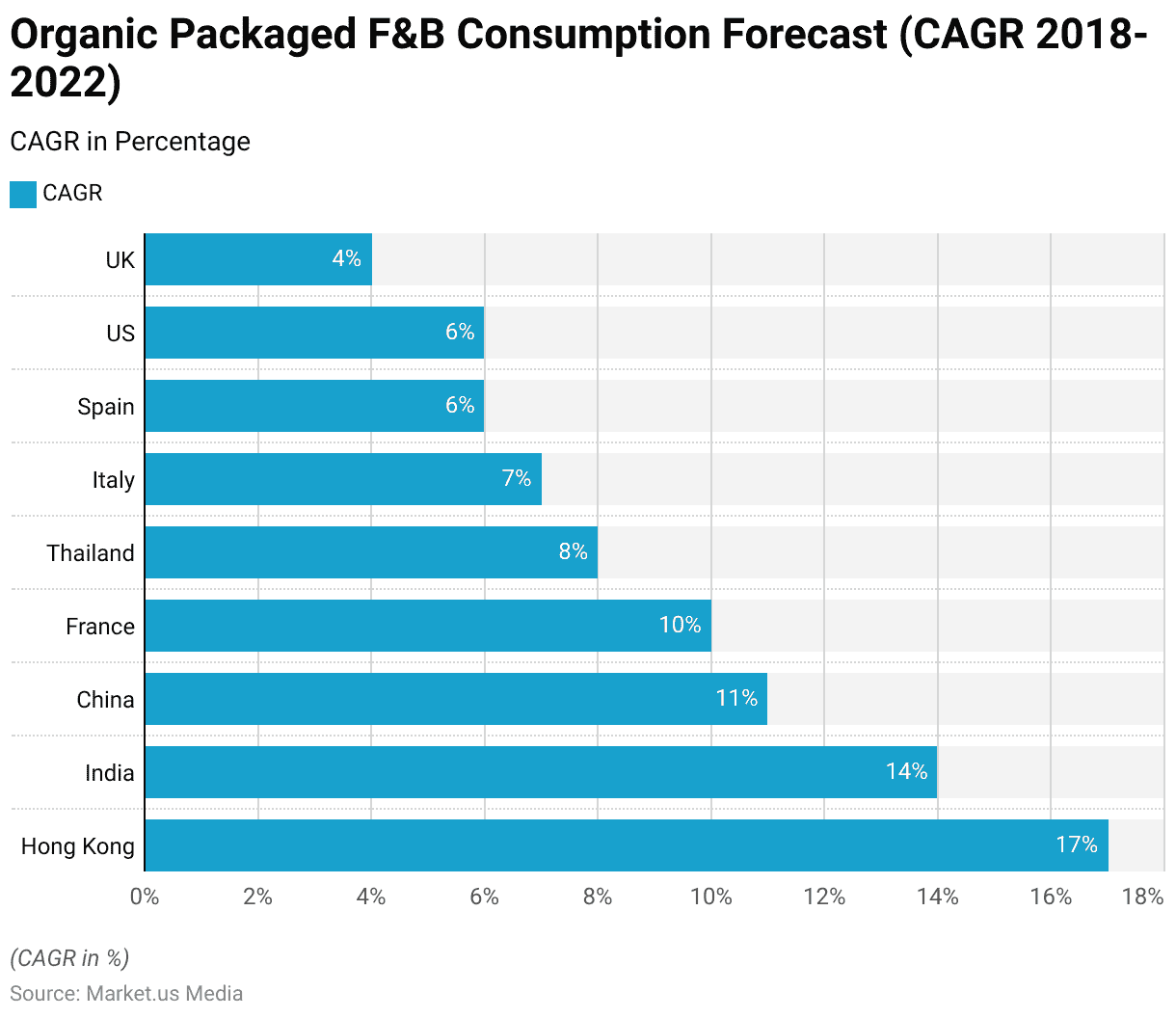

Organic Packaged Food and Beverage Consumption

- The forecast for organic packaged food and beverage consumption between 2018 and 2022 reveals diverse growth rates across various countries.

- Hong Kong leads with a robust compound annual growth rate (CAGR) of 17%, followed by India with a 14% CAGR and China with an 11% CAGR.

- France shows a solid growth rate of 10%, while Thailand is projected to grow at 8%.

- Italy and Spain are expected to see CAGRs of 7% and 6%, respectively, matching the growth rate of the United States.

- The United Kingdom anticipates a more modest growth, with a 4% CAGR.

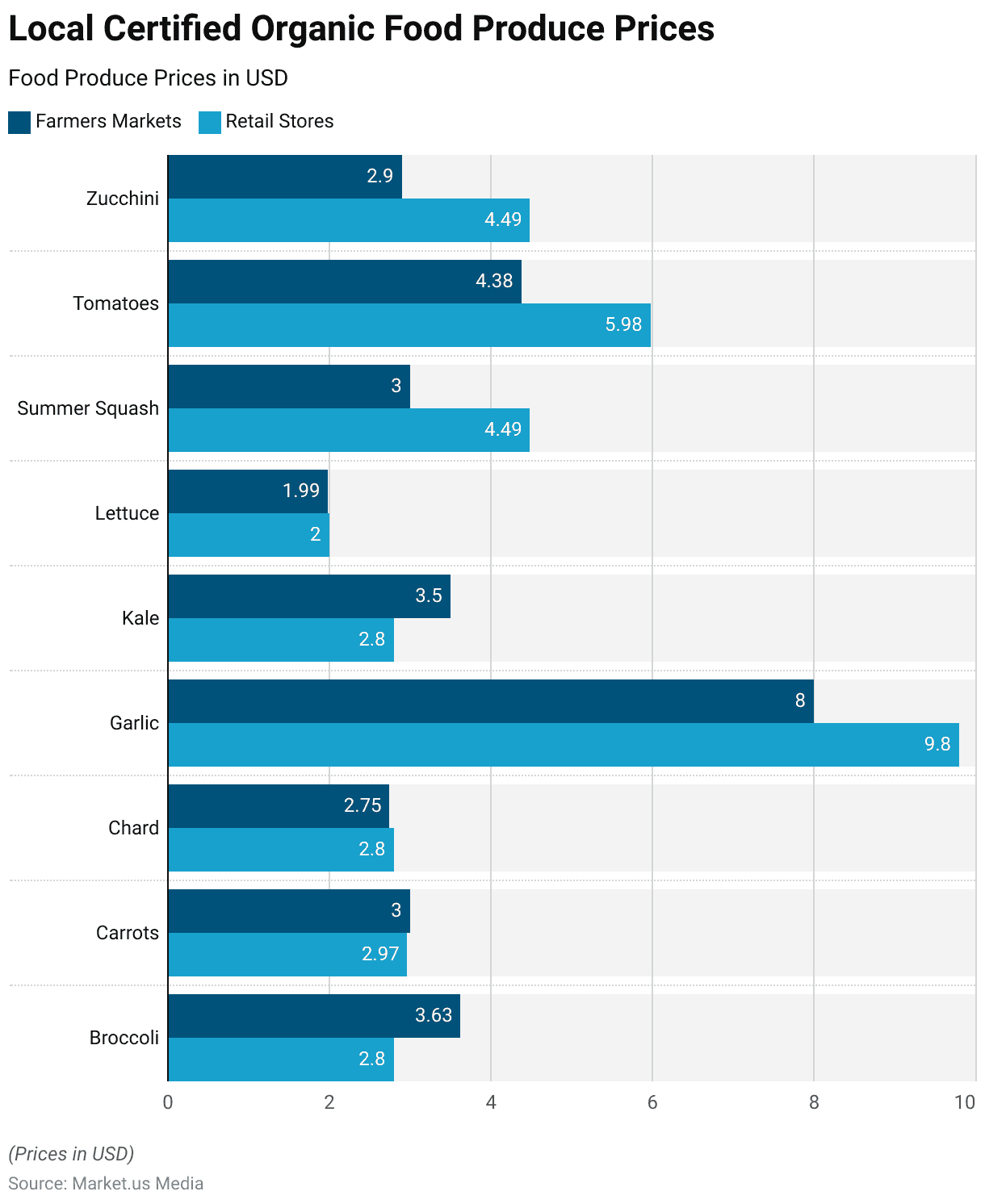

Local Certified Organic Food Produce Prices

- At farmer’s markets, the price per pound for broccoli is USD 3.63, whereas, in retail stores, it is slightly lower at USD 2.80.

- Carrots are priced at USD 3.00 per pound in farmers’ markets, comparable to USD 2.97 in retail stores.

- Chard is sold for USD 2.75 per pound at farmers’ markets and USD 2.80 in retail stores.

- Garlic, however, is more expensive at retail stores, priced at USD 9.80 per pound, compared to USD 8.00 at farmers’ markets.

- Kale is priced at USD 3.50 per pound at farmers’ markets and USD 2.80 in retail stores.

- Lettuce shows a marginal price difference, with USD 1.99 per pound at farmers’ markets and USD 2.00 in retail stores.

- Summer squash is USD 3.00 per pound at farmers’ markets, whereas it is significantly higher at retail stores, priced at USD 4.49.

- Tomatoes are USD 4.38 per pound at farmers’ markets and USD 5.98 in retail stores.

Demographics of Organic Packaged Food Consumers

By Age

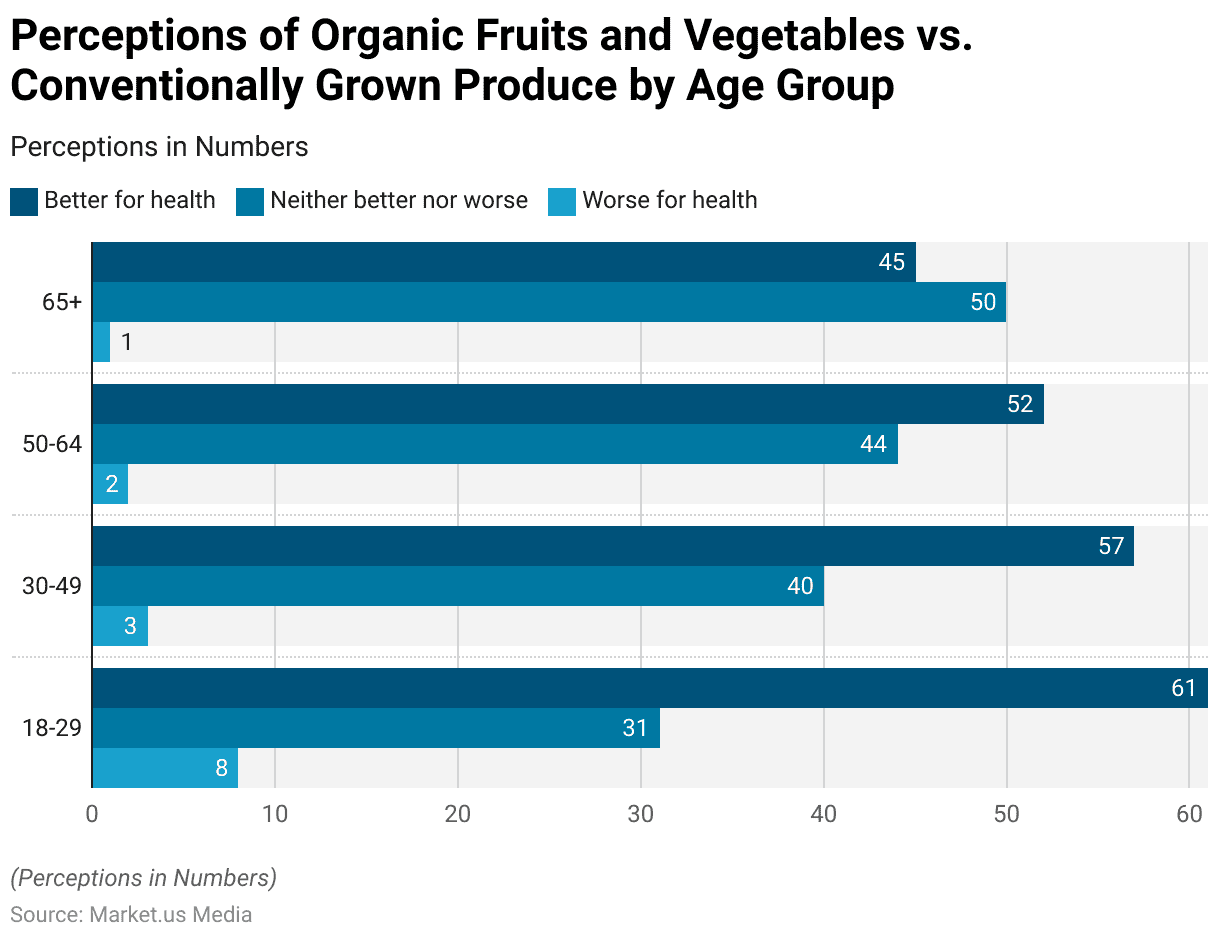

- A survey on the perceptions of organic fruits and vegetables compared to conventionally grown produce among U.S. adults reveals significant age-based differences.

- Among the 18-29 age group, 61% believe organic produce is better for health, while 31% see no difference, and 8% consider it worse.

- In the 30-49 age group, 57% view organic as healthier, 40% perceive no difference, and 3% think it is worse.

- For those aged 50-64, 52% believe organic is better, 44% see no difference, and 2% consider it worse.

- Among adults aged 65 and older, 45% think organic produce is better for health, 50% see no difference, and 1% believe it is worse.

By Gender

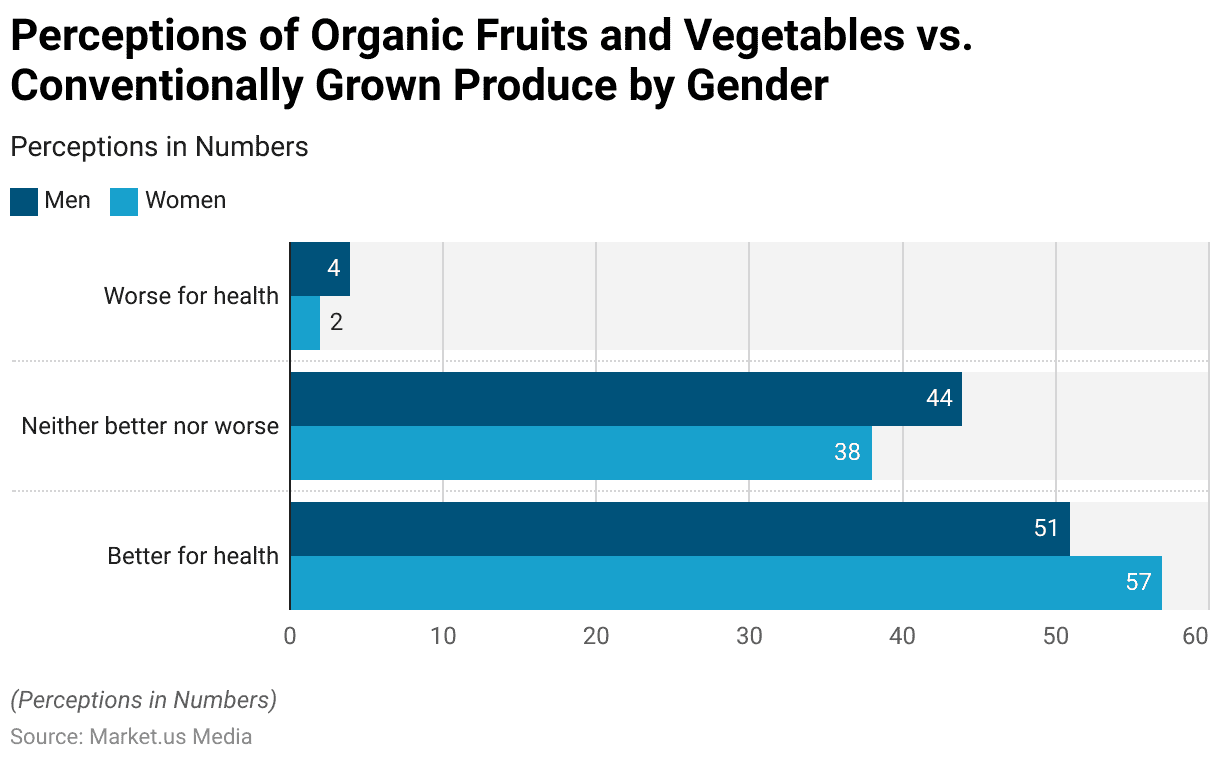

- A survey examining the perceptions of organic fruits and vegetables versus conventionally grown produce among U.S. adults highlights gender differences in views.

- Among men, 51% believe organic produce is better for health, 44% think there is no difference, and 4% consider it worse for health.

- In contrast, 57% of women view organic produce as healthier, 38% see no difference, and 2% believe it is worse for health.

Consumer Behaviour and Perceptions

- The majority of Americans are opting for organic foods due to health concerns, with 55% believing organic fruits and vegetables are superior for one’s well-being.

- Additionally, 76% of those who purchased organic foods recently did so for health reasons.

- However, only 32% think organic produce tastes better than conventionally grown ones, while 59% believe they taste the same.

- Other motivations for buying organic, such as environmental benefits or convenience, are less prevalent, with 33% and 22%, respectively, citing these factors.

- While a majority of Americans (59%) believe organic produce tastes similar to conventionally grown produce, fewer individuals perceive a taste advantage for organic options.

- Among those who consume mostly or some organic foods, 51% believe organic produce tastes better, while 45% think it tastes about the same.

Challenges and Key Considerations

- Approximately 72% of American adults consider the price difference between organic and conventionally grown foods when deciding whether to purchase organic.

- Even regular organic consumers demonstrate cost sensitivity, with 65% of frequent consumers and 79% of less frequent consumers factoring in the comparative cost of organic foods when making purchasing decisions.

- Availability can influence organic food purchases, with 33% of Americans finding it very easy to locate organic options locally and an additional 48% stating they are easy to find.

- Conversely, 18% find organic foods hard to come by in their communities.

- Rural residents are less likely to find organic foods that are very easy to locate compared to urban and suburban dwellers.

Regulations for Organic Packaged Food in Various Nations

- Regulations for organic packaged food vary significantly across different nations, reflecting diverse standards and consumer expectations.

- In the United States, the USDA’s National Organic Program (NOP) establishes comprehensive regulations, including production, handling, and labeling standards, with new rules enhancing animal welfare practices for organic livestock and poultry.

- In Europe, the EU Organic Regulation sets strict guidelines for organic production, covering everything from farming practices to food processing and labeling, aimed at ensuring consistency across member states.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)