Table of Contents

Overview

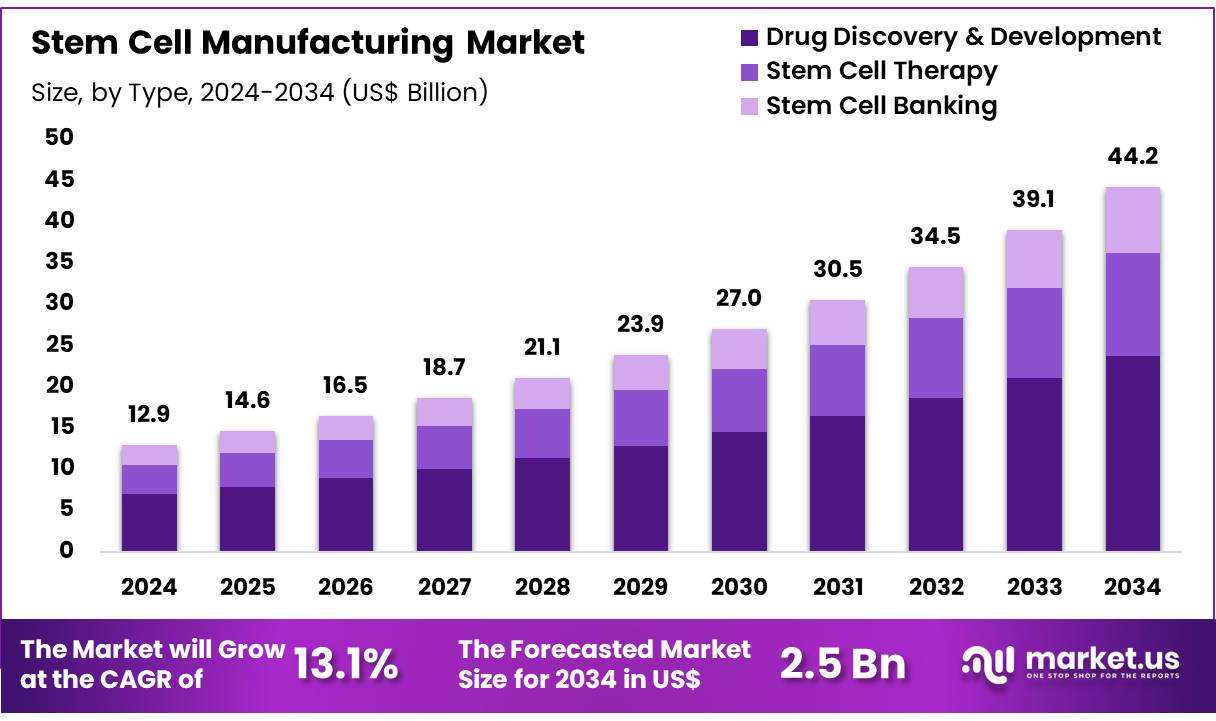

New York, NY – Oct 30, 2025 – Global Stem Cell Manufacturing Market size is expected to be worth around US$ 44.2 Billion by 2034 from US$ 12.9 Billion in 2024, growing at a CAGR of 13.1% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 39.5% share with a revenue of US$ 5.1 Billion.

The advancement of stem cell manufacturing is being recognized as a pivotal step in modern biomedical innovation. A significant development has been observed in scalable, high-quality stem cell production, which continues to drive progress in regenerative medicine, drug discovery, and personalized therapies. As healthcare systems increasingly adopt cell-based treatment approaches, robust and standardized manufacturing solutions have become essential.

Recent initiatives have focused on improving process efficiency, reducing production variability, and accelerating regulatory compliance. Automated bioprocessing platforms, advanced bioreactors, and refined quality control systems have been implemented to ensure consistent stem cell expansion and differentiation. As a result, the reliability and commercial viability of stem cell products have been strengthened.

Market demand has been rising as clinical applications expand, particularly in neurology, cardiology, orthopedics, and rare disease treatment. The growth of the market can be attributed to increasing research funding, strategic partnerships across biotech and pharmaceutical sectors, and technological improvements enabling large-scale production. Government support and rising investments from private institutions have further encouraged rapid adoption of stem cell technologies in therapeutic programs and research pipelines.

Manufacturing facilities are being strategically enhanced to meet global regulatory standards, ensuring safety, traceability, and efficiency throughout production workflows. Collaboration between academic institutions, biotechnology companies, and industry regulators continues to support forward-looking approaches in stem cell production.

This breakthrough reflects a significant milestone toward enabling broader clinical accessibility to stem cell-based therapies, ultimately contributing to improved patient outcomes and accelerating innovation in regenerative medicine.

Key Takeaways

- In 2024, the stem cell manufacturing market was valued at US$ 12.9 billion. The market is projected to expand at a compound annual growth rate (CAGR) of 13.1%, reaching an estimated value of US$ 44.2 billion by 2034.

- Based on type, the market is categorized into products and services. Services emerged as the leading category in 2024, accounting for 64.5% of total revenue.

- In terms of application, the industry is segmented into drug discovery and development, stem cell therapy, and stem cell banking. Drug discovery and development represented the largest share, comprising 53.8% of the global market in 2024.

- With respect to end users, the market is classified into pharmaceutical and biotechnology companies & contract research organizations (CROs), cell banks and tissue banks, and academic and research institutes. The pharmaceutical and biotechnology companies & CRO segment dominated the market, contributing 57.2% of total revenue in 2024.

- Regionally, North America maintained a leading position in the global stem cell manufacturing industry, capturing a market share of 39.5% in 2024.

Segmentation Analysis

Type Analysis: In 2023, the services segment commanded a dominant share of 64.5%, driven by increasing demand for specialized capabilities such as cell culture processing, cryopreservation, and rigorous quality control. The complexity of stem cell production, combined with the need for strict GMP standards and sterile environments, is encouraging biopharmaceutical developers to outsource manufacturing activities to expert service providers.

As stem cell therapies continue advancing from research phases into clinical and commercial deployment, the requirement for scalable, standardized, and regulatory-compliant manufacturing services is anticipated to expand significantly.

Application Analysis: The drug discovery and development segment represented 53.8% of the market in 2023, supported by the rising adoption of stem cells for disease modeling, toxicity screening, and target validation. Stem-cell-based platforms enable more accurate human-relevant biological assessments, improving precision in pharmaceutical R&D.

With growing interest in personalized medicine and increasing preference for predictive, human-derived data in regulatory frameworks, demand for stem cell-enabled research tools is expected to accelerate over the coming years.

End-User Analysis: Pharmaceutical and biotechnology companies accounted for the largest share at 57.2% in 2023, reflecting their expanding reliance on stem cells for drug development, regenerative therapies, and tissue engineering programs. These organizations continue investing in advanced cell production systems and infrastructure to support clinical-grade manufacturing.

As therapeutic pipelines targeting chronic and genetic diseases expand and regulatory systems evolve to support cell-based innovations, this end-user segment is projected to maintain its leadership position throughout the forecast period.

Regional Analysis

North America accounted for the largest revenue share of 39.5% in 2024, driven by advancements in regenerative medicine, rising adoption of stem cell-based therapies, and substantial investments in biotechnology. The region’s strategic focus on developing innovative treatments for chronic and degenerative diseases has strengthened the role of stem cell technologies in addressing conditions such as heart failure, diabetes, and neurological disorders.

A study published in January 2024 in the Journal of the American Heart Association indicated a global rise in heart failure cases, reaching 56.19 million patients. This increasing disease burden has heightened interest in stem cell-based cardiac therapies, particularly for tissue repair and cardiac regeneration.

Growing government funding and expanding private sector investments are fostering innovation across the region. Companies in North America are prioritizing advanced bioprocessing, automation, and scalable manufacturing platforms to support the rising demand for clinical-grade stem cell products. Supportive regulatory frameworks and a strong emphasis on personalized medicine are expected to further reinforce growth prospects in the region.

The Asia Pacific market is projected to register the fastest CAGR during the forecast period. The growth can be attributed to increasing investment in biotechnology, expanding stem cell research programs, and rising demand for advanced healthcare solutions. China, Japan, and South Korea are anticipated to witness significant progress in stem cell therapy development as healthcare systems modernize and prioritize regenerative medicine.

In December 2023, Fujifilm announced an investment of US$ 200 million to expand its global cell therapy development and manufacturing capabilities, underscoring the region’s strategic commitment to cell-based therapeutics. Supportive government initiatives, expanding biopharmaceutical infrastructure, and increasing prevalence of chronic diseases are expected to further accelerate the adoption of scalable stem cell manufacturing technologies across Asia Pacific.

Frequently Asked Questions on Stem Cell Manufacturing Market

- Why is stem cell manufacturing important?

Stem cell manufacturing is essential because it enables the large-scale production of safe and reliable stem cells for regenerative medicine, disease modeling, and pharmaceutical testing. It supports advancements in personalized medicine and accelerates the development of novel therapeutic strategies. - What technologies are used in stem cell manufacturing?

Technologies include bioreactors, automated cell culture systems, cryopreservation tools, and quality-control platforms. These systems help maintain optimal growth conditions, reduce variability, and improve scalability, allowing consistent production of clinical-grade stem cells for therapeutic applications. - What quality standards are required?

Stem cell manufacturing follows Good Manufacturing Practices and strict regulatory guidelines to ensure cell safety, potency, and traceability. Comprehensive testing for sterility, identity, and viability is conducted to support clinical-grade quality and regulatory approvals worldwide. - What is driving growth in the stem cell manufacturing market?

Growth is supported by increasing adoption of regenerative medicine, expanding clinical trials, and rising investments in biotechnology. Demand for personalized therapies and innovative treatment solutions continues to accelerate spending on advanced manufacturing technologies worldwide. - Which segment dominates the stem cell manufacturing market?

Services represent the leading segment due to increasing outsourcing for stem cell processing, quality testing, and regulatory support. Organizations prefer specialized service providers to improve production efficiency, reduce costs, and accelerate product development activities. - Which applications hold the largest market share?

Drug discovery and development account for the largest share, driven by rising use of stem cells for screening, toxicity testing, and disease modeling. This trend supports pharmaceutical innovation and enhances success rates in early-stage drug research programs. - Which region leads the global market?

North America leads the market owing to advanced research infrastructure, strong regulatory support, and rising investments in cell-based therapies. High adoption of regenerative medicine and biomanufacturing technologies further strengthens regional market dominance.

Conclusion

The global stem cell manufacturing market is advancing rapidly, supported by technological innovation, expanding clinical applications, and strong investment momentum from pharmaceutical and biotechnology companies. Increasing adoption of regenerative therapies, rising demand for high-quality stem cell production, and regulatory progress are reinforcing long-term growth prospects.

North America remains the leading region, while Asia Pacific is positioned for the fastest expansion driven by research advancements and infrastructure development. As scalable and compliant production systems continue to evolve, the industry is expected to play a vital role in accelerating personalized medicine, improving treatment outcomes, and enabling broader access to next-generation cell-based therapies.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)