Table of Contents

Overview

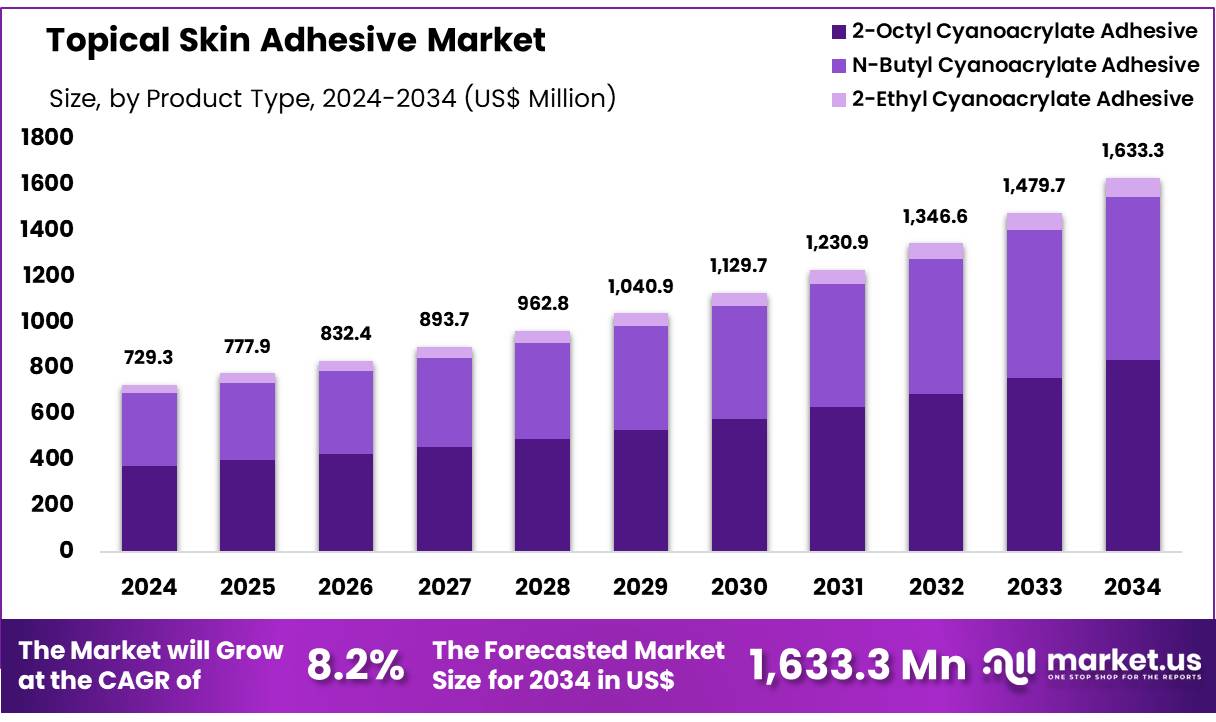

New York, NY – Nov 12, 2025 – Global Topical Skin Adhesive Market size is expected to be worth around US$ 1633.3 Million by 2034 from US$ 729.30 Million in 2024, growing at a CAGR of 8.2% during the forecast period from 2024 to 2034. In 2024, North America led the market, achieving over 42.20% share with a revenue of US$ 307.76 Million.

The introduction of the new Topical Skin Adhesive marks a significant advancement in wound closure technology. Designed for both medical professionals and patient use, this adhesive provides a non-invasive, efficient, and sterile alternative to conventional sutures and staples. The formulation is based on medical-grade cyanoacrylate, known for its superior bonding strength, biocompatibility, and fast polymerization upon contact with skin moisture.

The product offers instant skin closure, reducing procedure time and minimizing the risk of infection. Its flexible film forms a protective barrier that naturally sloughs off as the wound heals, eliminating the need for removal. This innovation supports enhanced patient comfort and improved aesthetic outcomes.

The global demand for topical skin adhesives has been driven by the increasing number of surgical procedures, a growing preference for minimally invasive treatments, and the rising incidence of traumatic injuries. The new product aligns with these trends, ensuring strong market potential across hospitals, clinics, and outpatient care settings.

The company remains committed to quality and innovation in advanced wound management solutions. With this launch, it aims to strengthen its position in the global medical adhesives market and contribute to safer, faster, and more effective wound healing outcomes.

Key Takeaways

- The Topical Skin Adhesive market was valued at US$ 729.30 million and is projected to reach US$ 1,633.25 million, registering a CAGR of 8.2% during the forecast period.

- By Product Type, the 2-Octyl Cyanoacrylate Adhesive segment dominated the market, accounting for a 51.3% share of total revenue.

- By End User, the Hospitals segment emerged as the leading contributor, representing 62.7% of the overall market share.

- By Application, the Surgical Incisions segment held the largest revenue share, contributing 37.3% to the market.

- By Distribution Channel, the Offline segment remained the major revenue generator, capturing 79.8% of the market share.

- Regionally, North America maintained its dominance in the global market, accounting for the largest share of 42.20%.

Segmentation Analysis

- Product Type Analysis: In 2023, N-2-Butyl-Cyanoacrylate Adhesive dominated the product type segment, accounting for over 51.3% of the market share. Its superior bonding strength, rapid healing properties, and effective infection control have positioned it as a preferred alternative to traditional sutures. The adhesive is extensively used in surgical, trauma, and dermatological procedures due to its flexibility, affordability, and patient-friendly application. Healthcare professionals favor this product for its improved cosmetic outcomes and non-invasive nature, which continue to support its widespread adoption across both emergency and routine medical practices.

- End-User Analysis: The hospitals segment held the largest share of the topical skin adhesive market in 2023. This dominance was attributed to the high volume of surgical procedures and trauma cases managed in hospital settings. Hospitals increasingly prefer topical skin adhesives for their ease of use, faster wound closure, and reduced infection risk compared to sutures. The rising number of outpatient surgeries and accident-related treatments further strengthened their adoption. With continuous advancements in healthcare infrastructure, hospitals are anticipated to remain the primary contributors to market demand in the coming years.

- Application Analysis: The surgical incisions segment led the application category in 2023, contributing over 37.3% of the total market share. Topical skin adhesives have become the standard choice for wound closure in hospitals and surgical centers, effectively replacing sutures in both major and minor procedures. Their quick bonding capability, reduced scarring, and convenience of use make them ideal for minimally invasive surgeries. The growing preference for efficient and aesthetically favorable wound management solutions is expected to sustain the demand for skin adhesives in surgical applications globally.

- Distribution Channel Analysis: The offline distribution channel remained dominant in 2023, supported by hospital pharmacies, retail medical outlets, and established supply networks. Healthcare providers rely on offline channels for verified product quality, regulatory assurance, and immediate accessibility. Bulk purchasing through contractual agreements with authorized distributors ensures consistent product availability. Although online platforms are gaining traction, offline distribution continues to lead due to strong supplier relationships and opportunities for in-person product demonstrations. This channel is expected to maintain its advantage as healthcare institutions prioritize reliability and prompt access to medical-grade adhesives.

Regional Analysis

North America holds a dominant position in the global topical skin adhesive market, driven by its advanced healthcare infrastructure, widespread adoption of innovative medical technologies, and the strong presence of major industry players. The region accounts for 42.20% of the global market share, with the United States leading in demand for advanced wound closure solutions. Prominent companies such as Johnson & Johnson (Ethicon) and Medtronic play a crucial role in driving product innovation and expanding the range of available solutions.

The region’s dominance is primarily attributed to the growing preference for minimally invasive surgical procedures, where topical skin adhesives are increasingly utilized as effective alternatives to traditional sutures and staples. The high number of surgical interventions, including cosmetic and trauma-related surgeries, further contributes to market growth.

Supportive regulatory frameworks from authorities such as the U.S. Food and Drug Administration (FDA) ensure the availability of safe, high-quality products, thereby strengthening consumer confidence and market expansion. The rising prevalence of chronic wounds, particularly among the elderly and diabetic populations, continues to drive the adoption of topical skin adhesives.

In addition, increasing awareness among healthcare professionals and patients regarding the benefits of these adhesives—such as reduced infection risks, faster healing, and improved cosmetic outcomes enhances market penetration. With continuous technological progress and higher healthcare spending, North America is expected to sustain its leadership in the topical skin adhesive market over the forecast period.

Frequently Asked Questions on Topical Skin Adhesive

- How does topical skin adhesive work?

The adhesive polymerizes quickly upon contact with skin moisture, forming a flexible film that bonds wound edges. It eliminates the need for sutures or staples and naturally sloughs off as the wound heals. - What are the main types of topical skin adhesives?

The primary types include 2-Octyl Cyanoacrylate and n-Butyl Cyanoacrylate. 2-Octyl is preferred for its flexibility and low toxicity, while n-Butyl is commonly used for general wound closure applications. - What are the key benefits of using topical skin adhesives?

These adhesives offer faster application, reduced pain, minimal scarring, and lower infection risks compared to traditional sutures. They are also ideal for pediatric, cosmetic, and minimally invasive surgical procedures. - Which segment leads the topical skin adhesive market by product type?

The 2-Octyl Cyanoacrylate Adhesive segment dominates the market, accounting for over half of global revenue due to its superior performance, strength, and biocompatibility in medical wound management applications. - Which end-user segment holds the largest market share?

The hospital segment leads the market, representing the highest revenue share. The extensive use of topical skin adhesives in surgical settings and trauma care drives their dominance in this category. - What are the major applications of topical skin adhesives?

These adhesives are widely used in surgical incisions, trauma wound closure, and cosmetic surgeries, providing strong and sterile closure solutions that enhance patient comfort and reduce postoperative complications. - Which region dominates the topical skin adhesive market?

North America remains the leading region, holding a 42.20% market share, supported by advanced healthcare infrastructure, high adoption of innovative technologies, and strong presence of key industry players. - Who are the key players in the topical skin adhesive market?

Major companies include Johnson & Johnson (Ethicon), Medtronic, Advanced Medical Solutions, and B. Braun Melsungen AG, all contributing to innovation, product expansion, and market competitiveness globally.

Conclusion

The global topical skin adhesive market is poised for substantial growth, driven by rising surgical volumes, technological advancements, and the growing preference for minimally invasive wound closure solutions. With a projected CAGR of 8.2%, the market is expected to reach USD 1.63 billion by 2034.

North America continues to lead due to its advanced healthcare infrastructure and strong industry presence. The increasing use of medical-grade cyanoacrylate adhesives in hospitals and surgical centers highlights their effectiveness, safety, and convenience. Continuous innovation, regulatory support, and expanding healthcare access are expected to sustain long-term market growth worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)