Table of Contents

Overview

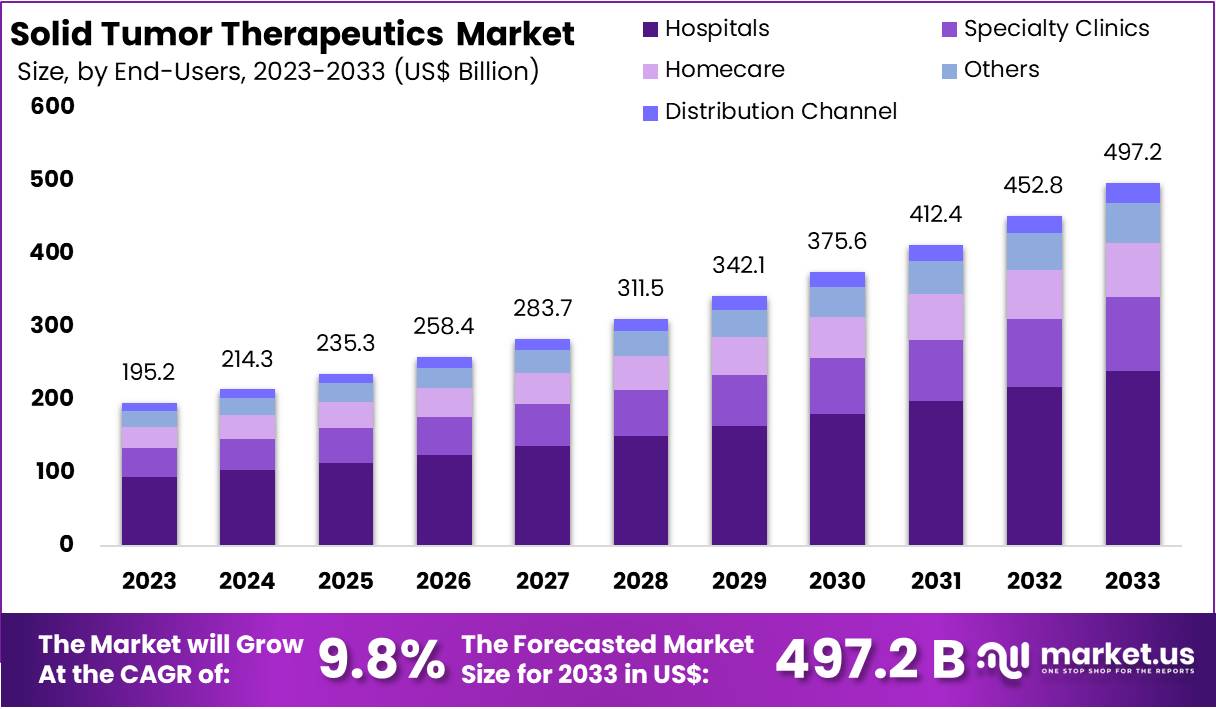

New York, NY – Feb 18, 2026 – The Global Solid Tumor Therapeutics Market size is expected to be worth around US$ 497.2 Billion by 2033, from US$ 195.2 Billion in 2023, growing at a CAGR of 9.8% during the forecast period from 2024 to 2033. North America maintained a leading market position, accounting for over 36% of the market share with a valuation of US$ 70.2 billion in the year.

A strategic foundation has been established for the advancement of solid tumor therapeutics, reflecting continued innovation in oncology research and precision medicine. Solid tumors, which account for nearly 90% of adult cancer diagnoses globally, remain a major area of unmet clinical need due to tumor heterogeneity, resistance mechanisms, and limited response rates to conventional therapies.

The newly structured initiative is focused on accelerating the development of targeted therapies, immuno-oncology platforms, and combination treatment strategies designed to improve patient outcomes across high-burden cancer indications, including lung, breast, colorectal, and pancreatic cancers. Research and development efforts are being aligned with biomarker-driven approaches to enhance treatment personalization and optimize therapeutic efficacy.

Strategic collaborations with academic institutions, biotechnology partners, and clinical research organizations are being implemented to strengthen translational research capabilities and expedite regulatory pathways. Advanced technologies, including next-generation sequencing and AI-enabled drug discovery platforms, are being integrated to streamline candidate identification and validation processes.

The global solid tumor therapeutics market is projected to witness sustained growth, supported by increasing cancer incidence, expanding clinical pipelines, and rising investment in oncology innovation. According to industry estimates, oncology remains one of the fastest-growing pharmaceutical segments, with immunotherapy and targeted therapy representing significant revenue contributors.

This foundational development underscores a long-term commitment to addressing critical treatment gaps, enhancing survival rates, and advancing next-generation oncology solutions in the evolving global healthcare landscape.

Key Takeaways

- The global solid tumor therapeutics market is anticipated to attain a valuation of US$ 497.2 billion by 2033, expanding at a compound annual growth rate (CAGR) of 9.8% during the forecast period from 2024 to 2033.

- In 2023, chemotherapy represented the leading therapy segment, accounting for more than 28% of the overall market share, underscoring its continued significance in solid tumor treatment protocols.

- The oral route of administration emerged as the dominant segment in 2023, capturing over 38% of total market revenue, supported by improved patient adherence and enhanced convenience.

- Hospitals constituted the largest end-user segment in 2023, contributing more than 48% of the total market share, attributed to the availability of specialized oncology infrastructure and comprehensive treatment facilities.

- North America maintained a leading regional position in 2023, securing approximately 36% of the global market share and reaching a valuation of US$ 70.2 billion, supported by well-established healthcare systems and robust oncology research capabilities.

Regional Analysis

In 2023, North America maintained a dominant position in the solid tumor therapeutics market, accounting for over 36% of global revenue and reaching a valuation of US$ 70.2 billion. This leadership has been supported by a highly advanced healthcare infrastructure and sustained investment in oncology research and development. Early access to innovative cancer therapies has strengthened treatment adoption rates and reinforced regional market growth.

Significant public and private funding, combined with strong patient awareness regarding available cancer treatments, has contributed to a favorable market environment. The presence of globally recognized cancer research institutions has accelerated the development and clinical integration of novel therapeutic solutions, supporting continuous advancements in solid tumor management.

A well-defined regulatory framework, particularly through the U.S. Food and Drug Administration (FDA), has enabled efficient drug approvals and timely commercialization. However, rising treatment costs and increasing competition from rapidly expanding regions such as Asia-Pacific may present challenges. Sustained innovation and improved affordability will remain critical to preserving North America’s market leadership.

Emerging Trends

- Tissue-Agnostic Targeted Therapies: Regulatory approvals are increasingly based on genetic mutations rather than tumor origin. In July 2022, the FDA approved dabrafenib plus trametinib for advanced solid tumors harboring BRAF V600 mutations, marking a milestone in precision oncology.

- Adoption of Cell-Based Immunotherapies: Autologous tumor-infiltrating lymphocyte therapies have expanded into solid tumor treatment. In February 2024, lifileucel received accelerated approval for unresectable or metastatic melanoma, representing the first approved cellular immunotherapy specifically for solid tumor indications.

- Expansion of Antibody-Drug Conjugates (ADCs): Antibody-drug conjugates are gaining regulatory momentum in solid tumors with defined molecular targets. In April 2024, trastuzumab deruxtecan received accelerated approval for HER2-positive unresectable or metastatic solid tumors, reinforcing ADCs’ role in targeted oncology treatment.

- Kinase Inhibitors for Rare Gene Fusions: Targeted small-molecule inhibitors addressing rare gene fusions are increasingly prioritized. In June 2024, repotrectinib was approved for patients aged 12 years and older with NTRK fusion-positive solid tumors, emphasizing molecularly stratified therapeutic strategies.

- Integration of AI in Treatment Selection: Artificial intelligence tools are being integrated into oncology decision-making. In February 2025, researchers reported that the AI platform SCORPIO predicted checkpoint inhibitor responses more accurately than conventional biomarkers, supporting AI-driven personalization in immunotherapy selection.

Use Cases

- Tumor-Infiltrating Lymphocyte Therapy in Melanoma: A pivotal clinical trial supporting lifileucel approval included 82 adults with unresectable or metastatic melanoma. Objective response rates and durability outcomes were assessed within this defined cohort, demonstrating real-world applicability in advanced melanoma management.

- Cellular Immunotherapy in Metastatic Colorectal Cancer: In an early-phase study conducted by the National Cancer Institute, an experimental cellular immunotherapy reduced tumors in 3 of 7 patients with metastatic colon cancer, reflecting promising preliminary efficacy in solid tumor immunotherapy development.

Frequently Asked Questions on Solid Tumor Therapeutics

- What types of cancers are classified as solid tumors?

Solid tumors include malignancies that form compact masses in organs or tissues, excluding blood-related cancers. Common examples include breast cancer, lung cancer, colorectal cancer, prostate cancer, liver cancer, and pancreatic cancer, among others. - What are the primary treatment modalities used for solid tumors?

Treatment approaches typically involve a combination of surgery, chemotherapy, radiation therapy, targeted therapy, hormone therapy, and immunotherapy. The selection depends on tumor stage, genetic profile, patient health status, and overall treatment objectives. - How does immunotherapy work in treating solid tumors?

Immunotherapy enhances the body’s immune system to recognize and eliminate cancer cells. Mechanisms include immune checkpoint inhibitors, CAR-T cell therapy, and cancer vaccines, which improve immune response specificity and reduce tumor immune evasion. - What role does precision medicine play in solid tumor treatment?

Precision medicine utilizes genetic profiling and biomarker testing to identify specific mutations driving tumor growth. This enables the selection of targeted therapies, improving treatment efficacy, minimizing adverse effects, and supporting personalized patient care strategies. - Which therapeutic segment dominates the market?

Immunotherapy and targeted therapy segments currently account for a significant revenue share due to high clinical efficacy and favorable reimbursement frameworks. However, chemotherapy continues to maintain substantial utilization, particularly in emerging healthcare markets. - Which regions lead the solid tumor therapeutics market?

North America leads the market due to advanced healthcare infrastructure, strong pharmaceutical presence, and high R&D expenditure. Europe follows closely, while Asia-Pacific is expected to witness the fastest growth owing to rising healthcare investments. - What future trends are expected in the solid tumor therapeutics market?

Future trends include increasing adoption of combination therapies, expansion of biosimilars, integration of artificial intelligence in drug discovery, and growing emphasis on personalized medicine, which collectively are expected to strengthen long-term market growth.

Conclusion

The solid tumor therapeutics market is positioned for sustained expansion, supported by continuous innovation in precision medicine, immuno-oncology, and biomarker-driven treatment strategies. With the market projected to reach US$ 497.2 billion by 2033 at a CAGR of 9.8%, significant opportunities are emerging across targeted therapies, cell-based immunotherapies, and antibody-drug conjugates.

North America maintains regional leadership, while technological integration, including AI-enabled platforms, is reshaping clinical decision-making. Despite cost and access challenges, strong research pipelines, strategic collaborations, and regulatory advancements are expected to enhance treatment outcomes and reinforce long-term growth across the global oncology landscape.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)