Table of Contents

Introduction

According to Frozen Food Statistics, The frozen food industry, a vital segment of the food and beverage sector, offers an extensive range of products like fruits, vegetables, meats, and prepared meals, appealing to consumers seeking convenience and variety.

Market growth is fueled by trends favoring convenience, health consciousness, and product innovation. Key players like Nestlé, Conagra, and General Mills compete fiercely, emphasizing factors such as quality, innovation, and distribution.

Regulatory bodies enforce strict standards to ensure product safety and quality. Despite challenges, the industry is poised for growth, driven by evolving consumer preferences and technological advancements, demanding ongoing attention to health, sustainability, and quality.

Editor’s Choice

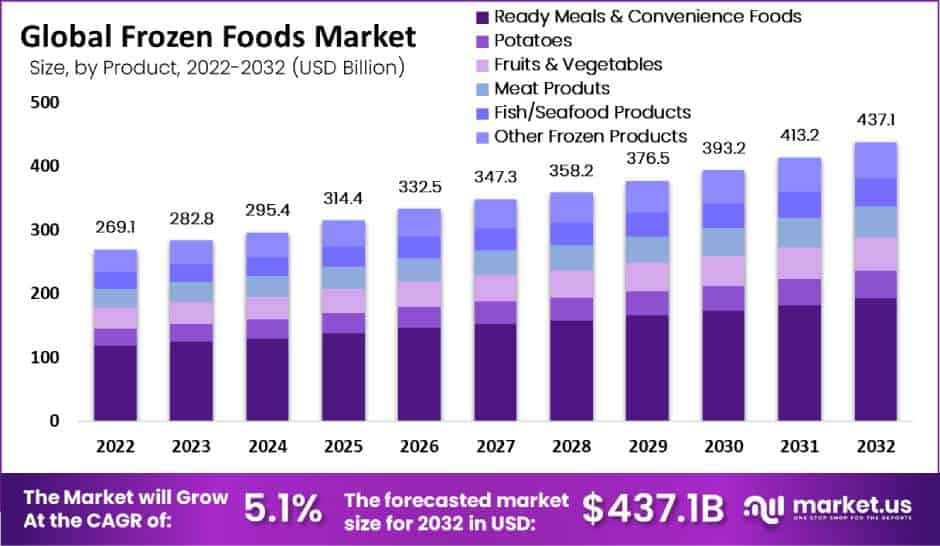

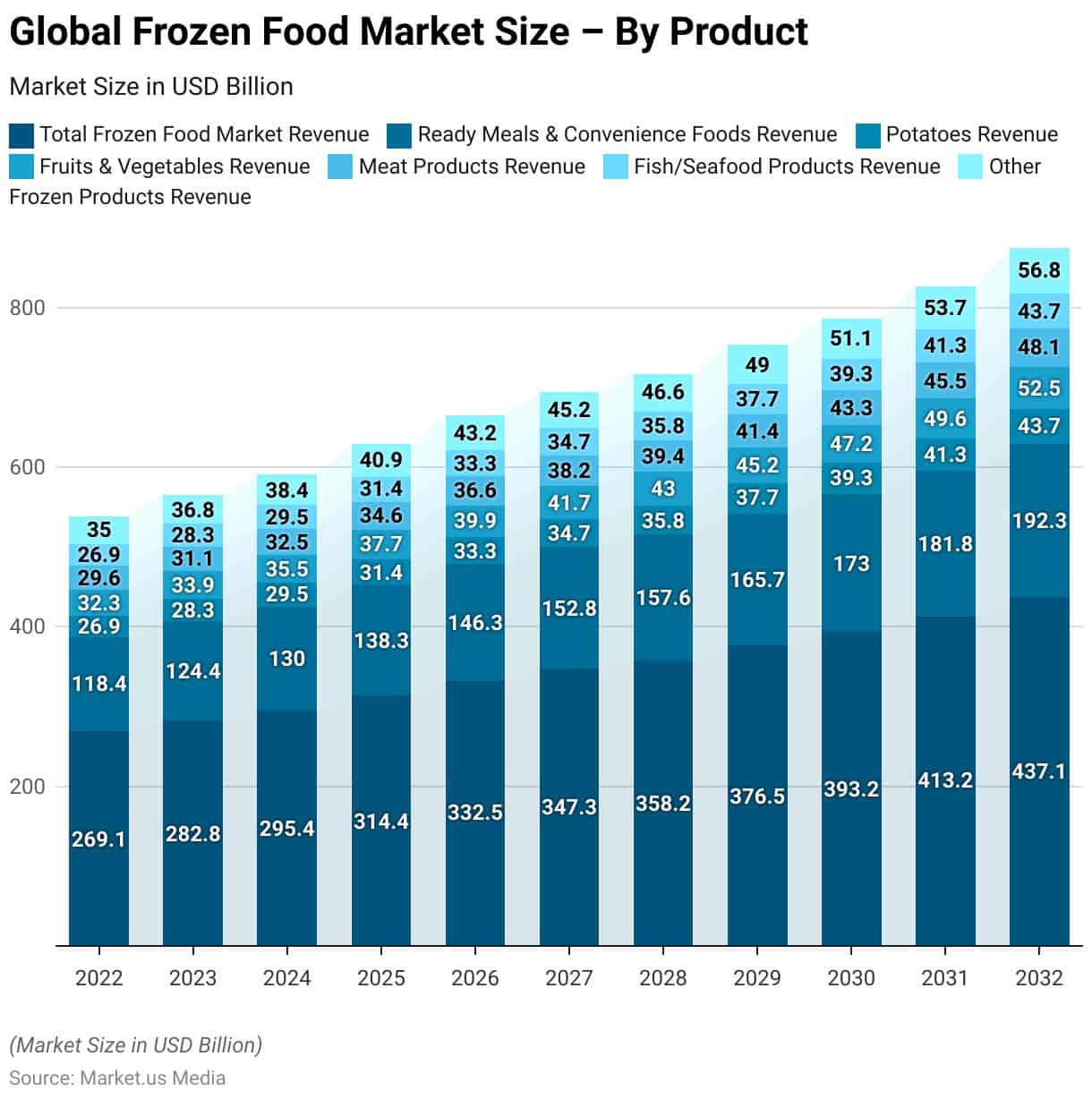

- The global frozen food market has been witnessing steady growth over the past decade, with revenues increasing from 269.1 billion USD in 2022 to 437.1 billion USD in 2032.

- In 2022, ready meals and convenience foods revenue accounted for 118.40 billion USD, followed by potatoes at 26.91 billion USD, and fruits and vegetables at 32.29 billion USD.

- India leads the exporters pack with a substantial volume of shipments, totaling 244,817 units, reflecting its significant presence in the food export sector.

- Topping the importer list is the United States, with a significant volume of shipments totaling 177,394 units, reflecting its vast consumer market and appetite for frozen goods.

- While the majority of frozen food buyers (83%) still regard frozen options as a backup choice, dedicated consumers tend to purchase with specific meals in mind.

- Online sales of frozen foods saw a notable increase in 2020, with 51% of shoppers having bought groceries online and 82% of them purchasing food.

- When considering the reasons consumers opt for frozen food products, several factors emerge as significant influencers. Foremost among these is the convenience offered by frozen meals, with 14% of respondents ranking it as their primary motive.

Frozen Food Market Overview

Frozen Food Market Size

- The global frozen food market has been witnessing steady growth over the past decade, with revenues increasing from 269.1 billion USD in 2022 to 437.1 billion USD in 2032.

- This growth trajectory reflects a compound annual growth rate (CAGR) of 5.1%, indicative of the market’s resilience and evolving consumer preferences.

- In 2023, the revenue climbed to 282.8 billion USD, marking a notable uptick from the previous year.

- Notably, the years ahead forecast continued growth, with projections estimating revenues to soar to 413.2 billion USD by 2031 and 437.1 billion USD by 2032.

Global Frozen Food Market Size – By Product

- In 2022, the total market revenue stood at 269.1 billion USD, with ready meals and convenience foods accounting for 118.40 billion USD, followed by potatoes at 26.91 billion USD, and fruits and vegetables at 32.29 billion USD.

- Meat products generated revenue of 29.60 billion USD, while fish/seafood products and other frozen products contributed 26.91 billion USD and 34.98 billion USD, respectively.

- Over the subsequent years, the market witnessed consistent expansion, with revenues reaching 437.1 billion USD in 2032.

- Ready meals and convenience foods remained the largest segment, with revenue climbing to 192.32 billion USD, followed by potatoes, fruits and vegetables, meat products, fish/seafood products, and other frozen products.

Frozen Food Market Share – By Distribution Channel

- In the distribution landscape of the frozen food market, offline channels dominate with an impressive market share of 88%.

- However, online channels have been steadily gaining traction, capturing a noteworthy 12% market share.

Global Frozen Food Trade Statistics

- According to Volza’s Global Import data, the worldwide import of frozen food under HSN Code 1905 amounted to 50.7 thousand shipments, facilitated by 691 importers from 443 suppliers.

- The primary sources for these imports are India, Italy, and Pakistan.

- The United States leads as the largest importer, receiving 36,163 shipments, followed by Australia with 4,440 shipments and Canada with 4,403 shipments.

- The top three categories within the frozen food and HSN Code 1905 imports include HSN Code 19059090, HSN Code 19059030, and HSN Code 190590.

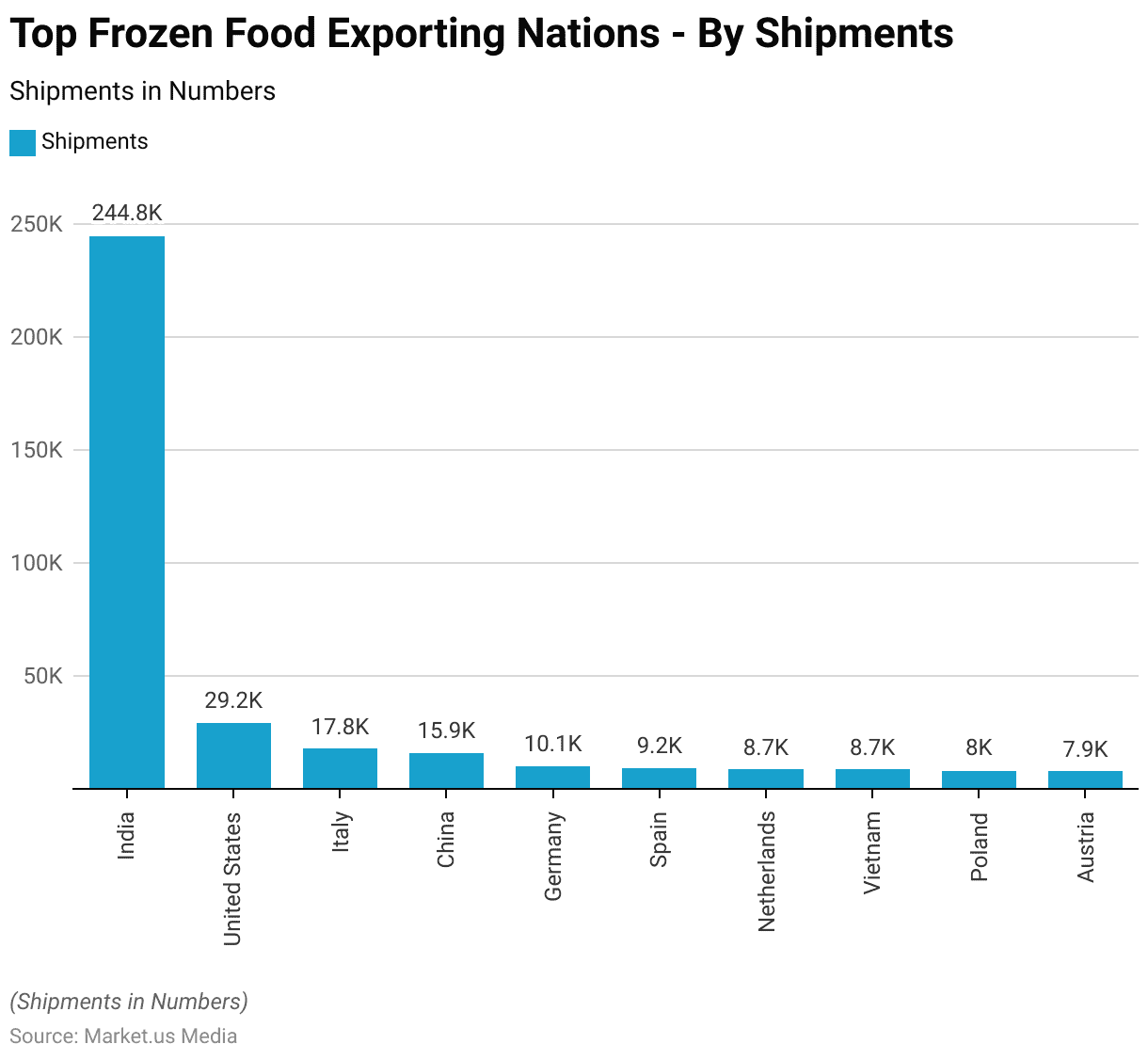

Top Frozen Food Exporting Countries

- The top frozen food exporting countries showcase a diverse range of global contributors to this lucrative market.

- India leads the pack with a substantial volume of shipments, totaling 244,817 units, reflecting its significant presence in the frozen food export sector.

- Following India, the United States stands out with 29,193 shipments, leveraging its advanced food processing infrastructure and quality standards.

- Italy and China also play pivotal roles, with 17,788 and 15,905 shipments, respectively, highlighting their culinary heritage and manufacturing prowess.

- Germany, Spain, and the Netherlands exhibit noteworthy performances with 10,086, 9,194, and 8,712 shipments, respectively, underscoring their position as key exporters.

- Vietnam, Poland, and Austria round out the top ten with impressive figures of 8,661, 7,958, and 7,900 shipments, demonstrating their growing influence in the global frozen food trade.

Top Frozen Food Importing Countries

- The top frozen food importing countries highlight the global demand for convenient and diverse food options.

- Topping the list is the United States, with a significant volume of shipments totaling 177,394 units, reflecting its vast consumer market and appetite for frozen goods.

- Australia and Vietnam follow closely behind, with 35,629 and 28,460 shipments, respectively, underscoring the international reach of the frozen food trade.

- The United Kingdom and the Netherlands also emerge as key importers, with 22,477 and 13,169 shipments, respectively, indicative of their diverse culinary landscapes and consumer preferences.

- Canada, New Zealand, Singapore, and the Philippines demonstrate substantial imports, with figures ranging from 11,467 to 7,527 shipments, highlighting their participation in the global food market.

- Germany rounds out the top ten with 7,217 shipments, emphasizing Europe’s significant role in the importation of frozen food products.

Frozen Food Purchase Preferences

- While the majority of frozen food buyers (83%) still regard frozen options as a backup choice, dedicated consumers tend to purchase with specific meals in mind. Frozen foods are valued for their affordability and the convenience of fewer grocery trips.

- Preferences for brands vary by product, with national brands slightly preferred (23%) over private labels (17%).

- In 2020, manufacturer brands accounted for 77.1% of dollar sales, experiencing a growth of 16.9% ($7.3 billion), while private labels grew by 22.8% ($2.8 billion).

- The proportion of sales attributed to promotions decreased from 30.2% in 2019 to 23.7% in 2020 due to reduced merchandising during the pandemic.

- Frozen food buyers express interest in more resealable packaging (38%), various pack sizes (31%), and environmentally friendly packaging (28%).

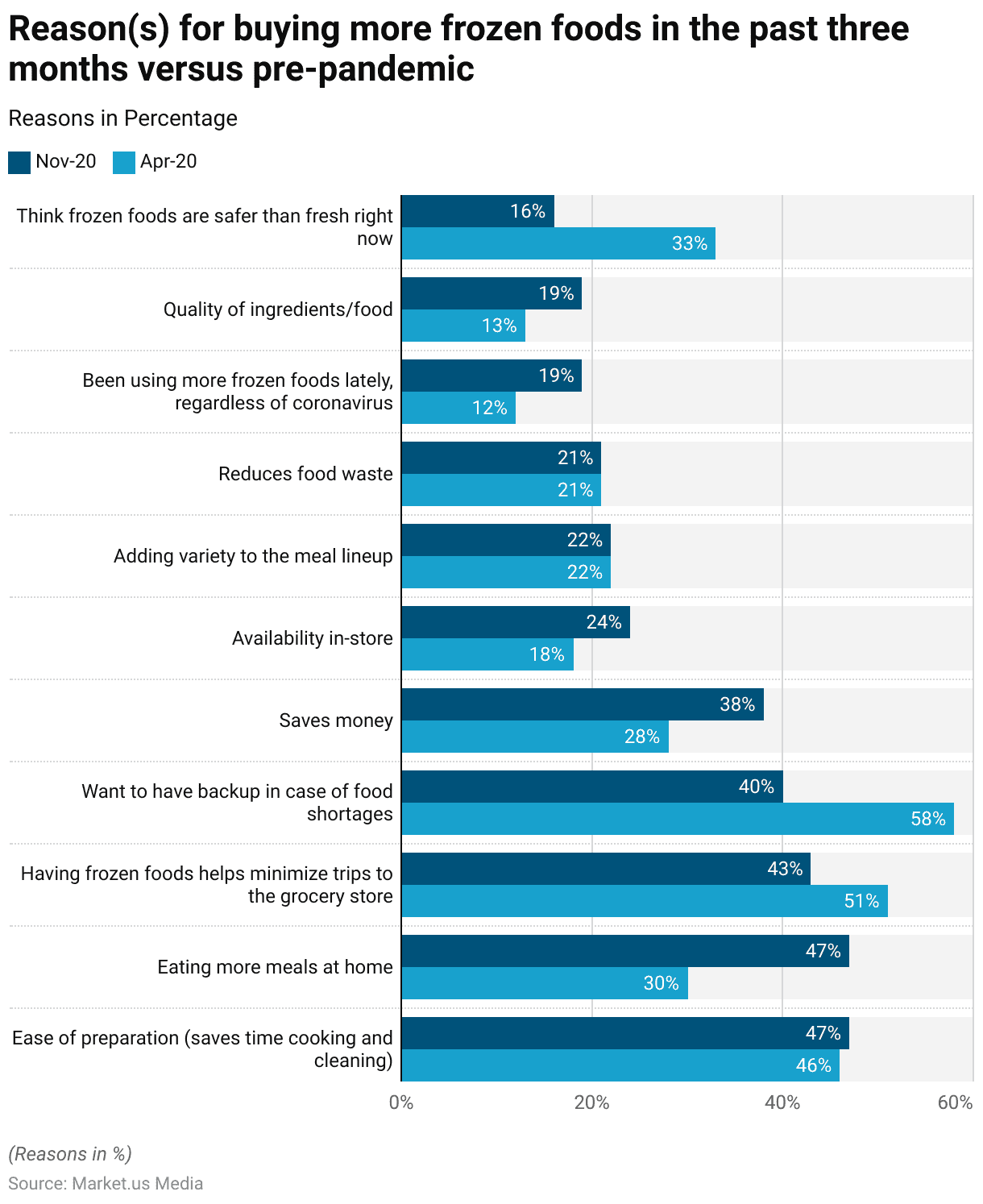

Buying Preferences During the COVID-19 Pandemic

- In the past three months, compared to pre-pandemic times, there has been an increase in the purchase of frozen foods for several reasons.

- Notably, 47% of consumers cite the ease of preparation, which saves time on cooking and cleaning, as a primary motivator. Similarly, 47% report eating more meals at home, driving the demand for convenient food options.

- Additionally, 43% find that having food on hand helps minimize trips to the grocery store, aligning with efforts to reduce exposure to public spaces.

- Other factors contributing to the rise in frozen food purchases include the desire to have a backup in case of food shortages (40%), the perceived cost savings (38%), and the availability of a variety of options in-store (24%).

- Furthermore, 22% of consumers appreciate the ability to add variety to their meal lineup, while 21% value the reduction of food waste.

- Despite these increases, some consumers (19%) indicate that they have been using more frozen foods lately, regardless of the pandemic, suggesting a broader shift in consumption habits.

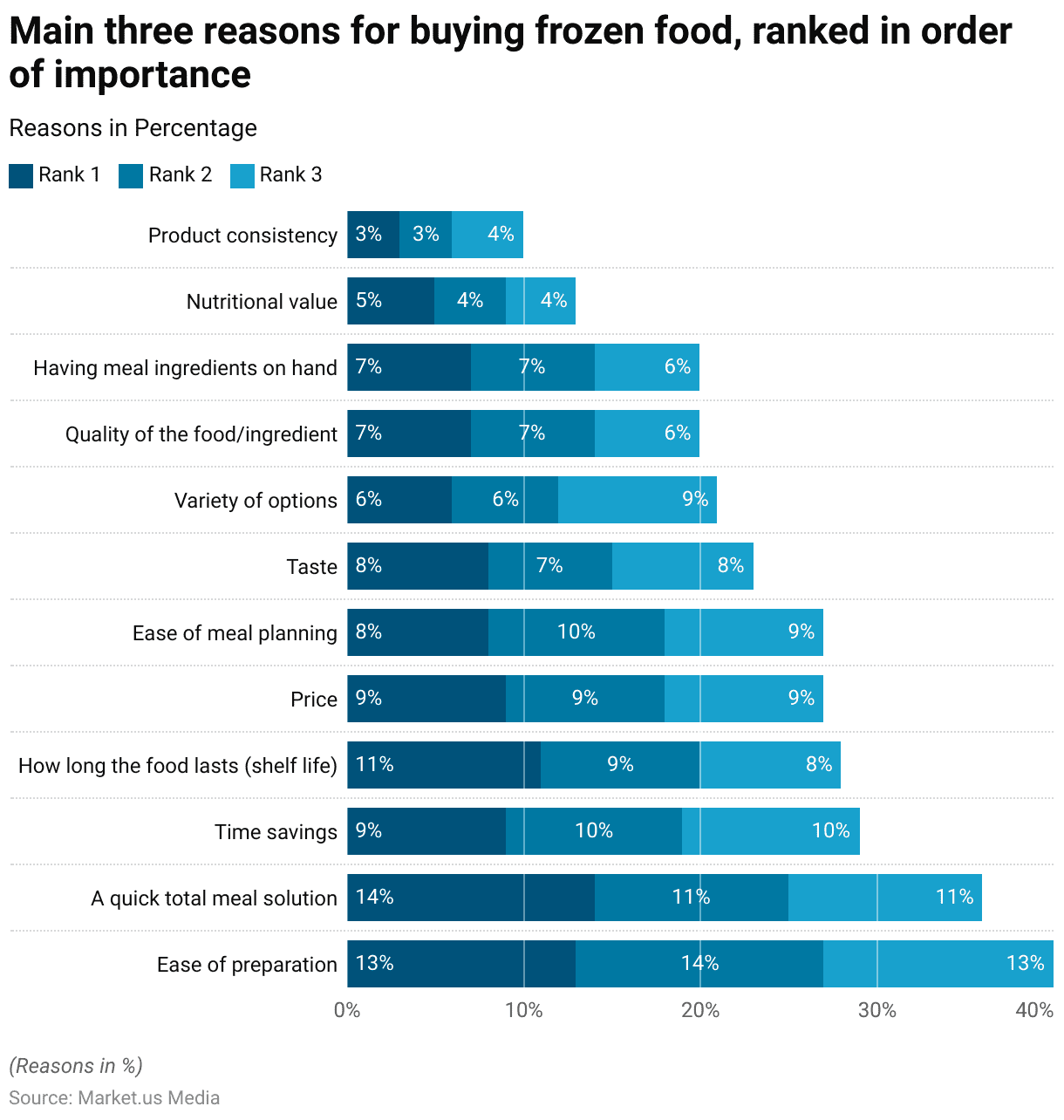

Reasons for Buying Frozen Food

- When considering the reasons consumers opt for frozen food products, several factors emerge as significant influencers. Foremost among these is the convenience offered by frozen meals, with 14% of respondents ranking it as their primary motive.

- This convenience encompasses ease of preparation (13%) and the ability to provide a quick total meal solution (14%), aligning closely with the modern lifestyle’s demand for efficiency and time-saving measures.

- Following closely behind, the aspect of time savings (9%) underscores the appeal of frozen foods in streamlining meal preparation processes, allowing individuals to balance busy schedules without sacrificing nutritional quality.

- Additionally, the longevity of frozen food items (11%) proves essential, addressing concerns about food wastage and ensuring a reliable supply of meal ingredients over time.

- While price (9%) and ease of meal planning (8%) also play significant roles, taste (8%) and variety of options (6%) contribute to enhancing the overall appeal of frozen food products, satisfying consumers’ diverse preferences and culinary interests.

- Moreover, considerations of quality (7%), nutritional value (5%), and product consistency (3%) underscore consumers’ expectations for high standards in their food choices, indicating a growing emphasis on health-consciousness and satisfaction with product performance.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)