Table of Contents

Overview

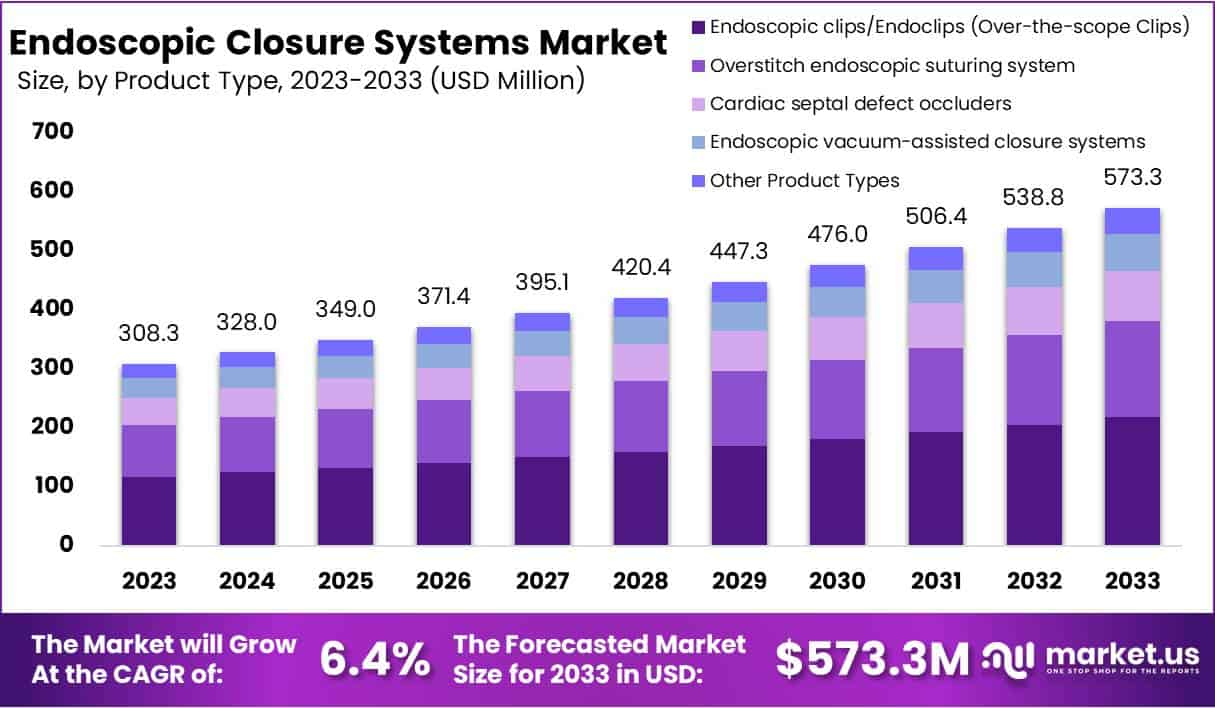

The Global Endoscopic Closure Systems Market is projected to reach USD 573.3 million by 2033, rising from USD 308.3 million in 2023 at a CAGR of 6.4% between 2024 and 2033. Growth in this sector is being driven by the increasing adoption of minimally invasive surgical procedures. Healthcare providers are shifting from traditional open surgeries to endoscopic methods that offer faster recovery, reduced postoperative pain, and shorter hospital stays. These systems are increasingly being used to manage gastrointestinal (GI) leaks, perforations, and fistulas, particularly in gastroenterology and bariatric surgeries.

Technological advancements have played a vital role in expanding the use of endoscopic closure systems. Innovations such as over-the-scope clips (OTSCs), suturing devices, and tissue approximation systems have enhanced procedural precision and patient safety. Companies are focusing on improving ergonomics, developing robotic-assisted endoscopy platforms, and using advanced biomaterials. These innovations are broadening clinical applications and improving efficiency, positioning endoscopic closure systems as an essential tool in minimally invasive medicine.

The market is further strengthened by the rising prevalence of gastrointestinal and bariatric disorders worldwide. The growing incidence of obesity, ulcers, and GI perforations has increased the number of related surgical and endoscopic interventions. Procedures such as endoscopic sleeve gastroplasty are becoming more common, creating higher demand for reliable closure devices. In addition, the expanding geriatric population, which is more prone to GI disorders, is driving consistent demand for diagnostic and therapeutic endoscopy.

Improving healthcare infrastructure and expenditure across developing economies are expanding market opportunities. Hospitals and ambulatory surgical centers (ASCs) are investing in advanced endoscopic systems, supported by better access to technology and increasing healthcare budgets. Positive clinical evidence has also accelerated market adoption. Numerous studies confirm the efficacy and safety of endoscopic closure systems compared to traditional surgical techniques, leading to greater confidence among clinicians and favorable reimbursement scenarios.

Favorable regulatory and industry developments are also shaping market growth. Streamlined approval pathways such as the U.S. FDA 510(k) and CE Mark in Europe are supporting quicker market entry for new devices. Strategic collaborations, mergers, and acquisitions are enabling leading players to expand their product portfolios and strengthen global distribution networks. Overall, the combination of technological innovation, expanding clinical use, and supportive policies is expected to sustain steady growth in the global endoscopic closure systems market through 2033.

Key Takeaways

- The global market is projected to reach USD 573.3 million by 2033, expanding at a compound annual growth rate of 6.4% from 2024 to 2033.

- Endoscopic clips dominated the market with over 38% share in 2023, attributed to their high versatility, reliability, and clinical effectiveness in procedures.

- Hospitals accounted for more than 56% of the market share in 2023, supported by extensive adoption of advanced endoscopic procedures and treatment technologies.

- Gastrointestinal diseases, affecting over 4.4 million people annually, significantly drive the demand for minimally invasive endoscopic closure systems and therapeutic interventions.

- The high cost of endoscopic procedures and specialized equipment remains a major barrier to market growth, particularly in low-resource healthcare settings.

- Technological advancements, including magnetic-assisted systems, are enhancing the precision and efficiency of endoscopic procedures, leading to improved patient outcomes and recovery.

- With over 80% of surgeries in the United States now minimally invasive, the rising preference continues to strengthen the demand for closure system solutions.

- North America leads the global market with a 37.8% share in 2023, followed by strong growth in Europe and emerging opportunities in Asia-Pacific.

Regional Analysis

In 2023, North America dominated the Endoscopic Closure Systems Market, capturing over 37.8% of the global share, valued at USD 116.5 million. The strong market position is attributed to advanced healthcare infrastructure and the high adoption of minimally invasive surgeries. The presence of leading medical device manufacturers further supports market dominance. Rising cases of gastrointestinal diseases, obesity, and colorectal cancer continue to drive demand for endoscopic closure systems across hospitals and specialized clinics in the region.

Europe followed as the second-largest market, supported by a robust healthcare system and favorable reimbursement policies. The region’s aging population, prone to gastrointestinal disorders, has increased the need for endoscopic closure devices. Major players’ presence and ongoing clinical trials also contribute to steady growth. Technological advancements and collaborations between research institutions and manufacturers are further propelling market expansion. These factors ensure Europe remains a key contributor to global revenue during the forecast period.

The Asia-Pacific region is projected to experience the fastest growth rate during the forecast period. This is driven by improved healthcare infrastructure and rising healthcare expenditure. Growing awareness of minimally invasive procedures among patients and professionals supports demand. China, Japan, and India are leading this growth, with increasing government initiatives to combat gastrointestinal diseases. Meanwhile, Latin America and the Middle East & Africa show gradual growth. However, high device costs and a lack of skilled professionals continue to hinder rapid expansion in these regions.

Segmentation Analysis

Type Analysis

In 2023, the Endoscopic clips/Endoclips (Over-the-scope Clips) segment dominated the Endoscopic Closure Systems Market, holding over 38% share. This dominance is due to their broad use in treating gastrointestinal bleeds, perforations, and device placements. Their high safety, precision, and flexibility have made them vital in endoscopic procedures. Ongoing innovations aimed at enhancing accuracy, ease of use, and closure efficiency continue to boost adoption, as demand for minimally invasive treatments rises worldwide.

Market growth is also supported by increasing cases of gastrointestinal diseases and the shift toward less invasive procedures. Major manufacturers are investing in R&D to expand the clinical applications of endoscopic clips in gastroenterology, pulmonology, and urology. The focus on patient safety and reducing post-surgical complications strengthens their adoption. The ability of these devices to provide quick, reliable tissue closure without additional surgery underscores their importance in modern healthcare.

Application Analysis

In 2023, hospitals led the Endoscopic Closure Systems Market by capturing more than 56% share of the end-user segment. Their dominance stems from the large number of endoscopic procedures performed in these facilities. Hospitals are equipped with advanced technologies and skilled professionals, which support the efficient use of these systems in surgeries such as gastrointestinal and bariatric operations. The use of endoscopic closure systems enhances safety, reduces infection risks, and promotes faster recovery.

The growth of this segment is further supported by hospitals’ strategic focus on upgrading surgical capabilities. Many healthcare institutions are investing in advanced endoscopic devices and staff training to improve outcomes. This approach aligns with the broader healthcare trend toward enhancing patient safety and operational efficiency. The integration of innovative closure systems in hospitals reflects the rising preference for precision-driven, minimally invasive surgical care worldwide.

Key Players Analysis

The Endoscopic Closure Systems Market demonstrates a highly competitive environment marked by continuous innovation and product advancement. Established manufacturers and emerging firms are actively expanding their presence through technological developments and strategic collaborations. The growing adoption of minimally invasive procedures has intensified competition, compelling companies to enhance product efficiency and reliability. CooperSurgical Inc. has strengthened its market position through a broad portfolio, including over-the-scope clips and sutures, supported by a strong global distribution network and brand credibility within the healthcare device sector.

US Endoscopy exhibits remarkable expertise in the development of endoscopic closure devices. The company’s research-driven approach and focus on product innovation have allowed it to address specific clinical needs effectively. Its specialized design and technology integration enable improved procedural safety and operational performance. The company’s emphasis on user-friendly solutions enhances its adoption among healthcare professionals, establishing US Endoscopy as a significant competitor. Its commitment to innovation continues to drive growth and sustain its market relevance across diverse medical applications.

Life Partners Europe emphasizes the delivery of minimally invasive surgical solutions that enhance patient recovery and procedural outcomes. Its wide range of endoscopic closure products demonstrates versatility and adaptability across surgical applications. Strategic partnerships and collaborations have strengthened its presence in both developed and emerging markets. The company’s targeted market expansion initiatives contribute to a steady rise in its revenue base. Through ongoing research and strong distribution alliances, Life Partners Europe continues to build its market influence within the endoscopic closure systems landscape.

Ovesco Endoscopy AG holds a strong market position in Europe due to its comprehensive product range and innovation-led operations. The company’s endoscopic closure devices are recognized for quality and advanced engineering, reflecting high clinical performance standards. It continues to invest in technology development to enhance product precision and ease of use. Alongside key players such as Apollo Endosurgery Inc. and St. Jude Medical Inc. (Abbott), Ovesco contributes to shaping the competitive environment and driving innovation in the global endoscopic closure systems market.

Challenges

1. Case Selection Limits and Size Constraints

The success of endoscopic closure depends on defect size, tissue condition, and location. Small, fresh defects are easier to manage. Larger or fibrotic defects often exceed the safe range for standard through-the-scope clips. In such cases, advanced closure tools like over-the-scope clips (OTSC) or suturing devices are needed. However, these are not always practical due to size limits or access issues. Careful case selection is essential. Choosing the right device for each defect type can help avoid complications and improve procedural outcomes.

2. Operator Learning Curve

Endoscopic closure systems require skilled handling and practice. Advanced tools such as OTSC and suturing devices demand specific training. Without proper technique, success rates may fall. Learning these systems takes time and experience. Simulation-based programs and structured workshops are being introduced to improve training. These programs help new users gain confidence and consistency. As proficiency increases, complication rates drop, and clinical outcomes improve. Ongoing education and continuous skill development are vital for maintaining high-quality performance in complex closure procedures.

3. Device-Related Adverse Events and Malfunction Risks

Although rare, device-related issues can occur during endoscopic closure. Potential problems include tissue injury, clip entrapment, or incomplete closure. Reports from safety databases such as MAUDE highlight these risks. Most problems arise from improper technique or device malfunction. Careful use, routine inspection, and adherence to manufacturer guidelines reduce risks. Operators should be prepared to manage unexpected device failures. Training and vigilance are key to preventing harm and ensuring patient safety during advanced endoscopic procedures.

4. Reprocessing, Compatibility, and Workflow

Endoscopic closure systems can increase procedure complexity. Each device has specific requirements for scope diameter, channel size, and accessory compatibility. Setup time and reprocessing steps are longer compared to standard clipping. These factors can slow procedure turnover and add workload for staff. Proper workflow planning helps maintain efficiency. Using compatible accessories and following cleaning protocols are essential for safety. Streamlined processes and team coordination improve overall productivity while ensuring that equipment remains reliable and ready for use.

5. Evidence Gaps for Some Indications

Clinical evidence strongly supports endoscopic closure for acute iatrogenic perforations and certain bleeding conditions. However, not all indications are well studied. Comparative trials between devices are limited, and standardized treatment algorithms are still evolving. More data are needed to define optimal device selection for different clinical settings. Research should also explore long-term outcomes and cost-effectiveness. Ongoing studies and registries are expected to fill these gaps, guiding best practices and ensuring evidence-based use of closure technologies.

6. Cost and Reimbursement Variability

Advanced closure devices can reduce the need for surgery and shorten hospital stays. However, their costs are higher than standard clips. Both capital equipment and disposable components add financial burden. Reimbursement policies differ across payers and indications. Hospital outpatient departments and ambulatory surgery centers often face different coverage levels. Procedure shifts between these settings further affect cost structures. Institutions must balance clinical benefits against economic impact. Clear reimbursement guidelines and cost-efficiency data are needed to support broader adoption.

7. Patient Risk Profile

The risk of bleeding and perforation increases in older adults and those with comorbidities or anticoagulation therapy. These patients benefit most from reliable closure systems. However, complications can be more severe if closure fails. Device choice and technique must consider patient-specific factors such as tissue fragility and healing potential. Proper pre-procedure planning and post-procedure monitoring reduce risks. Personalized strategies help ensure safety and successful recovery in high-risk patient populations undergoing endoscopic interventions.

Opportunities

1. Guideline-Driven Expansion of Therapeutic Endoscopy

Professional bodies such as ESGE and AGA now recommend endoscopic closure for many iatrogenic perforations and selected esophageal defects. These endorsements are promoting the use of advanced closure tools in routine therapeutic procedures. The ability to perform resections and manage leaks without open surgery supports greater adoption of these systems. As more complex endoscopic resections stay within the endoscopy suite, hospitals and ambulatory centers can rely on minimally invasive closure devices. This guideline-driven expansion is expected to accelerate the integration of suturing and clipping systems into advanced GI practices.

2. Prophylactic Defect Closure to Reduce Post-Resection Bleeding

Prophylactic closure following large EMR or ESD procedures has shown strong evidence in reducing delayed bleeding. This approach helps in lowering hospital readmissions and overall treatment costs. Recent studies have further validated these benefits, leading to broader use in both high-risk and moderate-risk patients. The growing emphasis on preventive endoscopy care encourages the standardization of closure techniques. With new data supporting these pathways, healthcare centers are increasingly adopting prophylactic closure devices as part of post-resection protocols. This trend enhances patient safety and ensures smoother recovery with fewer complications.

3. Shift of Procedures to Ambulatory Surgery Centers (ASCs)

The migration of gastrointestinal endoscopy procedures to Ambulatory Surgery Centers (ASCs) continues to accelerate. This shift increases the need for closure systems that are reliable, fast, and easy to use in outpatient settings. Efficient closure tools help avoid surgical transfers, keeping cases within the ASC environment. As payers and regulators favor outpatient care due to cost savings, ASCs demand technologies that support same-day discharge. Manufacturers focusing on simplified, quick-deployment closure devices can capture this growing market. The ASC trend is driving innovation toward compact, versatile, and time-efficient endoscopic closure solutions.

4. Rising Screening and Therapeutic Volumes

The updated USPSTF guidelines recommending colorectal cancer screening from age 45 have expanded the population eligible for endoscopic procedures. This increase in screenings naturally raises the volume of therapeutic interventions and associated complications. As more resections and polypectomies are performed, the need for closure tools to manage perforations and bleeding grows. Hospitals and endoscopy centers are investing in advanced closure systems to handle higher patient throughput safely. This rising procedural demand directly strengthens the market for endoscopic clips, suturing systems, and other closure technologies.

5. Regulatory Clarity and Platform Upgrades

The regulatory landscape for endoscopic closure systems has become more defined with multiple generations of FDA-cleared devices now available. Innovations such as the OverStitch Sx and NXT platforms demonstrate consistent usability improvements. Manufacturers are benefiting from a clearer path to product approval, reducing time-to-market. Incremental upgrades in design and functionality make these systems easier for clinicians to adopt. This evolution, coupled with established safety data, fosters confidence among end-users and healthcare administrators. Regulatory clarity supports ongoing platform development and encourages sustained investment in closure technology innovation.

6. Training Innovation

Training and skill development in endoscopic closure have seen major progress. Validated simulators and structured curricula are being introduced to reduce the learning curve for clinicians. These tools help standardize performance across hospitals and endoscopy centers, ensuring consistent outcomes. By integrating realistic simulation models, training programs make complex closure techniques more accessible. Institutions are prioritizing competency-based learning to improve proficiency and safety. This emphasis on training innovation accelerates adoption rates and builds confidence among practitioners performing advanced endoscopic procedures.

7. Broader Indications in Advanced Endoscopy

The scope of advanced endoscopy is widening with new therapeutic applications such as full-thickness resection, endoscopic bariatric therapy, and NOTES-adjacent techniques. These complex procedures require closure systems capable of secure, full-thickness apposition. As clinicians perform more challenging interventions endoscopically, the demand for durable closure tools increases. Device innovation focuses on strength, precision, and adaptability to different tissue types. The expanding range of indications positions endoscopic closure systems as essential tools for advanced gastrointestinal therapies. This trend is expected to drive significant market growth over the coming years.

Conclusion

The global endoscopic closure systems market is growing steadily due to the rising demand for minimally invasive surgeries and technological innovation. Continuous advancements in endoscopic tools, such as clips and suturing devices, have improved surgical precision and patient recovery. Increasing cases of gastrointestinal and bariatric disorders are driving adoption across hospitals and clinics worldwide. Supportive healthcare policies, improved infrastructure, and training programs are further enhancing accessibility and safety. With strong clinical outcomes, expanding applications, and growing investments from key players, the market is set to witness consistent progress. These systems are becoming vital for modern healthcare, ensuring safer and faster treatment outcomes.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)