Table of Contents

Overview

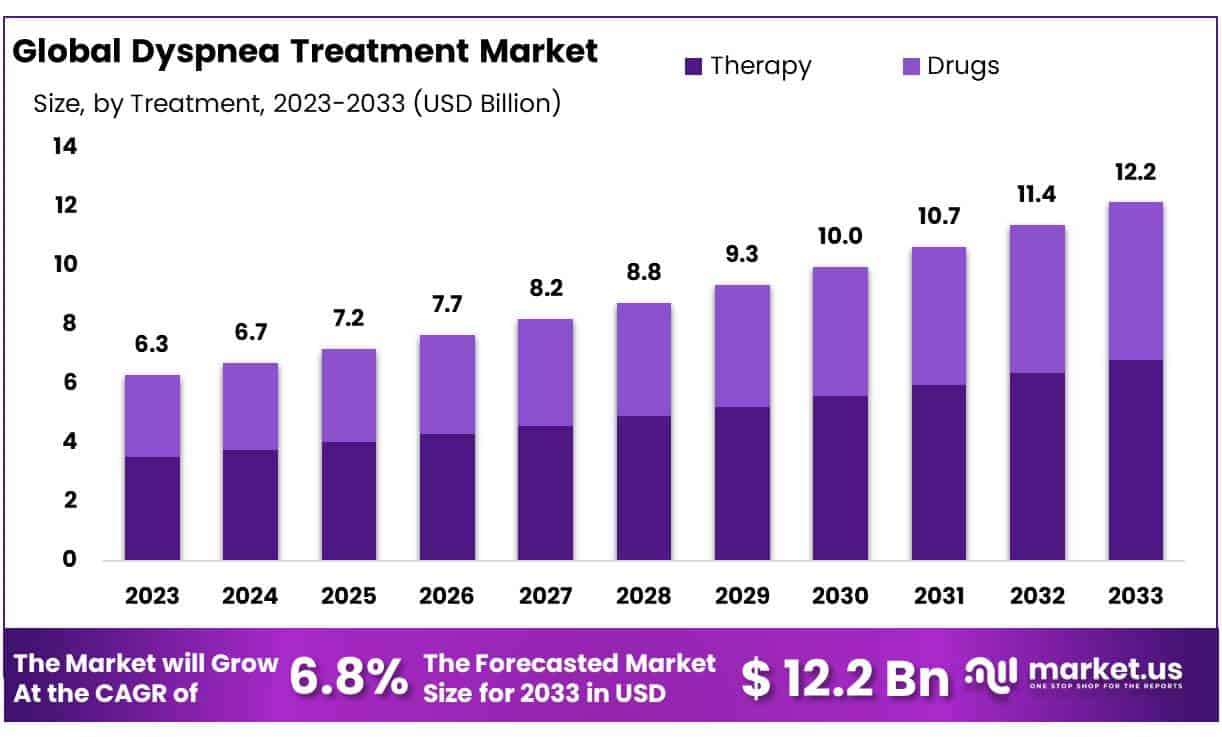

New York, NY – Oct 14, 2025 – The Global Dyspnea Treatment Market size is expected to be worth around USD 12.2 Billion by 2033 from USD 6.3 Billion in 2024, growing at a CAGR of 6.8% during the forecast period from 2025 to 2033.

The treatment landscape for dyspnea, commonly known as shortness of breath, is witnessing significant advancements driven by innovations in medical technology, respiratory therapeutics, and diagnostic techniques. The growing prevalence of chronic respiratory conditions such as COPD, asthma, and heart failure has accelerated the demand for effective dyspnea management solutions. Recent developments in pharmacological therapies, including bronchodilators and corticosteroids, alongside the emergence of non-invasive ventilation devices, have enhanced patient outcomes and quality of life.

Additionally, research into precision medicine and targeted therapies is expanding treatment options tailored to the underlying causes of dyspnea. The dyspnea treatment market is expected to record steady growth, supported by rising healthcare expenditure, increased awareness regarding early diagnosis, and the adoption of advanced respiratory monitoring systems.

Collaborative initiatives between pharmaceutical companies and healthcare providers continue to drive clinical innovation and accessibility of care. Experts believe that integrating digital health platforms, AI-based monitoring tools, and telemedicine will further improve the management and monitoring of patients experiencing dyspnea symptoms.

Key Takeaways

- Market Overview: Global Dyspnea Treatment Market size is expected to be worth around USD 12.2 Billion by 2033 from USD 6.3 Billion in 2024, growing at a CAGR of 6.8% during the forecast period from 2025 to 2033.

- Treatment Analysis: In 2023, the therapies segment accounted for the largest market share, representing 56% of the global dyspnea treatment market. The dominance of this segment is attributed to the growing adoption of pharmacological and non-pharmacological therapies aimed at symptom relief and improved respiratory function.

- Route of Administration Analysis: The inhalation route remained the preferred and most widely used mode of drug delivery, capturing 58% of the total market share in 2023. Its continued dominance is supported by its rapid onset of action and high efficacy in delivering respiratory medications directly to the lungs.

- End-Use Analysis: Hospitals emerged as the leading end-use segment, holding approximately 39% of the market share in 2023. The segment’s leadership is primarily driven by the increasing number of hospital-based treatments and the availability of advanced diagnostic and therapeutic facilities.

- Regional Analysis: North America held a substantial 40% market share, generating around USD 2.5 billion in revenue in 2023. The region’s strong position is supported by advanced healthcare infrastructure, favorable reimbursement policies, and the high prevalence of respiratory disorders.

Regional Analysis

North America accounted for approximately 40% of the global dyspnea treatment market, generating around USD 2.5 billion in revenue in 2023. This dominance is attributed to multiple contributing factors, including an aging population, rising smoking prevalence, and increasing environmental pollution, all of which have led to a notable surge in dyspnea cases and related respiratory and cardiovascular disorders across the region.

The market growth is further reinforced by continuous advancements in medical technology and pharmaceutical research, resulting in the development of innovative and more effective therapeutic solutions for dyspnea management. Moreover, heightened awareness regarding the impact of dyspnea on overall quality of life, coupled with well-established healthcare infrastructure and comprehensive insurance coverage, continues to support market expansion across the United States and Canada.

Each country-specific analysis within the dyspnea treatment market report provides an in-depth examination of domestic market drivers, regulatory developments, and their influence on the competitive environment. Key metrics such as consumption volumes, production capacities, trade flows, pricing trends, raw material costs, and value chain analyses spanning both upstream and downstream operations serve as essential indicators for assessing current market dynamics and forecasting future growth opportunities.

Use Cases

- Chronic Obstructive Pulmonary Disease (COPD): Approximately 65 million people globally suffer from moderate to severe COPD, with dyspnea being a predominant symptom. Treatment strategies include bronchodilator therapy, pulmonary rehabilitation, and, in certain cases, oxygen supplementation to alleviate breathlessness and enhance daily functioning.

- Heart Failure: Dyspnea is a common manifestation in heart failure patients, affecting about 26 million individuals worldwide. Management involves optimizing heart failure therapy, which may include diuretics, inotropes, and lifestyle modifications to reduce fluid overload and improve breathing comfort.

- Asthma: In asthma patients, dyspnea episodes are managed with inhaled bronchodilators and corticosteroids. Approximately 339 million people globally are affected by asthma, and timely use of these medications is essential to control symptoms and prevent exacerbations.

- Anxiety Disorders: Dyspnea can also be a physical manifestation of anxiety, affecting up to 33.7% of the population during their lifetime. In such cases, treatment focuses on anxiety management through cognitive-behavioral therapy, relaxation techniques, and, when necessary, pharmacotherapy to alleviate breathlessness.

- Post-COVID-19 Recovery: Persistent dyspnea has been observed in patients recovering from COVID-19, with studies indicating that up to 30% of individuals experience ongoing breathlessness weeks after infection. Management includes pulmonary rehabilitation and supportive care to facilitate respiratory recovery.

Frequently Asked Questions on Dyspnea Treatment

- What is dyspnea and what causes it? Dyspnea, commonly known as shortness of breath, is caused by various conditions such as asthma, chronic obstructive pulmonary disease (COPD), heart failure, pneumonia, and anxiety. It occurs when the body’s oxygen demand exceeds supply during breathing.

- How is dyspnea diagnosed? Dyspnea is diagnosed through medical history evaluation, physical examination, and diagnostic tests such as chest X-rays, ECGs, pulmonary function tests, and arterial blood gas analysis to determine underlying respiratory or cardiovascular abnormalities.

- What are the common treatments for dyspnea? Treatment for dyspnea depends on the cause and may include bronchodilators, corticosteroids, oxygen therapy, antibiotics, lifestyle modifications, and pulmonary rehabilitation programs aimed at improving lung function and reducing breathing discomfort.

- Can dyspnea be prevented? Prevention involves managing chronic conditions such as asthma or COPD, quitting smoking, maintaining a healthy weight, regular exercise, and avoiding exposure to environmental pollutants or allergens that may trigger breathing difficulties.

- What are the complications of untreated dyspnea? If left untreated, dyspnea can lead to severe oxygen deprivation, fatigue, reduced physical activity, anxiety, and worsening of underlying respiratory or cardiac diseases, ultimately compromising the patient’s overall quality of life.

- What is the dyspnea treatment market? The dyspnea treatment market comprises pharmaceutical drugs, medical devices, and therapeutic solutions designed to manage shortness of breath arising from respiratory or cardiovascular diseases, with growing demand due to increasing disease prevalence.

- Which regions dominate the dyspnea treatment market? North America and Europe currently dominate the market due to advanced healthcare infrastructure, strong research initiatives, and high prevalence of respiratory disorders, while Asia-Pacific is witnessing rapid market expansion.

- Who are the major players in the dyspnea treatment market? Key players include GlaxoSmithKline plc, AstraZeneca plc, Novartis AG, Boehringer Ingelheim, and Teva Pharmaceuticals, which focus on product innovation and strategic collaborations to enhance global market presence.

Conclusion:

The dyspnea treatment market is poised for sustained growth, driven by rising respiratory disease prevalence, advancements in therapeutic innovations, and increasing adoption of digital health technologies. Continuous developments in pharmacological and non-invasive treatments are significantly improving patient outcomes and care accessibility.

The dominance of North America reflects robust healthcare infrastructure and strong R&D initiatives, while emerging economies in Asia-Pacific offer untapped opportunities for expansion. Strategic collaborations among pharmaceutical firms, healthcare providers, and technology companies are expected to accelerate innovation, enhance disease management efficiency, and strengthen the overall global market outlook for dyspnea treatment in the coming years.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)