Table of Contents

Overview

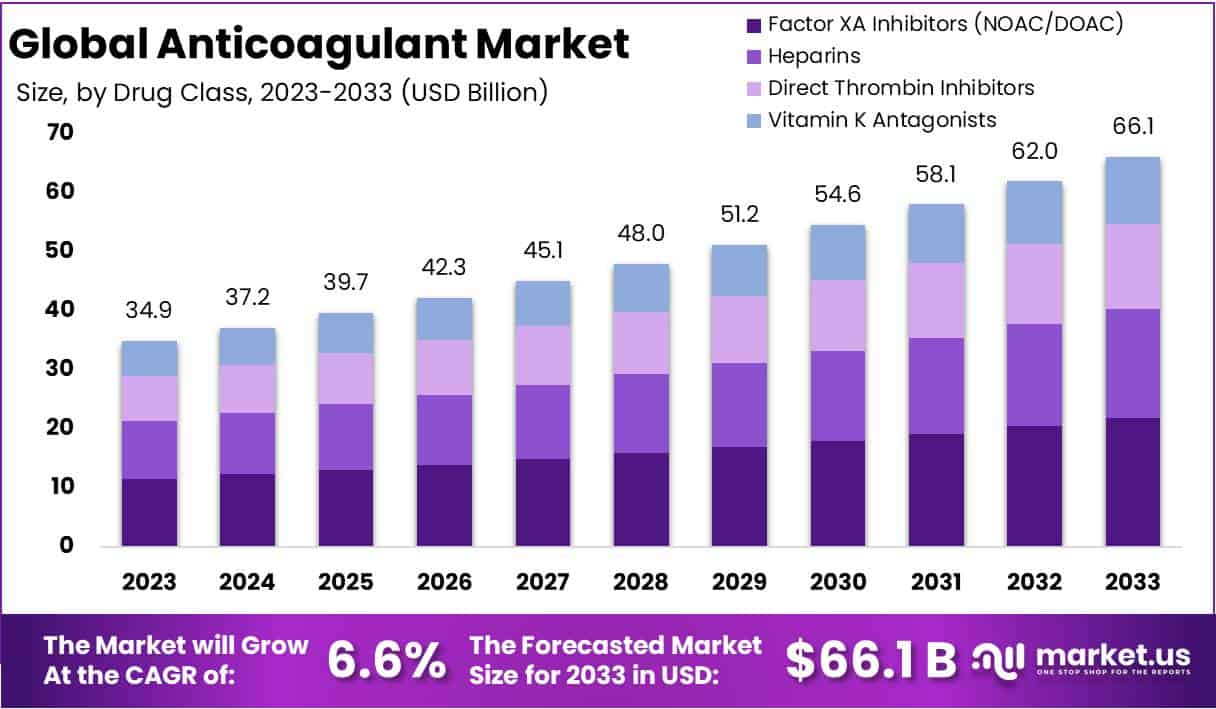

The Global Anticoagulant Market is projected to reach USD 66.1 billion by 2033, up from USD 34.9 billion in 2023, at a CAGR of 6.6% during 2024–2033. Growth is driven by expanding clinical applications, regulatory support, and broader preventive use across healthcare systems. Rising awareness of venous thromboembolism (VTE) and other clotting disorders is leading to higher adoption of anticoagulants in both inpatient and outpatient care.

Hospitals are emphasizing routine VTE risk assessment as part of national quality standards. In England, 89% of adult admissions were assessed in 2024, encouraging consistent prophylactic anticoagulant use. These programs ensure early intervention and raise baseline utilization across healthcare providers. As prevention becomes a core component of hospital quality metrics, steady demand for both injectable and oral anticoagulants is being maintained worldwide.

The product landscape is shifting toward direct oral anticoagulants (DOACs), such as apixaban and dabigatran. These agents offer better safety, convenience, and adherence compared to vitamin K antagonists. In England, DOACs accounted for 85% of oral anticoagulant prescriptions in 2022, reflecting a clear preference in clinical practice. Global regulatory inclusion, such as India’s National List of Essential Medicines, further broadens access and affordability for these treatments.

Market growth is reinforced by the approval of new therapeutic indications and safety features. For instance, rivaroxaban’s expanded use with aspirin for chronic coronary and peripheral artery disease adds new patient segments. The availability of reversal agents like andexanet alfa and idarucizumab enhances physician confidence and promotes wider adoption in higher-risk patients. These advances are improving long-term therapy outcomes and supporting sustained prescription volumes.

Rising lifestyle-related diseases and chronic conditions are also boosting demand. Obesity, physical inactivity, and chronic kidney disease (CKD) significantly increase clot risks. WHO reports show 16% global obesity prevalence and around 674 million CKD patients in 2025. Additionally, trauma and orthopedic surgeries continue to drive short-term anticoagulant use. Together, these factors, coupled with home-monitoring coverage for warfarin users, ensure consistent market growth and strengthen the foundation for future expansion.

Key Takeaways

- The global anticoagulant market is projected to rise from USD 34.9 billion in 2023 to USD 66.1 billion by 2033, registering 6.6% CAGR.

- Cardiovascular diseases remain the key demand driver, with the WHO reporting around 17.9 million global deaths annually due to these conditions.

- Regulatory authorities such as the FDA and EMA influence over 60% of market decisions, maintaining strict control over drug safety and efficacy standards.

- Factor XA inhibitors dominated the segment with a 33% market share in 2023, valued for superior safety profiles and therapeutic effectiveness.

- Oral anticoagulants held a 61% market share, preferred by patients and healthcare providers for their ease of administration and better compliance.

- Hospital pharmacies accounted for 57% of global sales, serving as the primary distribution channel for critical and immediate anticoagulant requirements.

- Growing geriatric populations and the increasing prevalence of cardiovascular diseases continue to propel global market growth.

- The risk of bleeding complications associated with anticoagulant therapy poses a significant restraint, influencing prescription and management patterns.

- North America led the global market with a 41.6% share in 2023, supported by advanced healthcare infrastructure and high disease incidence.

- The Asia-Pacific region is anticipated to grow rapidly, driven by healthcare investments and rising lifestyle-related cardiovascular health challenges.

Regional Analysis

In 2023, North America dominated the anticoagulant market, capturing over 41.6% of the total share, valued at USD 14.5 billion. The strong market position was driven by the high prevalence of cardiovascular diseases and a well-established healthcare system. The presence of key industry players also strengthened regional growth. Additionally, increasing awareness of advanced treatment options and the expanding aging population, which is more vulnerable to venous thromboembolism, significantly supported the market expansion across the region during the year.

Europe followed closely behind North America in the anticoagulant market. The region’s growth was supported by robust healthcare infrastructure and substantial healthcare spending. Rising obesity rates and sedentary lifestyles have led to a higher incidence of conditions requiring anticoagulation therapy. Furthermore, strong government support and an emphasis on research and development initiatives have enhanced innovation in treatment options, driving further adoption. These factors collectively positioned Europe as one of the most competitive markets for anticoagulant therapies globally.

The Asia-Pacific region emerged as the fastest-growing market for anticoagulants, supported by rapid improvements in healthcare infrastructure and increasing healthcare investments. Rising awareness of cardiovascular health and an expanding middle-class population have boosted market penetration. Countries such as China and India have shown remarkable potential due to large patient pools and a rising burden of lifestyle-related disorders. Continuous government initiatives and growing private sector involvement in healthcare services are expected to further accelerate the adoption of anticoagulant therapies across the region.

Latin America held a smaller market share but demonstrated steady growth in recent years. The expansion was driven by improving healthcare access, government initiatives, and increased awareness of blood-related disorders. Countries like Brazil and Mexico are witnessing higher adoption of advanced treatments due to better healthcare funding. Meanwhile, the Middle East and Africa regions are projected to show moderate growth. Limited healthcare infrastructure and restricted access to advanced medical facilities remain challenges, yet gradual improvements are expected to support future market expansion.

Segmentation Analysis

In 2023, the anticoagulant market was dominated by Factor XA Inhibitors, also known as NOACs or DOACs, which held over 33% of the market share. Their rise is due to their safety, convenience, and superior clinical outcomes compared to traditional anticoagulants. Heparins also maintained a strong position, especially in acute and surgical cases, due to their fast action and reversibility. Direct Thrombin Inhibitors serve niche needs, while Vitamin K Antagonists continue to be relevant for specific patients despite a steady decline in overall usage.

The oral route of administration led the anticoagulant market in 2023, securing more than 61% of the total share. This dominance stems from the convenience and independence oral anticoagulants offer to patients. The availability of novel oral anticoagulants (NOACs) with improved safety and simplified dosing supports this trend. Oral drugs enable long-term adherence, particularly for chronic cardiovascular conditions. Injectable anticoagulants, however, remain essential in hospital settings for urgent treatment needs, ensuring balanced market growth across both administration routes.

Pulmonary Embolism represented the largest indication segment in the 2023 anticoagulant market, accounting for over 65% of total share. Its prevalence is rising due to aging populations, sedentary lifestyles, and obesity. Early detection and improved diagnostic capabilities are further driving demand. Deep Vein Thrombosis (DVT) treatment remains a key focus, supported by public awareness and preventive healthcare initiatives. The segmental trends underscore the importance of innovation in anticoagulant therapies, ensuring effective, safe, and patient-oriented solutions for thrombotic conditions.

In 2023, hospital pharmacies dominated the anticoagulant distribution landscape, holding over 57% of the market. Their prominence is attributed to their critical role in providing immediate therapies within hospital settings. Retail pharmacies followed closely, ensuring consistent access for long-term treatments. Online pharmacies have also grown rapidly, supported by digital healthcare advancements and consumer preference for convenience. Together, these channels create a robust distribution network, improving accessibility and adherence for patients requiring continuous anticoagulation therapy.

Drug Class

- Factor XA Inhibitors (NOAC/DOAC)

- Heparins

- Direct Thrombin Inhibitors

- Vitamin K Antagonists

Route of Administration

- Oral

- Injectable

Indication

- Deep Vein Thrombosis

- Pulmonary Embolism

- Atrial Fibrillation & Heart Attack

- Ischemic Stroke

- Others

Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Key Players Analysis

The anticoagulant market is characterized by strong competition and continuous innovation, driven by leading pharmaceutical companies. These organizations invest heavily in research and development to enhance product effectiveness and safety. Among them, Pfizer Inc. plays a pivotal role through its extensive product portfolio and global presence. Sanofi SA also contributes significantly by offering advanced anticoagulant therapies aimed at preventing and treating thromboembolic disorders, thus supporting improved patient outcomes across multiple healthcare settings.

Generic drug manufacturers further strengthen market accessibility through affordable treatment options. Dr. Reddy’s Laboratories leads in this area, emphasizing cost-effective anticoagulant solutions without compromising quality. Aspen Holdings complements this approach by expanding its product line and building strategic alliances that enhance market reach. Such initiatives collectively support affordability and ensure a consistent supply of life-saving anticoagulant medications in both developed and emerging markets.

Global healthcare leaders also influence innovation and expansion strategies in this sector. Abbott Laboratories continues to improve treatment efficiency through technological integration and advanced formulation techniques. Leo Pharma AS and Alexion Pharmaceuticals Inc. focus on niche therapeutic segments, introducing targeted solutions that address complex cardiovascular conditions. Their strategic research collaborations foster medical advancement and strengthen their competitive positions within the anticoagulant market.

The market’s competitive edge is further defined by companies such as Bayer AG, Johnson & Johnson, and Bristol-Myers Squibb Company, which dominate through innovation and global distribution networks. Daiichi Sankyo Company and Boehringer Ingelheim Pharmaceuticals Inc. also contribute by introducing novel anticoagulant drugs with enhanced efficacy and safety profiles. Collectively, these key players drive the evolution of the anticoagulant market, promoting innovation, improving patient care, and ensuring the availability of effective treatment options worldwide.

Market Key Players

- Pfizer Inc.

- Sanofi SA

- Dr. Reddy’s Laboratories

- Aspen Holdings

- Abbott Laboratories

- Leo Pharma AS

- Alexion Pharmaceuticals Inc.

- Bayer AG

- Johnson & Johnson

- Bristol-Myers Squibb Company

- Daiichi Sankyo Company

- Boehringer Ingelheim Pharmaceuticals Inc.

Challenges

Bleeding Risk and Reversal Needs

Bleeding risk remains the major safety concern in anticoagulant therapy. Reversal agents are available but remain limited due to high cost and narrow indications. Idarucizumab reverses dabigatran and was first approved by the FDA in October 2015. Andexanet alfa, approved in May 2018, reverses apixaban and rivaroxaban. However, global access to these reversal agents is still uneven. Many healthcare systems face challenges in ensuring affordability and timely availability. Broader access to safe and cost-effective reversal options remains a key need in clinical practice.

Use in Special Populations

The use of direct oral anticoagulants (DOACs) in special populations remains restricted. They are generally not recommended during pregnancy or breastfeeding. In such cases, clinicians often rely on heparins or warfarin as safer alternatives. Patients with severe kidney or liver disease require special consideration. Drug exposure and metabolism can vary significantly, making dose adjustment critical. Clinical reviews highlight caution in advanced liver conditions. These variations in safety and dosing create challenges for uniform treatment practices across patient groups.

Affordability and Access

Affordability is a major challenge for patients using DOACs. These drugs are significantly more expensive than warfarin. Medicare data show that DOACs cost between 12 and 30 times more per unit. Such high prices increase both payer and patient burdens. Many patients face monthly out-of-pocket costs exceeding $100, which can reduce adherence. Limited insurance coverage further restricts access. To improve adherence, healthcare systems must address affordability through better pricing policies and broader reimbursement coverage.

Monitoring in Real-World Settings

While INR monitoring is not required for DOACs, real-world challenges persist. Adherence remains inconsistent due to factors like cost, complexity, and limited awareness. Drug–drug interactions and inappropriate dosing still occur. These issues highlight the need for stronger patient education and healthcare support systems. In elderly or multimorbid patients, comparative safety data are still evolving. Ongoing guideline updates and pragmatic studies aim to refine best practices. Continuous monitoring of real-world outcomes remains essential for safer anticoagulant use.

Regulatory and Pharmacovigilance Demands

Regulatory oversight and pharmacovigilance requirements remain intensive. Managing bleeding risks and peri-procedural protocols adds complexity and cost to treatment. These measures, while essential for safety, increase the overall lifecycle cost of DOACs. Lower-resource settings often face slow adoption due to such regulatory and logistical barriers. National and international guidelines recommend cautious use, emphasizing patient selection and risk minimization. Ongoing safety monitoring and compliance with evolving regulations remain vital to sustain market trust and patient safety.

Opportunities

Population Growth in Eligible Patients

The number of people eligible for anticoagulant therapy is increasing globally. This rise is mainly due to the growing burden of atrial fibrillation (AF) and venous thromboembolism (VTE). Aging populations and higher rates of chronic diseases such as diabetes and hypertension are major drivers. As life expectancy rises, more patients will require long-term anticoagulation treatment. This trend will expand the addressable patient base for both existing and new therapies. Over the next decade, this growing population is expected to be a key factor supporting consistent market growth for anticoagulant products.

Guideline Momentum Toward DOACs

Direct Oral Anticoagulants (DOACs) are now preferred in most leading cardiology treatment guidelines. These recommendations strengthen the global transition away from warfarin. Clinicians favor DOACs because of their predictable dosing, fewer interactions, and no need for routine monitoring. The presence of clear prescribing guidelines simplifies adoption, especially in newly diagnosed AF patients. Hospitals and healthcare systems are increasingly standardizing these pathways. As a result, DOACs are expected to capture a larger share of the market, supporting steady class growth over the coming years.

Patent Expiries Enabling Generics

Upcoming patent expiries will open opportunities for generic competition in the DOAC market. Apixaban (Eliquis) is projected to face generic entry in the U.S. by April 2028, while key European markets could see generics as early as the second half of 2026. Rivaroxaban (Xarelto) maintains dosage protection in Europe until mid-January 2026, guiding regional timelines. These patent expiries are likely to lower prices, making treatment more affordable and accessible. The entry of generics will expand patient reach and stimulate market competition, especially in cost-sensitive healthcare systems.

Reversal and Safety Innovations

Safety advancements are improving physician confidence in DOACs. The introduction of targeted reversal agents such as idarucizumab and andexanet alfa allows rapid reversal of anticoagulation in emergencies. These agents reduce concerns about bleeding risks and improve hospital safety protocols. As these reversal therapies become more widely available, clinicians may be more willing to prescribe DOACs to high-risk patients. Such innovations enhance patient safety and can drive adoption in both acute and chronic care settings, strengthening the overall trust in DOAC therapy.

Label Optimization and Precision Use

Better dose management is supporting safer and more effective DOAC use. Recent clinical reviews provide practical guidance for adjusting doses in patients with renal or hepatic impairments. These recommendations help reduce adverse events and discontinuations. Improved dosing precision enhances patient adherence and persistence with long-term therapy. Optimized labels and evidence-based dosing criteria increase confidence among healthcare professionals. As a result, treatment outcomes improve, supporting broader clinical acceptance and patient retention in the anticoagulant market.

Health-Economic Value Cases

Economic studies continue to demonstrate the long-term value of DOACs over warfarin. Traditional warfarin therapy requires frequent monitoring and carries higher complication risks, adding to overall healthcare costs. DOACs, though initially more expensive, can reduce hospitalizations and improve quality of life. When total care costs are considered, DOACs often prove cost-effective. This makes them attractive for value-based healthcare models. Payers and providers are increasingly open to contracts that reward outcomes, creating new opportunities for DOAC adoption and sustainable market expansion.

Conclusion

The global anticoagulant market is set for strong growth, supported by rising cardiovascular cases, expanding clinical use, and advances in drug safety. The demand for direct oral anticoagulants continues to grow as they offer better convenience and fewer complications. Hospitals and healthcare systems worldwide are promoting early prevention and consistent treatment, which helps drive long-term adoption. Expanding patient awareness, supportive regulations, and upcoming generic drug launches will make these therapies more accessible and affordable. With ongoing innovations, improved safety profiles, and wider patient coverage, the anticoagulant market is expected to remain a key focus area in the global pharmaceutical landscape over the coming years.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)