Table of Contents

Overview

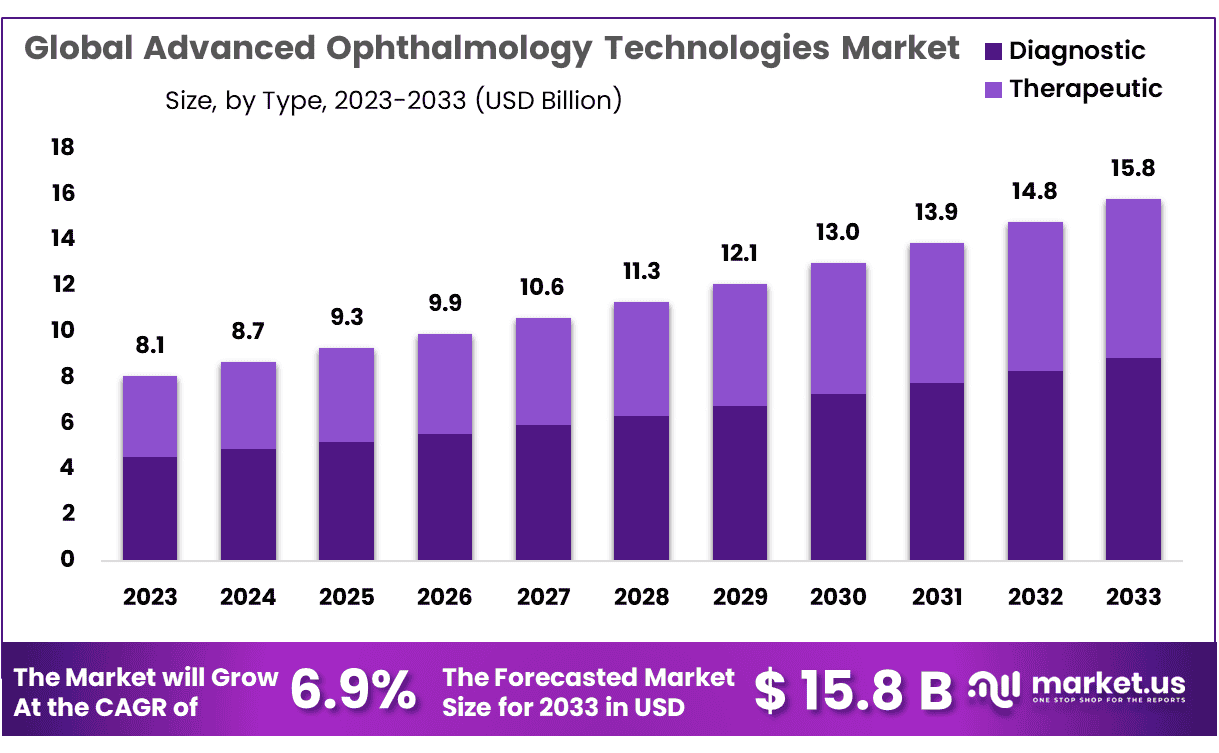

New York, NY – Jan 27, 2026 – The Global Advanced Ophthalmology Technologies Market size is expected to be worth around USD 15.8 Billion by 2033 from USD 8.1 Billion in 2023, growing at a CAGR of 6.9% during the forecast period from 2024 to 2033.

Advanced ophthalmology technologies represent a significant progression in the diagnosis, treatment, and management of eye-related disorders. These technologies are designed to improve clinical accuracy, enhance patient outcomes, and support ophthalmologists in delivering efficient and precise eye care services. The growing prevalence of visual impairment, cataracts, glaucoma, diabetic retinopathy, and age-related macular degeneration has accelerated the adoption of innovative ophthalmic solutions globally.

Modern ophthalmology technologies encompass diagnostic imaging systems, surgical devices, vision correction tools, and digital health platforms. Diagnostic advancements such as optical coherence tomography (OCT), fundus cameras, and corneal topography systems allow detailed visualization of ocular structures, enabling early disease detection and timely intervention. These systems are increasingly integrated with artificial intelligence (AI) algorithms, which support automated image analysis and clinical decision-making.

On the surgical front, technologies such as femtosecond lasers, phacoemulsification systems, and minimally invasive glaucoma surgery (MIGS) devices have transformed ophthalmic procedures. These solutions are associated with higher precision, reduced surgical time, and faster patient recovery. In addition, advancements in intraocular lenses (IOLs) and refractive surgery platforms have expanded treatment options for vision correction.

Digital ophthalmology, including teleophthalmology platforms and electronic medical records, is further improving access to eye care and streamlining clinical workflows. The integration of cloud-based data management and remote monitoring tools supports continuity of care, particularly in underserved regions.

Overall, advanced ophthalmology technologies are expected to play a critical role in addressing the rising global burden of eye diseases. Continuous research, technological innovation, and increasing healthcare investments are anticipated to sustain market growth and long-term adoption.

Key Takeaways

- Market Size: The Advanced Ophthalmology Technologies Market is projected to reach approximately USD 15.8 billion by 2033, increasing from USD 8.1 billion in 2023.

- Market Growth: Market expansion is expected to occur at a compound annual growth rate (CAGR) of 6.9% over the forecast period spanning 2024 to 2033.

- Type Analysis: The diagnostic segment maintains a dominant position, accounting for nearly 56% of the total market share.

- End-Use Analysis: Hospitals represent the leading end-use segment, capturing around 38% of overall market demand.

- Regional Analysis: North America held a significant market presence, contributing approximately 34.5% of global revenue, equivalent to USD 2.7 billion.

- Teleophthalmology Trend: The COVID-19 pandemic significantly accelerated the adoption of teleophthalmology solutions, enabling remote eye examinations, consultations, and patient monitoring, and emerging as a key industry trend.

Regional Analysis

In 2023, North America accounted for a significant 34.5% share of the global Advanced Ophthalmology Technologies Market, generating approximately USD 2.7 billion in revenue. This strong market position is supported by multiple structural and demand-side factors.

The region benefits from a large and diverse patient population, which continues to drive sustained demand for advanced diagnostic and therapeutic ophthalmic solutions. In parallel, the presence of leading industry participants and a well-established healthcare infrastructure further reinforces regional market strength.

In addition, the consistent introduction of technologically advanced ophthalmic devices, particularly within the United States, plays a critical role in supporting market expansion. Manufacturers are actively focused on innovation to enhance diagnostic accuracy and clinical efficiency.

For instance, NIDEK introduced the RS-3000 Advance 2 Optical Coherence Tomography (OCT) system in June 2018. This device integrates a laser ophthalmoscope (SLO), enabling detailed imaging and analysis of retinal and glaucoma-related conditions. Such product launches highlight the region’s emphasis on adopting advanced ophthalmology technologies and contribute to its continued market leadership.

Emerging Trends

- Artificial Intelligence (AI) in Ophthalmic Diagnostics: AI-based algorithms are increasingly being adopted for the analysis of retinal images, supporting the early detection of conditions such as diabetic retinopathy and age-related macular degeneration. These solutions demonstrate high diagnostic accuracy and operational efficiency, enabling earlier clinical intervention and contributing to a reduction in the risk of advanced vision impairment.

- Expansion of Teleophthalmology Services: The integration of telemedicine into ophthalmic care has significantly improved access to diagnosis and treatment, particularly in rural and underserved regions. Teleophthalmology supports remote screening, diagnosis, and disease management, enhancing patient convenience while extending the reach of specialist eye care services.

- Advancements in Gene and Stem Cell Therapies: Ongoing developments in gene editing and stem cell–based therapies are addressing retinal disorders that were previously considered untreatable. These novel approaches focus on correcting defective genes or regenerating damaged retinal cells, with the objective of restoring or preserving visual function.

- Growth of Minimally Invasive Surgical Techniques: Innovations in ophthalmic surgery, including femtosecond laser-assisted procedures, are enabling higher precision with reduced surgical trauma. These minimally invasive techniques are associated with shorter recovery periods, improved safety outcomes, and enhanced patient comfort, particularly in procedures such as cataract surgery.

- Adoption of Augmented Reality (AR) and Virtual Reality (VR): AR and VR technologies are increasingly utilized in ophthalmic training and surgical practice. These tools provide immersive simulations for skill development and real-time intraoperative assistance, supporting improved surgical accuracy and clinical outcomes.

- Shift Toward Personalized Ophthalmic Care: There is a growing emphasis on personalized medicine in ophthalmology, with treatments being tailored to individual patient characteristics, including genetic profiles and disease-specific factors. This approach is intended to improve therapeutic effectiveness, optimize clinical outcomes, and enhance patient satisfaction.

Key Use Cases

- AI-Enabled Screening for Diabetic Retinopathy: AI-driven screening platforms are widely deployed for the detection of diabetic retinopathy, achieving diagnostic accuracy rates exceeding 90%. These systems support large-scale screening programs, facilitating early diagnosis and timely disease management to prevent vision loss.

- Gene Therapy for Leber Congenital Amaurosis (LCA): Gene therapy has demonstrated clinical success in treating Leber Congenital Amaurosis, a rare inherited retinal disorder. Clinical studies have reported measurable improvements in visual function among pediatric patients, including enhanced object recognition and improved mobility in low-light environments.

- Remote Ophthalmic Consultations via Teleophthalmology: Teleophthalmology has enabled remote specialist consultations, particularly benefiting patients in geographically isolated or resource-limited settings. Its adoption increased significantly during the COVID-19 pandemic, ensuring continuity of care while reducing the risk of infection exposure.

- Minimally Invasive Glaucoma Surgery (MIGS): MIGS procedures are gaining widespread acceptance due to their favorable safety profile and effectiveness in reducing intraocular pressure. Compared to conventional glaucoma surgeries, these techniques involve minimal tissue disruption, resulting in faster recovery and lower complication rates.

- AR-Assisted Surgical Navigation: Augmented reality systems are being used to overlay real-time imaging data onto the surgical field, enhancing precision during complex ophthalmic procedures such as retinal surgeries. This capability supports accurate instrument positioning and improved tissue handling during surgery.

Frequently Asked Questions on Advanced Ophthalmology Technologies

- What are advanced ophthalmology technologies?

Advanced ophthalmology technologies refer to innovative diagnostic, surgical, and therapeutic solutions used in eye care, including laser systems, imaging devices, and digital platforms, designed to improve clinical accuracy, treatment outcomes, and patient safety. - How do advanced imaging technologies improve eye disease diagnosis?

Advanced imaging technologies, such as optical coherence tomography and digital fundus imaging, enable high-resolution visualization of ocular structures, allowing earlier disease detection, precise monitoring, and improved clinical decision-making across multiple ophthalmic conditions. - What role does laser technology play in modern ophthalmology?

Laser technology plays a critical role in ophthalmology by enabling minimally invasive procedures for refractive correction, cataract surgery, and retinal disorders, resulting in reduced recovery time, enhanced precision, and improved long-term visual outcomes. - How are digital and AI-based tools transforming ophthalmology care?

Digital platforms and artificial intelligence tools support automated image analysis, disease screening, and workflow optimization, improving diagnostic efficiency, reducing clinician burden, and enabling scalable eye care delivery, particularly in high-volume clinical environments. - What factors are driving the growth of the advanced ophthalmology technologies market?

Market growth is driven by the rising prevalence of eye disorders, increasing aging populations, technological advancements, and growing demand for minimally invasive procedures, supported by improved healthcare infrastructure and higher awareness of eye health. - Which product segments dominate the advanced ophthalmology technologies market?

Diagnostic and surgical devices represent dominant market segments, supported by high adoption of imaging systems, laser-based platforms, and vision correction technologies, which are widely used across hospitals, specialty clinics, and ambulatory surgical centers. - How does the aging population impact market demand?

The aging population significantly increases demand for advanced ophthalmology technologies, as age-related conditions such as cataracts, glaucoma, and macular degeneration require early diagnosis, continuous monitoring, and technologically advanced treatment solutions.

Conclusion

Advanced ophthalmology technologies are reshaping eye care by enabling earlier diagnosis, greater surgical precision, and improved long-term patient outcomes. The growing burden of visual impairment, combined with rapid innovation in imaging systems, laser-based surgery, AI-enabled diagnostics, and digital health platforms, continues to drive market expansion globally.

Strong adoption across hospitals and specialty clinics, particularly in North America, reflects robust healthcare infrastructure and sustained investment in innovation. Looking ahead, continued advancements in minimally invasive procedures, teleophthalmology, and personalized treatments are expected to strengthen clinical efficiency and accessibility, supporting steady market growth over the forecast period.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)