Table of Contents

Overview

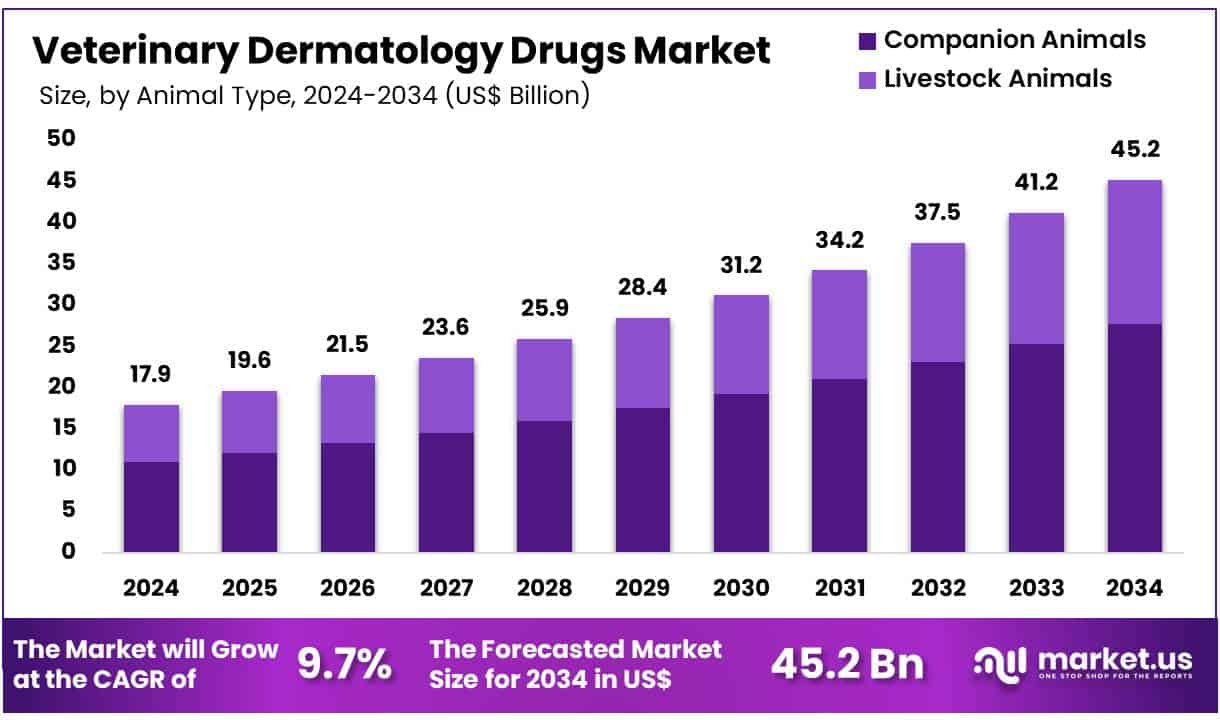

New York, NY – July 08, 2025 – Global Veterinary Dermatology Drugs Market size is expected to be worth around US$ 45.2 Billion by 2034 from US$ 17.9 Billion in 2024, growing at a CAGR of 9.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.2% share with a revenue of US$ 7.0 Billion.

The global Veterinary Dermatology Drugs Market is witnessing significant growth, driven by increasing pet ownership and heightened awareness of animal health and skin conditions. The market size is projected to expand steadily over the next decade, supported by advancements in veterinary therapeutics and growing demand for dermatological solutions in companion and livestock animals.

Skin diseases such as dermatitis, flea allergy, pyoderma, and mange are increasingly prevalent in animals, prompting the development and adoption of specialized veterinary drugs. Key pharmaceutical interventions include antiparasitics, anti-inflammatories, antifungals, and antibiotics, administered through topical, oral, and injectable routes.

Rising expenditure on pet healthcare, particularly in North America and Europe, continues to accelerate market expansion. According to the American Pet Products Association, U.S. pet owners spent over US$ 136 billion on pet products and services in 2023, with dermatology treatments forming a critical component. Furthermore, the emergence of targeted therapies, such as monoclonal antibodies for canine atopic dermatitis, highlights the industry’s shift toward precision treatment.

Leading players are investing in research to introduce safer and more effective formulations. Regulatory support and increasing awareness among veterinarians and pet owners further enhance market opportunities. The Asia-Pacific region is anticipated to exhibit substantial growth, driven by the expanding pet population and improving veterinary infrastructure.

Key Takeaways

- In 2024, the Veterinary Dermatology Drugs Market generated a revenue of US$ 17.9 billion, and it is projected to reach approximately US$ 45.2 billion by 2034, expanding at a compound annual growth rate (CAGR) of 9.7% during the forecast period.

- By animal type, the market is categorized into companion animals and livestock animals. Among these, companion animals dominated the market in 2023, accounting for a 61.5% share, driven by increasing pet ownership and heightened spending on companion animal healthcare.

- In terms of the route of administration, the market is segmented into oral, topical, and injectable formulations. The topical segment held the largest share, contributing 49.2% to the global market in 2023, owing to its ease of application and effectiveness in treating external dermatological conditions.

- Based on application, the market is classified into parasitic infections, allergic infections, and others. Parasitic infections emerged as the leading segment, capturing a 52.3% revenue share, reflecting the high prevalence of fleas, ticks, and mites among domestic and farm animals.

- By distribution channel, the market is divided into hospital pharmacies, retail, and e-commerce platforms. Hospital pharmacies led the market, accounting for 53.8% of total revenue, driven by the growing preference for veterinarian-prescribed medications.

- Regionally, North America dominated the global market, securing a 39.2% share in 2023, supported by advanced veterinary infrastructure and high awareness of animal dermatological health.

Segmentation Analysis

- Animal Type Analysis: The companion animals segment accounted for 61.5% of the market, driven by rising global pet ownership and growing awareness of pet healthcare. The increasing incidence of skin allergies, infections, and parasitic conditions in pets is boosting demand for dermatological treatments. Enhanced pet humanization trends and willingness to invest in animal health are further supporting growth. Technological advancements in safe, effective topical therapies continue to strengthen this segment’s expansion in veterinary dermatology.

- Route of Administration Analysis: Topical drugs held a dominant 49.2% market share due to their direct and convenient application for treating skin conditions. These formulations, including creams, sprays, and ointments, are preferred for managing allergies, infections, and parasitic infestations. Their effectiveness, ease of use, and reduced systemic side effects make them ideal for both companion and livestock animals. The growing availability of non-invasive topical solutions continues to drive segment growth, supported by rising awareness of veterinary dermatological care.

- Application Analysis: The parasitic infections segment led with 52.3% of total revenue, fueled by the high prevalence of flea, tick, and mite infestations in pets and livestock. Growing concern over parasitic diseases and their zoonotic potential has increased demand for targeted treatments. Advancements in spot-on solutions, medicated shampoos, and systemic antiparasitics are expanding therapeutic options. Veterinarian recommendations and owner awareness are expected to sustain strong growth in this segment over the forecast period.

- Distribution Channel Analysis: Hospital pharmacies captured 53.8% of the market, benefiting from their central role in veterinary care. These facilities provide specialized and emergency treatments, making them key distribution points for dermatology drugs. The expansion of veterinary clinics and the increasing complexity of animal skin conditions are driving demand for clinical access to advanced therapies. Strong supplier relationships and comprehensive pharmaceutical offerings position hospital pharmacies as the leading channel in the veterinary dermatology drugs market.

Market Segments

By Animal Type

- Companion Animals

- Dogs

- Cats

- Horses

- Others

- Livestock Animals

- Cattle

- Others

By Route of Administration

- Oral

- Topical

- Injectable

By Application

- Parasitic Infections

- Allergic Infections

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail

- E-commerce

Regional Analysis

North America led the veterinary dermatology drugs market in 2024, accounting for the highest revenue share of 39.2%. This dominance is attributed to increasing pet ownership, heightened awareness of pet health, and the growing trend of pet humanization. According to the American Pet Products Association (APPA), pet-owning households in the U.S. rose to 94 million in 2024, up from 82 million in 2023, significantly expanding the addressable market. Younger demographics such as Gen Z and Millennials are driving this shift, contributing to greater spending on specialized veterinary care, including dermatological treatments.

Key industry players such as Zoetis and Merck Animal Health have reported strong growth in dermatology product sales. Zoetis noted a 7% increase in U.S. companion animal revenue in Q4 2024, led by demand for products like Apoquel and Cytopoint. Similarly, Merck’s BRAVECTO line saw a 12% increase in sales in Q4 2023 due to rising need for flea and tick treatments.

The Asia Pacific region is projected to witness the fastest CAGR during the forecast period. Rising disposable incomes, increasing pet populations in countries like China (116 million pets) and India (32 million pets), and greater access to veterinary services are fueling regional growth. Strategic expansion by companies like Zoetis and Elanco further supports this trend.

Emerging Trends

- Expansion of Targeted Oral JAK Inhibitors: The development of novel Janus kinase (JAK) inhibitors for canine skin disease has accelerated. In September 2024, the FDA approved ilunocitinib tablets (Zenrelia™) for control of pruritus associated with allergic and atopic dermatitis in dogs aged ≥12 months. In field studies, 306 client-owned dogs (146 males, 160 females) received daily doses of 0.6–0.8 mg/kg, achieving significant reduction in owner-assessed itch scores and lesion severity over 28 days. This follows the earlier approval of oclacitinib (Apoquel®) in 2013, marking a sustained trend toward small-molecule immunomodulators administered orally.

- Rise of Monoclonal Antibody Therapies: Biologic immunotherapeutics are becoming standard for canine allergic dermatitis. In April 2025, USDA APHIS listed “Canine Allergic Dermatitis Immunotherapeutic” (Cytopoint™), a monoclonal antibody targeting interleukin-31, for subcutaneous use in dogs. Such agents offer prolonged itch relief with dosing intervals extending 4–8 weeks, reducing reliance on daily medications.

- Greater Use of Systemic Immunosuppressants in Felines: Cyclosporine soft-gel capsules (Atopica® for Cats) continue to be widely employed for feline allergic dermatitis. A multi-center field trial enrolled 217 cats (92 males, 125 females) treated once daily at 7 mg/kg for 42 days, demonstrating effective control of excoriations, eosinophilic plaques, and pruritus, with the ability to taper dosing frequency. This reflects ongoing reliance on systemic immunosuppressants where topical options are insufficient.

- Emphasis on Antimicrobial Stewardship: Increased attention to antibiotic resistance has driven more frequent culture and susceptibility testing in refractory pyoderma cases. When methicillin-resistant Staphylococcus pseudintermedius* is identified, veterinarians resort to less-commonly used agents (e.g., chloramphenicol, tetracyclines, rifampin), balancing efficacy and safety .

- Improved Topical Formulations for Localized Therapy: New spray and cream formulations of topical glucocorticoids (e.g., hydrocortisone sprays) are gaining traction as adjunctive treatments to minimize systemic exposure. These are indicated for mild inflammation and as steroid-sparing agents in long-term management.

Use Cases

- Control of Canine Pruritus with Ilunocitinib

- Indication: Pruritus associated with allergic and atopic dermatitis in dogs ≥12 months.

- Dosage & Efficacy: Once-daily oral dose of 0.6–0.8 mg/kg in 306 dogs resulted in a mean 60% reduction in pruritus visual analog scale (PVAS) scores by Day 28; the highest dose group (42 dogs) showed superior lesion improvement on CADESI-4 scoring.

- Monoclonal Antibody Therapy for Canine Allergy

- Agent: Cytopoint™ (lokivetmab), a canine IL-31 monoclonal antibody.

- Administration: Single subcutaneous injection, repeated every 4–8 weeks.

- Benefit: Over 70% of treated dogs experience ≥50% itch reduction within 24 hours, improving quality of life and owner compliance.

- Feline Allergic Dermatitis Management with Cyclosporine

- Study Population: 217 client-owned cats aged 1–16 years, weight 1.95–9.91 kg.

- Regimen: Oral cyclosporine at 7 mg/kg once daily for 42 days.

- Outcome: 85% of cats achieved “good” or “excellent” overall clinical improvement; dosing could be tapered to every-other-day based on response.

- Addressing Canine Pyoderma with Cephalosporins

- First-line Therapy: First-generation cephalosporins (e.g., cephalexin at 22 mg/kg BID) administered for 14–28 days.

- Efficacy: Well tolerated with clinical cure rates exceeding 90% in uncomplicated pyoderma cases, and rare occurrence of antibiotic resistance.

- Culture-Guided Treatment of Resistant Infections

- Context: In refractory dermatologic infections, culture and susceptibility testing is performed in approximately 30% of cases to identify MRSP.

- Alternative Agents: Chloramphenicol, aminoglycosides, tetracyclines, rifampin, and linezolid may be used when first-line antibiotics fail .

- Adjunctive Topical Therapy for Mild Lesions

- Formulation: Hydrocortisone spray applied twice daily to affected areas.

Role: Reduces lesion erythema and itch, allowing for lower doses of systemic anti-inflammatories in long-term management.

- Formulation: Hydrocortisone spray applied twice daily to affected areas.

Conclusion

The global veterinary dermatology drugs market is experiencing sustained growth, driven by increasing pet ownership, advancements in targeted therapies, and rising demand for specialized skin treatments in animals. With strong market performance in North America and rapid expansion in Asia Pacific, the industry is supported by innovation in immunotherapeutics, improved topical formulations, and enhanced diagnostic stewardship.

Key players are focusing on companion animal care, particularly for parasitic and allergic conditions, ensuring continued investment in product development. As awareness and access to veterinary care improve globally, the market is expected to remain resilient and expand steadily over the coming decade.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)