Table of Contents

Overview

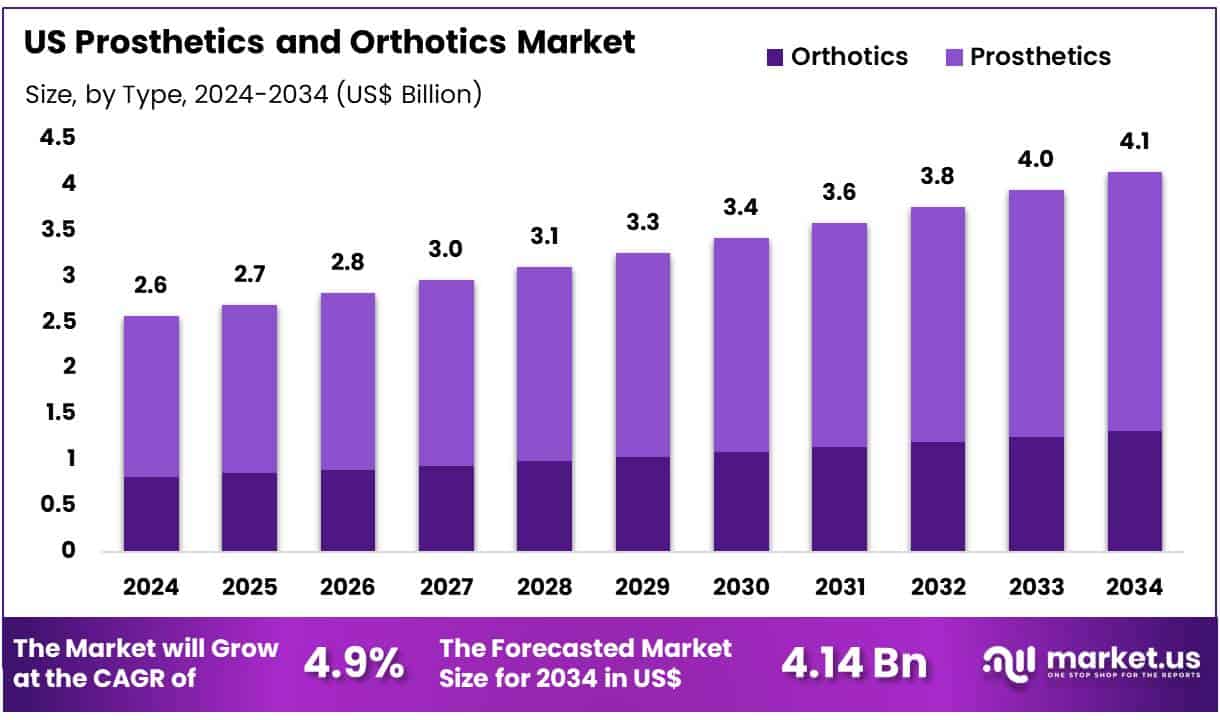

New York, NY – July 04, 2025 – The US Prosthetics and Orthotics Market reach USD 2.57 Billion by 2024 And the market is anticipated to grow at a CAGR of 4.9% between 2024 and 2034, reaching USD 4.14 Billion by 2034.

The U.S. prosthetics and orthotics market is experiencing steady expansion, supported by growing incidences of limb loss, musculoskeletal disorders, and an aging population requiring mobility assistance. Increasing prevalence of conditions such as diabetes, vascular disease, osteoarthritis, and trauma-related injuries is driving demand for advanced prosthetic and orthotic solutions across the country.

Technological advancements, including the integration of microprocessor-controlled devices, 3D printing, and lightweight materials, are significantly improving the functionality, durability, and patient comfort of these medical devices. These innovations are fostering greater adoption, particularly among active users seeking improved mobility and lifestyle integration.

The orthotics segment continues to dominate the market due to its widespread application in managing spinal conditions, joint deformities, and injury rehabilitation. Meanwhile, the prosthetics segment is witnessing increasing attention owing to the development of personalized and sensor-integrated limb replacements.

Hospitals, rehabilitation centers, and specialty clinics remain the key end-users of prosthetics and orthotics devices. Government initiatives aimed at improving access to assistive technologies, coupled with favorable reimbursement policies, are further contributing to market growth.

As awareness increases and new technologies continue to emerge, the U.S. prosthetics and orthotics market is poised for continued advancement, offering opportunities for innovation, improved patient outcomes, and enhanced quality of life for individuals with mobility impairments.

Key Takeaways

- By Type: The market is segmented into orthotics and prosthetics, with orthotics accounting for 68.3% of the total share. This dominance is attributed to the increasing prevalence of musculoskeletal disorders and a growing elderly population. Conditions such as arthritis, diabetic foot complications, and sports-related injuries are contributing to rising demand for orthotic devices, which provide support, enhance mobility, and aid in rehabilitation, especially among aging and physically active individuals.

- By Technology: The technology segment includes electric-powered, conventional, and hybrid orthopedic prosthetics. Conventional prosthetics hold a leading share of 43.8%, driven by their cost-effectiveness, reliability, and ease of use. These devices remain widely adopted, particularly in regions with limited access to high-tech solutions. Their mechanical design offers durability and functional performance, making them suitable for patients in both urban and rural healthcare settings.

- By End User: End users include hospitals, rehabilitation centers, prosthetics clinics, and others. Hospitals dominate with a 45.8% market share, serving as key centers for prosthetic and orthotic services. Their role in offering comprehensive care ranging from prosthetic fittings to post-operative support and physiotherapy has become increasingly vital due to the rising incidence of traumatic injuries, chronic illnesses, and limb amputations, which require integrated care solutions within hospital environments.

Segmentation Analysis

- Type Analysis: Orthotics held the largest share of 68.3% in the U.S. prosthetics and orthotics market, primarily due to the high prevalence of musculoskeletal disorders and an aging population. Orthotic devices like braces, supports, and shoe inserts are widely used for conditions such as arthritis, scoliosis, and diabetic foot ulcers. Their non-invasive nature, lower cost, and applicability across a broader patient base, including sports injury cases, contribute to their popularity among hospitals, clinics, and rehabilitation centers.

- Technology Analysis: Conventional prosthetics led the market with a 43.8% share, favored for their affordability, ease of use, and mechanical reliability. These body-powered devices are commonly chosen by elderly patients and those in rural areas with limited access to advanced technology. Conventional systems require less maintenance and are not dependent on electronics, making them suitable for first-time users. Their durability and ease of adaptation continue to drive demand in both urban and underserved healthcare settings.

- End User Analysis: Hospitals dominated the end-user segment with a 45.8% market share due to their comprehensive services, including surgery, prosthetic fitting, and rehabilitation. With access to specialized staff and advanced equipment, hospitals serve as primary centers for patients needing prosthetic and orthotic care. High patient volume and structured reimbursement systems further reinforce their position as the leading end-user within the U.S. prosthetics and orthotics market.

Market Segments

By Type

- Orthotics

- Spinal Orthotics

- Upper Limb

- Lower Limb

- Prosthetics

- Upper Extremity

- Lower Extremity

- Modular Components

- Liners

- Sockets

By Technology

- Electric-powered

- Conventional

- Hybrid Orthopedic Prosthetics

By End User

- Hospitals

- Rehabilitation Centre

- Prosthetics Clinics

- Others

Key Player Analysis

The U.S. prosthetics and orthotics market is highly competitive, with key players driving innovation, patient care, and technological advancement. Prominent companies include Össur, Ottobock, Hanger Clinic (Hanger Inc.), College Park Industries, Proteor USA, Advanced Arm Dynamics, Blatchford, Freedom Innovations, Zimmer Biomet, Fillauer, Mobius Bionics, Ohio Willow Wood, Esper Bionics, Comprehensive Prosthetics & Orthotics, Rebound Orthotics & Prosthetics, and others.

Össur, headquartered in Iceland, is a global leader in non-invasive orthopedic technologies. In the U.S., the company maintains a strong presence with its advanced prosthetic systems, including the Rheo Knee, Proprio Foot, and Empower Ankle. These devices feature AI and sensor-driven technologies that enable real-time adaptability and improved user mobility. Össur also offers a comprehensive range of orthotic solutions targeting spinal, osteoarthritis, and injury-related conditions.

Ottobock, based in Germany, is a dominant player in the U.S. market, recognized for pioneering smart prosthetics such as the C-Leg, Genium, and myoelectric upper-limb devices. These microprocessor-controlled solutions significantly enhance user safety, mobility, and comfort, especially for lower and upper limb amputees.

Hanger Clinic, a subsidiary of Hanger Inc., is the largest provider of patient care services in the U.S. prosthetics and orthotics space. With a network of over 800 clinics nationwide, Hanger Clinic focuses on personalized fittings, rehabilitation, and ongoing care. The clinic collaborates with top manufacturers like Össur and Ottobock to deliver customized, high-performance prosthetic and orthotic solutions tailored to individual patient needs.

Emerging Trends

- Growth of 3D-Printed, Patient-Specific Devices: The use of 3D printing has expanded to produce external prostheses tailored to each individual’s anatomy. This technology allows manufacturers to adjust designs quickly without new tooling, enabling patient-matched limbs and braces with complex internal structures for improved fit and function.

- Advances in Neuroprosthetics with Sensory Feedback: Recent government-funded research has demonstrated upper-limb prosthetics that connect directly to residual nerves, enabling a sense of touch. In small clinical trials, stimulators implanted near nerves have allowed users to perceive contact and better control their prosthetic hands.

- Rapid Workforce Expansion: Employment for orthotists and prosthetists in the US is projected to grow from about 9,100 in 2023 to 10,400 by 2033 a 15.1% increase over the decade. This rate far exceeds the average for all occupations, reflecting rising demand for customized limb and brace fittings. The median annual wage was USD 78,310 in May 2024.

Use Cases

- Diabetic Foot Prevention with Therapeutic Footwear: Medicare Part B covers one pair of extra-depth shoes (or custom molded shoes) and up to two pairs of inserts each year for adults with diabetes at risk of foot ulcers. With an estimated 38 million American adults living with diabetes 80% of whom face foot complications this benefit can prevent up to 85% of diabetes-related amputations by providing properly fitted footwear annually.

- Post-Amputation Prosthetic Fitting: In 2020, US hospitals recorded approximately 160,000 lower-extremity amputations among adults with diabetes (6.8 per 1,000 adults with diabetes). Each of these cases typically requires a custom prosthetic limb, demonstrating the critical role of orthotic-prosthetic teams in restoring mobility and independence.

- Orthotic Support for Stroke Survivors: Stroke was associated with about 321,000 hospitalizations in 2020 among adults with diabetes, many of whom benefit from ankle-foot orthoses to aid walking and balance during rehabilitation. By providing rigid or dynamic support, these braces can improve gait symmetry and reduce fall risk, supporting over 300,000 stroke patients annually.

- Home Health Aide Assistance with Prosthetic Care: Under the Medicare home health benefit, certified aides can deliver personal care related to prosthetic and orthotic devices such as assisting with donning, doffing, and basic maintenance under the supervision of a registered nurse every 14 days. This use case highlights the integration of O&P services into at-home care for patients recovering from surgery or adjusting to assistive devices.

Conclusion

The U.S. prosthetics and orthotics market is poised for sustained growth, driven by a rising aging population, increasing chronic disease burden, and rapid technological advancements. With orthotics accounting for a major market share due to musculoskeletal disorders, and conventional prosthetics remaining popular for their affordability and reliability, the sector continues to evolve.

Strong hospital infrastructure, favorable reimbursement frameworks, and innovative efforts by key players such as Össur, Ottobock, and Hanger Clinic further strengthen market performance. As demand for personalized, sensor-enabled, and 3D-printed devices rises, the industry is well-positioned to improve mobility outcomes and enhance patient quality of life.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)