Table of Contents

Overview

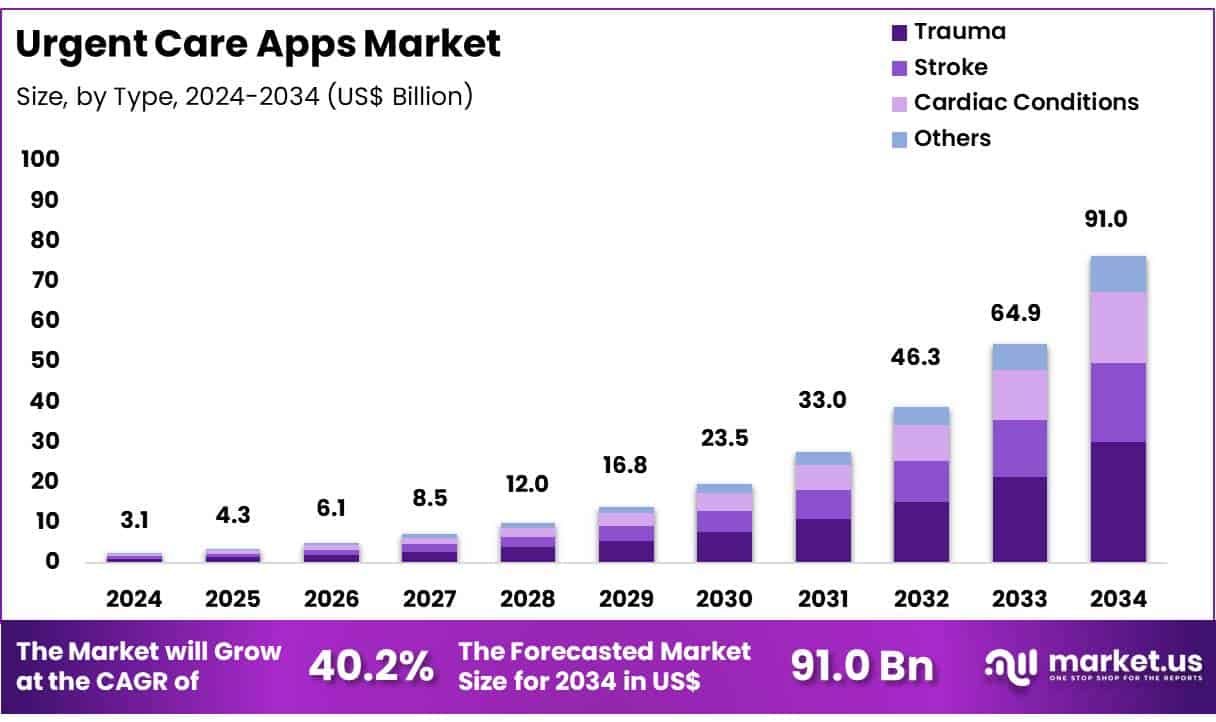

New York, NY – May 26, 2025 – Global Urgent Care Apps Market was valued at USD 3.1 billion in 2024 and is anticipated to register substantial growth of USD 91.0 billion by 2034, with 40.2% CAGR.

The global Urgent Care Apps Market is experiencing notable growth, driven by rising demand for real-time healthcare access, increased smartphone penetration, and growing adoption of digital health platforms. These mobile applications are transforming the delivery of emergency and semi-emergency care by enabling rapid communication between patients, caregivers, and healthcare providers.

Urgent care apps offer features such as appointment scheduling, symptom checkers, real-time triage, and video consultations. The increased burden on emergency departments, coupled with the global focus on reducing avoidable hospital visits, is propelling the market forward. These applications are being widely adopted by healthcare systems, insurance providers, and patients seeking convenient and cost-effective medical services.

North America currently dominates the market due to advanced digital infrastructure, supportive regulatory policies, and high healthcare spending. However, the Asia-Pacific region is expected to witness the fastest growth, fueled by expanding mobile health initiatives, increasing urbanization, and growing health awareness.

The COVID-19 pandemic significantly accelerated the adoption of urgent care apps, highlighting the importance of remote healthcare delivery. Continued investments in telehealth technology, AI-based triage tools, and user-friendly interfaces are expected to drive further innovation in this space. As healthcare systems worldwide aim for greater efficiency and accessibility, urgent care apps are poised to become an integral part of the digital health ecosystem.

Key Takeaways

- The global Urgent Care Apps Market was valued at USD 3.1 billion in 2024 and is projected to reach USD 91.0 billion by 2034, expanding at a compound annual growth rate (CAGR) of 40.2% during the forecast period.

- In 2024, the Post-hospital Apps segment emerged as the dominant category, accounting for approximately 43% of the total market revenue.

- The Trauma segment held a significant position, capturing around 33% of the global revenue share in the same year.

- North America continued to lead the global market, contributing over 39% of the total revenue in 2024, supported by advanced healthcare infrastructure and widespread digital health adoption.

Segmentation Analysis

- Type Analysis: Based on type, the urgent care apps market is segmented into pre-hospital emergency care & triaging apps, in-hospital communication & collaboration apps, and post-hospital apps. In 2024, the post-hospital apps segment held the largest share, accounting for 53% of the global market. This dominance is attributed to rising demand for remote monitoring and continuity of care after discharge. These apps assist in managing chronic conditions, preventing readmissions, and enhancing recovery through features such as progress tracking, digital wound care, and provider collaboration.

- Clinical Area Analysis: By clinical area, the market is segmented into trauma, stroke, cardiac conditions, and others. In 2024, the trauma segment led the global urgent care apps market with a 49% share. This growth is driven by the critical need for timely responses to injuries and improved pre-hospital care. Apps supporting trauma management enhance emergency response through real-time coordination among responders and healthcare providers. Initiatives like Nigeria’s Trauma Care International Foundation app exemplify the use of digital tools to reduce trauma-related morbidity and mortality.

Market Segments

Type

- Pre-hospital Emergency care & Triaging Apps

- In-hospital Communication & Collaboration Apps

- Post-hospital Apps

- Medication Management Apps

- Rehabilitation Apps

- Care Provider Communication & Collaboration Apps

Clinical Area

- Trauma

- Stroke

- Cardiac Conditions

- Others

Regional Analysis

North America accounted for a significant 39% share of the global urgent care apps market in 2024, supported by the region’s advanced healthcare infrastructure, high smartphone penetration, and widespread adoption of digital health technologies. The increasing demand for accessible, real-time medical assistance is driving the uptake of mobile health solutions across both urban and remote settings.

The growth of urgent care apps in North America is further propelled by the need to ease pressure on conventional healthcare systems while improving patient convenience. These apps offer rapid access to medical consultations, particularly for non-emergency conditions, by integrating seamlessly with existing healthcare networks.

A key example is the Cedars-Sinai Connect app, launched in October 2023, which utilizes AI technology from K Health to deliver 24/7 virtual care for urgent and primary healthcare needs. The app enables users to undergo an AI-driven intake process and connect with licensed providers through video consultations, exemplifying the region’s commitment to enhancing care delivery through digital innovation.

Emerging Trends

- Rapid Adoption by Providers: The use of telemedicine has expanded markedly in recent years. In 2021, 80.5 percent of office-based physicians reported using telemedicine for patient care, compared with just 16.0 percent in 2019. This increase can be attributed to emergency policy flexibilities and growing comfort with digital health tools.

- Stabilization and Modest Decline in Use: After peaking during the pandemic, telehealth utilization has partially stabilized. In 2023, 25 percent of Medicare fee-for-service beneficiaries had at least one telehealth service—a 4 percent decline from 2022 levels. Meanwhile, 96 percent of Health Resources and Services Administration–funded health centers incorporated telehealth into primary care delivery in 2023.

- Broad Community Penetration: In 2021, 37 percent of U.S. adults reported using telemedicine in the past 12 months. Use was higher among older adults (43.3 percent for those 65 and over) and women (42.0 percent) than among younger adults. This wide demographic reach demonstrates the perceived convenience and accessibility of virtual urgent care solutions.

- Integration with Electronic Health Records: Larger practices and those utilizing electronic health record (EHR) systems were more likely to adopt telemedicine, indicating that digital integration and scale facilitate urgent care app deployment in clinical workflows.

Use Cases

- Management of Minor or Acute Illnesses: Urgent care apps are commonly used for non-serious, acute complaints. Among telehealth users, 32.2 percent of visits addressed minor or acute illnesses (e.g., fever, sore throat), reflecting patient preference for rapid evaluation without in-person travel.

- Chronic Disease Monitoring: Approximately 21.5 percent of telehealth encounters were devoted to chronic disease management, such as diabetes and hypertension follow-up, supporting continuity of care through remote monitoring and medication adjustments.

- Behavioral and Mental Health Services: Mental health and substance use support accounted for 16.9 percent of virtual visits, underlining the role of urgent care apps in expanding access to counseling and therapy, especially in underserved or rural areas.

- After-Hours and Night-Time Consultations: The use of telehealth for after-hours care increased from 9.9 percent of practices in 2018 to 24.4 percent in 2022, illustrating the value of urgent care apps in providing night-time and weekend access when traditional clinics are closed.

Conclusion

The global urgent care apps market is undergoing rapid expansion, driven by the increasing demand for real-time, accessible healthcare and supported by widespread digital adoption. Key growth factors include the rising burden on emergency services, post-discharge care needs, and broader telehealth integration.

With North America leading the market and Asia-Pacific showing high growth potential, these apps are reshaping how non-emergency and urgent health issues are managed. Use cases span from acute illness consultations to chronic disease monitoring and mental health services. As technology advances and healthcare systems digitize, urgent care apps are poised to play a vital role in modern care delivery.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)