Table of Contents

Overview

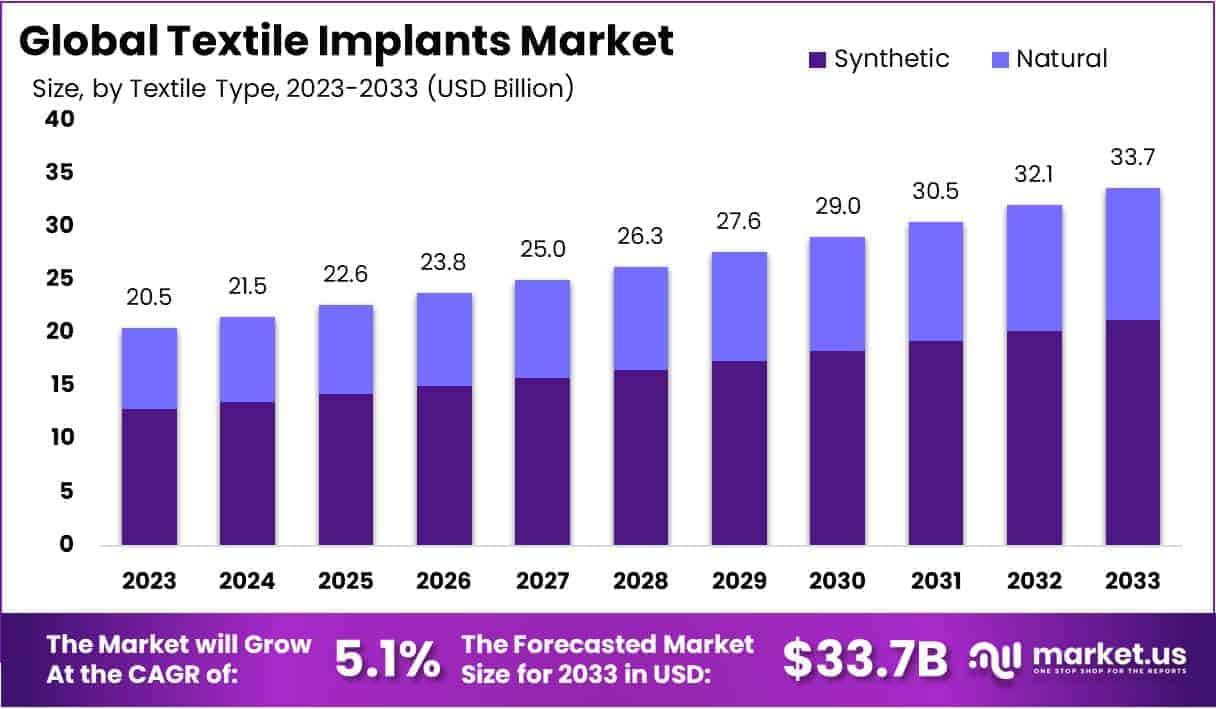

New York, NY – July 15, 2025 – The Global Textile Implants Market size is expected to be worth around USD 37.7 Billion by 2033, from USD 20.5 Billion in 2023, growing at a CAGR of 5.1% during the forecast period from 2024 to 2033.

The global textile implants market is experiencing notable growth, fueled by rising surgical procedures and technological advancements in implantable medical textiles. Textile implants are specially engineered fabrics used in a range of surgical applications, including hernia repair, cardiovascular surgery, orthopedic reconstruction, and gynecological procedures. These implants provide structural support, promote tissue regeneration, and are biocompatible with human tissues.

The demand for textile implants is increasing due to the growing aging population, a rise in chronic disorders, and advancements in minimally invasive surgical techniques. Materials such as polyester, polypropylene, and polytetrafluoroethylene (PTFE) are widely used for their strength, flexibility, and resistance to infection. Innovations in bioresorbable and antibacterial textiles are expected to further accelerate market adoption.

Hospitals and ambulatory surgical centers are the key end-users, supported by an increasing number of surgical interventions and post-operative care standards. In addition, favorable reimbursement policies and regulatory approvals are expanding access to advanced textile implants, particularly in developed markets.

North America currently holds a significant share of the global market, attributed to the presence of key manufacturers and early adoption of innovative medical technologies. Meanwhile, Asia-Pacific is projected to witness the fastest growth, driven by rising healthcare investments and expanding surgical infrastructure.

The global textile implants market continues to evolve with rising demand for safe, durable, and patient-friendly surgical solutions.

Key Takeaways

- The global textile implants market is projected to expand from USD 20.5 billion in 2023 to approximately USD 37.7 billion by 2033, registering a compound annual growth rate (CAGR) of 5.1% during the forecast period from 2024 to 2033.

- In terms of textile type, the synthetic segment held a dominant position in 2023, accounting for over 63% of the market share. This is attributed to the superior durability, biocompatibility, and mechanical strength of materials such as polyethylene terephthalate (PET) and polypropylene.

- By indication, cardiovascular surgery emerged as the leading segment, capturing more than 26% of the market share in 2023. The segment’s growth is driven by the high prevalence of cardiovascular conditions and increased adoption of textile-based vascular grafts and patches.

- Based on application, hospitals remained the primary end-use segment, contributing to over 51% of the total market share. This dominance is supported by the high number of surgical procedures and the availability of advanced surgical infrastructure in hospital settings.

- Regionally, North America led the global textile implants market in 2023, securing more than 37% of the market share. This leadership is attributed to a robust healthcare infrastructure, early adoption of medical innovations, and strong investment in R\&D activities.

Segmentation Analysis

Textile Type Analysis: In 2023, synthetic textile implants dominated the market with over a 63% share, driven by their superior mechanical strength and adaptability. Materials such as PET, polypropylene, polyester, polyethylene, and PTFE are widely used due to their durability and biocompatibility. PET and polypropylene are especially preferred in vascular and hernia surgeries. In contrast, natural materials like collagen, while less common, remain vital in applications requiring enhanced biocompatibility and tissue integration.

Indication Analysis: The cardiovascular surgery segment led the market in 2023, accounting for over 26% of the indication share. This growth is linked to rising cardiovascular cases and advancements in synthetic textiles like Dacron and ePTFE, known for biocompatibility and infection resistance. Orthopedic surgery is also expanding rapidly due to increased sports injuries and aging populations. Hernia repair and dental grafts continue to gain traction, supported by global health awareness and technological improvements in surgical mesh materials.

Application Analysis: Hospitals held the leading application share in 2023, with over 51%, supported by high surgical volumes, advanced infrastructure, and skilled professionals. Their capacity to manage complex procedures and ensure post-surgical care reinforces this position. Clinics followed, driven by rising outpatient services and demand for specialized treatments. Ambulatory Surgical Centers (ASCs) are also growing, offering cost-effective, minimally invasive care and faster recovery. These trends highlight the expanding reach of textile implants across diverse healthcare settings.

Market Segments

Textile Type

- Synthetic

- Polyethylene Terephthalate (PET)

- Polypropylene

- Polyester

- Polyethylene

- Polytetrafluoroethylene (PTFE)

- Natural

- Collagen-based

- Others

Indication

- Cardiovascular Surgery

- Orthopedic Surgery

- Hernia Repair

- Dental grafts

- Others

Application

- Hospitals

- Clinics

- Ambulatory Surgical Centers

Regional Analysis

In 2023, North America held the leading position in the global textile implants market, accounting for over 37% of the total share, with a market value of approximately USD 7.6 billion. This dominance is supported by advanced healthcare infrastructure, widespread adoption of minimally invasive procedures, and strong investment in research and development. The presence of key industry players actively engaged in product innovation has further contributed to regional market expansion.

Europe ranked second, driven by a robust regulatory environment for medical devices and an aging population increasingly affected by chronic conditions. Government support for healthcare initiatives and the rising adoption of advanced implant technologies have sustained market growth in the region.

Asia-Pacific is expected to register the highest growth rate during the forecast period. Factors such as increasing healthcare expenditure in countries like China and India, expanding population base, and significant improvements in healthcare infrastructure are fueling regional demand. The growing number of surgical procedures is also contributing to the region’s rapid market development.

Latin America and the Middle East & Africa are projected to exhibit moderate growth. Market expansion in these regions is supported by gradual improvements in healthcare systems and a slow but steady shift toward adopting modern medical technologies, including textile implants.

Emerging Trends

- Textile fabrication methods such as knitting, braiding, and electrospinning are being applied to produce implants with finely controlled fiber architectures. This enables tailoring of mechanical strength and porosity to match native tissue properties, supporting better cell integration and load transfer in tissue engineering applications.

- Cell free, biohybrid vascular grafts are being developed by reinforcing hydrogels with textile fibers. These off the shelf implants eliminate the need for cell culture, shortening production time and reducing regulatory complexity.

- Antimicrobial treatments are now being integrated directly into textile implants, achieving over 99% reduction in common pathogen loads (e.g., Staphylococcus aureus, Escherichia coli, Candida albicans). This innovation addresses surgical site infection risks without systemic antibiotics.

- Smart textile implants combining fiber constructs with embedded sensors are under investigation. These devices aim to monitor parameters such as pH, strain, or biochemical markers in real time, enabling personalized assessment of healing and early detection of complications.

Use Cases

- Hernia Repair Meshes: Synthetic polymer meshes (polypropylene, polyester, PTFE) are used in over 80% of hernia repairs worldwide due to their elasticity, tensile strength, and cost efficiency.

- Abdominal Wall Hernia Repair in Low Resource Settings: In a sub Saharan African hospital study of 1,175 hernia operations (2007–2017), mesh repair accounted for 42.5% of cases. Inguinal hernias represented 80.4% of these, with polypropylene mesh used in 96.2% of repairs.

- Clinical Outcomes in the United States: Between 2010 and 2020, 6,387 patients at a single U.S. center underwent mesh based hernia repair. Inguinal procedures (65% of cases) saw mesh infection rates as low as 0.4%, while incisional repairs had a 1.3% infection rate.

- Cardiovascular Textile Grafts and Stents: Knitted and braided fiber constructs are being utilized to fabricate vascular stents and grafts. These implants mimic the mechanical behavior of blood vessels, improving hemodynamics and reducing thrombosis risk in vascular surgery.

Conclusion

The global textile implants market is poised for steady expansion, driven by the rising demand for biocompatible, durable, and advanced surgical solutions. Growth is supported by increasing surgical volumes, a growing elderly population, and advancements in textile engineering, including antimicrobial and smart implants. Synthetic materials remain dominant, especially in cardiovascular and hernia applications.

North America leads the market, while Asia-Pacific is emerging as the fastest-growing region. Continued innovations in textile fabrication and integration of smart technologies are expected to enhance clinical outcomes, making textile implants a critical component in modern surgical and tissue repair practices worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)