Table of Contents

Overview

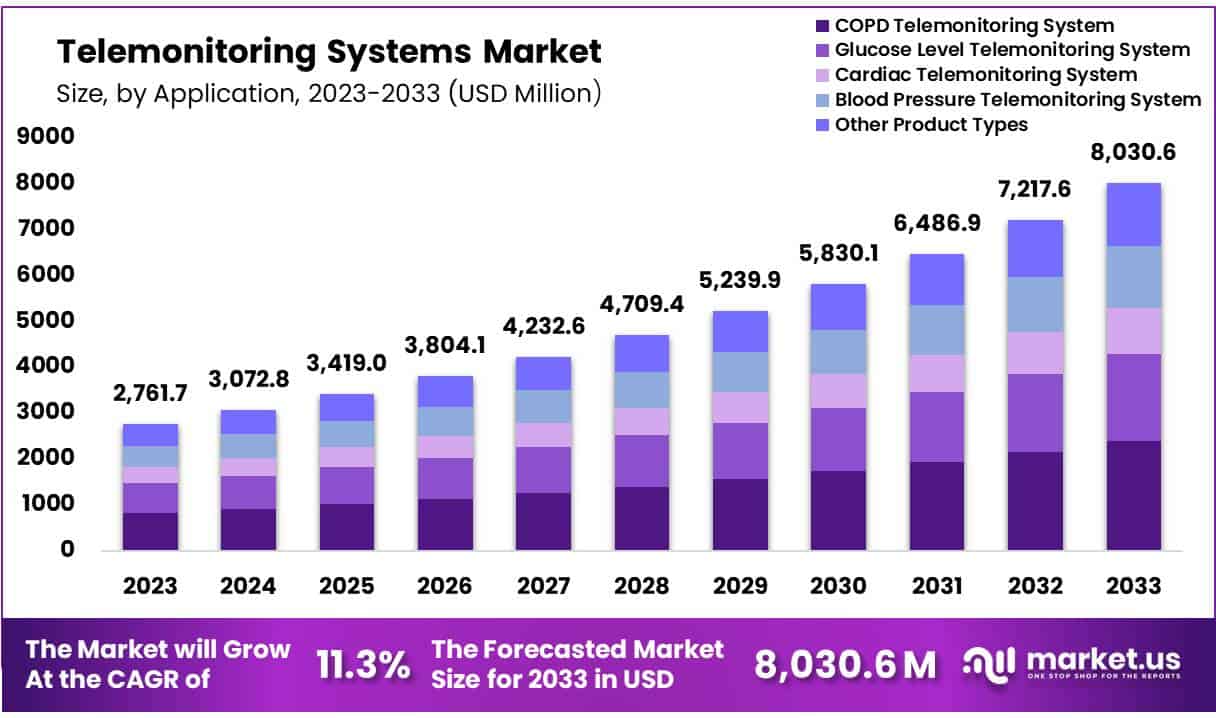

New York, NY – Jan 07, 2026 – Global Telemonitoring Systems Market size is expected to be worth around USD 8,030.6 Million by 2033 from USD 2,761.7 Million in 2023, growing at a CAGR of 11.3% during the forecast period from 2024 to 2033.

Telemonitoring systems are increasingly being recognized as a foundational component of modern digital healthcare infrastructure. These systems are designed to remotely collect, transmit, and analyze patient health data, enabling continuous monitoring outside traditional clinical settings. The basic formation of telemonitoring systems typically includes connected medical devices, secure data transmission networks, data storage platforms, and clinical dashboards for healthcare professionals.

Medical devices such as blood pressure monitors, glucose meters, pulse oximeters, and wearable sensors are used to capture real-time physiological data. This data is transmitted through wireless technologies, including cellular networks, Wi-Fi, or Bluetooth, to centralized cloud-based platforms. Advanced software applications process and organize the data, allowing clinicians to track patient conditions, identify trends, and receive alerts when predefined thresholds are exceeded.

The integration of telemonitoring systems into healthcare delivery is being driven by the growing prevalence of chronic diseases, aging populations, and the need to reduce hospital admissions and healthcare costs. These systems support proactive care models by enabling early intervention, improving treatment adherence, and enhancing patient engagement. From a healthcare provider perspective, operational efficiency is improved through optimized resource utilization and reduced burden on physical facilities.

Data security and regulatory compliance form a critical part of system design, with encryption, authentication, and data privacy controls embedded into the core architecture. As digital health adoption continues to expand, telemonitoring systems are expected to play a central role in enabling scalable, patient-centric, and value-based healthcare delivery models.

Key Takeaways

- Market Size: The Telemonitoring Systems market is projected to reach approximately USD 8,030.6 million by 2033, rising from an estimated USD 2,761.7 million in 2023.

- Market Growth: Market expansion is expected to occur at a compound annual growth rate (CAGR) of 11.3% over the forecast period from 2024 to 2033.

- Component Analysis: In 2023, software solutions represented the largest share of the market, contributing 54.1% of total revenue.

- Mode of Delivery Analysis: Web-based delivery platforms led the market in 2023, accounting for a 58.1% share due to their scalability and ease of access.

- Application Analysis: Among application segments, COPD telemonitoring systems held the leading position in 2023, capturing 29.7% of the overall market.

- End-Use Analysis: Home care settings emerged as the primary end-use segment in 2023, representing 27.8% of the total market share.

- Regional Analysis: North America dominated the global Telemonitoring Systems market in 2023, securing a 41.3% share of total market revenue.

Regional Analysis

In 2023, North America emerged as the leading region in the Telemonitoring Systems market, accounting for 41.3% of the global market share. This leadership position is primarily supported by well-established healthcare infrastructure, widespread adoption of digital health solutions, and a strong regional focus on chronic disease management and preventive healthcare services.

Market expansion in the region is further reinforced by the strong presence of key healthcare and technology companies actively advancing innovation in telemonitoring solutions. In addition, favorable government initiatives and regulatory frameworks encouraging telehealth adoption have accelerated market penetration. The rising incidence of chronic diseases, coupled with a steadily aging population, continues to increase the demand for remote patient monitoring solutions. These factors collectively highlight North America’s critical role in shaping the growth and development of the global Telemonitoring Systems market.

Emerging Trends

- Continuous Monitoring: Telemonitoring systems are transitioning from intermittent assessments to continuous monitoring models. This evolution enables real-time observation of vital parameters such as heart rate, respiratory rate, and oxygen saturation, supporting early identification of clinical deterioration and timely medical intervention.

- Integration of Artificial Intelligence (AI): Artificial intelligence is increasingly embedded in telemonitoring platforms to enhance data interpretation. AI-driven analytics support pattern recognition, risk prediction, and the generation of personalized care insights, thereby improving clinical decision-making and patient outcomes.

- Expansion of Virtual Care Services: Healthcare organizations are establishing centralized virtual care units to manage patients remotely. These departments deliver services including virtual consultations, follow-up care, and urgent care coordination, contributing to improved operational efficiency and broader patient access.

- Adoption of Wearable Devices: Wearable technologies, such as smartwatches and fitness trackers, are becoming integral to telemonitoring ecosystems. These devices continuously capture health metrics, including heart rate, physical activity, and sleep patterns, enabling proactive and preventive health management.

- Predictive Analytics for Chronic Conditions: Predictive analytics is increasingly applied in the management of chronic diseases, particularly conditions such as heart failure. By evaluating longitudinal data trends, healthcare providers can anticipate disease exacerbations and optimize treatment strategies in advance.

Key Use Cases

- Chronic Disease Management: Telemonitoring is extensively utilized for managing chronic conditions such as diabetes, hypertension, and cardiovascular diseases. Continuous tracking of vital signs supports improved disease control and contributes to a reduction in emergency visits and hospital admissions.

- Post-Surgical Recovery Monitoring: Remote monitoring following surgical procedures enables healthcare providers to assess recovery progress outside hospital settings. Early detection of post-operative complications allows for timely clinical response and may lead to shorter hospital stays.

- Elderly Care: In aging populations, telemonitoring supports independent living while ensuring consistent health oversight. Applications include fall detection, chronic condition monitoring, and medication adherence tracking, enhancing patient safety and quality of life.

- Mental Health Support: Telemonitoring solutions are increasingly applied in mental health care to monitor indicators such as sleep behavior, physical activity, and treatment adherence. These insights support personalized mental health interventions and ongoing care management.

- Healthcare Access in Remote and Underserved Areas: Telemonitoring plays a critical role in extending healthcare services to remote and underserved regions. By enabling regular health assessments without the need for physical travel, it improves continuity of care and reduces access barriers.

Frequently Asked Questions on Telemonitoring Systems

- How do Telemonitoring Systems work?

Telemonitoring systems operate by capturing patient health metrics through medical devices and wearables, transmitting the data securely to cloud-based platforms where healthcare providers can monitor trends, receive alerts, and manage patient care remotely. - What are the key components of Telemonitoring Systems?

The core components include medical monitoring devices, data transmission networks, software platforms for data analytics, cloud-based storage systems, and clinician dashboards, all designed to ensure secure, real-time access to patient health information. - What conditions are commonly monitored using Telemonitoring Systems?

Telemonitoring systems are widely used for managing chronic conditions such as COPD, diabetes, cardiovascular diseases, and hypertension, enabling continuous monitoring, improved treatment adherence, and timely clinical interventions to reduce hospitalizations. - What factors are driving the growth of the Telemonitoring Systems market?

Market growth is driven by the rising prevalence of chronic diseases, increasing aging populations, growing adoption of digital health technologies, demand for cost-effective care delivery, and supportive government initiatives promoting remote healthcare solutions. - Which component segment dominates the Telemonitoring Systems market?

Software components dominate the market due to their critical role in data integration, analytics, real-time monitoring, and interoperability, enabling healthcare providers to efficiently manage large volumes of patient data across care settings. - Which end-use segment leads the Telemonitoring Systems market?

Home care settings lead the market as telemonitoring supports remote patient management, reduces hospital visits, enhances patient convenience, and aligns with the growing preference for decentralized and patient-centric healthcare delivery models. - Which region holds the largest share in the Telemonitoring Systems market?

North America holds the largest market share, supported by advanced healthcare infrastructure, high digital health adoption, strong presence of technology providers, and a growing focus on chronic disease management and preventive healthcare services.

Conclusion

Telemonitoring systems have become a critical pillar of modern digital healthcare by enabling continuous, remote, and data-driven patient care. Their integration supports proactive disease management, reduces hospital admissions, and improves clinical efficiency, particularly in home care and chronic disease settings.

Market growth is being driven by aging populations, rising chronic disease prevalence, and rapid adoption of digital health technologies. With strong dominance in North America and increasing use of AI, wearables, and predictive analytics, telemonitoring systems are well positioned to support scalable, patient-centric, and value-based healthcare models over the long term.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)