Table of Contents

Overview

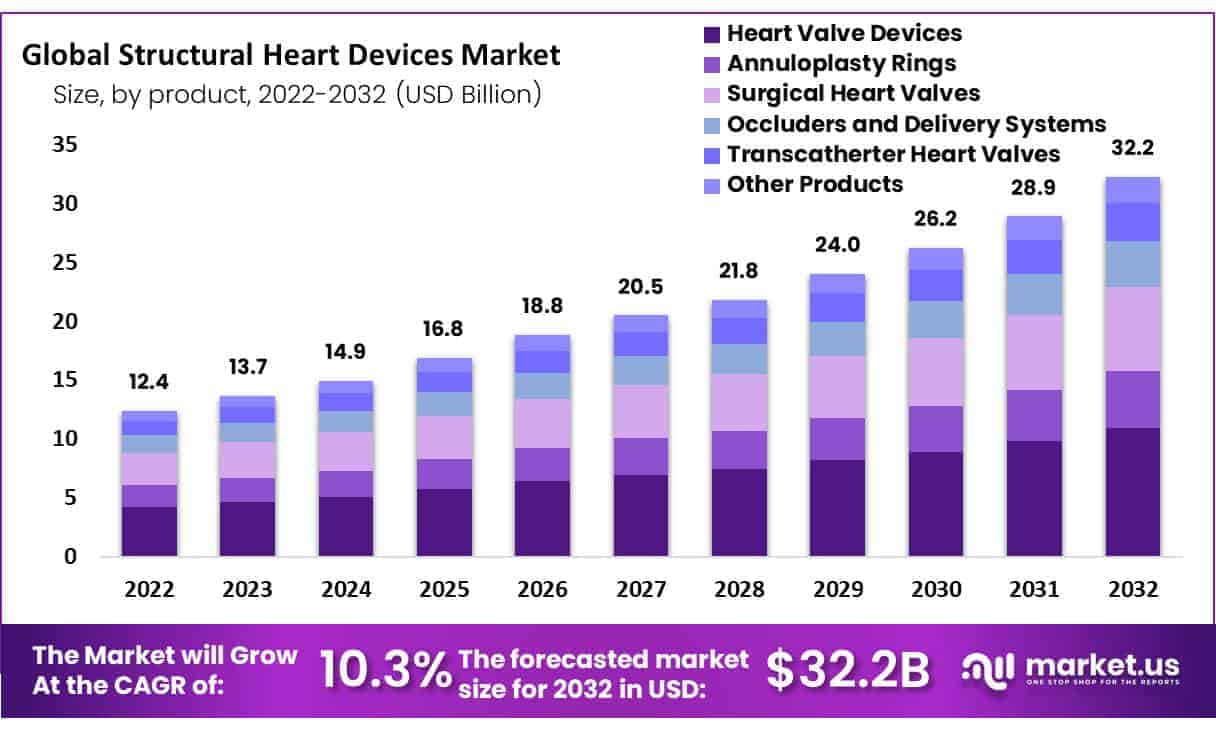

New York, NY – Sep 08, 2025 – Global Structural Heart Devices Market size is expected to be worth around USD 32.2 Billion by 2032 from USD 14.9 Billion in 2024, growing at a CAGR of 10.3% during the forecast period from 2025 to 2032.

The structural heart devices market is experiencing robust growth, driven by the increasing prevalence of cardiovascular diseases, rising adoption of minimally invasive procedures, and ongoing advancements in medical technology. Structural heart devices, which include transcatheter heart valves, annuloplasty rings, occluders, and repair devices, are playing a critical role in the management of valvular and congenital heart conditions.

The market expansion can be attributed to the growing geriatric population, high incidence of lifestyle-related risk factors, and the continuous introduction of innovative products designed to enhance patient safety and procedural efficiency. In addition, supportive regulatory approvals and increased clinical adoption of transcatheter aortic valve replacement (TAVR) procedures are further accelerating demand.

North America continues to dominate the global market, supported by advanced healthcare infrastructure and early adoption of new therapies. However, Asia-Pacific is expected to register the fastest growth, propelled by improving access to healthcare, rising awareness, and expanding investments in cardiovascular care.

Key industry players are actively engaging in strategic collaborations, product launches, and research initiatives to strengthen their market position and address the rising clinical needs. The emphasis remains on developing minimally invasive, cost-effective, and technologically advanced solutions for improved patient outcomes.

The outlook for the structural heart devices market remains positive, with sustained growth anticipated over the coming years as demand for innovative cardiac care solutions continues to rise.

Key Takeaways

- The global structural heart devices market size is projected to expand from USD 13.7 billion in 2023 to USD 32.2 billion by 2032, growing at a CAGR of 10.3% during 2025–2032.

- Approximately 60 million individuals in the United States are affected by structural abnormalities in the heart.

- Structural heart defects impact 20–25% of the overall U.S. population.

- The heart valve devices segment is expected to dominate the market with a 34% share during the forecast period.

- The aortic valve stenosis segment accounted for the highest revenue share of 25% in 2022.

- By procedure, the replacement procedures segment is anticipated to capture the largest share of 39% throughout the forecast period.

- Among end-users, the hospitals segment is projected to record significant growth, supported by high patient inflow and advanced facilities.

- The incidence of congenital heart defects stands at 1 in every 100 newborns globally.

- The cost of a SAPIEN transcatheter heart valve exceeds USD 32,000.

- In the United Kingdom, more than 7 million people are currently living with circulatory and heart diseases.

- Regionally, North America is expected to maintain dominance, accounting for a 45.3% revenue share during the forecast period.

- In May 2022, Abbott launched an innovative vascular heart valve repair device, strengthening its product portfolio.

Regional Analysis

North America accounted for a dominant revenue share of 45.3% in the global structural heart devices market. Market growth in the region is primarily driven by the high prevalence of structural heart diseases, rapid technological advancements, and the development of innovative devices. Furthermore, the presence of a well-established healthcare infrastructure facilitates early detection and effective treatment of structural heart conditions, thereby supporting market expansion.

In contrast, the Asia Pacific region is projected to register the fastest growth during the forecast period. Key factors contributing to this growth include a rising geriatric population, an increase in regulatory approvals, and the adoption of government-funded insurance schemes. Additionally, the region benefits from a growing medical tourism industry, a favorable reimbursement environment, and the implementation of improved newborn screening programs. Enhanced healthcare accessibility and rising awareness of cardiac diseases are further expected to stimulate demand for structural heart devices across Asia Pacific.

Frequently Asked Questions on Structural Heart Devices

- What are structural heart devices?

Structural heart devices are specialized medical technologies designed to diagnose, repair, or replace abnormal heart structures. These include transcatheter valves, occluders, annuloplasty rings, and repair systems, which improve cardiac function and patient outcomes through minimally invasive or surgical interventions. - Which conditions are treated using structural heart devices?

Structural heart devices are primarily used for treating heart valve diseases, congenital heart defects, aortic stenosis, atrial septal defects, and regurgitation. They restore normal blood flow, prevent complications, and significantly reduce the risks of heart failure and other cardiac disorders. - What are the main types of structural heart devices?

The major categories include heart valve devices, occluders and delivery systems, annuloplasty rings, repair devices, and accessories. Heart valve devices, especially for aortic valve stenosis, account for the largest share due to increasing adoption of transcatheter valve replacement procedures globally. - Why are structural heart devices important?

Structural heart devices are crucial because they provide life-saving treatments for patients who are often unsuitable for open-heart surgery. They enable minimally invasive procedures, reduce hospital stays, improve recovery, and enhance survival rates among individuals with serious cardiac abnormalities. - Which region dominates the structural heart devices market?

North America dominates the global market with a 45.3% revenue share, supported by advanced healthcare infrastructure, higher prevalence of structural heart diseases, and rapid adoption of innovative technologies. The region also benefits from strong regulatory support and high procedural volumes. - Which region will grow the fastest in the market?

The Asia Pacific region is expected to witness the fastest growth. Rising geriatric populations, improved healthcare access, medical tourism, newborn screening programs, and favorable reimbursement policies are fueling increased adoption of structural heart devices in emerging APAC economies. - What factors are driving market growth?

The market growth is driven by increasing prevalence of cardiovascular diseases, technological advancements, rising demand for minimally invasive procedures, and favorable regulatory approvals. Government initiatives, reimbursement policies, and awareness campaigns are also contributing to sustained market expansion worldwide. - Which market segments hold the largest share?

The heart valve devices segment is projected to hold a 34% share, while replacement procedures account for the largest procedural share at 39%. Among disease types, aortic valve stenosis recorded the highest revenue contribution, highlighting the dominance of valve-related therapies.

Conclusion

The structural heart devices market is poised for sustained growth, supported by rising cardiovascular disease prevalence, technological advancements, and growing adoption of minimally invasive procedures. With North America maintaining dominance and Asia Pacific emerging as the fastest-growing region, opportunities remain strong across developed and developing economies.

Segments such as heart valve devices and replacement procedures are expected to drive the largest market shares, while innovations from leading players continue to expand treatment possibilities. Favorable reimbursement frameworks, enhanced healthcare access, and awareness programs will further accelerate adoption, positioning structural heart devices as a cornerstone in modern cardiac care.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)