Table of Contents

- Introduction

- Editor’s Choice

- Still Wine Market Overview

- Average Revenue Per Capita Generated from Still Wine

- Still Wine Consumption Volume

- Still Wine Price Statistics

- Winery Sales Channels Statistics

- Demographics of Still Wine Consumers

- Consumer Choice Factors in Selecting Wine

- Supply Difficulties in the Wine Industry

Introduction

According to Still Wines Statistics, Still wine, derived from fermented grape juice, is a staple alcoholic beverage produced from various grape varieties.

It includes red, white, rosé, and orange wines, each with distinct flavors and characteristics. Red wines, crafted from dark grapes, offer a range of flavors, from fruity to earthy, while white wines, made from green or yellow grapes, exhibit fruity and floral notes.

Rosé wines, produced with limited skin contact from red grapes, feature a pink hue and diverse flavor profiles. Orange wines, fermented with grape skins, boast an amber color and fuller body.

Terroir, encompassing factors like soil, climate, and winemaking practices, shapes the wine’s unique attributes.

Still wine pairs well with a variety of foods, making it a versatile and beloved choice for wine enthusiasts worldwide.

Editor’s Choice

- The global still wine market revenue is projected to reach USD 363.8 billion in 2028.

- Rosé wine is projected to reach USD 23.3 billion in 2024 and USD 31.3 billion by 2028, while white wine is forecasted to rise to USD 86.4 billion in 2024 and USD 107.1 billion by 2028.

- By 2025, offline sales are anticipated to drop to 96.8%, with online sales increasing to 3.2%, a trend that is expected to remain consistent through 2027.

- The global still wine market revenue varies significantly by country, with the United States leading the market with a revenue of USD 31,230 million.

- By 2028, the prices are projected to reach USD 16.65 for red wine, USD 10.65 for rosé wine, and USD 12.39 for white wine.

- According to wine industry statistics, the highest winery sales channel is the tasting room, accounting for 29% of total sales.

- Among individuals aged 21 to 34 years, who constitute 25.2% of the total population, 19.8% are wine consumers.

Still Wine Market Overview

Global Still Wine Market Size

- The global still wine market has exhibited a fluctuating revenue trend over the past years.

- In 2018, the market revenue stood at USD 290.7 billion, slightly declining to USD 289.1 billion in 2019.

- Projections indicate that the market will continue to grow, with expected revenues of USD 293.4 billion in 2024, USD 310.8 billion in 2025, USD 328.8 billion in 2026, USD 347.4 billion in 2027, and USD 363.8 billion in 2028.

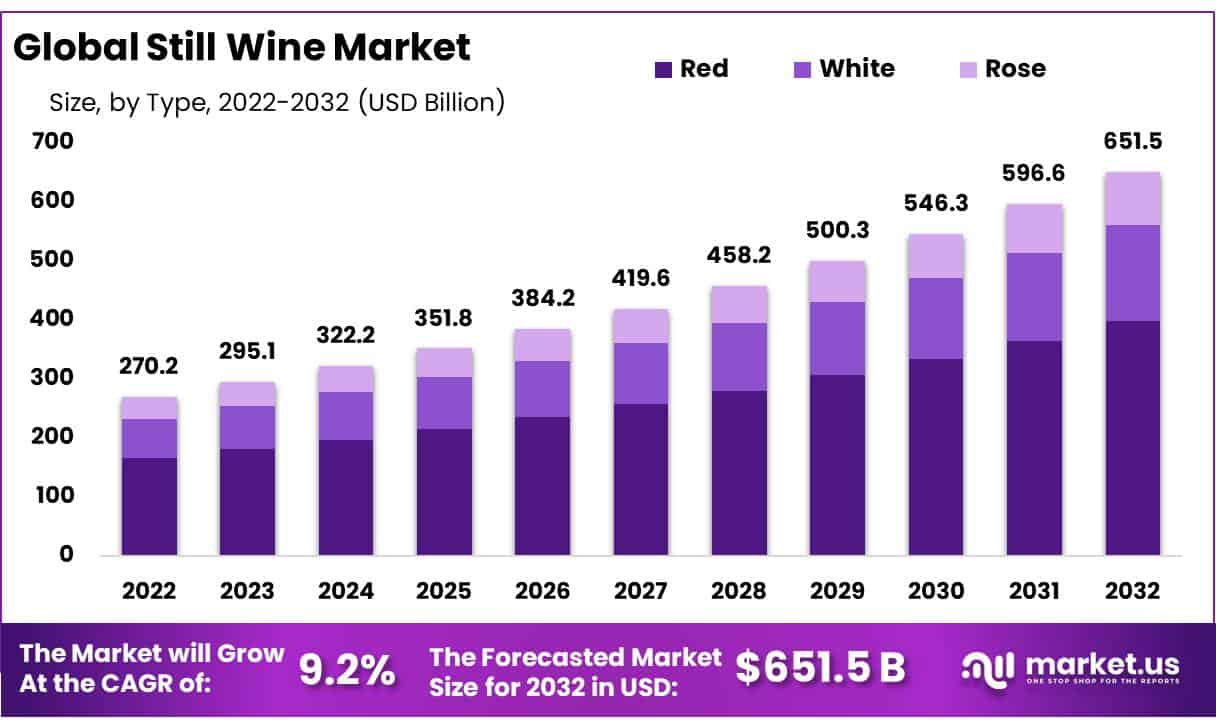

Still Wine Market Size – By Type

- The global still wine market, segmented by type, has shown varied revenue trends across red, rosé, and white wines from 2018 to 2028.

- In 2018, red wine led the market with a revenue of USD 184.2 billion, followed by white wine at USD 85.4 billion and rosé wine at USD 21.1 billion.

- Future projections indicate continued growth, with red wine expected to generate USD 183.8 billion in 2024, USD 194.0 billion in 2025, and USD 225.4 billion by 2028.

- Similarly, rosé wine is projected to reach USD 23.3 billion in 2024 and USD 31.3 billion by 2028, while white wine is forecasted to rise to USD 86.4 billion in 2024 and USD 107.1 billion by 2028.

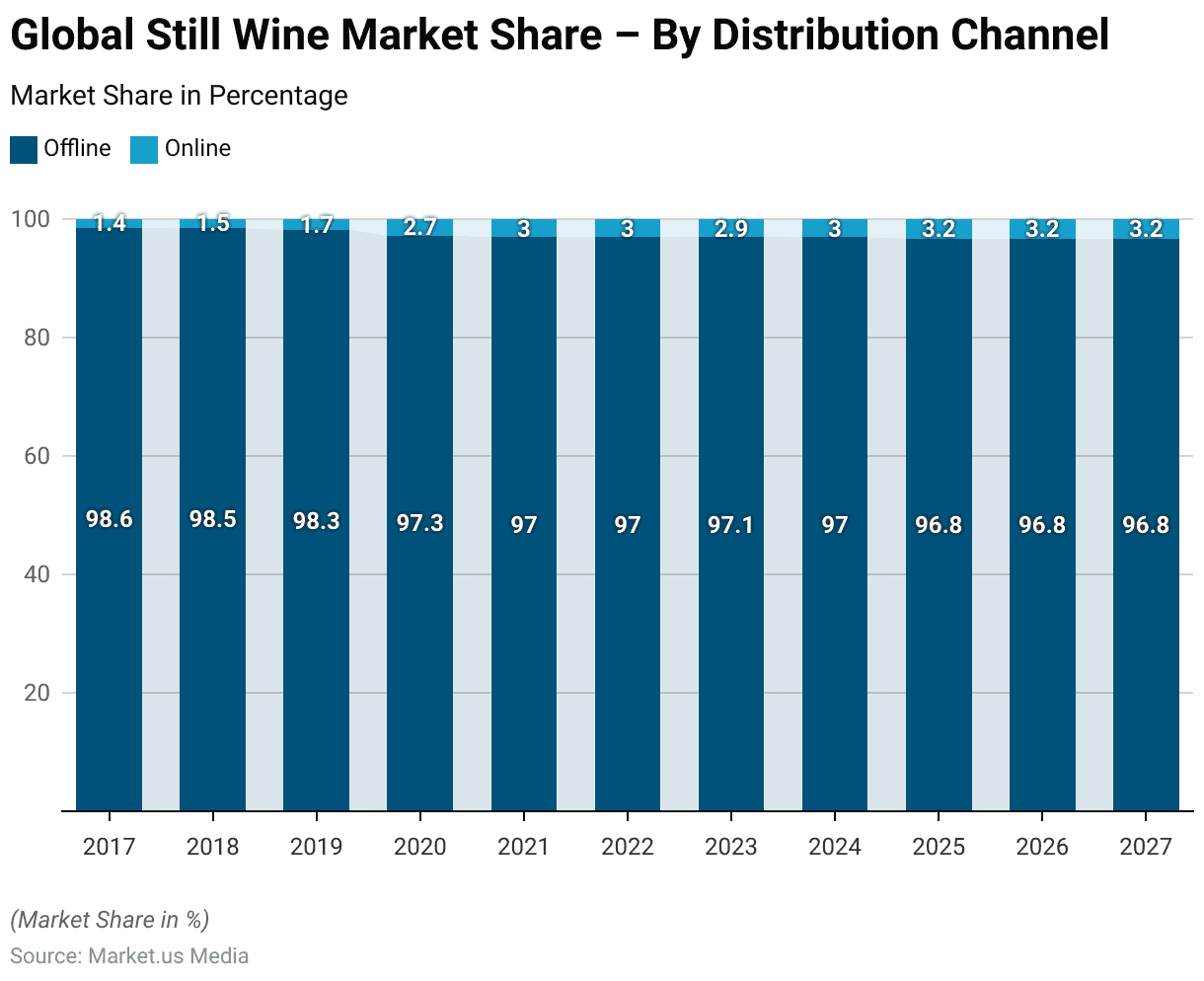

Still Wine Market Share – By Distribution Channel

- The global still wine market share by distribution channel has shown a gradual shift from offline to online sales from 2017 to 2027.

- In 2017, the market was predominantly offline, with 98.6% of sales occurring through this channel, while online sales accounted for only 1.4%.

- By 2025, offline sales are anticipated to drop to 96.8%, with online sales increasing to 3.2%, a trend that is expected to remain consistent through 2027.

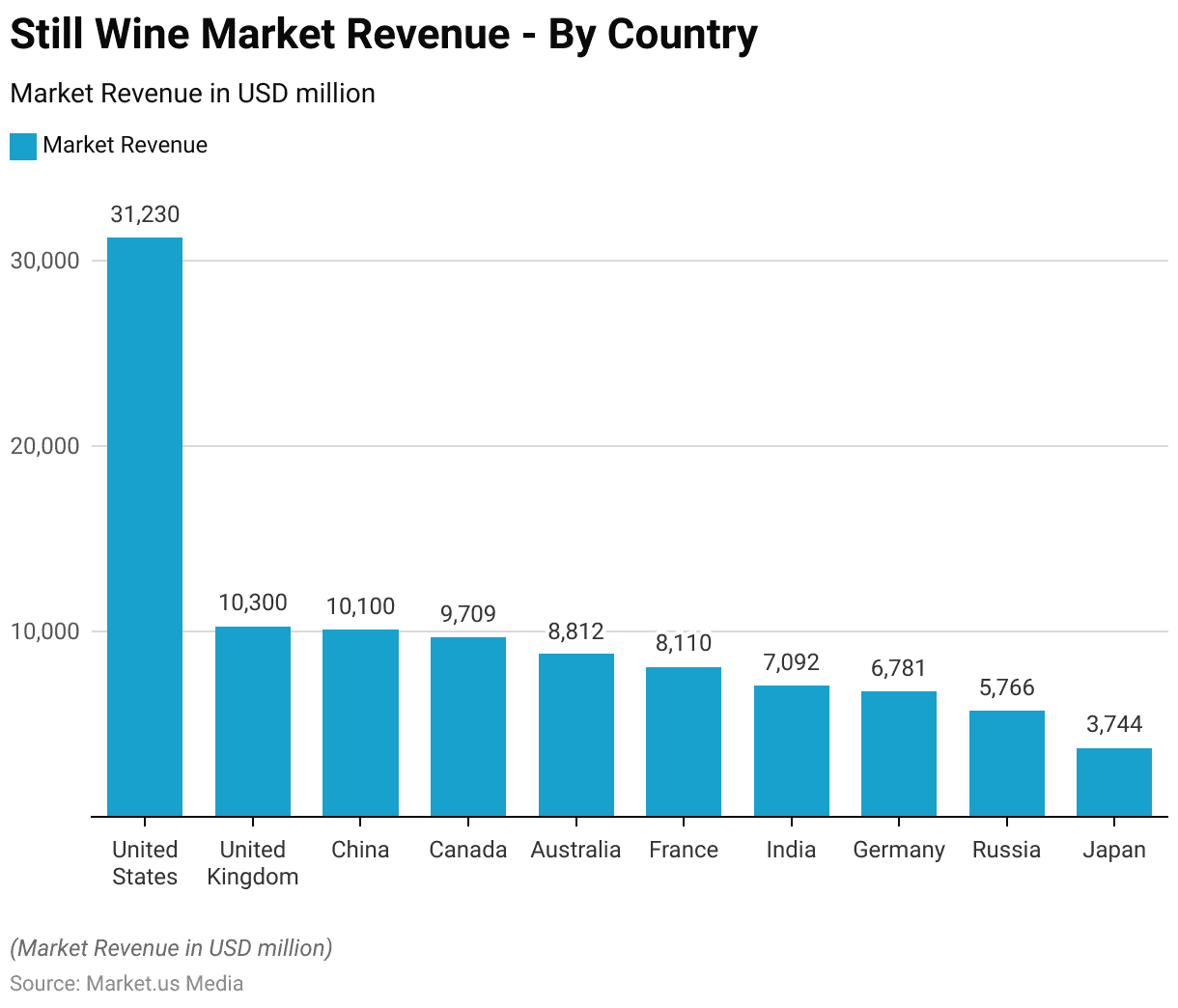

Regional Analysis of the Global Still Wine Market

- The global still wine market revenue varies significantly by country, with the United States leading the market with a revenue of USD 31,230 million.

- The United Kingdom and China follow, generating revenues of USD 10,300 million and USD 10,100 million, respectively.

- Canada also holds a significant share with USD 9,709 million.

- Australia’s still wine market revenue stands at USD 8,812 million, while

- France, known for its rich wine culture, contributes USD 8,110 million.

- India, a growing market for still wine, generates USD 7,092 million.

- Germany’s revenue is USD 6,781 million, and Russia’s is USD 5,766 million.

- Japan, with a still wine market revenue of USD 3,744 million, rounds out the list of top countries in this sector.

Average Revenue Per Capita Generated from Still Wine

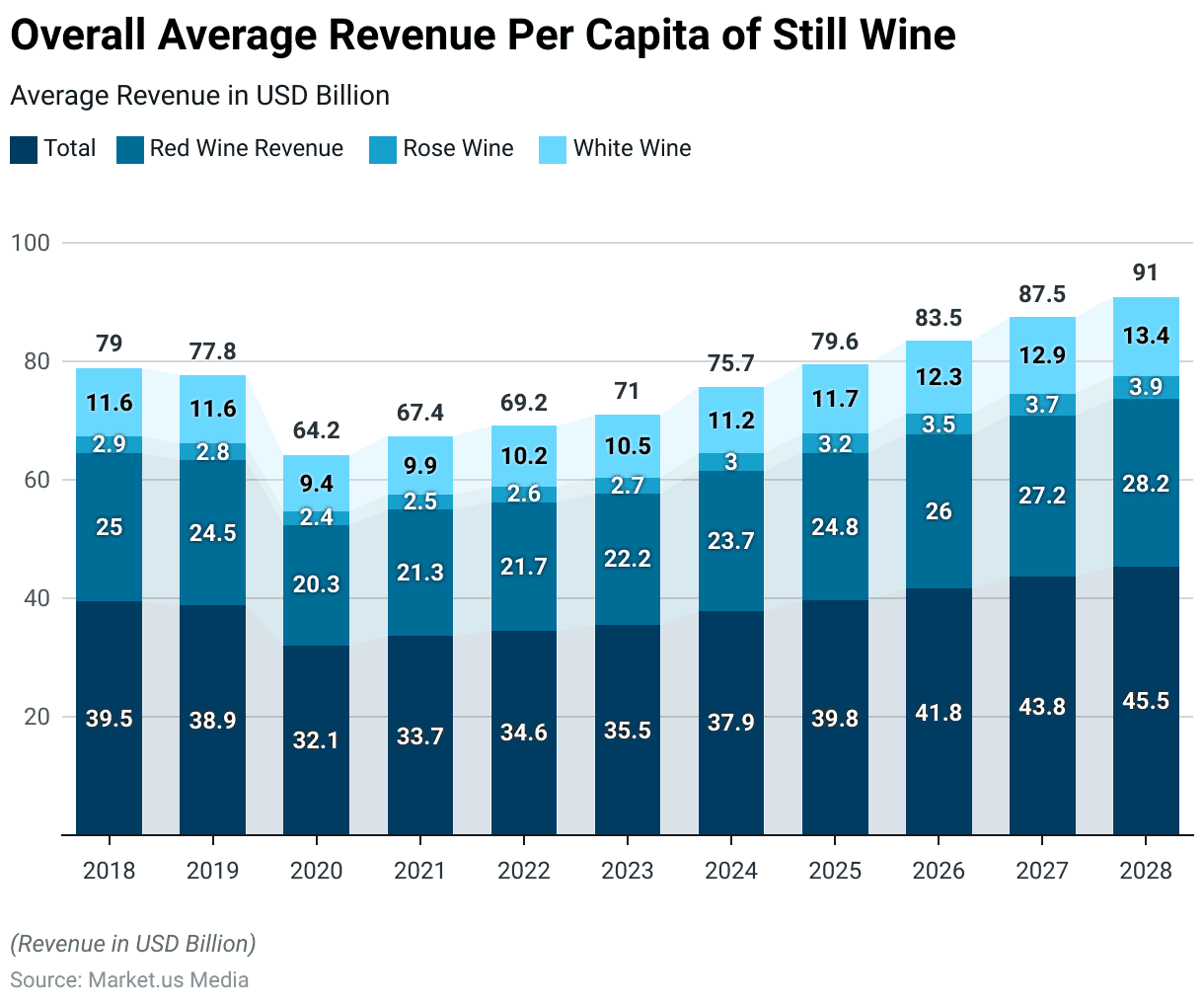

Overall Average Revenue Per Capita

- The global still wine market has displayed discernible fluctuations in average revenue per capita across various wine categories from 2018 to 2028.

- In 2018, total average revenue per capita stood at USD 39.49, with red wine leading at USD 25.02, followed by white wine at USD 11.60 and rosé wine at USD 2.87.

- Projections indicate sustained growth, with the total expected to reach USD 45.48 by 2028, led by red wine at USD 28.18, followed by white wine at USD 13.39, and rosé wine at USD 3.91.

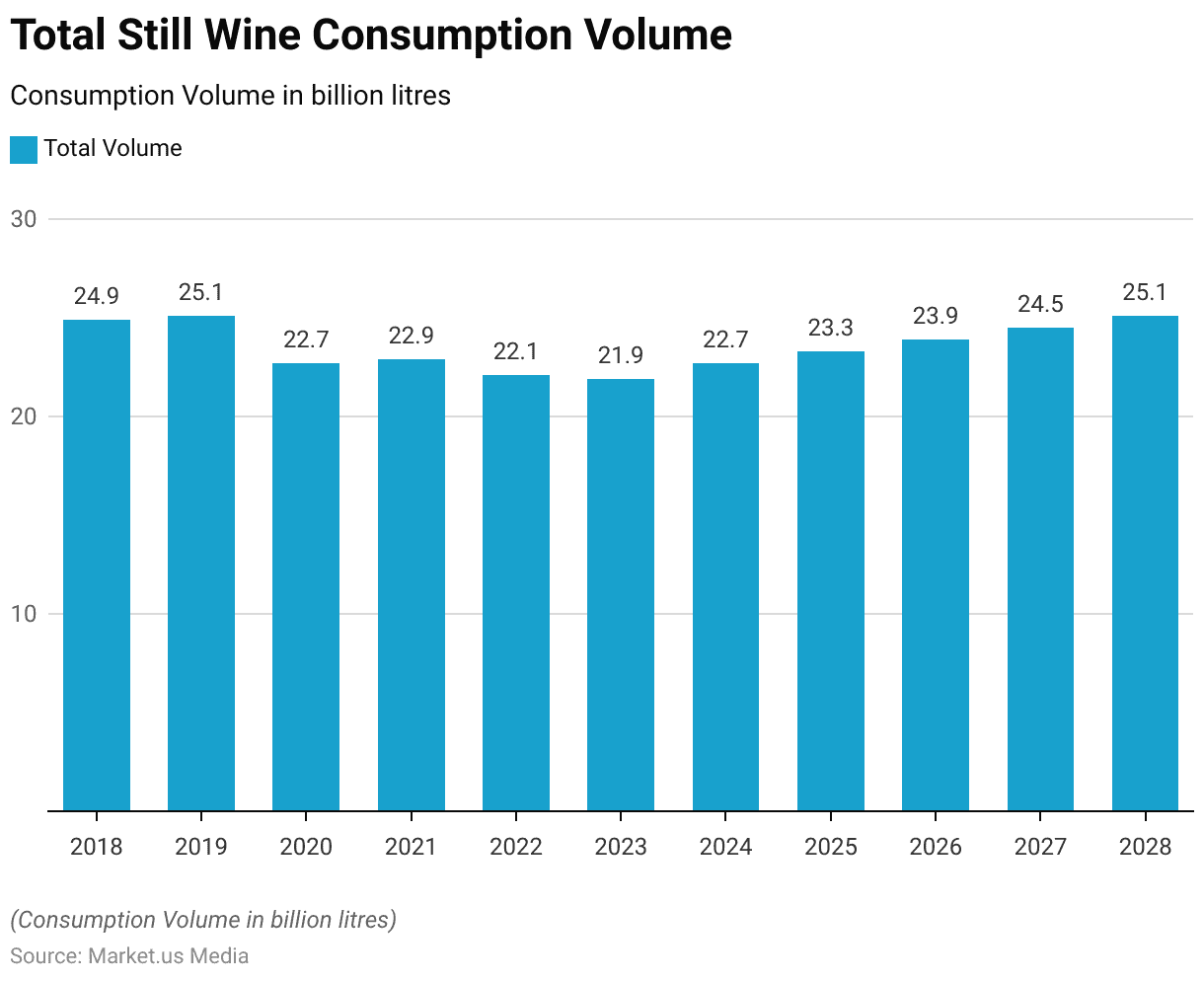

Still Wine Consumption Volume

Total Volume

- The global consumption volume of still wine has shown varying trends from 2018 to 2028.

- In 2018, the total volume consumed was 24.9 billion liters, slightly increasing to 25.1 billion liters in 2019.

- The upward trend is anticipated to continue, reaching 24.5 billion liters in 2027 and returning to 25.1 billion liters by 2028.

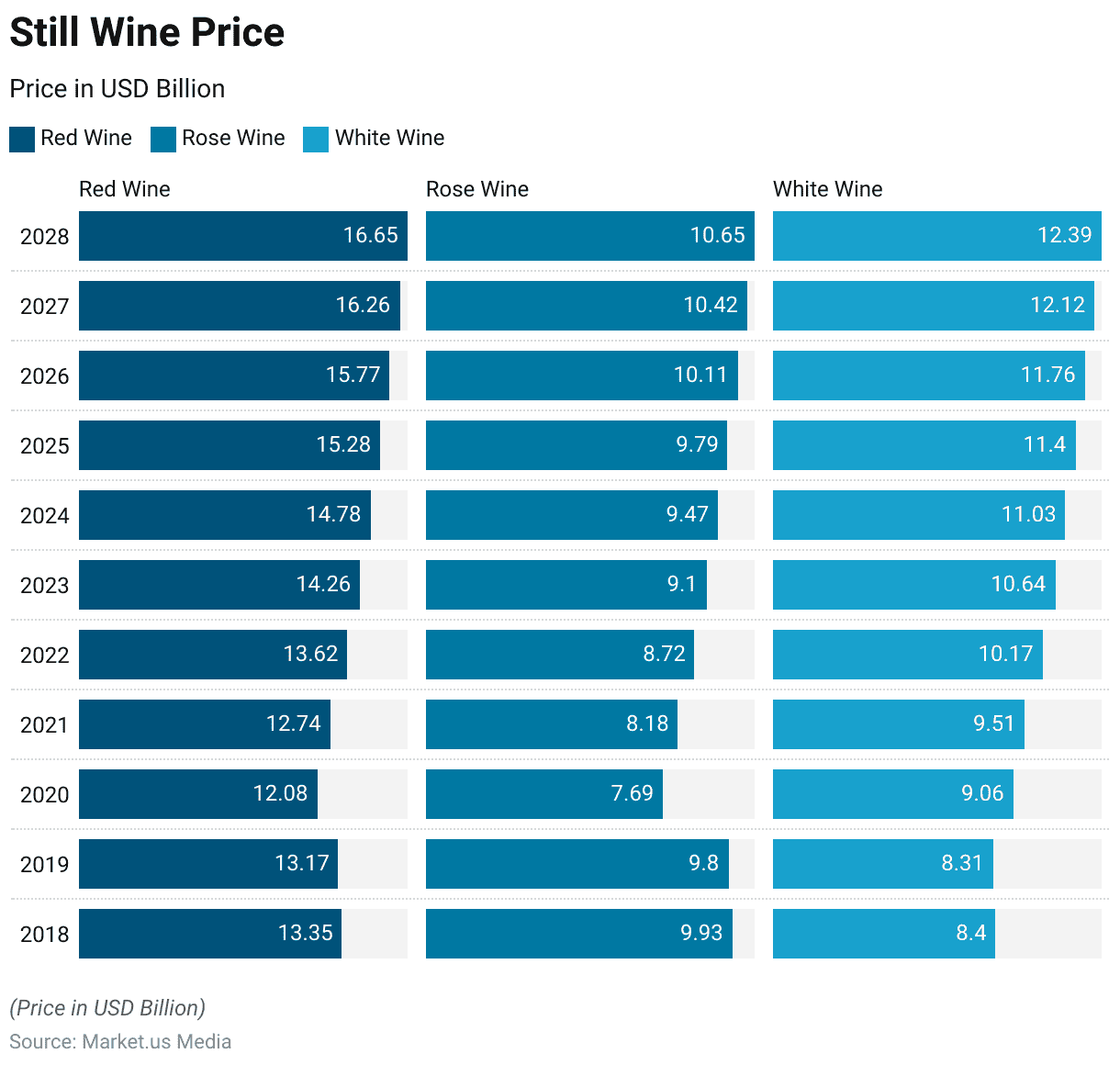

Still Wine Price Statistics

- The prices of still wine have shown varied trends across red, rosé, and white wines from 2018 to 2028.

- In 2018, the price of red wine was USD 13.35, rosé wine USD 9.93, and white wine USD 8.40.

- Finally, by 2028, the prices are projected to reach USD 16.65 for red wine, USD 10.65 for rosé wine, and USD 12.39 for white wine.

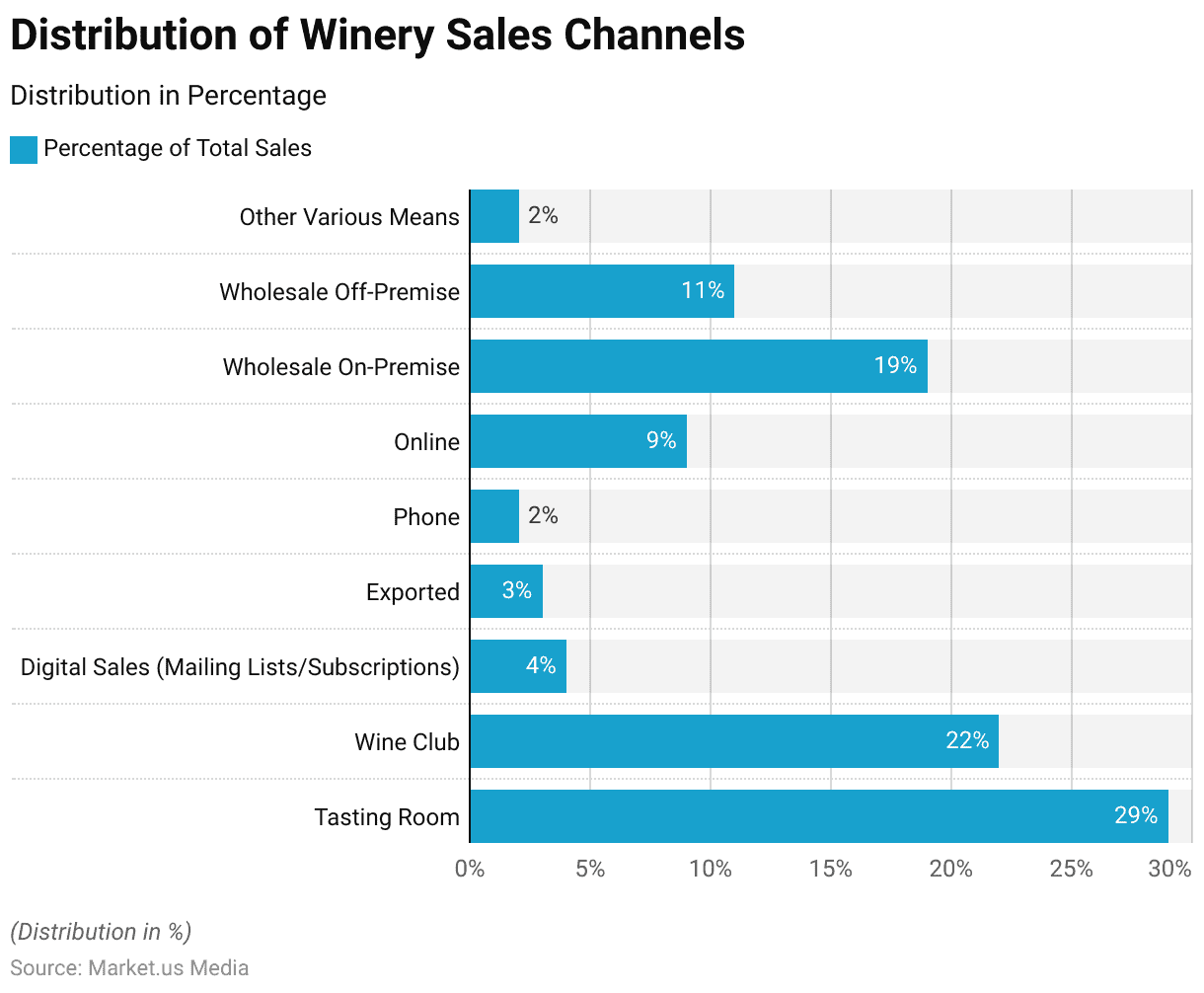

Winery Sales Channels Statistics

- According to wine industry statistics, the highest winery sales channel is the tasting room, accounting for 29% of total sales.

- Wine clubs contribute to 22% of the overall sales.

- Digital sales, including those from mailing lists or subscriptions, represent 4% of the market.

- Other sales channels include exported sales at 3%, phone sales at 2%, online sales at 9%, wholesale on-premise sales at 19%, and wholesale off-premise sales at 11%.

- Additionally, various other means account for 2% of the overall winery sales channels.

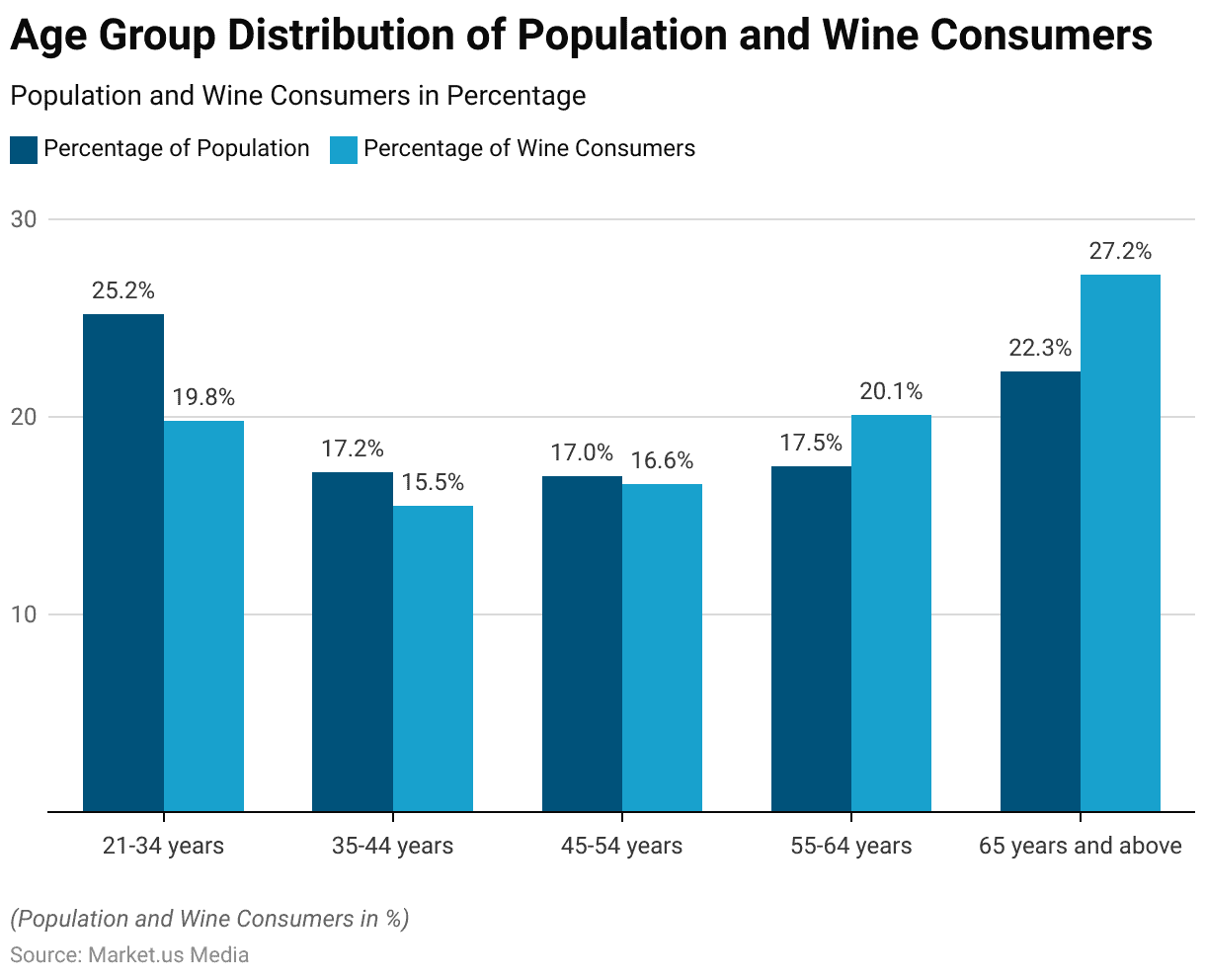

Demographics of Still Wine Consumers

By Age

- The wine consumption demographics reveal distinct trends across various age groups.

- Among individuals aged 21 to 34 years, who constitute 25.2% of the total population, 19.8% are wine consumers.

- In the 35 to 44 years age group, 15.5% of wine consumers belong to the 17.2% of the population in this age bracket.

- The 45 to 54 years age group shows a minor difference between the overall population (17.0%) and wine consumers (16.6%).

- For those aged 55 to 64 years, 17.5% of the population accounts for a higher percentage of wine consumers at 20.1%.

- Notably, the population aged 65 years and above, which represents 22.3% of the total population, has the highest proportion of wine consumers at 27.2%.

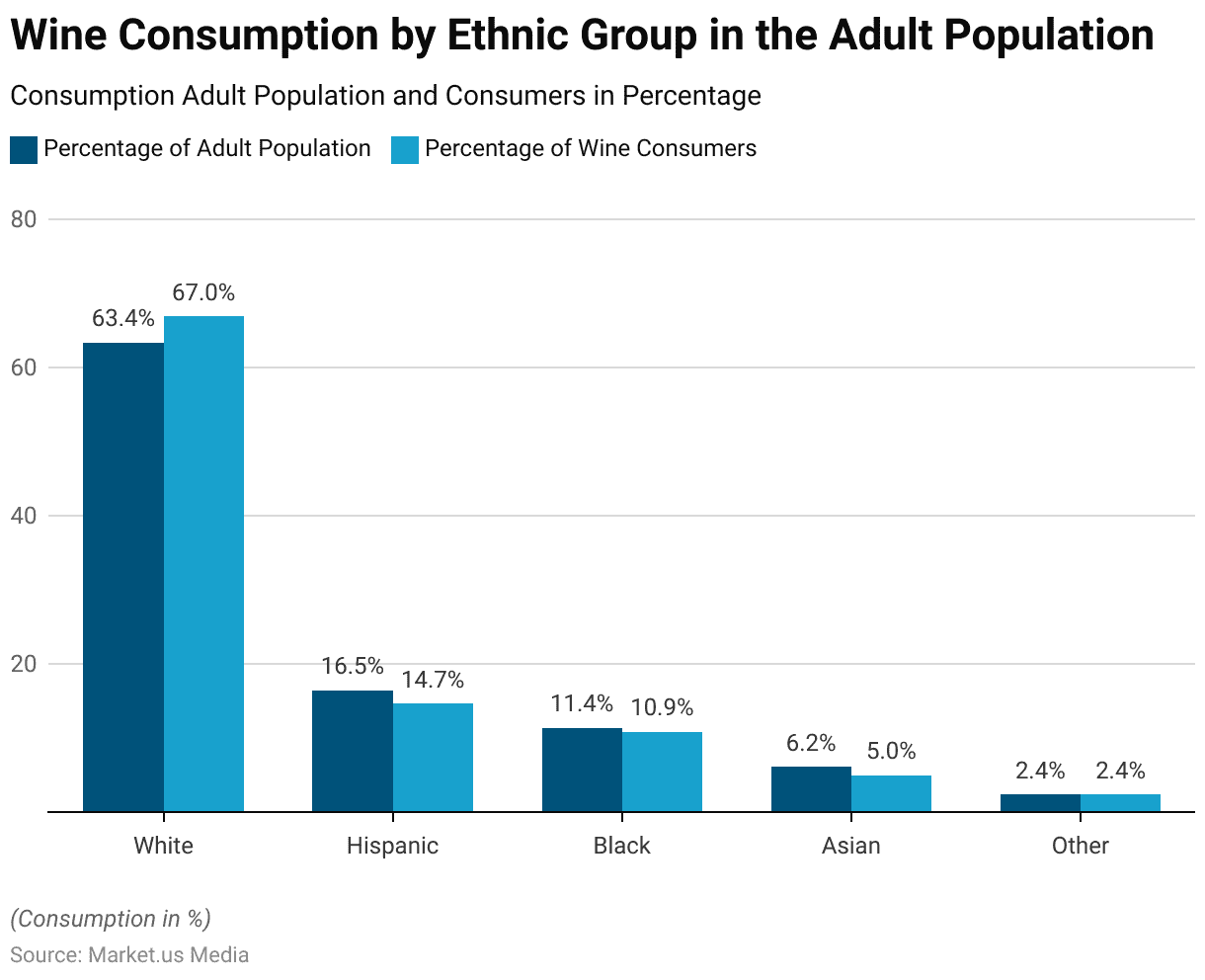

By Ethnicity

- The distribution of wine consumption among different ethnic groups shows distinct patterns.

- White people comprise 63.4% of the adult population and represent 67% of wine consumers.

- Hispanic people account for 16.5% of the adult population, with 14.7% being wine drinkers.

- Black people make up 11.4% of the adult population, and 10.9% are wine consumers.

- Among Asian people, 6.2% of the adult population corresponds to 5% of wine consumers.

- Other ethnic groups have a similar share of the adult population and wine consumers, both at 2.4%.

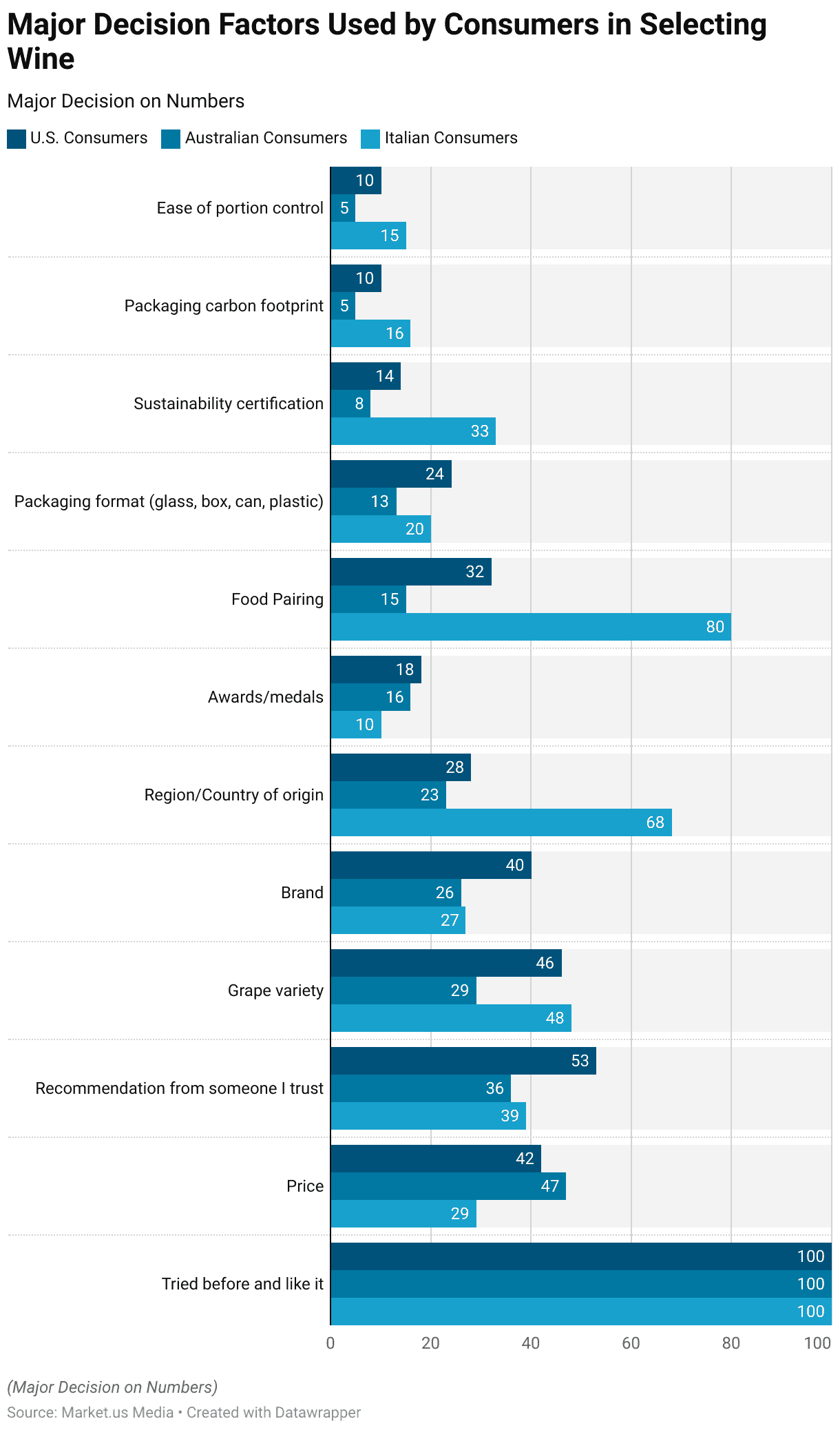

Consumer Choice Factors in Selecting Wine

- When selecting wine, consumers in the U.S., Australia, and Italy consider various decision factors with differing levels of importance.

- Universally, all consumers prioritize having tried the wine before and liking it, each scoring a perfect 100.

- Price is a significant factor, with U.S. consumers rating it at 42, Australians at 47, and Italians at 29.

- Recommendations from trusted sources are more influential among U.S. (53) and Italian (39) consumers compared to Australians (36).

- Grape variety holds high importance for Italian consumers (48), moderately for U.S. consumers (46), and less so for Australians (29). Brand importance scores are 40 for U.S. consumers, 26 for Australians, and 27 for Italians.

- The region or country of origin is highly significant for Italian consumers (68) but less so for U.S. (28) and Australian (23) consumers.

- Awards and medals have lower importance scores, with 18 for U.S. consumers, 16 for Australians, and 10 for Italians.

- Food pairing is notably important for Italian consumers (80), while U.S. (32) and Australian (15) consumers rate it lower.

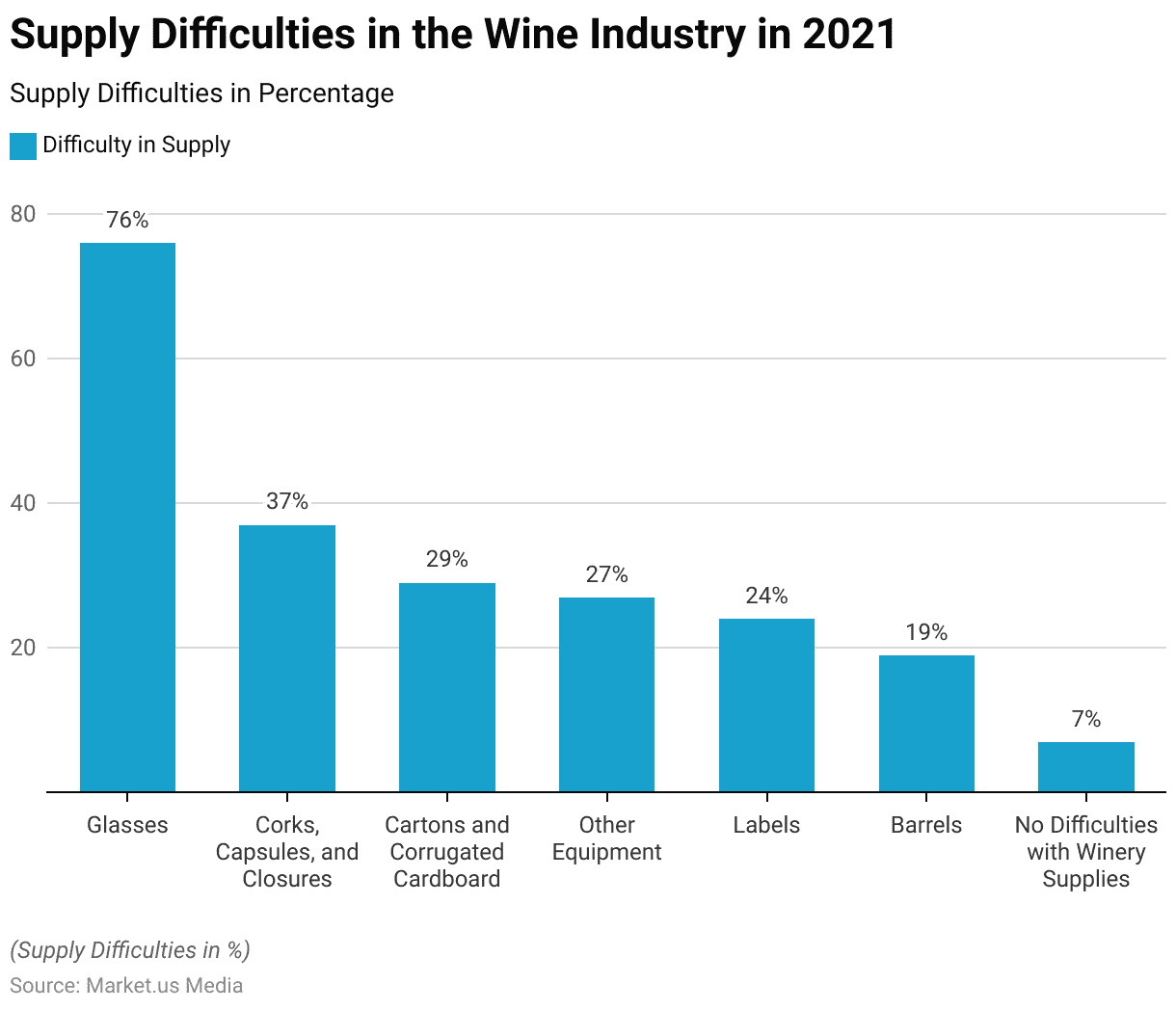

Supply Difficulties in the Wine Industry

- As of 2021, the wine industry faced significant supply challenges, with glasses being the most difficult to supply, as reported by 76% of respondents.

- Corks, capsules, and closures followed, with a 37% difficulty rate.

- Cartons and corrugated cardboard recorded a 29% difficulty rate.

- Other equipment required in wineries had a supply difficulty rate of 27%.

- Labels and barrels were also challenging to supply, with difficulty rates of 24% and 19%, respectively.

- Notably, 7% of respondents reported no difficulties with winery supplies.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)