Table of Contents

Overview

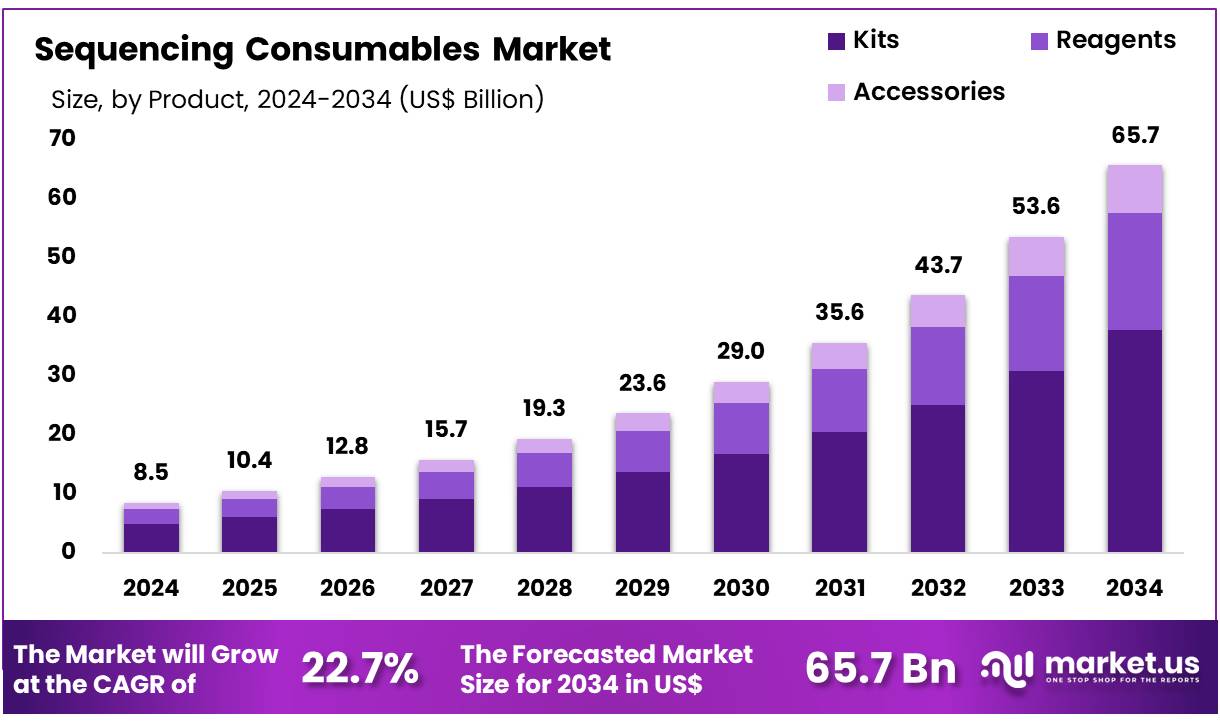

New York, NY – Nov 27, 2025 – Global Sequencing Consumables Market size is expected to be worth around US$ 65.7 billion by 2034 from US$ 8.5 billion in 2024, growing at a CAGR of 22.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 47.3% share with a revenue of US$ 4.0 Billion.

The global sequencing consumables market is experiencing steady expansion as the adoption of high-throughput sequencing technologies increases across clinical, research, and industrial domains. Growth of the market is being driven by the rising use of genomic workflows, expansion of precision medicine programs, and higher demand for reliable, high-quality consumables that support continuous sequencing operations. Consumables such as library preparation kits, reagents, flow cells, and sample preparation materials are being utilized more widely due to the increasing volume of genomic data generated worldwide.

Industry uptake has been reinforced by advancements in next-generation sequencing platforms, which require a consistent supply of standardized consumables to maintain accuracy, sensitivity, and throughput. The market has also benefited from the growing prevalence of genetic disorders and oncology applications, where sequencing is being adopted as a core diagnostic and monitoring tool. As a result, healthcare institutions and research laboratories have increased procurement of sequencing consumables to support clinical workflows and translational research programs.

Strategic collaborations between reagent manufacturers, sequencing platform developers, and research institutions have further strengthened product innovation. The introduction of automation-ready kits and high-efficiency reagents has improved workflow productivity, while cost optimization efforts have supported broader market penetration.

Future growth is expected to be supported by expanding investments in genomics infrastructure, national genome initiatives, and the rapid integration of sequencing in infectious disease surveillance. The market is positioned for sustained progress as consumables remain essential inputs for all sequencing-based applications.

Key Takeaways

- The sequencing consumables market generated US$ 8.5 billion in revenue in 2024, and with a CAGR of 22.7%, the market is projected to reach US$ 65.7 billion by 2033.

- The product segment comprises kits, reagents, and accessories, with kits dominating in 2024 by accounting for 57.6% of the total market share.

- Based on technology, the market is categorized into 3rd generation, 2nd generation, and 1st generation sequencing, where 2nd generation sequencing held the largest share of 55.4%.

- In terms of application, the market is segmented into cancer diagnostics, reproductive health diagnostics, pharmacogenomics, infectious disease diagnostics, agrigenomics, and others, with cancer diagnostics leading the segment at 54.9% revenue share.

- The end-use segment includes hospitals & laboratories, academic research institutes, pharmaceutical & biotechnology companies, and others, and hospitals & laboratories accounted for 59.8% of the market share.

- North America emerged as the leading regional market, capturing 47.3% of the global share in 2024.

Segmentation Analysis

- Product Analysis: In 2023, the kits segment accounted for 57.6% of total revenue, supported by rising demand for high-throughput sequencing and improved sample preparation efficiency. Kits provide integrated workflow solutions that simplify sequencing protocols. Continued development of platform-specific and application-focused kits is expected to strengthen adoption in clinical diagnostics. The growing emphasis on personalized medicine further contributes to sustained utilization across research and healthcare environments.

- Technology Analysis: Second-generation sequencing technology, or next-generation sequencing (NGS), represented 55.4% of the market in 2023 due to its favorable cost structure, scalability, and accuracy. This technology enables high-throughput applications such as whole-genome and transcriptome sequencing. Ongoing technological advancements and declining sequencing costs are anticipated to reinforce demand for second-generation consumables. Its established presence in clinical, academic, and commercial settings is expected to maintain its dominant position throughout the forecast period.

- Application Analysis: The cancer diagnostics segment held a 54.9% share, driven by the expanding role of genomic testing in cancer detection, classification, and therapeutic decision-making. Sequencing-based tumor profiling supports precision treatment strategies by identifying individual genetic mutations. As personalized oncology continues to advance, reliance on sequencing consumables is projected to increase. Rising global cancer incidence and wider adoption of targeted therapies are expected to accelerate integration of sequencing into routine oncology workflows.

- End-Use Analysis: Hospitals and laboratories led the market with a 59.8% share in 2023, reflecting rapid integration of sequencing technologies into clinical diagnostics and research operations. These institutions remain central to genomic testing for disease characterization, treatment planning, and biomarker identification. Demand is strengthened by the growing shift toward precision medicine and continuous reductions in sequencing costs. Increasing investments by healthcare organizations to build genomic infrastructure are expected to drive substantial segment expansion.

Regional Analysis

North America as the Leading Market for Sequencing Consumables

North America accounted for the largest revenue share of 47.3% in the sequencing consumables market, supported by substantial investment in genomics research and broader clinical adoption of sequencing technologies. Continued funding from organizations such as the U.S. National Institutes of Health (NIH) for major sequencing initiatives, including the Human Pangenome Project, contributed significantly to the consumption of reagents, library preparation kits, and related materials.

Integration of sequencing into routine clinical diagnostics further strengthened regional demand, particularly in oncology and infectious disease monitoring. The Centers for Disease Control and Prevention (CDC) demonstrated extensive sequencing activity, processing more than 270,000 SARS-CoV-2 genomic sequences in 2022, which indicated high volumes of consumables required to sustain these workflows.

In addition, research institutions and universities across the United States and Canada expanded sequencing programs throughout 2024, reinforcing the continuous need for consumables such as reagents, flow cells, and preparation kits. This combined rise in research and clinical applications acted as a major catalyst for market dominance in North America.

Asia Pacific Expected to Register the Fastest CAGR

The Asia Pacific region is projected to record the highest CAGR over the forecast period, driven by strong governmental support for precision medicine and large-scale genomics programs. China’s national genomics initiative is expected to involve large investments in sequencing infrastructure, resulting in increased demand for consumables.

India’s Genome India Project, aimed at sequencing a broad population cohort, is anticipated to require substantial volumes of reagents and kits. Countries such as South Korea and Japan are also expanding genomics research and clinical sequencing efforts, further contributing to regional growth.

Improving healthcare infrastructure and rising awareness of personalized medicine across emerging Asia Pacific economies indicate sustained demand for sequencing technologies and essential consumables, positioning the region for significant future expansion.

Frequently Asked Questions on Sequencing Consumables

- Why are sequencing consumables important in genomics?

Sequencing consumables support each workflow stage, from library preparation to data generation, ensuring high accuracy, reproducibility, and throughput. Their role is critical because sequencing platforms depend on these inputs to maintain quality performance, sensitivity, and efficiency in advanced genomic analysis. - What types of sequencing consumables are commonly used?

Common consumables include library prep kits, reagents, buffers, sequencing chips, flow cells, and quality control materials. Their usage varies depending on platform chemistry, sample complexity, and research objectives, enabling consistent results across clinical diagnostics, life sciences research, and personalized medicine applications. - How do sequencing consumables impact data quality?

Data accuracy is strongly influenced by the purity, stability, and efficiency of consumables used during sample preparation and sequencing runs. High-quality consumables reduce contamination risks, enhance read lengths, and improve reproducibility, supporting reliable decision-making in clinical and research environments. - What factors influence the cost of sequencing consumables?

Costs are affected by reagent composition, platform compatibility, throughput requirements, and vendor pricing models. Increased adoption of high-throughput sequencers and specialized kits contributes to higher expenditure, while economies of scale and automation solutions gradually reduce overall operational costs. - Which end-user segments dominate the sequencing consumables market?

Major end users include academic research centers, clinical laboratories, pharmaceutical companies, and biotechnology firms. Their procurement is driven by large-scale sequencing projects, translational medicine programs, and routine diagnostic workflows that depend heavily on reliable consumables to maintain operational continuity. - Which regions are expected to lead market expansion?

North America and Europe are expected to dominate market share due to strong research infrastructure and funding, while Asia-Pacific is projected to record faster growth. Increased investments in precision medicine and expanding diagnostic capabilities support regional market advancement. - What trends are shaping the future of the sequencing consumables market?

The market is shaped by automation, miniaturized consumable formats, integrated cartridge systems, and growing adoption of single-cell sequencing. Sustainable packaging and cost-efficient reagent chemistries are also emerging as priorities, supporting improved scalability and broader clinical adoption.

Conclusion

The global sequencing consumables market is positioned for sustained expansion as demand for high-throughput genomic workflows continues to rise across clinical, research, and industrial settings. Growth is supported by broader adoption of precision medicine, increasing utilization of next-generation sequencing technologies, and continuous advancements in kits and reagents that enhance workflow efficiency.

Strong investments in national genomics initiatives and expanding applications in oncology, infectious disease surveillance, and population-scale studies further reinforce market momentum. North America maintains leadership, while Asia Pacific is expected to grow rapidly. Overall, sequencing consumables remain essential components driving scalable and reliable genomic analysis worldwide.