Table of Contents

Overview

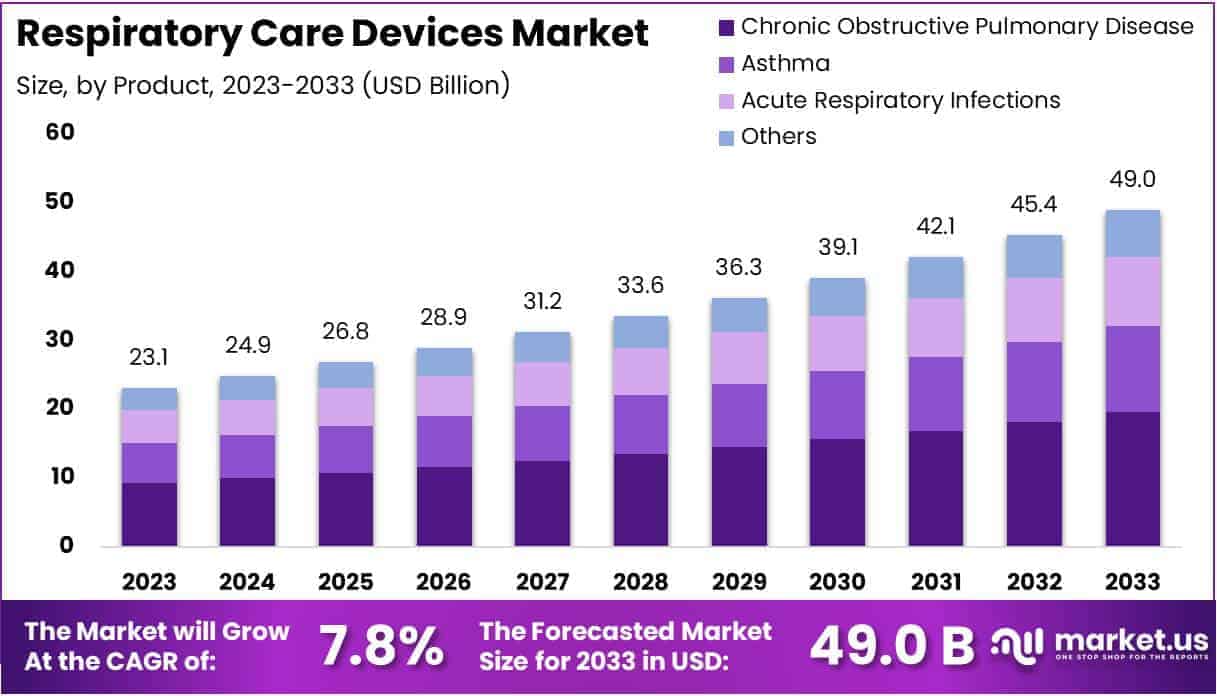

New York, NY – July 23, 2025 – The Respiratory Care Devices Market size is expected to be worth around USD 49.0 billion by 2033 from USD 23.1 billion in 2023, growing at a CAGR of 7.8% during the forecast period 2024 to 2033.

The global Respiratory Care Devices market is witnessing strong growth, driven by the rising prevalence of chronic respiratory diseases such as asthma, chronic obstructive pulmonary disease (COPD), and sleep apnea. The increasing geriatric population, rising air pollution levels, and the impact of infectious diseases like COVID-19 have significantly amplified the demand for advanced respiratory support technologies.

Respiratory care devices include therapeutic, monitoring, diagnostic, and consumable products that are essential for managing pulmonary conditions. Key product segments include nebulizers, ventilators, oxygen concentrators, CPAP devices, and spirometers. These technologies help improve patient outcomes by enabling precise diagnosis, continuous monitoring, and effective respiratory therapy.

Hospitals, home care settings, and ambulatory care centers are the primary end-users adopting these devices to ensure timely and efficient care. The shift toward home-based respiratory care and the integration of smart technologies such as IoT-enabled monitoring are further contributing to market expansion.

North America currently dominates the market due to advanced healthcare infrastructure and high disease awareness, while the Asia Pacific region is expected to witness the fastest growth owing to rising healthcare investments and improving access to respiratory care.

With technological innovation and growing global health concerns, the respiratory care devices market is projected to sustain long-term growth, ensuring improved respiratory health outcomes across diverse patient populations.

Key Takeaways

- In 2023, the global Respiratory Care Devices market was valued at USD 23.1 billion, and it is projected to reach USD 49.0 billion by 2033, expanding at a compound annual growth rate (CAGR) of 7.8% during the forecast period.

- Based on product type, the market is segmented into mechanical ventilators, respiratory consumables, oxygen concentrators, positive airway pressure (PAP) devices, nebulizers, polysomnography devices, pulse oximeters, and spirometers. Among these, oxygen concentrators dominated the segment in 2023, accounting for a 33.5% share of the total market revenue.

- By application, the market is categorized into chronic obstructive pulmonary disease (COPD), acute respiratory infections, asthma, and others. The COPD segment emerged as the leading application area, contributing 40% of the market share in 2023.

- In terms of end-users, the market includes hospitals, clinics, ambulatory surgical centers (ASCs), and others. Hospitals held the largest share, representing 47.5% of the market in 2023 due to their advanced respiratory care infrastructure.

- Regionally, North America led the global market, capturing a 39.6% share in 2023, supported by high healthcare spending, technological advancement, and increased awareness of respiratory conditions.

Segmentation Analysis

- Product Type Analysis: The oxygen concentrators segment dominated the respiratory care devices market in 2023, accounting for a 33.5% share. This growth is driven by the increasing prevalence of COPD and asthma, which require long-term oxygen therapy. Technological advancements have improved the efficiency and usability of concentrators, especially portable models suited for home-based care. The growing aging population and rising demand for non-hospital treatment options are expected to further propel the adoption of oxygen concentrators globally.

- Application Analysis: Chronic obstructive pulmonary disease (COPD) accounted for 40% of the application segment in 2023, making it the leading contributor. The rising global burden of COPD, largely due to tobacco use, air pollution, and occupational exposures, has elevated the need for effective respiratory care devices. Increased awareness, earlier diagnosis, and a focus on disease management have spurred demand for specialized devices. Continued innovations in therapy delivery systems are expected to support improved outcomes in COPD management.

- End-user Analysis: Hospitals held the largest share in 2023, representing 47.5% of the end-user segment. This dominance is attributed to the rising incidence of severe respiratory conditions requiring complex interventions. Hospitals are increasingly investing in advanced respiratory technologies to support intensive care, emergency response, and postoperative respiratory support. Expansion of critical care units and respiratory therapy departments, along with growing emphasis on patient safety and clinical outcomes, is expected to sustain high demand for these devices in hospital settings.

Market Segments

By Product Type

- Mechanical Ventilators

- Respiratory Consumables

- Oxygen Concentrators

- Positive airway pressure devices

- Nebulizers

- Polysomnography Devices

- Pulse Oximeters

- Spirometers

By Application

- Chronic Obstructive Pulmonary Disease

- Acute Respiratory Infections

- Asthma

- Others

By End-user

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Others

Regional Analysis

North America led the global respiratory care devices market in 2023, securing the highest revenue share of 39.6%. This dominance is primarily attributed to the increasing prevalence of chronic respiratory conditions and continuous advancements in healthcare technologies. According to the American Lung Association (February 2023), more than 34 million people in the United States are affected by chronic lung diseases such as COPD, asthma, chronic bronchitis, and emphysema.

The substantial disease burden has fueled demand for advanced respiratory care solutions. Market growth in the region is supported by heightened awareness, improved diagnostic capabilities, robust healthcare infrastructure, and favorable insurance coverage. In addition, increased healthcare spending and the introduction of technologically advanced devices have further contributed to the region’s strong market position.

The Asia Pacific region is projected to exhibit the highest compound annual growth rate (CAGR) over the forecast period. A notable example includes the Bolivian government’s selection of CANTA oxygen concentrators in November 2022 for public hospitals in La Paz, which underscores the growing reliance on high-quality respiratory equipment sourced from Asia.

Market expansion in Asia Pacific is driven by rising rates of respiratory disorders, growing investments in healthcare infrastructure, and the adoption of advanced medical technologies. Enhanced access to innovative devices and supportive government policies are expected to accelerate regional growth. Furthermore, CANTA Medical’s global presence in over 120 countries reflects Asia Pacific’s increasing influence in the international respiratory care market.

Emerging Trends

- Enhanced Performance Standards: Regulatory bodies have intensified focus on device safety and accuracy. In January 2025, the FDA issued draft guidance detailing non clinical and clinical performance testing requirements for pulse oximeters, emphasizing standardized evaluation methods and labeling recommendations for medical purposes. This trend can be attributed to concerns over device variability in diverse patient populations.

- Expansion of Oxygen Equipment Supply: Global health agencies have scaled up distribution of oxygen devices. As of February 2021, WHO and partners had delivered over 30000 oxygen concentrators and 40000 pulse oximeters across 121 countries, including 37 classified as “fragile,” to address critical oxygen shortages during the COVID 19 pandemic. The growth in supply reflects a shift toward ensuring baseline respiratory support in low resource settings.

- Rise of AI Enabled Respiratory Monitoring: Artificial intelligence is increasingly integrated into respiratory devices. The FDA’s AI Enabled Medical Device List—updated as recently as last week now includes multiple respiratory monitoring systems that employ AI algorithms for signal analysis and predictive alerts. This development supports real time decision support and may improve early detection of respiratory distress.

- Advancement in Non invasive Ventilation Equipment: Standards for high flow nasal cannula (HFNC) devices have been formally recognized. In June 2025, the FDA adopted ISO80601-2-12, defining safety and essential performance criteria for respiratory HFNC equipment used with spontaneously breathing patients. This underscores a trend toward more sophisticated non invasive ventilation modalities outside the intensive care unit.

- Focus on Accessibility in Remote and Low Resource Areas: Surveys have highlighted persistent gaps in medical gas availability: a 2020 WHO survey in Somalia found that only 4% of health facilities had oxygen concentrators and 22% had oxygen cylinders. In response, international programs are prioritizing the deployment of compact, portable concentrators and simplified oxygen delivery kits suitable for clinics with unreliable power and limited infrastructure.

Use Cases

- Home Management of Chronic Lung Disease: Self administered devices enable patients with COPD and asthma to manage symptoms outside hospitals. In 2021, an estimated 14.2million U.S. adults (6.5%) had physician diagnosed COPD, and in 2023, 8.9% of adults reported current asthma. Home oxygen concentrators and smart inhalers allow dose tracking and remote monitoring, reducing exacerbations and hospital readmissions.

- Acute Respiratory Support in Hospitals: Mechanical ventilators and high flow systems remain critical in intensive care. During the COVID 19 pandemic, the FDA issued Emergency Use Authorizations to expand ventilator availability and accessories, supporting treatment of severe respiratory distress in thousands of hospitalized patients.

- Sleep Apnea Treatment: Continuous Positive Airway Pressure (CPAP) devices are standard for obstructive sleep apnea therapy. Training materials from WHO webinars in 2022 outline proper CPAP setup and use, reflecting the role of CPAP machines in sleep clinics and home therapy to maintain airway patency throughout the night.

- Emergency Medical Services: Portable ventilators and oxygen systems are increasingly standard in ambulances. Although no longer under shortage for adult devices, pediatric ventricular assist bypass systems remain scarce, indicating continued reliance on compact ventilators for pre hospital stabilization of critical patients.

- Remote Patient Monitoring: Pulse oximeters and telemonitoring platforms facilitate tracking of vital respiratory parameters. In 2023, the rate of physician office visits with asthma as the first listed diagnosis was 304.4 per 10000 persons, illustrating the demand for continuous monitoring outside the hospital setting. Integration with telehealth allows clinicians to adjust therapy based on home measured SpO2 and respiratory rate data.

Conclusion

The global respiratory care devices market is poised for sustained growth, driven by the rising burden of chronic respiratory diseases, aging populations, and technological advancements. Increasing demand for home-based care, regulatory emphasis on device safety, and AI integration are reshaping the industry.

North America leads the market, while Asia Pacific is expected to witness the fastest growth. Expanded access to devices in low-resource settings and the adoption of non-invasive solutions highlight the sector’s evolution. With growing awareness and innovation, respiratory care devices will remain essential for improving patient outcomes and supporting global respiratory health across diverse care environments.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)