Table of Contents

Overview

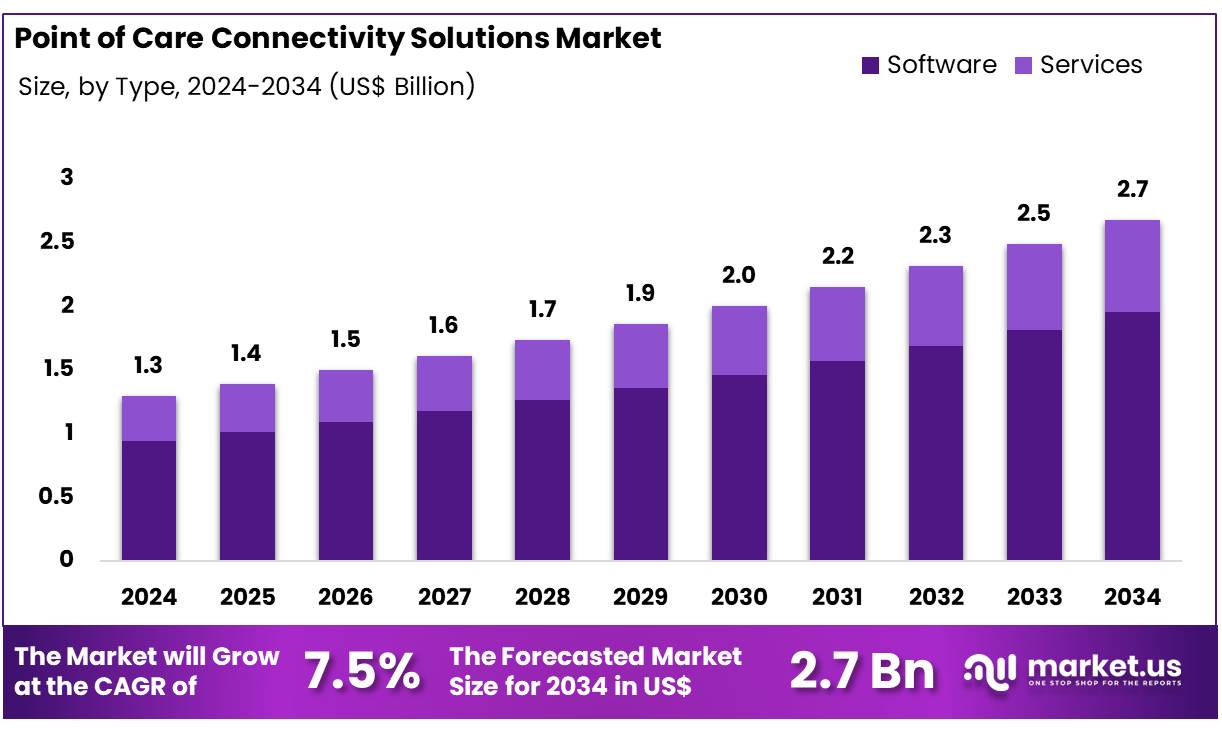

New York, NY – Nov 03, 2025 – Global Point of Care Connectivity Solutions Market size is expected to be worth around US$ 2.7 Billion by 2034 from US$ 1.3 Billion in 2024, growing at a CAGR of 7.5% during the forecast period from 2024 to 2034. In 2023, North America led the market, achieving over 31% share with a revenue of US$ 0.4 Billion.

Point-of-care connectivity solutions have been positioned as a transformative component in modern healthcare delivery. Enhanced interoperability, real-time data transmission, and automated diagnostic workflows have significantly improved clinical decision-making and error reduction.

The growth of this market can be attributed to rising digital health adoption, increased demand for rapid diagnostics, and the integration of advanced analytics. Improved patient monitoring and streamlined data management have strengthened operational efficiency across care settings.

Ongoing investments in healthcare IT infrastructure and regulatory support for connected medical systems are expected to sustain momentum. As digital transformation accelerates, point-of-care connectivity will remain central to efficient, patient-centric care models.

Key Takeaways

- The global Point of Care Connectivity Solutions market achieved a valuation of USD 1.3 billion in 2024. The market is projected to expand to approximately USD 2.7 billion by 2034, reflecting a compound annual growth rate of 7.5%.

- The software segment dominated the global landscape in 2024, accounting for nearly 73% of the total revenue contribution.

- Hospitals and clinics emerged as the leading end-use segment, capturing approximately 32% of the overall revenue share in 2024.

- The glucose monitoring category held the largest share among applications, contributing around 17% to the market during the same year.

- North America sustained its position as the foremost regional market in 2024, with a revenue share exceeding 31%.

Regional Analysis

North America accounted for a major share of the Point of Care (PoC) connectivity solutions market, supported by a robust healthcare infrastructure, widespread use of digital health technologies, and consistent investment in healthcare modernization. The U.S. remains a key contributor, backed by a structured healthcare ecosystem that emphasizes technological innovation, improved patient management, and workflow optimization.

The region’s emphasis on cost reduction and enhanced clinical outcomes continues to drive the deployment of PoC connectivity platforms. Growing integration of cloud-based services within healthcare systems is further strengthening market expansion. Favorable reimbursement frameworks and strong regulatory support additionally reinforce North America’s leading market position.

Adoption of public cloud technologies has risen notably. According to HIPAA Journal insights, healthcare organizations used an average of 19 public cloud services in 2019, increasing to 24 by 2022. This growth indicates a rising dependence on cloud solutions to securely store, process, and exchange patient information.

Emerging Trends

- Real-time, Secure Data Exchange and Interoperability: The public health environment is transitioning toward instant and secure exchange of clinical and device data. National initiatives, including the CDC’s Public Health Data Strategy, promote rapid information flow between care providers and public health agencies. Widespread adoption of standardized frameworks such as HL7 FHIR is being driven by federal policies, enabling seamless movement of clinical data across systems without additional user burden.

- Mobile and Remote Health Integration: Mobile devices, biosensors, and handheld platforms are increasingly used to expand point-of-care connectivity toward patient-centered environments. The World Health Organization’s digital health roadmap emphasizes mobile health as a means to improve affordability and care accessibility, especially in underserved regions. Advances in microfluidics and sensor engineering now allow diagnostic devices to integrate with mobile applications for real-time support in chronic disease management and telehealth operations.

- Standards-based Device Communication and Security: Growing focus on interoperability is enhancing adoption of standards such as ISO/IEEE 11073 for plug-and-play communication of clinical devices. These frameworks guide real-time data exchange and secure network connectivity at the bedside. Regulatory authorities, including the FDA, are strengthening cybersecurity guidance for connected medical technologies to safeguard patient information and maintain safety as digital integration accelerates.

Use Cases

- Syndromic Surveillance through Emergency Department Data: The CDC’s National Syndromic Surveillance Program gathers real-time information from connected emergency departments to monitor infectious diseases and urgent public health events. As of May 2024, participation reached 78% of U.S. emergency departments, enabling timely assessment of respiratory illness trends and early outbreak identification. Weekly analytics contribute to informed public health responses for conditions including COVID-19, influenza, and RSV.

- Continuous Glucose Monitoring for Diabetes Care: Connected continuous glucose monitoring systems transmit patient glucose readings directly to care teams and electronic records, supporting advanced diabetes self-management. Usage rose from 0.4% in 2014 to 4.1% in 2020 in the United States, indicating expanding adoption of connected monitoring devices. Furthermore, 87.6% of insulin-using adults with diabetes reported daily glucose tracking, reflecting strong reliance on digital tools for timely clinical oversight.

Frequently Asked Questions on Point of Care Connectivity Solutions

- What are Point of Care (PoC) Connectivity Solutions?

Point of Care connectivity solutions are digital systems designed to link diagnostic devices, electronic health records, and clinical information platforms. These solutions enable real-time data exchange, streamline workflows, and support faster clinical decision-making at patient care locations. - How do PoC connectivity solutions improve healthcare delivery?

Healthcare delivery is improved through automated data transfer, reduced manual errors, and enhanced patient monitoring. Clinicians gain immediate access to testing results, enabling faster treatment decisions and improved patient management across hospital, clinic, and remote care environments. - Which technologies are commonly used in PoC connectivity solutions?

Technologies include wireless communication networks, middleware platforms, cloud-based systems, and secure data integration protocols. These components enable seamless connectivity between medical devices, laboratory systems, and healthcare information technology platforms for efficient data transmission and interoperability. - Why are PoC connectivity solutions important in modern healthcare systems?

PoC connectivity solutions support efficient clinical workflows, improve diagnostics accuracy, and enhance patient safety. They enable clinicians to receive automated and accurate test results, reducing turnaround times and optimizing resource use in hospitals and diagnostic centers. - What is the PoC connectivity solutions market?

The Point of Care connectivity solutions market encompasses technology providers offering software, hardware, and integration platforms for connecting diagnostic devices to health information systems. Market growth is driven by increasing digitization, rising demand for rapid diagnostics, and expanding healthcare investments. - What factors are driving growth in the PoC connectivity solutions market?

Growth is attributed to expanding adoption of digital health solutions, increasing emphasis on patient data accuracy, rising chronic disease prevalence, and technological advancements. Investments in healthcare IT infrastructure and demand for faster diagnostics further support global market expansion. - Which end-user segment leads the PoC connectivity solutions market?

Hospitals represent the dominant end-user segment, driven by higher patient volumes, advanced medical infrastructure, and greater adoption of integrated clinical data systems. Clinics, diagnostic laboratories, and long-term care facilities are also increasing deployment of connectivity platforms. - What role does cloud technology play in PoC connectivity solutions?

Cloud technology plays a significant role in secure data storage, remote access, and real-time information sharing. Healthcare providers benefit from scalable infrastructure, improved system interoperability, and reduced maintenance requirements, supporting efficient data management across care settings.

Conclusion

The point-of-care connectivity solutions market is experiencing sustained expansion, supported by the increasing adoption of digital health technologies, advanced analytics, and interoperable medical systems. Significant improvements in real-time data exchange, diagnostic efficiency, and patient monitoring have strengthened clinical workflows and care coordination.

Rising healthcare digitization, favorable policy support, and investment in connected infrastructure continue to drive market momentum across regions, particularly in North America.

As standards-based communication, cloud integration, and cybersecurity frameworks evolve, point-of-care connectivity will remain integral to modern healthcare delivery, enabling patient-centric models and enhancing operational performance in hospitals, clinics, and remote care environments.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)