Table of Contents

Overview

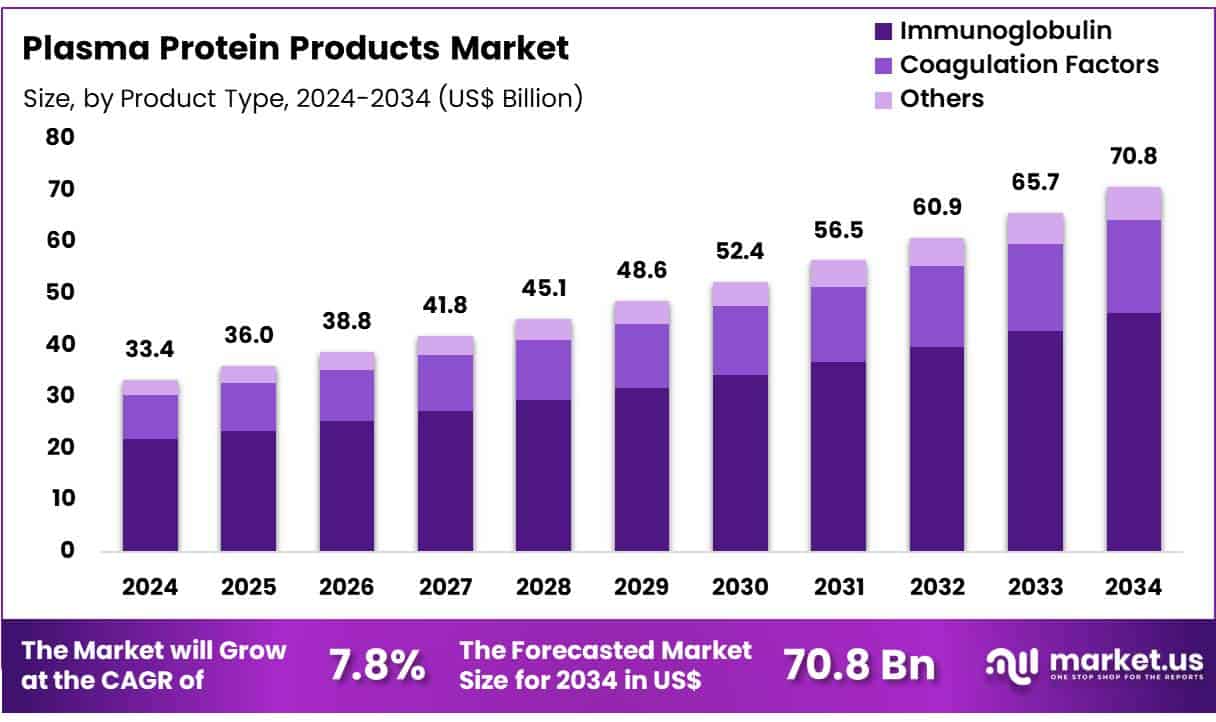

Global Plasma Protein Products Market size is expected to be worth around US$ 70.8 Billion by 2034 from US$ 33.4 Billion in 2024, growing at a CAGR of 7.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.4% share with a revenue of US$ 12.8 Billion.

The global Plasma Protein Products market is experiencing consistent growth, supported by increasing clinical demand for therapies targeting immune deficiencies, bleeding disorders, and critical care conditions. These life-saving products derived from human plasma play an essential role in treating a wide range of chronic and acute medical conditions.

Key plasma-derived products include immunoglobulins, coagulation factors, and albumin. Each serves a vital function in medical care strengthening the immune response, managing hereditary bleeding disorders such as hemophilia, and maintaining blood volume in trauma or surgical cases. Continuous advancements in plasma fractionation technologies and improved safety protocols have enhanced both the quality and availability of these therapies.

Healthcare systems across North America, Europe, and Asia-Pacific are increasingly adopting plasma protein treatments as part of routine and emergency medical practice. Growing awareness of rare diseases and increased investment in healthcare infrastructure have further contributed to market expansion, particularly in emerging economies.

Supportive regulatory environments, expansion in plasma collection networks, and ongoing clinical research are expected to sustain market growth. As the global healthcare landscape evolves, plasma protein products will remain indispensable in both therapeutic innovation and life-saving patient care.

Key Takeaways

- In 2024, the plasma protein products market demonstrated robust performance, generating substantial revenue with a steady growth trajectory. The market is projected to nearly double by 2034, driven by the increasing demand for specialized plasma-derived therapies.

- By product type, the market is segmented into immunoglobulin, coagulation factors, and others. Immunoglobulin emerged as the dominant segment in 2023, accounting for the largest market share due to its widespread application in immune-related disorders.

- In terms of application, the market is categorized into hospitals, retail pharmacies, and others. Hospitals constituted the primary end-use setting, capturing a significant portion of the market share, attributed to the rising number of inpatient treatments and reliance on plasma-derived therapies in critical care.

- Regionally, North America held the leading position in 2023, supported by advanced healthcare infrastructure, high plasma collection rates, and favorable reimbursement policies. This regional dominance is further reinforced by continuous clinical adoption and regulatory support for plasma-based treatments.

Segmentation Analysis

- Product Type Analysis: Immunoglobulin accounts for the largest market share of 65.3% in the plasma protein products segment. This is attributed to its essential role in treating immune deficiencies, autoimmune conditions, and inflammatory diseases. The rising incidence of disorders like primary immunodeficiency (PID), improved diagnosis rates, and continued advancements in immunoglobulin formulations are supporting this segment’s growth. Additionally, increasing acceptance among healthcare providers and targeted therapy developments are expected to maintain immunoglobulin’s dominant market position.

- Application Analysis: Hospitals dominate the plasma protein products market with a 70.2% share, primarily due to their capacity to handle complex plasma-based treatments. These facilities provide access to trained professionals and advanced equipment required for administering therapies to patients with chronic conditions like hemophilia and immune deficiencies. Rising hospital admissions, the evolution of healthcare infrastructure, especially in emerging economies, and the expansion of specialized treatment protocols are all contributing to the sustained demand for plasma protein products in hospital settings.

Market Segments

By Product Type

- Immunoglobulin

- Coagulation Factors

- Others

By Application

- Hospitals

- Retail Pharmacy

- Others

Regional Analysis

North America Maintains Leadership in the Plasma Protein Products Market

North America led the global plasma protein products market with a revenue share of 38.4%, supported by rising diagnoses of rare diseases, growing awareness of therapeutic benefits, and increased plasma collection efforts. Plasma-derived treatments are vital for managing primary immunodeficiencies, hemophilia, and alpha-1 antitrypsin deficiency, contributing to this regional dominance.

The demand for intravenous immunoglobulins (IVIg) remains strong due to the rising prevalence of neurological and immunological disorders. CSL Behring, a major player, reported a 10% revenue increase for the half-year ending December 31, 2024, driven by immunoglobulin sales and improved supply chains. Grifols also highlighted continued momentum in its Biopharma division, including plasma therapies, with strong performances across 2023 and 2024. Takeda’s Plasma-Derived Therapies (PDT) Immunology segment significantly contributed to its financial growth in 2024, reflecting robust demand across North America.

Asia Pacific Expected to Record Fastest Growth Rate

Asia Pacific is projected to witness the highest compound annual growth rate during the forecast period, driven by expanding healthcare infrastructure, improved diagnostic capabilities, and rising medical awareness of plasma therapies. Government efforts to strengthen blood and plasma management systems are further supporting this trend.

In 2023, China recorded 16.99 million voluntary blood donations a 5.9% increase from 2022 according to the National Health Commission. This growth in plasma supply directly supports the manufacture of plasma-derived medicines. Meanwhile, Japan’s Ministry of Health, Labour and Welfare continues to enforce stringent oversight of blood products to ensure quality and safety.

Leading pharmaceutical companies are expanding regional operations. Takeda, with a strong presence in Asia Pacific, is expected to leverage its manufacturing capabilities and product pipeline to meet growing demand. As healthcare access improves and chronic disease management becomes a policy priority, the adoption of plasma protein therapies is anticipated to accelerate across the region.

Emerging Trends

- Steady Growth in Immunoglobulin Demand: The demand for intravenous and subcutaneous immunoglobulin products was growing at an average rate of 8–9% per year prior to the COVID-19 pandemic, driven by expanding indications and wider patient access.

- Concentration of Global Plasma Supply: In 2019, the global plasma collection volume reached approximately 69 million liters, with 67% supplied by the United States, highlighting a pronounced regional imbalance in source plasma availability.

- Shift Toward Patient-Friendly SC-IgG: Subcutaneous immunoglobulin formulations have gained traction due to ease of home administration, with peak serum levels achieved in 2–4 days and bioavailability exceeding 60%.

- Supply Disruptions from the SARS-CoV-2 Pandemic: Plasma collections declined by 14.5% in 2020 compared to 2019, underscoring vulnerabilities in the plasma supply chain during global health crises.

Use Cases

- Replacement Therapy in Primary Immunodeficiency: Immunoglobulin replacement is the standard of care for primary immunodeficiency diseases, which occur in approximately 1 in 2,000 to 1 in 10,000 live births; nearly 40% of affected individuals are under 18 years of age.

- Long-Term Therapy with SC-IgG: Subcutaneous immunoglobulin is administered weekly or biweekly, with absorption profiles showing peak concentrations within 2–4 days and bioavailability above 60%, facilitating stable trough levels for chronic management.

- Prophylactic Management in Hemophilia: Regular infusions of plasma-derived clotting factor concentrates have reduced bleeding complications; prophylaxis use rose from about one-third of patients in 1999 to 50% by 2010, with 75% of those under 20 years on preventive regimens by 2010.

Conclusion

The plasma protein products market is poised for sustained growth, driven by rising clinical demand, expanding diagnostic capabilities, and increased global awareness of plasma-derived therapies. Immunoglobulin remains the dominant product type, while hospitals continue to serve as the primary application segment.

North America leads the market, with Asia Pacific showing the fastest growth potential. Emerging trends such as subcutaneous immunoglobulin formulations and enhanced plasma collection systems are shaping the market’s evolution. With ongoing innovations, robust use cases, and improving healthcare infrastructure, plasma protein products are expected to remain essential in the treatment of rare and chronic conditions globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)