Table of Contents

Overview

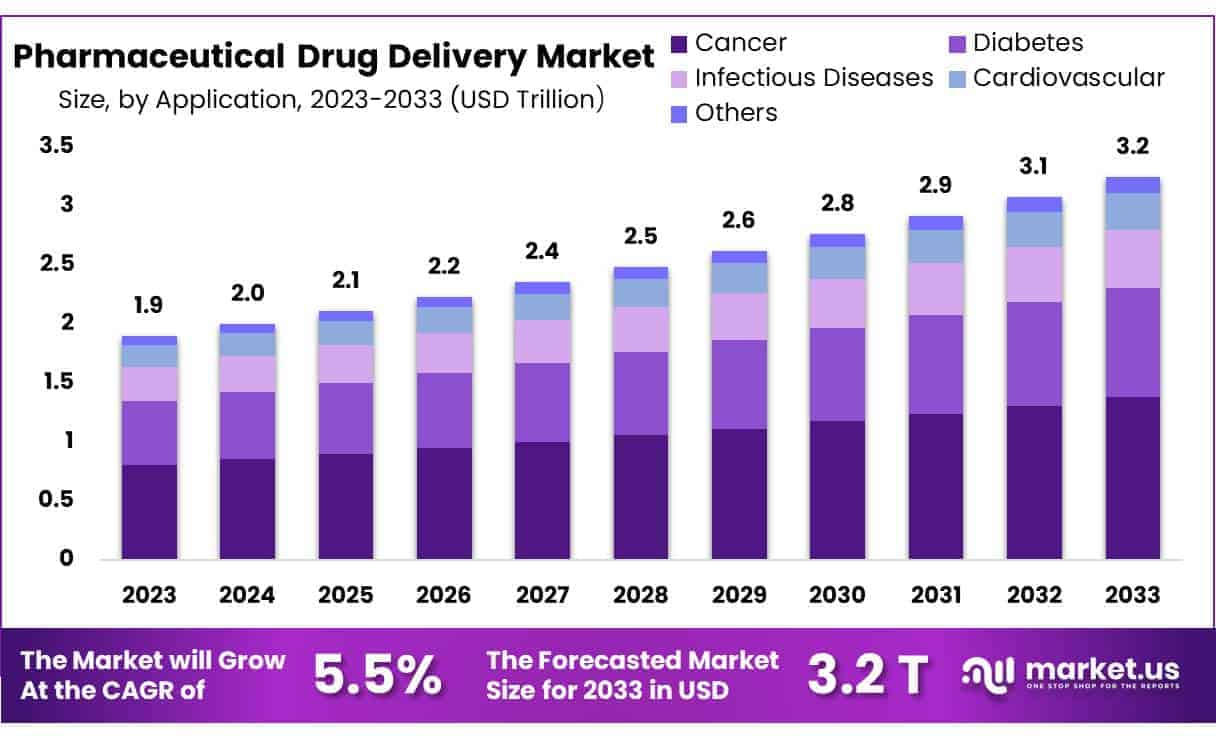

New York, NY – May 13, 2025 – Global Pharmaceutical Drug Delivery Market size is expected to be worth around US$ 3.2 trillion by 2033 from US$ 1.9 trillion in 2023, growing at a CAGR of 5.5% during the forecast period 2024 to 2033.

Pharmaceutical drug delivery refers to the method and technology by which therapeutic substances are administered to achieve a desired clinical effect in patients. It plays a critical role in enhancing drug efficacy, minimizing side effects, and improving patient compliance. Drug delivery systems are designed to control the rate, time, and place of release of drugs in the body, making treatment more targeted and effective.

The industry encompasses a wide range of delivery routes, including oral, injectable, transdermal, inhalation, and ocular methods. Among these, oral drug delivery remains the most widely used due to its ease of administration and high patient acceptability. However, innovations in sustained-release formulations, nanotechnology, and targeted delivery systems are expanding capabilities across all routes.

The global pharmaceutical drug delivery market is witnessing significant growth, driven by the rising prevalence of chronic diseases, increasing demand for biologics, and advancements in personalized medicine. Hospitals and specialty clinics remain primary end-users, supported by expanding healthcare infrastructure and evolving treatment protocols.

In addition, regulatory approvals for novel delivery technologies and the integration of digital health platforms are fostering a dynamic innovation landscape. As healthcare shifts towards more patient-centric models, drug delivery technologies are becoming central to the development of next-generation therapeutics, ensuring safer, faster, and more effective treatments across various medical conditions.

Key Takeaways

- Market Size: The global pharmaceutical drug delivery market is projected to reach approximately US$ 3.2 trillion by 2033, increasing from US$ 1.9 trillion in 2023.

- Market Growth: The market is expected to grow at a compound annual growth rate (CAGR) of 5.5% over the forecast period from 2024 to 2033.

- Route of Administration Analysis: In 2023, the oral drug delivery segment held the largest market share at 55.7%. This dominance is attributed to the increasing preference for non-invasive, convenient, and cost-effective administration methods among patients and healthcare providers.

- Application Analysis: The cancer treatment segment accounted for a significant market share of 42.5% in 2023. This growth reflects the rising global burden of cancer and the growing emphasis on targeted therapies and drug delivery innovations in oncology.

- End-Use Analysis: Hospitals emerged as the dominant end-user in 2023, contributing 64.1% of total market revenue. Their leadership is driven by the extensive use of advanced drug delivery systems for inpatient treatments and complex therapeutic procedures.

- Regional Analysis: North America led the global market with a 40.1% revenue share in 2023. This position is supported by robust healthcare infrastructure, strong pharmaceutical manufacturing capabilities, and a high rate of technology adoption.

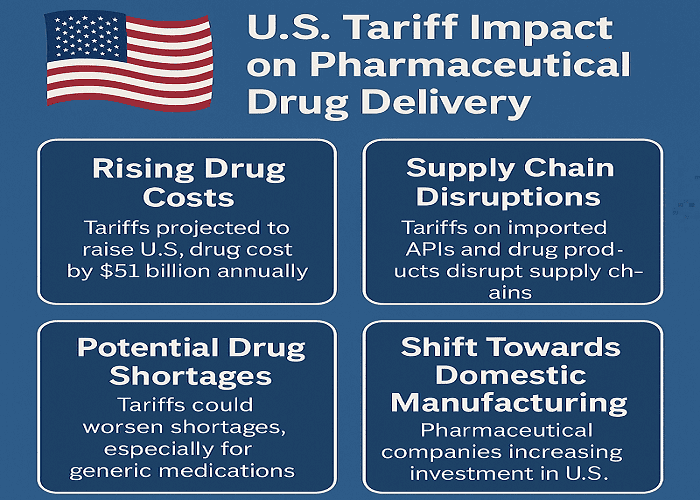

U.S. Tariffs Impacts on Pharmaceutical Drug Delivery

- Rising Drug Costs: A proposed 25% tariff on imported pharmaceuticals is projected to elevate U.S. drug costs by approximately $51 billion annually. This could result in price increases of up to 12.9% for consumers, depending on how much of the tariff burden is transferred through the supply chain.

- Supply Chain Disruptions: The U.S. heavily relies on imported active pharmaceutical ingredients (APIs) and finished drug products. Tariffs on these imports have disrupted established supply chains, leading to increased production costs and potential delays in drug availability.

- Potential Drug Shortages: Experts warn that tariffs could exacerbate drug shortages, particularly for generic medications that constitute a significant portion of prescriptions. The added financial strain may compel manufacturers to reduce production or withdraw certain drugs from the market.

- Impact on Generic Drug Manufacturers: Generic drug producers, operating on thin profit margins, are especially vulnerable to tariff-induced cost increases. The financial pressure may lead to reduced competition and higher prices for essential medications.

- Shift Towards Domestic Manufacturing: In response to tariffs, some pharmaceutical companies are investing in domestic manufacturing facilities to mitigate reliance on imports. For instance, Roche announced a $700 million investment in a new drug manufacturing facility in North Carolina, aiming to strengthen its U.S. production capabilities.

Segmentation Analysis

- Route of Administration Analysis: In 2023, the oral segment dominated the pharmaceutical drug delivery market, accounting for 55.7% of the global share. This leadership is attributed to its convenience, cost-effectiveness, and high patient compliance. Oral delivery systems are widely used for chronic conditions, offering ease of administration without the need for medical supervision. The ongoing innovation in controlled-release and targeted oral formulations is expected to further support the growth of this segment during the forecast period.

- Application Analysis: The cancer segment held a significant share of 42.5% in 2023, driven by the global rise in cancer incidence and increased demand for advanced therapies. Targeted drug delivery technologies have gained momentum in oncology to improve treatment precision and minimize side effects. The growing adoption of biologics and personalized treatment approaches continues to expand the use of novel delivery systems in cancer care, positioning this segment for sustained growth in the coming years.

- End-Use Analysis: In terms of end use, the hospital segment emerged as the leading contributor, securing a 64.1% revenue share in 2023. Hospitals remain the primary centers for administering complex therapies, including injectables, infusions, and advanced drug delivery systems. The rising number of surgical procedures, critical care needs, and the integration of smart drug delivery devices in clinical settings are expected to reinforce hospital dominance throughout the forecast period.

- Regional Analysis: North America led the global pharmaceutical drug delivery market in 2023, capturing 40.1% of total revenue. This regional leadership is supported by a strong pharmaceutical industry, advanced healthcare infrastructure, and significant investments in R&D. The region’s early adoption of innovative drug delivery platforms, including nanocarriers and implantable devices, further strengthens its position. Ongoing efforts in precision medicine and the high burden of chronic diseases continue to drive market growth in North America.

Market Segments

By Route of Administration

- Oral

- Ocular

- Nasal

- Pulmonary

- Injectable

- Topical

- Others

By Application

- Cardiovascular

- Cancer

- Diabetes

- Infectious Diseases

- Others

By End-users

- Hospitals

- Ambulatory Services

- Home Care

Regional Analysis

North America Dominates the Pharmaceutical Drug Delivery Market

As of 2023, North America holds the largest share in the global pharmaceutical drug delivery market, accounting for 40.1% of total revenue. This dominance is primarily driven by the rising prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders, which necessitate advanced and efficient drug delivery methods to enhance therapeutic efficacy and improve patient adherence.

The region has witnessed substantial progress in drug formulation and delivery technologies, including the development of targeted therapies and sustained-release systems. A significant milestone was achieved in February 2022, when the U.S. Food and Drug Administration (FDA) approved TAKHZYRO (lanadelumab-flyo) as a single-dose prefilled syringe for the prevention of hereditary angioedema (HAE) attacks in individuals aged 12 years and older. This reflects a broader industry shift toward self-administered, patient-friendly delivery formats.

Additionally, North America continues to invest heavily in personalized medicine and digital health integration, both of which support the innovation of tailored and connected drug delivery solutions. These combined factors contribute to the region’s robust market position and are expected to sustain its leadership over the forecast period.

Asia Pacific to Register the Fastest Growth Rate

The Asia Pacific region is projected to record the highest compound annual growth rate (CAGR) in the pharmaceutical drug delivery market during the forecast period. This growth is primarily attributed to the escalating burden of chronic diseases, particularly diabetes. According to the International Diabetes Federation’s Diabetes Atlas 2021, the age-adjusted prevalence of diabetes in China stood at 10.6% in 2021, with projections reaching 11.8% by 2030 and 12.5% by 2045.

Such statistics highlight the urgent need for innovative drug delivery technologies capable of addressing widespread and complex healthcare challenges. Furthermore, increased healthcare spending, expansion of biopharmaceutical capabilities, and rising disposable incomes are improving patient access to advanced therapeutic products. The growing emphasis on combination therapies and the development of specialized delivery systems to support them will also enhance market growth.

As healthcare infrastructure and research initiatives continue to expand across countries such as China, India, and South Korea, the Asia Pacific region is poised to become a major hub for drug delivery innovation, driving strong and sustained market development.

Emerging Trends

- Nanotechnology-Enhanced Drug Delivery: Nanocarriers, including lipid-based nanoparticles and polymeric micelles, are increasingly utilized to improve drug stability and targeting. These systems enhance the delivery of chemotherapeutic agents, reducing systemic toxicity and improving therapeutic outcomes .

- Artificial Intelligence (AI) Integration: AI is being employed to optimize drug formulation and delivery strategies. Machine learning algorithms assist in predicting drug release profiles and identifying optimal delivery pathways, thereby accelerating the development process and enhancing precision.

- Stimuli-Responsive Delivery Systems: Smart polymers and hydrogels that respond to physiological stimuli such as pH, temperature, or glucose levels are being developed. These systems allow for controlled and site-specific drug release, improving efficacy and minimizing side effects.

- 3D and 4D Bioprinting: Advancements in bioprinting technologies enable the fabrication of complex drug delivery devices tailored to individual patient needs. 4D bioprinting introduces time as a factor, allowing printed structures to change shape or function in response to environmental stimuli, offering dynamic control over drug release.

Use Cases

- Targeted Cancer Therapy: Nanoparticle-based delivery systems are employed to transport chemotherapeutic agents directly to tumor cells, enhancing drug accumulation at the tumor site while sparing healthy tissues. This approach has demonstrated improved treatment efficacy and reduced adverse effects.

- Insulin Delivery for Diabetes Management: Glucose-responsive hydrogels are being developed to release insulin in response to blood sugar levels. These systems aim to mimic the body’s natural insulin regulation, offering potential improvements in glycemic control for diabetic patients.

- Brain Drug Delivery: Nanoparticles are engineered to cross the blood-brain barrier, facilitating the delivery of therapeutic agents for neurological conditions such as Alzheimer’s and Parkinson’s diseases. This strategy enhances drug concentration in the brain while minimizing systemic exposure.

- Personalized Medicine: 3D-printed drug delivery systems allow for the customization of dosage forms to meet individual patient requirements. This personalization can improve patient adherence and therapeutic outcomes, particularly in populations with specific needs, such as pediatric or geriatric patients.

Conclusion

The pharmaceutical drug delivery market is evolving rapidly, driven by technological advancements, rising chronic disease prevalence, and increasing demand for patient-centric therapies. Innovations such as nanotechnology, AI integration, and stimuli-responsive systems are enhancing treatment precision, safety, and effectiveness.

North America leads the market due to its advanced healthcare infrastructure, while Asia Pacific is expected to witness the fastest growth, propelled by expanding healthcare access and research investments. With ongoing developments in personalized medicine and smart delivery systems, pharmaceutical drug delivery is poised to remain a critical component in global healthcare, transforming how treatments are administered and improving overall patient outcomes.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)