Table of Contents

Introduction

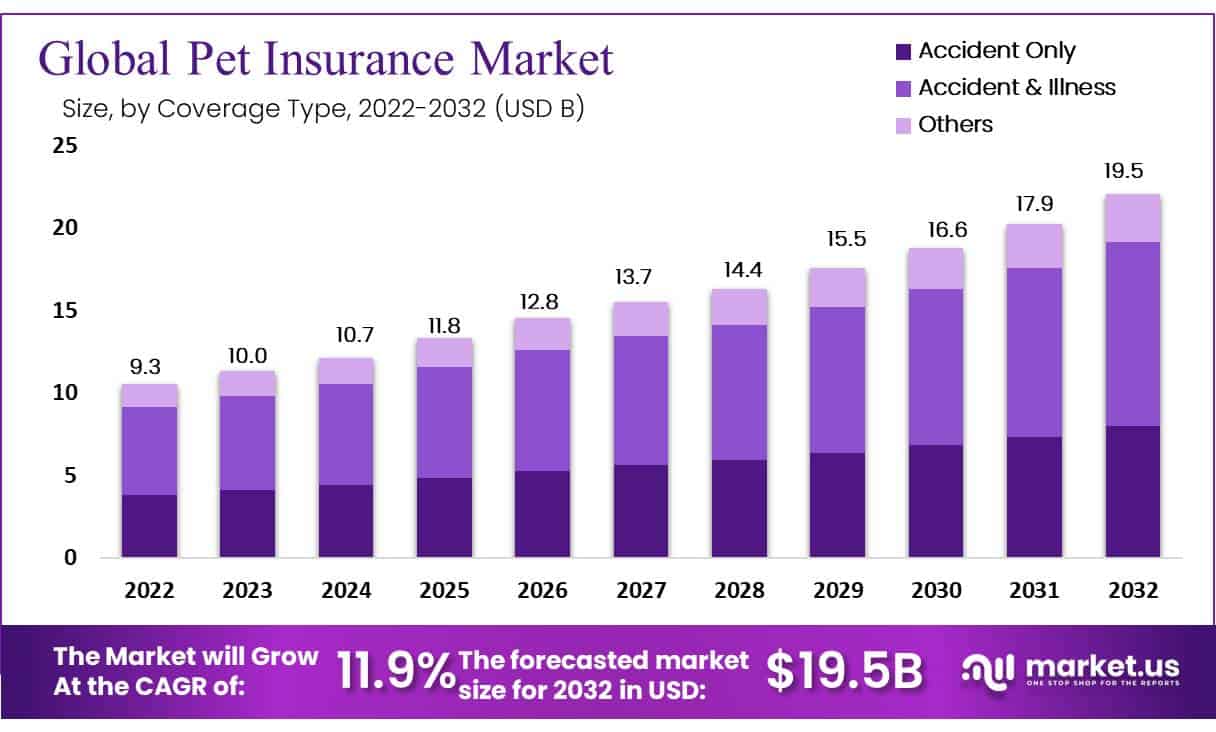

Global Pet Insurance Market size is expected to be worth around US$ 19.15 Bn by 2032 from US$ 10.0 Bn in 2023, growing at a CAGR of 11.9% during the forecast period from 2024 to 2032. In 2023, Europe led the market, achieving over 30% share with a revenue of US$ 2.7 Billion.

The pet insurance market is experiencing significant growth due to several key factors. The surge in pet adoption rates, particularly during and after the COVID-19 pandemic, has played a pivotal role. During lockdowns, many individuals turned to pets for companionship, leading to a notable increase in pet ownership.

Additionally, the rising costs of veterinary care have driven pet owners to seek insurance as a way to manage expenses. For instance, in the United States, the average annual spending on veterinary visits for dog-owning households rose by over 60% between 2020 and 2022.

Despite this growth, the market faces notable challenges. A lack of standardized pet health codes for insurance reimbursement and limited awareness about pet insurance in regions such as Asia-Pacific pose hurdles. However, increasing awareness campaigns and the development of tailored insurance products are expected to mitigate these challenges and sustain market expansion.

Recent advancements are reshaping the market landscape. Collaborations between pet insurance providers and veterinary service organizations are becoming more common, while technological innovations are enhancing customer experience and streamlining operations. For example, Embrace Pet Insurance Agency LLC introduced an AI-driven platform in 2023, automating routine claims processes to improve efficiency and customer satisfaction.

Overall, the pet insurance market is positioned for robust growth, fueled by increasing pet ownership, escalating veterinary expenses, and the continuous evolution of innovative insurance products designed to meet diverse pet health needs.

Key Takeaways

- The pet insurance market is anticipated to reach US$ 27.8 billion by 2032.

- From 2023 to 2032, the market is expected to grow at a CAGR of 11.9%.

- In 2022, the accident & illness pet insurance segment led the market.

- The cat segment is projected to lead the market by animal type during the forecast period.

- The direct sale channel sub-segment dominated the market by sales channel in 2022.

- Europe held a dominant 30% market share in 2022.

- North America is expected to have the second-largest revenue during the forecast period.

- Asia Pacific is projected to experience the highest CAGR in the forecast period.

Pet Insurance Statistics

- 2022 Statistics

- Over 4.8 million pets were insured in 2022, reflecting a significant increase compared to 2018.

- Monthly insurance premiums averaged $44 for dogs and $30 for cats.

- 76% of dog owners overestimated the cost of pet insurance, assuming prices much higher than actual figures.

- Only 11% of respondents accurately estimated insurance costs at under $50 per month, while 28% believed costs ranged from $100 to $149 monthly.

- Veterinary costs were a concern for 19% of pet owners, while 31% were somewhat worried.

- In the U.S., insured pets are predominantly dogs (80%) compared to cats (20%).

- The average annual expense for dog ownership, excluding unexpected vet bills, is $1,400, compared to $1,150 for cats.

- Emergency veterinary care is required every 2.5 seconds in the U.S.

- Pet insurance coverage remains low, with only 4% of dogs and 1% of cats insured.

- The pet insurance market was valued at $8.6 billion in 2022 and is projected to reach $16 billion by 2032.

- Insured pets grew by 26.6% over four years, representing a strong double-digit growth trend.

- Pet insurance premiums generated $3.2 billion in revenue in 2022.

- Average monthly premiums for accident and illness coverage were $53 for dogs and $32 for cats.

- Veterinary visit costs for pet-owning households have risen significantly over the past three years.

- Recreational drugs ranked among the top 10 toxins for pets treated by the ASPCA in 2022.

- The leading medical issues were skin conditions in dogs and urinary tract infections in cats.

- The highest insurance claims in 2022 reached $60,882 for dogs and $40,057 for cats.

- Approximately 78% of dogs and 85% of cats are spayed or neutered.

- Vaccination costs averaged $176 for dogs and $88 for cats.

- Due to financial constraints, 35% of pet owners delayed annual vet visits, and 23% postponed vaccinations or boosters.

- In 2021, 60% of pet owners reported being extremely satisfied with veterinary services.

- 2023 Statistics

- In 2023, U.S. pet insurance premiums totaled $3.9 billion, covering around 5.7 million pets.

- Average annual accident/illness premiums were $676 for dogs and $383 for cats.

- States with the highest insured pet populations were California, New York, and Florida, with 80% being dogs.

- Pet ownership in the U.S. rose to 66% of households, equating to 86.9 million families, up from 56% in 1988.

- The pet industry expenditure in the U.S. reached $147 billion in 2023, a 7.5% increase from 2022.

- Dogs remain the most common pet, with 65.1 million owned, followed by 46.5 million cats.

- 2024 Statistics

- Over 51% of pet owners now view their pets as equal to human family members.

- During the pandemic, 78% of surveyed pet owners acquired their pets.

- Households earning $100,000+ annually are most likely to own pets, with 63% owning dogs and 40% owning cats.

- Homeowners are more likely to have pets, with 58% owning dogs and 36% owning cats, compared to renters (39% and 29%, respectively).

- Rural Americans are more likely to own pets, with 71% of adults in rural areas having at least one pet.

- Rural residents also tend to own multiple pets, with 47% having more than one, compared to 32% in suburbs and 26% in urban areas.

- Among dog owners, 42% purchased pets from stores, and 38% adopted from shelters or rescues.

- For cat owners, 43% acquired pets from stores, while 40% adopted from shelters or rescues.

- Breeders accounted for 23% of dog purchases but only 7% of cat acquisitions.

- Over one-third (35%) of Americans own more than one pet.

Emerging Trends in Pet Insurance

- Increasing Pet Ownership: Pet ownership rates continue to rise as more households welcome pets into their families. This growth is influenced by urbanization, shifting demographics, and the recognition of pets’ physical and mental health benefits for their owners.

- Rising Veterinary Costs: Veterinary care costs have steadily increased, creating financial challenges for many pet owners. Pet insurance serves as a financial safeguard, enabling access to high-quality veterinary care without the stress of expensive bills.

- Innovative Coverage Options: Pet insurance providers are diversifying their offerings to cater to varied owner needs. Emerging options include wellness plans covering routine care, alternative therapies such as acupuncture and hydrotherapy, and policies tailored for specific breeds or pre-existing conditions.

- Technological Advancements: The pet insurance sector is leveraging technology to enhance customer experiences and streamline processes. Features like mobile apps, online portals, and telemedicine services allow pet owners to access information, submit claims, and consult veterinarians with greater convenience.

- Personalized Plans: Customizable insurance plans are gaining traction, enabling pet owners to adapt coverage based on their specific needs and budgets. Options include flexible deductibles, co-pays, and coverage limits, ensuring owners can find the most suitable plan.

Key Use Cases for Pet Insurance

- Accident and Illness Coverage: Pet insurance primarily helps manage unexpected veterinary costs from accidents or illnesses. Policies cover treatments for injuries, surgeries, diagnostic tests, and long-term care for chronic conditions.

- Routine and Preventive Care: Some plans include coverage for routine and preventive care, such as annual check-ups, vaccinations, dental cleanings, and flea and tick prevention, supporting pets’ overall health and mitigating future costly issues.

- Hereditary and Congenital Conditions: Policies covering hereditary and congenital conditions are especially beneficial for purebred pets or breeds with specific health concerns, offering peace of mind for potential long-term needs.

- Emergency and Specialized Care: Pet insurance often includes coverage for emergencies and specialized treatments like cancer therapies or orthopedic surgeries. This ensures financial support for critical, high-cost medical needs.

- Travel and Boarding Coverage: Certain policies extend coverage to travel-related expenses, such as emergency veterinary care while traveling or reimbursement for boarding fees if the pet owner is hospitalized, adding flexibility and security for owners on the go.

Conclusion

The pet insurance market is poised for substantial growth, driven by increasing pet ownership, rising veterinary costs, and innovative insurance solutions. The market is expected to reach $27.8 billion by 2032, growing at a CAGR of 11.9%. Key factors include heightened pet adoption during the COVID-19 pandemic, escalating veterinary expenses, and a growing awareness of the need for financial safeguards for pet healthcare. Challenges like limited standardization and regional awareness are being addressed through tailored products and awareness campaigns.

Technological advancements, such as AI-driven claims processing, enhance efficiency and customer satisfaction. Europe dominated the market in 2022, while Asia-Pacific is expected to grow the fastest. With personalized plans, routine care options, and emergency coverage, pet insurance is becoming an essential tool for managing pet healthcare expenses globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)