Table of Contents

Overview

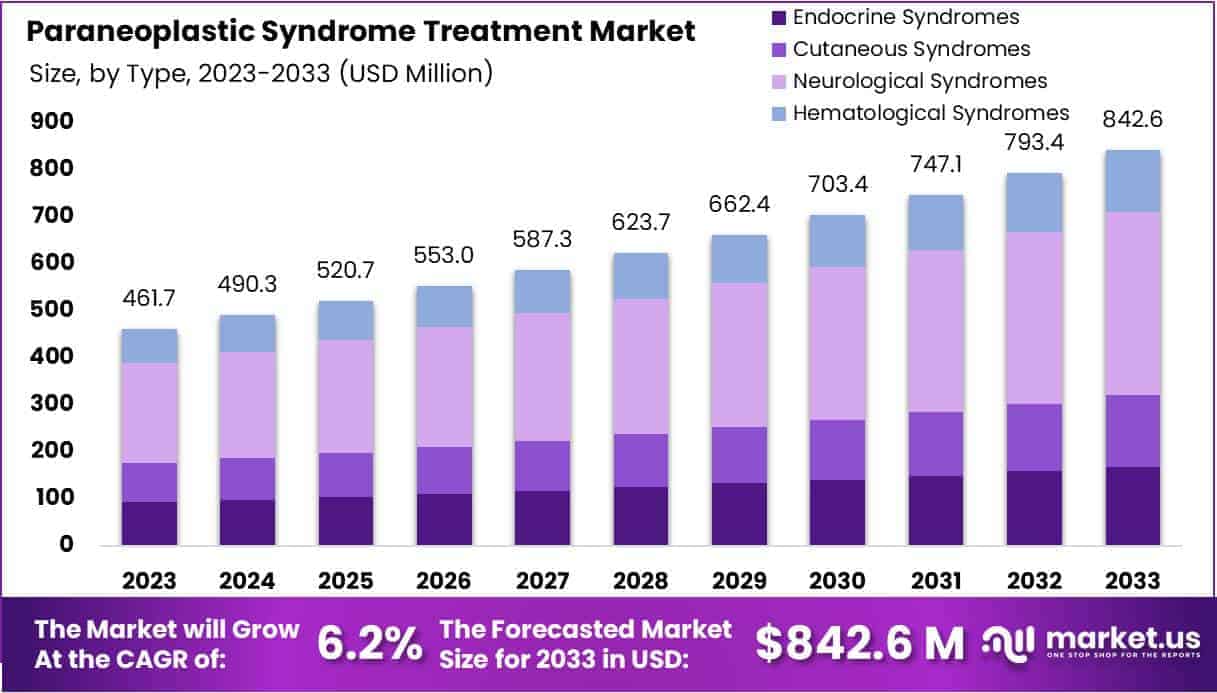

New York, NY – July 16, 2025 – The Global Paraneoplastic Syndrome Treatment Market size is expected to be worth around USD 842.6 Million by 2033, from USD 461.7 Million in 2023, growing at a CAGR of 6.2% during the forecast period from 2024 to 2033.

Paraneoplastic syndromes (PNS) are a group of rare, immune-mediated conditions that occur in association with malignancies, often before the underlying cancer is diagnosed. These syndromes affect various organ systems including the nervous, endocrine, and dermatologic systems. The management of PNS has gained attention due to its complex pathophysiology and the need for prompt, coordinated care.

Treatment of paraneoplastic syndromes primarily focuses on two key strategies: addressing the underlying malignancy and modulating the immune response. Anticancer therapies such as surgical resection, chemotherapy, radiotherapy, and targeted therapies are essential to eliminate the source of paraneoplastic triggers. Clinical evidence supports that early treatment of the tumor often leads to partial or complete resolution of PNS symptoms.

Immunosuppressive and immunomodulatory therapies, including corticosteroids, intravenous immunoglobulin (IVIG), plasmapheresis, and monoclonal antibodies like rituximab, are used to control autoimmune responses. In neurological variants such as paraneoplastic limbic encephalitis or cerebellar degeneration, these interventions have shown varying levels of efficacy, depending on the type of antibodies involved and the timeliness of treatment.

Ongoing clinical trials are exploring novel immunotherapies and biomarker-driven treatment strategies. Early diagnosis remains crucial, as irreversible damage can occur if PNS is not promptly recognized. Increased clinical awareness and integrated oncology-neurology care pathways are expected to enhance patient outcomes and quality of life.

Key Takeaways

- Market Valuation: The global market for paraneoplastic syndrome treatment is projected to rise from USD 461.7 million in 2023 to approximately USD 842.6 million by 2033.

- Growth Rate: This expansion reflects a compound annual growth rate (CAGR) of 6.2% during the forecast period 2024 to 2033.

- By Type: Neurological paraneoplastic syndromes dominated the market in 2023, accounting for over 46.3% of the total share. Other key types include endocrine, cutaneous, and hematological syndromes.

- By Diagnosis: Imaging tests held the largest share in the diagnostic segment, contributing more than 44.1%. These tools are vital for accurate identification and continuous monitoring of the condition.

- By Treatment: Medications remained the leading treatment approach in 2023, representing over 52% of the market share. These are primarily used to manage immune-mediated responses and neurological complications.

- By End User: Hospitals and clinics comprised the largest end-user segment, securing a share of over 58.7%. Their dominance is supported by access to multidisciplinary care and specialized treatment pathways.

- Regional Insights: North America led the global market with more than 36% share, reaching a valuation of USD 166.2 million in 2023. This leadership is attributed to robust healthcare infrastructure and heightened clinical awareness across the region.

Segmentation Analysis

- Type Analysis: In 2023, Neurological Syndromes led the Paraneoplastic Syndrome Treatment Market with a 46.3% share, driven by their frequent occurrence in cancer patients. These syndromes present complex diagnostic and therapeutic challenges, necessitating advanced medical interventions. Endocrine Syndromes followed closely, requiring precise hormonal management. Though smaller, Cutaneous and Hematological Syndromes remain important for early cancer detection and hematologic complications, respectively, underscoring the need for specialized and integrated treatment approaches.

- Diagnosis Analysis: Imaging Tests dominated the diagnostic segment in 2023, accounting for over 44.1% of the market share. Technologies like CT, MRI, and PET scans are essential for identifying hidden malignancies linked to paraneoplastic syndromes. Blood Tests play a vital role in biomarker detection and monitoring. Though smaller in share, spinal taps, EEGs, and biopsies are critical in confirming complex neurological cases, highlighting the importance of multimodal diagnostics in improving treatment outcomes.

- Treatment Analysis: Medications led the treatment segment in 2023 with over 52% market share, primarily due to their ability to manage autoimmune responses and systemic symptoms. Immunosuppressants remain a key secondary option, especially in resistant cases. IVIg therapies provide immune modulation where conventional drugs are insufficient. Anti-seizure medications are widely used for neurological symptoms. The market continues to expand with new targeted therapies and supportive care solutions aimed at improving quality of life and patient outcomes.

- End-User Analysis: Hospitals and Clinics held a dominant 58.7% share in the end-user segment in 2023, attributed to their capacity for multidisciplinary, specialist-led care. These facilities ensure comprehensive management of paraneoplastic syndromes. Diagnostic Centers contribute significantly by providing early, accurate detection using advanced technologies. Ambulatory Care Centers are gaining traction due to affordability and convenience, reflecting a shift toward decentralized care models and outpatient-based treatment strategies in modern healthcare environments.

Market Segments

Type

- Endocrine Syndromes

- Cutaneous Syndromes

- Neurological Syndromes

- Hematological Syndromes

Diagnosis

- Blood Tests

- Imaging Tests

- Spinal Tap

- Others Diagnosis

Treatment

- Medication

- Immunosuppressants

- Intravenous Immunoglobulin (IVIg)

- Anti-Seizure Medications

- Other Treatments

End-User

- Hospitals & Clinics

- Diagnostic Centers

- Ambulatory Care Centers

Regional Analysis

In 2023, North America led the global paraneoplastic syndrome treatment market, accounting for over 36% of the total share with a valuation of USD 166.2 million. This leadership is attributed to the region’s advanced healthcare infrastructure, heightened clinical awareness, and the strong presence of major pharmaceutical and biotechnology firms. Supportive healthcare policies that emphasize early diagnosis and intervention further strengthen market performance across the region.

Europe followed with a substantial share, driven by the growing incidence of cancer-related conditions and robust research initiatives. Public and private sector funding dedicated to rare and complex disease treatment has accelerated innovation, contributing to market expansion.

The Asia-Pacific region is witnessing the fastest growth, supported by increased healthcare investments, infrastructure development, and rising awareness of paraneoplastic syndromes. High cancer prevalence in densely populated countries such as China and India is further driving demand for early diagnostic services and effective therapeutic options.

Latin America and the Middle East & Africa represent emerging markets with steady growth potential. Improvements in healthcare access, rising awareness among healthcare professionals, and gradual adoption of modern diagnostic and treatment practices are key growth drivers in these regions.

Emerging Trends

- Expanded Use of Immunomodulatory Therapies: Treatment protocols have increasingly incorporated immune-modulating agents such as high dose corticosteroids, intravenous immunoglobulins (IVIG), and plasmapheresis to manage neurological symptoms. Such approaches are being initiated earlier in the care pathway to curb irreversible neuronal damage.

- Integration of Targeted Biologics: Monoclonal antibodies directed against B cell markers (e.g., rituximab) and adhesion molecules (e.g., natalizumab) are under evaluation in phase II studies for specific onconeural antibody–mediated syndromes, reflecting a shift toward precision immunotherapy.

- Biomarker Guided Diagnosis and Management: Advances in autoantibody testing have improved identification of onconeural antibodies (e.g., Hu, Yo, CRMP5), enabling tailored treatment plans. The refinement of diagnostic criteria in 2021 has enhanced specificity, with only 42.3% of previously “definite” cases by 2004 standards remaining so under updated guidelines.

- Awareness of Checkpoint Inhibitor Associated Syndromes: As immune checkpoint inhibitors (ICIs) gain prominence in oncology, recognition of ICI induced paraneoplastic neurological events has become critical. Protocols are being developed to distinguish these immune related adverse events from classic PNS and to guide their management.

- Emphasis on Multidisciplinary Care: Collaborative models involving oncology, neurology, and rehabilitation specialists are being adopted to address both tumor control and functional recovery, reflecting a holistic approach to patient outcomes.

Use Cases

- Early Immunotherapy in Neurological PNS: In a cohort of 12 patients with paraneoplastic neurologic syndromes, 75% (n=9) received immunotherapy, and 78% of those (n=7) were treated with corticosteroids within four weeks of symptom onset. This early intervention correlated with stabilization or improvement in 67% of cases.

- Prompt Oncologic Diagnosis Triggered by PNS: Among six patients presenting initially with neurological PNS, the median interval to cancer diagnosis was 73 days; 83% were found to have underlying malignancies (lymphoma 25%, lung cancer 17%, ovarian cancer 17%) during the PNS work up.

- Pediatric PNS Outcomes: In children with paraneoplastic syndromes, concurrent diagnosis and treatment of underlying cancer and immunosuppression are recommended. Pediatric malignancies are curable in up to 85.7% of cases, underscoring the importance of rapid PNS recognition in this group.

- Paraneoplastic Neurologic Disorders in SCLC: In a population of small cell lung cancer patients (n=255), 9.4% developed paraneoplastic neurologic disorders. Breakdown by syndrome: Lambert Eaton myasthenic syndrome (3.8%), sensory neuronopathy (1.9%), and limbic encephalitis (1.5%). Autoantibodies to SOX2, HuD, or P/Q VGCC were detected in 87% of affected patients.

- Population Level Incidence Guiding Resource Allocation: A community based study reported an overall PNS incidence of 0.6 per 100,000 person years, rising to 0.8/100,000 in 2003–2018. Prevalence in those over 60 years was 11.0 per 100,000, informing the need for geriatric neurology services.

Conclusion

The paraneoplastic syndrome treatment market is witnessing significant growth, driven by increasing clinical awareness, advancements in diagnostic technologies, and evolving therapeutic strategies. With a projected market value of USD 842.6 million by 2033 and a CAGR of 6.2%, the field is benefiting from early immunotherapy use, integration of biologics, and biomarker-guided approaches.

North America remains the leading region, while Asia-Pacific shows the fastest expansion. Multidisciplinary care models and early diagnosis are key to improving patient outcomes. As research progresses and clinical protocols refine, the global healthcare community is better positioned to manage these rare but critical cancer-associated conditions.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)