Table of Contents

Overview

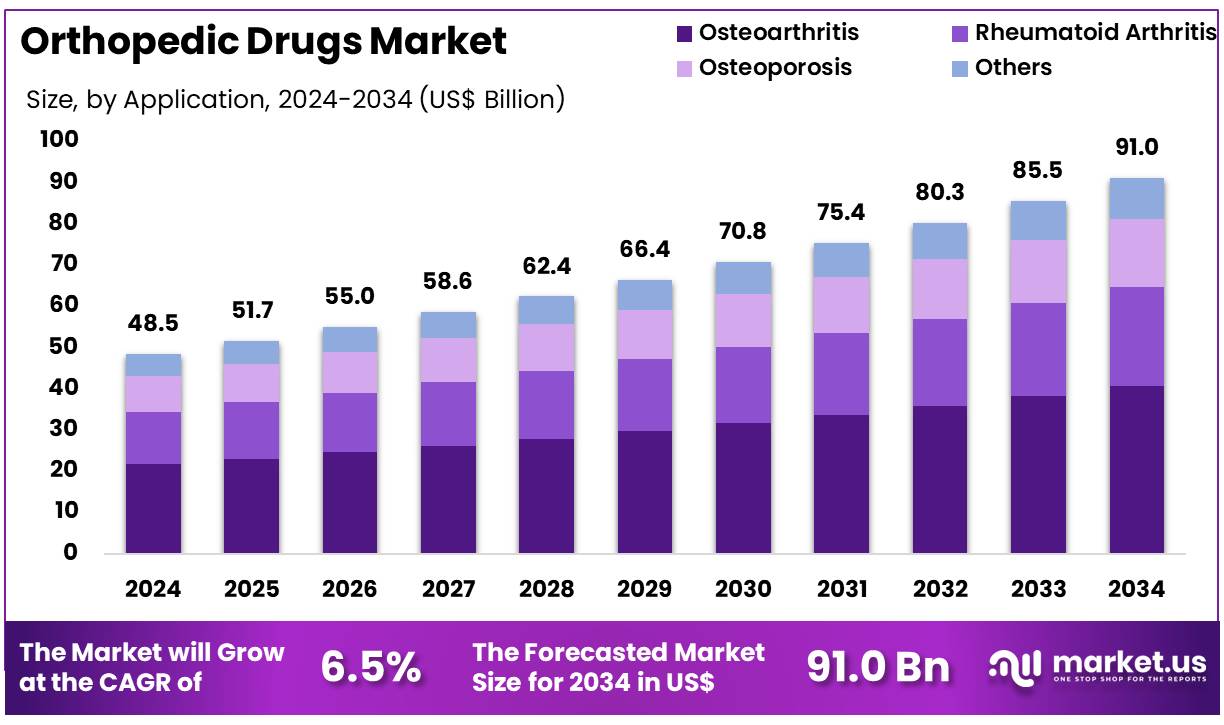

New York, NY – Dec 04, 2025 – Global Orthopedic Drugs Market size is expected to be worth around US$ 91.0 Billion by 2034 from US$ 48.5 Billion in 2024, growing at a CAGR of 6.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.1% share with a revenue of US$ 20.4 Billion.

The global orthopedic drugs market has been experiencing steady expansion, supported by the increasing prevalence of musculoskeletal conditions and the rapid adoption of advanced therapeutic options. The demand for effective pain management, inflammation control, and bone-health therapies has been rising consistently, leading to notable investments in research and development activities.

Growth of the market has been attributed to the rising incidence of arthritis, osteoporosis, and traumatic injuries, alongside an aging population that requires long-term orthopedic care. The introduction of biologics, targeted therapies, and improved drug-delivery systems has been widening the treatment landscape and enhancing clinical outcomes for patients. Continued innovation in disease-modifying agents and anti-inflammatory drugs has also supported positive market momentum.

North America has been maintaining a leading share due to strong healthcare infrastructure and high adoption of novel pharmaceuticals. However, Asia-Pacific is projected to demonstrate the most accelerated growth, driven by a large patient base and increased healthcare investments.

Pharmaceutical companies have been focusing on strategic collaborations, regulatory approvals, and product launches to strengthen their market presence. Emphasis has been placed on developing safer and more effective drug formulations to address unmet clinical needs.

Overall, the orthopedic drugs market is expected to maintain a stable growth trajectory, supported by technological advancements and sustained demand for improved therapeutic solutions. The industry outlook remains cautiously optimistic as stakeholders continue to invest in innovation, accessibility, and patient-centered treatment development.

Key Takeaways

- The orthopedic drugs market generated revenue of US$ 48.5 billion in 2024, supported by a CAGR of 6.5%, and is projected to achieve US$ 91.0 billion by 2034.

- By product type, nonsteroidal anti-inflammatory drugs (NSAIDs) accounted for the largest share in 2024, representing 48.6% of the market.

- Based on application, osteoarthritis remained the leading segment in 2024, contributing 44.7% to total market revenue.

- Within the distribution channel category, retail pharmacies dominated the market, capturing 53.8% of overall revenue.

- North America emerged as the leading regional market in 2024, holding a 42.1% share.

Segmentation Analysis

- Product Type Analysis: Nonsteroidal anti-inflammatory drugs (NSAIDs) accounted for a dominant 48.6% share in 2023, reflecting their extensive use in treating musculoskeletal pain and inflammation associated with osteoarthritis and rheumatoid arthritis. The segment’s growth is supported by rising preference for non-opioid therapies, availability of gastrointestinal-friendly formulations, and improvements in overall safety profiles. Widely used agents such as ibuprofen and naproxen are expected to retain strong prescription rates due to their proven efficacy and affordability.

- Application Analysis: Osteoarthritis represented 44.7% of the orthopedic drugs market, driven by increasing global incidence, particularly among aging populations. This degenerative disorder results in chronic pain, mobility limitations, and sustained reliance on pharmaceutical interventions. Factors such as demographic aging, obesity, and sedentary lifestyles are contributing to rising disease burden. Advances in drug development, including selective COX-2 inhibitors, and improved awareness of early therapeutic approaches are supporting this segment’s expansion by enhancing patient outcomes and slowing disease progression.

- Distribution Channel Analysis: Retail pharmacies held a 53.8% share of the distribution market, supported by their accessibility, convenience, and established role in providing orthopedic medications. These channels supply both prescription and over-the-counter drugs, making them essential for managing acute and chronic musculoskeletal conditions. Growth is being reinforced by the expansion of pharmacy chains, increasing use of digital prescription systems, and widespread adoption of home delivery models. As telehealth continues to expand, retail pharmacies are expected to maintain a central position in orthopedic drug distribution.

Regional Analysis

North America Leading the Orthopedic Drugs Market

North America has been maintaining a dominant position in the orthopedic drugs market, accounting for a revenue share of 42.1%. This leadership can be attributed to the rising burden of musculoskeletal disorders and the continuous introduction of advanced pharmaceutical therapies. According to data from the Centers for Disease Control and Prevention (CDC), more than 32 million adults in the United States are affected by osteoarthritis, one of the most prevalent orthopedic conditions requiring consistent pharmacological intervention. This substantial patient base has been creating sustained demand for medications designed to relieve pain and enhance mobility.

Regulatory support continues to strengthen regional growth. The U.S. Food and Drug Administration (FDA) has been actively approving new formulations and expanding indications for existing orthopedic treatments. In January 2024, the FDA granted an expanded indication for ZYNRELEF (bupivacaine and meloxicam) to include additional orthopedic surgical procedures, as reported by Heron Therapeutics. This development reflects ongoing progress in improving pain management options for orthopedic patients. The availability of such innovative therapies has broadened clinical choices and reinforced regional market expansion.

Use Cases

- Symptom Relief in Osteoarthritis with NSAIDs: Arthritis affects an estimated 53.2 million adults in the United States, representing 21.2% of the population, with many experiencing chronic joint pain and stiffness. NSAIDs such as ibuprofen and naproxen are widely utilized as first-line therapies to reduce inflammation and support improved functional mobility in these patients.

- Fracture Risk Reduction in Osteoporosis with Bisphosphonates: Among adults aged 50 years and older, 12.6% are diagnosed with osteoporosis, representing approximately 10.2 million individuals at increased fracture risk. Bisphosphonates including alendronate are prescribed to limit bone resorption and have demonstrated the ability to reduce vertebral fracture incidence by up to 50% in this population.

- Senolytic Drug Trials for Knee Osteoarthritis: Emerging senolytic compounds are being evaluated for their potential to modify osteoarthritis progression. A notable Phase 2 trial (NCT04129944) assessed a single intra-articular administration of UBX0101 in individuals with moderate to severe knee osteoarthritis, aiming to remove senescent cells and mitigate continued joint degeneration.

Frequently Asked Questions on Orthopedic Drugs

- What are orthopedic drugs?

Orthopedic drugs are medications formulated to manage conditions affecting bones, joints, muscles, and connective tissues. Their usage has been driven by rising musculoskeletal disorders, and they support pain reduction, inflammation control, and functional recovery across diverse patient groups. - What conditions are commonly treated with orthopedic drugs?

These drugs are widely used for treating osteoarthritis, rheumatoid arthritis, osteoporosis, fractures, and soft-tissue injuries. Increased aging populations and rising lifestyle-related disorders have contributed to growing treatment demand across clinical settings. - What types of orthopedic drugs are available?

Orthopedic drugs include analgesics, NSAIDs, corticosteroids, biologics, and bone-health agents such as bisphosphonates. Their selection is determined by disease severity, patient profile, and long-term therapeutic goals associated with musculoskeletal management. - Are orthopedic drugs safe for long-term use?

Long-term usage is considered safe when monitored by professionals, although risks such as gastrointestinal, cardiovascular, or metabolic effects may occur. Continuous clinical supervision is recommended to balance therapeutic benefits with potential safety concerns. - Which drug classes dominate the orthopedic drugs market?

Biologics, NSAIDs, and corticosteroids remain dominant due to wide therapeutic use and sustained prescription volumes. Biologic agents have shown strong uptake, supported by favorable clinical outcomes and extended disease-modifying capabilities. - Which regions lead the orthopedic drugs market?

North America and Europe maintain dominant shares due to high healthcare expenditure, advanced diagnostic capabilities, and strong pharmaceutical infrastructure. Asia-Pacific is showing notable expansion, supported by population growth and increased access to musculoskeletal care. - What trends are shaping the future of the orthopedic drugs market?

Growth is being shaped by rising biologic and biosimilar utilization, advancements in targeted therapies, increasing preference for minimally invasive treatments, and wider digital health integration. These developments are expected to support sustained innovation and market expansion.

Conclusion

The orthopedic drugs market has been progressing steadily, supported by rising musculoskeletal disorders, an aging population, and continuous advancements in therapeutic technologies. Increased adoption of NSAIDs, biologics, and targeted agents has strengthened treatment outcomes and expanded clinical applications.

Regional performance remains led by North America, while Asia-Pacific is set to record the fastest gains due to improving healthcare access. Ongoing regulatory approvals, R&D investments, and industry collaborations have reinforced market growth. Overall, the sector is expected to maintain a favorable long-term outlook as innovation, accessibility, and patient-centered treatment approaches continue to advance global orthopedic care.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)