Table of Contents

Overview

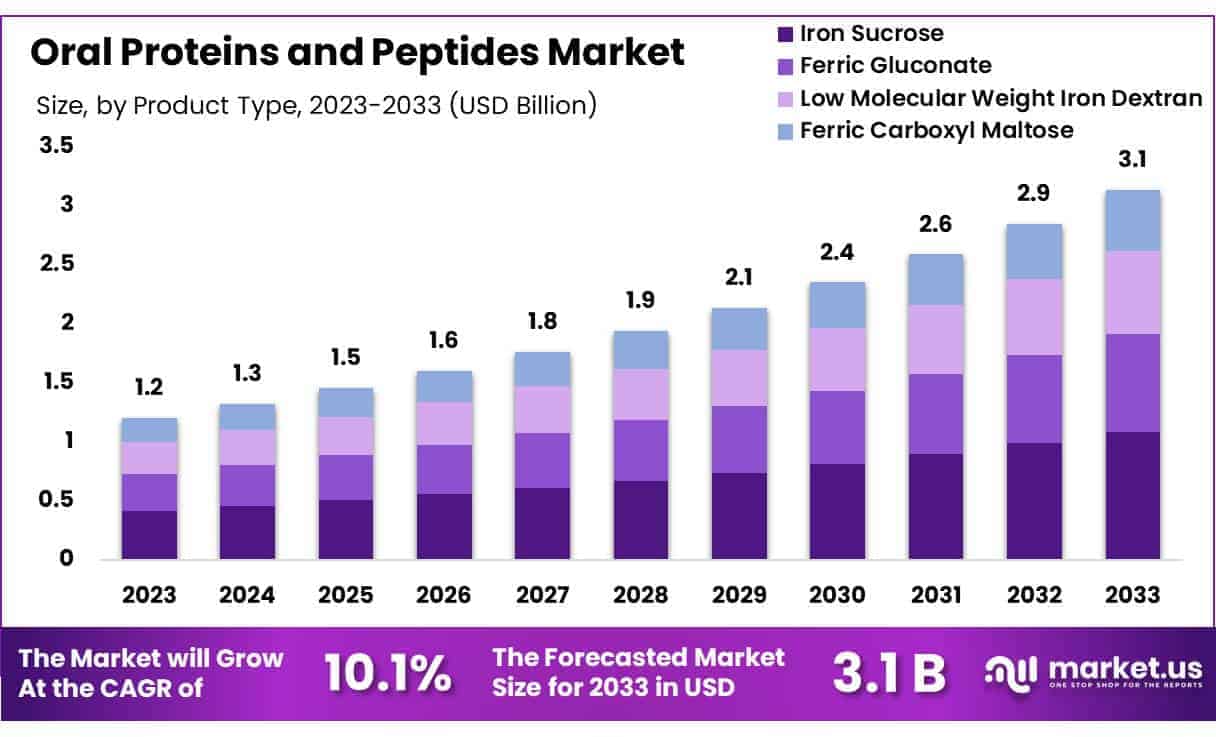

New York, NY – May 15, 2025 – Global Oral Proteins and Peptides Market size is expected to be worth around US$ 3.1 billion by 2033 from US$ 1.2 billion in 2023, growing at a CAGR of 10.1% during the forecast period 2024 to 2033.

Oral proteins and peptides have emerged as a promising class of therapeutic agents designed for administration by mouth. These bioactive molecules are derived from amino acid chains and are intended to target a variety of physiological pathways. Their oral delivery is being advanced to improve patient convenience and adherence.

The formulation of oral proteins and peptides can be attributed to recent innovations in protective coatings and encapsulation techniques. Stability in the gastrointestinal tract is enhanced by enteric polymers and nanoparticle carriers. As a result, degradation by stomach acid and digestive enzymes can be minimized. Patient compliance is expected to be increased through the availability of tablets or capsules rather than injections.

Despite these advantages, the development of oral proteins and peptides has been impeded by challenges in maintaining bioavailability. Absorption across the intestinal epithelium is inherently low for large molecules. This issue can be mitigated by permeation enhancers and enzyme inhibitors. Additionally, manufacturing processes must ensure consistent peptide purity and activity, which can be achieved through advanced chromatography and lyophilization methods.

Future prospects for oral proteins and peptides are driven by ongoing research in formulation science. Novel approaches such as mucoadhesive delivery systems and pH-responsive release are under evaluation. Collaborations between pharmaceutical companies and academic institutions are being established to expedite clinical trials. The growth of this segment is expected to support broader access to peptide-based therapies and to redefine standards in patient-centric treatment.

Key Takeaways

- Market Overview: The global oral proteins and peptides market generated a revenue of US$ 2 billion in 2023. It is projected to expand at a compound annual growth rate (CAGR) of 10.1%, reaching approximately US$ 3.1 billion by 2033.

- By Product Type: The market is categorized into ferric gluconate, low molecular weight iron dextran, iron sucrose, and ferric carboxyl maltose. Among these, iron sucrose emerged as the leading product in 2023, accounting for 34.6% of the total market share.

- By Application: Key applications include diabetes, gastric and digestive disorders, bone diseases, and hormonal disorders. The diabetes segment held the largest share, contributing 40.7% to the overall market.

- By Drug Type: The drug type segment comprises linaclotide, calcitonin, insulin, plecanatide, and octreotide. Insulin dominated the segment, with a revenue share of 38.5% in 2023.

- By End User: The market is segmented into hospitals, pharmaceutical companies, and others. Hospitals were the leading end users, holding 52.3% of the revenue share.

- Regional Insights: North America led the global market in 2023, capturing a market share of 38.2%, reflecting strong adoption and advanced healthcare infrastructure in the region.

Segmentation Analysis

- Product Type Analysis: In 2023, the iron sucrose segment led the market with a 34.6% share, driven by its effectiveness in treating iron deficiency anemia, especially in patients with chronic kidney disease and pregnant women. Its favorable safety profile, better absorption, and fewer side effects compared to other formulations have increased preference among healthcare providers. Rising anemia cases and advancements in oral delivery systems are expected to further boost demand for iron sucrose in the oral proteins and peptides market.

- Application Analysis: The diabetes segment accounted for 40.7% of the market share in 2023, driven by the global rise in diabetes prevalence and growing demand for non-invasive therapies. Oral proteins and peptides offer improved patient adherence compared to injectables, making them a preferred treatment. Innovations in peptide stability and absorption support this growth. As healthcare systems focus on enhancing diabetes care, the segment is expected to expand through improved delivery technologies and broader access to oral treatment options.

- Drug Type Analysis: Insulin dominated the drug type segment with a 38.5% revenue share in 2023, due to increasing diabetes cases and patient preference for non-injectable treatment options. Oral insulin is gaining traction as it enhances compliance and reduces discomfort associated with injections. Technological advancements have improved insulin stability and absorption in the digestive tract. With ongoing research and investment in oral insulin development, this segment is projected to experience strong growth in the coming years.

- End-user Analysis: Hospitals led the end-user segment in 2023 with a 52.3% revenue share, driven by rising adoption of protein and peptide therapies for chronic diseases. Hospitals offer the infrastructure and expertise required to manage complex treatments, leading to better patient outcomes. Growth in chronic conditions and regulatory approvals for oral peptide drugs support hospital-based demand. Additionally, expanding healthcare facilities in emerging markets are contributing to the segment’s continued growth within the oral proteins and peptides market.

Market Segments

By Product Type

- Ferric Gluconate

- Low Molecular Weight Iron Dextran

- Iron Sucrose

- Ferric Carboxyl Maltose

By Application

- Diabetes

- Gastric & Digestive Disorders

- Bone Diseases

- Hormonal Disorders

By Drug Type

- Linaclotide

- Calcitonin

- Insulin

- Plecanatide

- Octreotide

By End-user

- Hospitals

- Pharmaceutical Companies

- Others

Regional Analysis

North America: Market Leader in Oral Proteins and Peptides

In 2023, North America led the global oral proteins and peptides market, accounting for a dominant revenue share of 38.2%. This leadership is attributed to advancements in drug delivery technologies and increasing demand for innovative, non-invasive therapeutic options targeting chronic conditions such as diabetes and inflammatory disorders. Enhanced patient compliance and shifting preferences toward oral treatment modalities have further supported regional growth.

A significant development driving innovation is from Biora Therapeutics, a U.S.-based company, which plans to present preclinical data on its BioJet Systemic Oral Delivery Platform at the Next Gen Peptide Formulation & Delivery Summit in June 2024. This technology is designed to improve systemic absorption of therapeutic proteins and peptides, addressing key challenges in oral delivery.

The region also benefits from strong biotechnology R&D, supportive regulatory frameworks, and high healthcare investment levels. Collaborative efforts between biotechnology firms and academic research institutions have further accelerated the commercialization of oral protein-based therapeutics, reinforcing North America’s position as a market leader.

Asia Pacific: Fastest Growing Regional Market

The Asia Pacific region is projected to register the highest CAGR over the forecast period, driven by the rising prevalence of chronic diseases and ongoing improvements in healthcare infrastructure. Countries such as India and China are witnessing an increase in diabetes and cardiovascular conditions, fueling demand for advanced treatment options such as oral proteins and peptides.

Government initiatives to boost biotechnology research, along with rising healthcare expenditure, are creating a favorable environment for market expansion. Additionally, strategic partnerships between regional pharmaceutical companies and global biotech firms are facilitating technology transfer and the development of localized oral therapeutic solutions.

Advancements in drug encapsulation and delivery platforms, tailored to meet regional needs, are expected to enhance product availability. With growing awareness and acceptance of non-invasive therapies, Asia Pacific is well-positioned for robust growth in the oral proteins and peptides market.

Emerging Trends

- Regulatory Milestones and Label Expansions: The first oral peptide drug, semaglutide (Rybelsus), was approved by the U.S. FDA in September 2019 as an adjunct to diet and exercise for type 2 diabetes mellitus. In June 2024, its supplemental new-drug application enabled updated dosing recommendations and a second manufacturing site, reflecting growing regulatory support for oral peptide formulations.

- Rapid Growth in Clinical Development: Interventional studies of oral peptide therapies have proliferated. For example, a Phase IIb trial (NCT06473662) randomized 153 type 2 diabetes patients to receive 75 IU or 150 IU of an oral insulin capsule twice daily for 12 weeks, demonstrating feasibility of non-injectable insulin delivery.

- Broadened Therapeutic Indications: Beyond glycemic control, oral peptides are being evaluated in metabolic liver disease. The SOUL trial is emulating a cardiovascular outcomes study of oral semaglutide versus sitagliptin in patients with type 2 diabetes and established atherosclerotic cardiovascular disease or chronic kidney disease, marking an expansion into cardiorenal risk reduction.

- Advanced Formulation Technologies: Low bioavailability (<1%) has driven the development of protective carriers. Chemical modifications (e.g., cyclization, D-amino acid substitution), enzyme inhibitors, and nanoparticle-based permeation enhancers are being combined to shield peptides from degradation and facilitate receptor-mediated uptake in the intestine.

Use Cases

- Improved Glycemic Control in Type 2 Diabetes: Oral semaglutide achieves clinically meaningful HbA1c reductions. In a 26-week monotherapy trial (NCT02906930), mean HbA1c fell by 1.0% with 7 mg and by 1.5% with 14 mg doses versus placebo, enabling effective blood-sugar management without injections.

- Weight Reduction Support: Concurrent with glycemic benefits, oral semaglutide induced weight loss. The same 26-week trial reported average weight reductions of 1.9 kg (7 mg) and 2.3 kg (14 mg) compared to placebo, illustrating a dual role in metabolic therapy.

- Nonalcoholic Steatohepatitis (NASH) Intervention: In an exploratory Phase 2 study (ORA-D-N02), 36 patients with NASH and type 2 diabetes received 8 mg oral insulin twice daily. Liver-fat content was assessed by MRI-PDFF, positioning oral peptides as potential non-invasive treatments for fatty liver disease.

- Cardiovascular Risk Reduction: The SOUL trial database emulation is evaluating oral semaglutide’s impact on major adverse cardiovascular events (MACE) including CV death, nonfatal myocardial infarction, or nonfatal stroke in high-risk diabetic patients, highlighting a use case in secondary prevention.

- Enhanced Patient Adherence: By replacing injections with once-daily capsules, oral peptides are being positioned to improve long-term adherence rates. Steady-state plasma concentrations of semaglutide (6.7 nmol/L for 7 mg; 14.6 nmol/L for 14 mg) are achieved within 4–5 weeks, supporting convenient dosing regimens.

Conclusion

The oral proteins and peptides market is evolving rapidly, driven by technological advancements, increasing prevalence of chronic diseases, and a growing demand for non-invasive therapies. Innovations in formulation science, regulatory approvals, and expanding clinical applications are enabling enhanced bioavailability and therapeutic efficacy.

North America leads in adoption, while Asia Pacific is poised for the fastest growth. Use cases such as improved glycemic control, weight loss, and cardiovascular risk reduction underscore their broad therapeutic potential. As research and strategic collaborations progress, oral peptide therapeutics are expected to redefine treatment standards and improve patient compliance across multiple disease areas.