Table of Contents

Overview

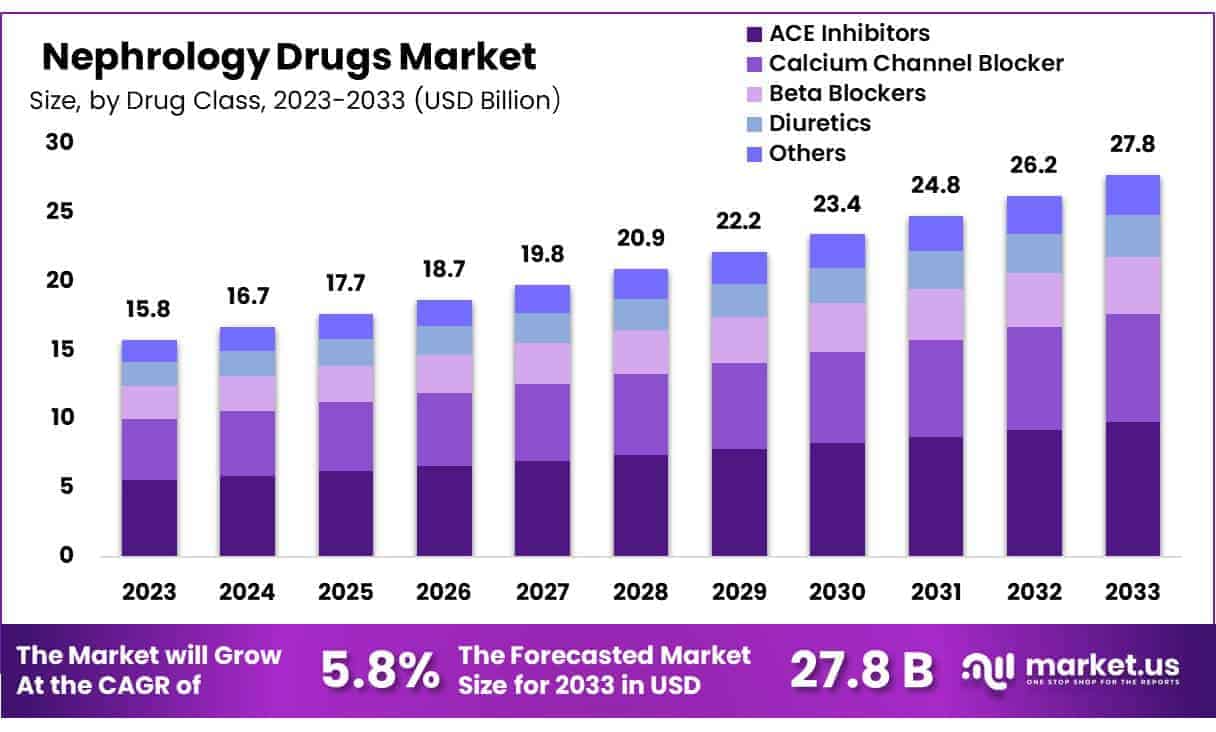

New York, NY – Oct 20, 2025 – Global Nephrology Drugs Market size is expected to be worth around USD 27.8 Billion by 2033 from USD 16.7 Billion in 2024, growing at a CAGR of 5.8% during the forecast period from 2025 to 2033.

The Nephrology Drugs Market plays a vital role in managing and treating kidney-related disorders such as chronic kidney disease (CKD), acute kidney injury, and nephrotic syndrome. These drugs are essential in maintaining renal function, controlling symptoms, and improving patient outcomes. With the growing global prevalence of kidney diseases due to diabetes, hypertension, and lifestyle changes, demand for nephrology therapeutics continues to rise steadily.

Pharmaceutical advancements have led to the development of innovative drug classes, including angiotensin receptor blockers (ARBs), diuretics, erythropoiesis-stimulating agents (ESAs), and novel immunosuppressants. These therapies are significantly improving disease management and reducing the burden of renal complications. Furthermore, ongoing clinical trials and the approval of new biologics are expanding treatment options and boosting market growth.

The global Nephrology Drugs Market is expected to witness substantial expansion, driven by increasing healthcare expenditure, better diagnostic capabilities, and rising awareness of kidney health. The growing adoption of precision medicine and the integration of digital health solutions are further enhancing patient care and treatment adherence.

Pharmaceutical companies are focusing on strategic collaborations, R&D investments, and the launch of targeted therapies to address unmet medical needs in nephrology. As the incidence of kidney disorders continues to climb globally, nephrology drugs are set to remain a cornerstone in improving patient quality of life and advancing renal care.

Key Takeaways

- Market Size: Global Nephrology Drugs Market size is expected to be worth around USD 27.8 Billion by 2033 from USD 16.7 Billion in 2024, growing at a CAGR of 5.8% during the forecast period from 2025 to 2033.

- By Drug Class: The ACE inhibitors segment dominated the global market, accounting for 27% of total revenue. Their widespread use in managing hypertension and chronic kidney diseases underscores their continued therapeutic significance.

- By Route of Administration: In 2023, the oral segment held a leading position with a 41% revenue share, driven by its ease of administration, improved patient compliance, and increasing availability of oral formulations for long-term renal care.

- By Distribution Channel: Hospital pharmacies led the distribution network due to the high volume of nephrology patients requiring specialized prescriptions and close clinical supervision.

- Regional Insights: North America remained the dominant regional market in 2023, capturing over 45% of global revenue, supported by advanced healthcare infrastructure, rising chronic kidney disease prevalence, and strong pharmaceutical innovation.

- Retail Pharmacy Growth: Retail pharmacies play a crucial role in chronic kidney disease management by providing convenient access to maintenance drugs and supporting patient education initiatives.

- Innovation and R&D: Ongoing advancements in drug discovery and biologics development are expanding treatment options, improving patient outcomes, and driving the overall growth of the nephrology drugs market.

Regional Analysis

North America:

North America continued to dominate the global nephrology drugs market in 2023, accounting for over 45% of total revenue. This leadership is driven by a combination of advanced healthcare infrastructure, high disease prevalence, and substantial investment in research and development. The region’s well-established regulatory framework supports the approval and commercialization of innovative nephrology therapies, strengthening its market position.

Growing awareness of kidney health among healthcare professionals and patients has increased the demand for nephrology drugs, including erythropoiesis-stimulating agents and phosphate binders. The ageing population, coupled with the rising incidence of diabetes and hypertension key risk factors for chronic kidney disease (CKD)—further contributes to market expansion.

According to the Population Reference Bureau, the U.S. population aged 65 years and older is projected to grow from 58 million in 2022 to 82 million by 2050. The strong presence of leading pharmaceutical companies and the continued progress in clinical trials for novel therapies reinforce North America’s dominance in the global nephrology drugs landscape.

Asia Pacific:

The Asia Pacific region is projected to register the highest compound annual growth rate (CAGR) during the forecast period. The increasing prevalence of chronic kidney disease (CKD) and growing awareness of renal health are key growth drivers. Rapid urbanization, lifestyle shifts, and poor dietary habits have led to higher rates of diabetes and hypertension, significantly elevating CKD incidence.

Expanding healthcare infrastructure, rising government healthcare initiatives, and greater investment in biotechnology and pharmaceuticals are further propelling market development. Emerging economies such as India and China are playing a pivotal role through increased healthcare spending and clinical research activities. Moreover, the introduction of innovative therapies is broadening treatment accessibility and improving patient outcomes.

Globally, chronic kidney disease (CKD) remains a major public health concern, with an estimated 13.4% prevalence. Within Asia, the total CKD burden is estimated at 434.3 million individuals, including 65.6 million suffering from advanced disease, underscoring the region’s urgent need for improved nephrology care and pharmaceutical intervention.

Frequently Asked Questions on Nephrology Drugs

- Why are nephrology drugs important?

Nephrology drugs play a crucial role in maintaining renal health by regulating blood pressure, controlling phosphate levels, and managing anemia. They significantly improve patient outcomes and reduce complications associated with chronic kidney and metabolic disorders. - What are the major types of nephrology drugs?

Key drug classes include ACE inhibitors, angiotensin receptor blockers (ARBs), diuretics, phosphate binders, erythropoiesis-stimulating agents (ESAs), and immunosuppressants. These medications are commonly used to manage blood pressure, anemia, and electrolyte imbalances in kidney disease patients. - Which factors are driving the nephrology drugs market?

Market growth is driven by the rising prevalence of chronic kidney disease (CKD), an ageing global population, and increased R&D investments. Technological advancements and improved access to renal care also contribute significantly to the expanding market. - Which region leads the global nephrology drugs market?

North America leads the global market, accounting for over 45% of revenue in 2023. This dominance is supported by advanced healthcare infrastructure, strong pharmaceutical presence, and high prevalence of chronic kidney diseases. - Which drug class dominates the nephrology drugs market?

ACE inhibitors held the largest market share of 27% in 2023, driven by their effectiveness in managing hypertension and protecting renal function, especially among patients with chronic kidney disease and diabetes. - What is the most common route of administration for nephrology drugs?

The oral route dominates the market, accounting for 41% of global sales in 2023, due to convenience, higher patient adherence, and the availability of effective oral formulations for long-term kidney disease management. - Which distribution channel contributes most to nephrology drug sales?

Hospital pharmacies dominate the distribution network, given the high volume of prescriptions and specialized care required for nephrology patients. Retail pharmacies also play a vital role in chronic disease management and patient education. - What future trends are shaping the nephrology drugs market?

Emerging trends include the development of biologics, precision medicine, and AI-driven clinical research. Increased focus on early diagnosis, digital monitoring, and patient-centered therapies will drive future innovation in nephrology care.

Conclusion

The global Nephrology Drugs Market is poised for sustained growth, driven by the rising prevalence of chronic kidney disease, advancements in drug development, and increasing healthcare investments. North America continues to lead the market, while the Asia Pacific region shows promising expansion due to growing awareness and healthcare infrastructure improvements.

Continuous R&D efforts, innovation in biologics, and the adoption of precision medicine are transforming renal care and enhancing patient outcomes. As kidney-related disorders become a growing global concern, nephrology drugs will remain essential in ensuring effective treatment, improved quality of life, and long-term disease management.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)