Table of Contents

Overview

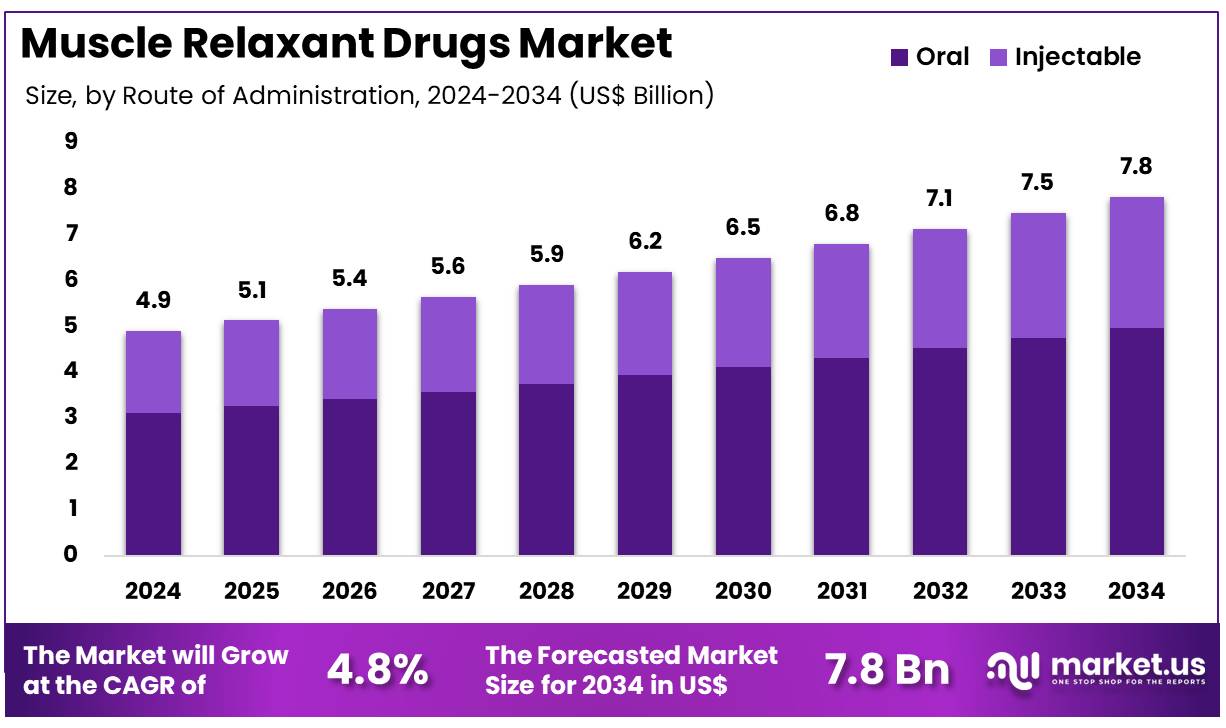

New York, NY – Dec 08, 2025 – Global Muscle Relaxant Drugs Market size is expected to be worth around US$ 7.8 Billion by 2034 from US$ 4.9 Billion in 2024, growing at a CAGR of 4.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.4% share with a revenue of US$ 1.9 Billion.

The global market for muscle relaxant drugs has been demonstrating steady expansion, supported by rising incidences of musculoskeletal disorders and growing demand for effective pain-management therapies. Increasing cases of muscle spasms, lower back pain, and arthritis have been driving the adoption of centrally acting and direct-acting muscle relaxants across healthcare settings. The growth of the market has also been supported by advancements in pharmaceutical formulations and the introduction of safer therapeutics with improved efficacy profiles.

Demand for prescription muscle relaxants has been increasing in hospitals, orthopedic centers, and rehabilitation facilities, where the medications are being used to manage acute and chronic conditions. The adoption of non-opioid alternatives has further contributed to market growth as healthcare professionals continue to prioritize safer pain-relief solutions. The market has also been influenced by rising awareness of early treatment and improved diagnostic rates for musculoskeletal conditions.

North America has been holding a dominant share due to high healthcare expenditure and strong presence of leading pharmaceutical manufacturers. Asia-Pacific has been projected to exhibit notable growth, supported by increasing patient populations and expanding access to advanced healthcare services. Strategic collaborations, product launches, and clinical research activities have been shaping the competitive landscape. The muscle relaxant drugs market is expected to maintain a positive trajectory as investment in research and development continues and as healthcare systems prioritize effective pain-management therapies.

Key Takeaways

- In 2024, the muscle relaxant drugs market recorded revenue of US$ 4.9 billion, growing at a CAGR of 4.8%, and is projected to reach US$ 7.8 billion by 2034.

- The drug type segment comprises skeletal muscle relaxant drugs, neuromuscular blocking agents, and facial muscle relaxant drugs, with skeletal muscle relaxant drugs leading in 2024 with a 50.6% market share.

- Based on route of administration, the market is categorized into oral and injectable, where the oral segment accounted for a significant 63.5% share.

- In terms of distribution channels, the market is segmented into hospital pharmacies, online pharmacies, and retail pharmacies, with hospital pharmacies dominating at 58.2% revenue share.

- North America emerged as the leading regional market, capturing a 38.4% share in 2024.

Regional Analysis

North America accounted for the highest revenue share of 38.4%, supported by the increasing prevalence of musculoskeletal disorders and chronic pain across the region. According to the Centers for Disease Control and Prevention (CDC), the age-adjusted prevalence of diagnosed arthritis in adults aged 18 and above reached 18.9% in 2022, demonstrating a substantial patient population requiring therapeutic interventions such as muscle relaxants for symptom alleviation.

In Canada, the demand for pain management solutions remains considerable. Statistics Canada reported in 2022 that 16.7% of individuals aged 15 years and older equivalent to 4.9 million people experienced a pain-related disability, illustrating the widespread need for effective pain and spasm relief. The increasing recognition of chronic pain management strategies, combined with a growing elderly demographic more susceptible to musculoskeletal ailments, has continued to support the expansion of the market in the region.

Further, while surgical volumes within the U.S. Military Health System recorded a slight decline from 4,649 procedures in 2022 to 4,413 in 2023, the broader North American healthcare ecosystem continues to perform a high number of surgical interventions. This sustained activity contributes to consistent demand for muscle relaxants for post-operative pain and spasm control.

Asia Pacific Expected to Register the Fastest CAGR

Asia Pacific is projected to exhibit the highest CAGR over the forecast period, driven by the rapidly expanding geriatric population and ongoing improvements in healthcare infrastructure. The United Nations’ World Population Ageing 2023 report highlights that nearly 60% of the global population resides in Asia and the Pacific, with a steadily aging demographic expected to increase the prevalence of age-associated musculoskeletal conditions. This trend is anticipated to enhance the demand for muscle relaxant therapies across the region.

Rising healthcare expenditure further accelerates market growth. In China, per capita healthcare spending reached US$672.45 in 2022, marking a 0.33% increase compared with 2021, indicating greater prioritization of healthcare services and improved access to treatment options. In India, a 2022 study found that 59.39% of middle-aged and older adults reported experiencing some form of pain, with 47.18% suffering from joint pain, underscoring a large unmet need for effective pain and spasm management solutions.

The expansion of healthcare facilities, coupled with increasing awareness of pain management strategies across diverse Asian economies, is expected to collectively support robust growth of the muscle relaxant drugs market throughout the Asia Pacific region.

Emerging Trends

- The global burden of low back pain has been increasing, and this has been driving sustained demand for muscle relaxant therapies. An estimated 619 million individuals were affected in 2020, and the number of cases is projected to reach 843 million by 2050, indicating persistent requirements for symptomatic management.

- Guideline-directed and cautious prescribing practices have been gaining prominence. The 2022 CDC–ACP clinical practice guideline advises that skeletal muscle relaxants should be used only when non-pharmacological interventions fail to provide adequate relief in acute low back pain, reflecting a shift toward conservative and safer treatment pathways.

- Enhanced safety regulations have been implemented to mitigate inappropriate prescribing. Beginning in Measurement Year 2025, six commonly used skeletal muscle relaxants, including carisoprodol and cyclobenzaprine, were incorporated into the CMS high-risk medication quality measures to reduce exposure among older adults.

- Clinical research activity has been expanding, with numerous interventional studies assessing new dosing strategies and emerging therapeutic applications. Recent examples include trials evaluating low-dose muscle relaxants in bronchoscopy procedures (NCT07035301) and objective monitoring protocols for anesthesia management (NCT03958201).

Use Cases

- Acute non-specific low back pain is frequently managed with short-term skeletal muscle relaxants when initial non-drug measures such as heat therapy or exercise do not provide sufficient relief. Utilization among adults aged 45–64 has been reported at up to 1.7% within the previous 30 days, illustrating controlled and time-limited prescribing.

- General anesthesia routinely incorporates neuromuscular blocking agents, including succinylcholine and rocuronium, to facilitate intubation and surgical access. The use of sugammadex for neuromuscular blockade reversal has demonstrated safety benefits by reducing the incidence of prolonged blockade, while boxed warnings for succinylcholine highlight the need for careful clinical assessment.

- Spasticity management in conditions such as pediatric cerebral palsy relies on targeted interventions including botulinum toxin injections. FDA-approved guidance recommends 1–2 Units/kg per injection site for lower-limb spasticity, supporting precise dosing for the hundreds of thousands of pediatric patients requiring treatment each year.

- Bronchoscopic procedures are being optimized through the adjunctive use of low-dose muscle relaxants to mitigate skeletal muscle injury during electroporation-based ablation. These innovations are currently being assessed in ongoing clinical trials to refine procedural safety and efficacy.

Frequently Asked Questions on Muscle Relaxant Drugs

- How do muscle relaxant drugs work?

These drugs function by depressing nerve transmission within the central nervous system or by blocking neuromuscular activity. This action leads to decreased muscle stiffness and improved mobility, supporting the management of acute or chronic musculoskeletal conditions requiring symptomatic relief. - What conditions are treated with muscle relaxants?

Muscle relaxants are prescribed for acute back pain, neck pain, fibromyalgia, multiple sclerosis, cerebral palsy, and post-operative muscle spasms. Their therapeutic role is centered on reducing involuntary contractions, facilitating patient comfort, and enhancing overall functional recovery in diverse clinical scenarios. - Are muscle relaxants safe for long-term use?

Long-term use is generally avoided due to risks of dependence, sedation, and reduced therapeutic effectiveness. Clinical guidelines recommend short-duration usage, with continued monitoring, as prolonged exposure may lead to adverse outcomes requiring adjustments in patient management strategies. - What are common side effects of muscle relaxant drugs?

Typical side effects include drowsiness, dizziness, dry mouth, and fatigue caused by central nervous system depression. In some cases, patients may experience gastrointestinal issues or blurred vision, necessitating careful dosage control and monitoring by healthcare professionals during treatment. - What are the major types of muscle relaxants?

Muscle relaxants are categorized into antispasmodics and antispastics. Antispasmodics act centrally to reduce involuntary muscle spasms, while antispastics target conditions such as multiple sclerosis by reducing muscle stiffness through actions on specific neural pathways. - Which regions dominate the muscle relaxant drugs market?

North America currently dominates due to higher healthcare spending, broad adoption of prescription therapies, and significant prevalence of back pain. Europe follows closely, while Asia-Pacific is witnessing accelerated growth supported by expanding healthcare infrastructure and rising patient awareness. - Who are the major players in the muscle relaxant drugs market?

Key players include Pfizer, Novartis, Teva Pharmaceuticals, Sanofi, and Acorda Therapeutics. These companies maintain prominence through extensive product portfolios, research investments, and distribution networks supporting availability of both branded and generic muscle relaxant formulations worldwide. - What trends are shaping the future of the muscle relaxant drugs market?

The market is shaped by increasing use of generics, rising preference for non-opioid pain management, and ongoing development of targeted therapies with improved safety profiles. Digital health tools are enhancing patient monitoring, supporting optimized treatment outcomes and higher therapeutic compliance.

Conclusion

The muscle relaxant drugs market is expected to maintain steady growth, driven by rising musculoskeletal disorders, expanding clinical applications, and increasing preference for non-opioid pain-management therapies. Demand has been supported by improved diagnostic rates, advancements in drug formulations, and broader adoption across hospitals and rehabilitation settings.

North America continues to lead, while Asia Pacific is set to record the fastest expansion due to an aging population and strengthening healthcare infrastructure. Evolving clinical guidelines, enhanced safety regulations, and active research initiatives are shaping future developments, ensuring continued investment and sustained market progression over the coming decade.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)