Table of Contents

Overview

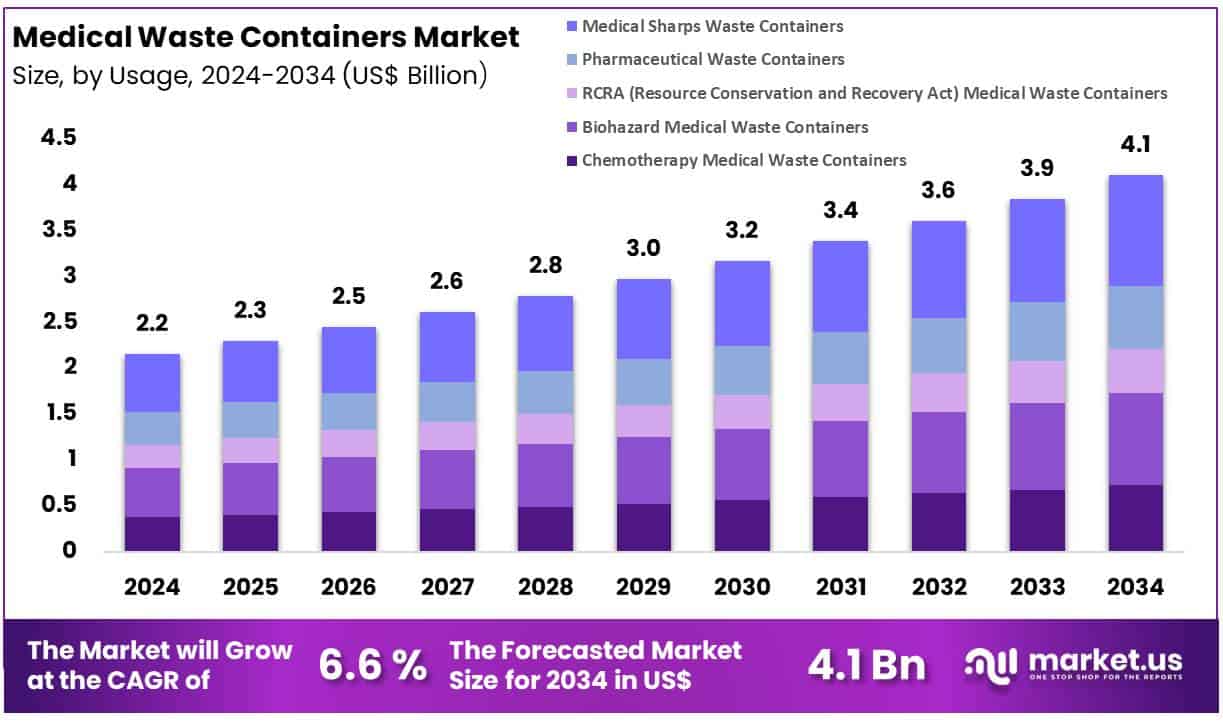

New York, NY – May 27, 2025 – Global Medical Waste Containers Market size is expected to be worth around US$ 4.1 Billion by 2033 from US$ 2.16 Billion in 2024, growing at a CAGR of 6.6% during the forecast period from 2024 to 2033.

The global demand for medical waste containers is increasing rapidly, driven by the growing volume of hazardous and infectious waste generated by hospitals, laboratories, and diagnostic centers. These specialized containers play a critical role in ensuring the safe collection, storage, transportation, and disposal of medical waste, thereby preventing cross-contamination, disease transmission, and environmental pollution.

Medical waste containers are designed to comply with strict health and safety regulations. They are manufactured using puncture-resistant, leak-proof materials and are color-coded and labeled for easy segregation of sharps, biohazard waste, pharmaceutical residues, and cytotoxic materials. According to the World Health Organization (WHO), an estimated 15% of total healthcare waste is hazardous, reinforcing the importance of robust containment solutions.

Regulatory mandates from bodies such as the U.S. Occupational Safety and Health Administration (OSHA) and Environmental Protection Agency (EPA) have led to an increase in the adoption of compliant waste containers across medical facilities. The rise in chronic diseases, surgical procedures, and home healthcare services has further accelerated market demand.

North America remains the leading region due to advanced healthcare infrastructure and stringent waste management protocols. However, Asia-Pacific is expected to witness the fastest growth, driven by healthcare expansion and increasing awareness of infection control standards. Continuous innovations in container design, sustainability features, and smart tracking technologies are expected to shape the next phase of growth in this essential healthcare segment.

Key Takeaways

- Market Size: In 2024, the Medical Waste Containers Market generated a revenue of approximately US$ 2.16 billion and is projected to reach around US$ 3.85 billion by 2034, expanding at a compound annual growth rate (CAGR) of 6.6%.

- Usage Categories: Medical Sharps Waste Containers emerged as the dominant segment, accounting for 29.3% of the total market revenue. These containers are widely used for the safe disposal of needles, scalpels, and other sharp instruments, reducing the risk of injury and contamination.

- Type of Waste: the Infectious and Pathological Waste segment led the market, capturing a 38.6% share. This reflects the increasing volume of biologically hazardous waste generated by hospitals, clinics, and laboratories.

- Product Type: Disposable Medical Waste Containers made the largest contribution to market revenue, holding a substantial 72.6% share. Their single-use design supports strict infection control protocols and is preferred across healthcare settings for its convenience and safety.

- Regional Analysis: North America remained the leading contributor to the global market, accounting for 43.6% of total revenue. This leadership is attributed to well-established regulatory frameworks, high healthcare expenditure, and advanced waste management infrastructure.

Segmentation Analysis

- By Usage Analysis: In 2024, Medical Sharps Waste Containers accounted for 29.3% of the usage segment, driven by the increasing volume of procedures involving needles and sharp objects. These containers reduce the risk of injuries and contamination, ensuring regulatory compliance. RCRA containers are projected to witness the fastest growth, with a CAGR of 8.1%, fueled by stringent waste disposal regulations requiring certified solutions for hazardous waste handling in healthcare facilities.

- By Type of Waste Analysis: Infectious and pathological waste dominated the waste type segment, comprising materials contaminated with blood, tissues, or pathogens. This segment’s growth is attributed to the rising number of medical procedures producing hazardous biological waste. Regulatory mandates enforcing strict infection control and safe disposal practices continue to drive demand for specialized containment solutions, ensuring public health protection and compliance with global safety standards.

- By Product Analysis: The disposable medical waste containers segment held the largest share at 72.6%, favored for their single-use design, ease of handling, and regulatory compliance. These containers are widely used to manage sharps, infectious, and hazardous waste safely. Growing procedural volumes and a focus on hygiene and convenience support their widespread adoption. Moreover, advancements in sustainable materials have increased demand for eco-friendly disposable options in healthcare facilities.

- By End Use Analysis: Hospitals led the end-user segment due to their high volume of waste generation from surgeries, diagnostics, and daily patient care. These facilities require reliable, compliant containers for managing sharps and infectious materials. Regulatory enforcement and a heightened focus on infection control have further driven container adoption in hospitals, reinforcing their leadership position in the market. Investments in high-quality containment solutions support operational efficiency and safety compliance.

Market Segments

By Usage

- Chemotherapy Medical Waste Containers

- Biohazard Medical Waste Containers

- RCRA (Resource Conservation and Recovery Act) Medical Waste Containers

- Pharmaceutical Waste Containers

- Medical Sharps Waste Containers

By Type of Waste

- Infectious & Pathological Waste

- Non-infectious Waste

- Radioactive Waste

- Sharps Waste

- Pharmaceutical Waste

By Product

- Disposable Medical Waste Containers

- Reusable Medical Waste Containers

By End Use

- Hospitals

- Clinics & Physicians’ Offices

- Pharmaceutical Companies

- Long Term Care & Urgent Care Centers

- Pharmacies

- Other Generators

Regional Analysis

North America Leads the Global Medical Waste Containers Market

North America retained its dominant position in the global medical waste containers market, supported by a robust healthcare infrastructure and stringent regulatory oversight. Agencies such as the U.S. Environmental Protection Agency (EPA) and Health Canada mandate strict protocols for waste handling, driving demand for compliant containers.

The region’s high volume of chronic disease treatments and surgical procedures further increases medical waste output. Additionally, rising focus on infection control, workplace safety, and eco-friendly innovations contributes to sustained growth and reinforces North America’s market leadership.

Emerging Trends

- Stricter Segregation Standards: Container use is being driven by enhanced regulations that require waste to be separated at the source. Color-coded bins for infectious versus non-infectious waste are now standard in many health systems. This measure reduces cross-contamination risks and is recommended by international guidelines for safe health-care waste management.

- Growth in Sharps Container Adoption: The use of FDA-cleared sharps disposal containers has been reinforced, particularly after large-scale vaccination campaigns. These rigid, puncture-resistant containers must be replaced once three-quarters full and are regulated as Class II medical devices.

- Shift to Hands-Free, Touchless Designs: To minimize contact and infection risk, foot-operated and sensor-equipped containers are gaining traction. Touchless models have been engineered to exceed CDC decontamination standards by up to four times, supporting higher hygiene levels in clinical areas.

- Sustainability and Eco-Friendly Materials: Interest is rising in containers made from recyclable or biodegradable plastics. Policy statements highlight the human and environmental impacts of health-care waste, prompting initiatives to develop containers that reduce plastic volume and facilitate recycling.

- Data-Driven Inventory Management: Although more common in municipal waste, pilot programs are applying fill-level sensors to medical bins. Real-time monitoring helps facilities plan pickups, minimizing overflows and reducing operating costs. This innovation aligns with broader smart-facility and IoT trends in health care.

Use Cases

- Hospital Bed Waste Management: In high-income settings, hazardous waste generation averages 0.5 kg per hospital bed per day ([World Health Organization][5]). A 200-bed hospital thus produces about 100 kg of hazardous waste daily. If a standard 5 L container holds roughly 5 kg, approximately 20 such containers are required each day for proper segregation.

- Annual Hospital Waste Volumes: U.S. hospitals alone generate nearly 3.2 million tons of medical waste per year, of which 10–15 % is classified as infectious and must be stored in specialized containers. This equates to 320,000–480,000 tons of hazardous material annually, necessitating robust container systems.

- Sharps Disposal in Vaccination Centers: During mass vaccination campaigns, millions of syringes are used daily. Each used needle requires a puncture-resistant sharps container. For example, administering 1 million injections per day generates 1 million sharps, all of which must be deposited into FDA-approved containers designed to close automatically when filled to ¾ capacity.

- Outpatient and Home Care Settings: As self-administration of injectable therapies grows, the number of home users requiring portable sharps containers has increased. Portable sharps bins (1 L or 2 L sizes) are now sold CDC-approved for consumer use, facilitating safe disposal and reducing community needle-stick injuries.

- Laboratory and Diagnostic Facilities: In labs handling specimens, puncture-resistant containers are deployed at every bench. To prevent aerosol generation, sharps containers are positioned adjacent to workstations and replaced weekly, based on volume thresholds defined by facility protocols and CDC safe handling guidelines.

Conclusion

The global medical waste containers market is poised for sustained growth, driven by increasing volumes of hazardous waste, stringent regulatory frameworks, and rising emphasis on infection control and environmental safety. With strong adoption across hospitals, diagnostic centers, and outpatient settings, the market is evolving through innovations in touchless design, eco-friendly materials, and smart waste tracking.

North America remains the market leader, while Asia-Pacific shows promising growth. As healthcare services expand globally, the demand for compliant, safe, and efficient medical waste disposal solutions will continue to grow, positioning medical waste containers as an essential component of healthcare waste management systems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)