Table of Contents

Overview

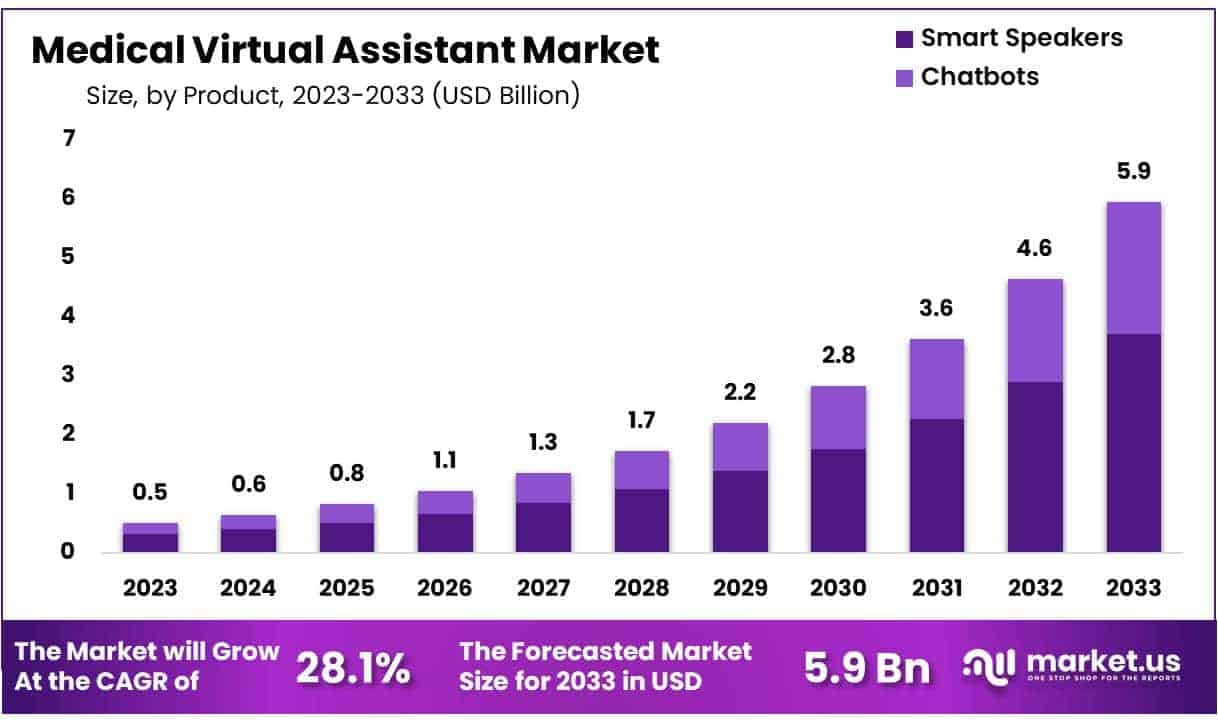

New York, NY – May 14, 2025 – Global Medical Virtual Assistant Market size is expected to be worth around US$ 5.9 billion by 2033 from US$ 0.5 billion in 2023, growing at a CAGR of 28.1% during the forecast period 2024 to 2033.

Medical Virtual Assistants (MVAs) are transforming patient care by streamlining communication between patients and healthcare providers, improving operational workflows, and enhancing patient engagement. These AI-powered tools are designed to assist with a wide range of tasks, including appointment scheduling, symptom checking, medical transcription, remote patient monitoring, and medication reminders.

Driven by advancements in natural language processing (NLP) and machine learning, MVAs can understand and respond to patient queries with high accuracy. Integration into electronic health records (EHRs) allows for seamless documentation and quick access to patient histories, thereby reducing administrative burden on healthcare professionals.

The adoption of MVAs has accelerated in both clinical and homecare settings, especially after the COVID-19 pandemic emphasized the need for contactless healthcare services. Patients benefit from 24/7 support, multilingual capabilities, and increased privacy, while providers experience improved workflow efficiency and cost reduction.

MVAs are also supporting chronic disease management through regular follow-ups and alerts, improving treatment adherence and health outcomes. Hospitals and clinics are increasingly incorporating these assistants into their digital strategies to enhance service delivery.

As the global healthcare system continues its digital transformation, Medical Virtual Assistants are expected to play a critical role in reshaping patient-provider interactions and addressing staffing challenges in an efficient, scalable manner.

Key Takeaways

- Market Size and Growth: In 2023, the global medical virtual assistant market generated revenue of approximately US$ 5.0 billion. The market is projected to expand at a compound annual growth rate (CAGR) of 28.1%, reaching a value of US$ 5.9 billion by 2033.

- By Product Type: The market is segmented into chatbots and smart speakers. Among these, smart speakers dominated in 2023, accounting for a market share of 62.4%, driven by their increasing integration in clinical environments and home care settings.

- By User Interface: Based on interface technology, the market is categorized into text-based, automatic speech recognition, and text-to-speech solutions. Automatic speech recognition emerged as the leading segment, contributing 53.7% of the overall market share in 2023, due to its ability to facilitate hands-free communication.

- By End User: The end-user landscape includes patients, healthcare providers, and healthcare payers. Healthcare providers were the primary adopters, representing the largest revenue share at 48.9%, owing to increasing demand for workflow automation and virtual patient interactions.

- By Region: North America remained the leading regional market in 2023, capturing a market share of 39.2%, supported by advanced healthcare infrastructure and high adoption of AI-driven healthcare technologies.

Segmentation Analysis

- By Product Analysis: In 2023, the smart speakers segment accounted for 62.4% of the market, driven by growing adoption of voice-activated tools in clinical and home care settings. Their hands-free operation supports functions like medication reminders and patient queries. Enhanced by AI, smart speakers now offer real-time, conversational responses. Their integration in chronic disease management and remote monitoring is expected to further drive their use across both healthcare facilities and personal health environments.

- By User Interface Analysis: Automatic speech recognition held 53.7% market share in 2023 due to the rising demand for intuitive, hands-free interactions in healthcare. This interface allows natural conversation between users and virtual assistants, improving efficiency in tasks such as telemedicine support, clinical note-taking, and remote monitoring. Advances in medical vocabulary recognition and voice accuracy are further enhancing its adoption, particularly in high-pressure environments like hospitals where speed and precision are critical.

- By End-user Analysis: Healthcare providers led the end-user segment in 2023 with a 48.9% revenue share, fueled by increasing demand for administrative automation and enhanced patient engagement. Virtual assistants are being used to streamline appointment scheduling, manage medical records, and support follow-up communications. Their integration with electronic health records (EHRs) is also improving decision-making and care coordination, making them valuable tools for both clinical efficiency and patient satisfaction in modern healthcare systems.

Market Segments

By Product

- Chatbots

- Smart Speakers

By User Interface

- Text Based

- Automatic Speech Recognition

- Text-to-Speech Based

By End-user

- Patients

- Healthcare Providers

- Healthcare Payers

Regional Analysis

North America Leads the Medical Virtual Assistant Market

In 2023, North America accounted for the largest revenue share of 39.2% in the medical virtual assistant market. This dominance is attributed to the rising adoption of AI-powered healthcare solutions aimed at enhancing patient engagement and streamlining provider-patient communication. The region has witnessed significant integration of virtual assistants in telemedicine, clinical workflows, and administrative operations.

A notable development includes AtlantiCare’s partnership with Orbita, Inc. in October 2022, enabling the deployment of a conversational AI platform. This implementation improved patient access through self-scheduling capabilities and enhanced user experience.

Furthermore, advancements in natural language processing (NLP) and AI technologies are enabling healthcare systems to reduce administrative burden and optimize care delivery, thereby accelerating the adoption of virtual assistant technologies across hospitals and clinics in the region.

Asia Pacific Expected to Register the Fastest Growth Rate

The Asia Pacific region is projected to witness the highest CAGR over the forecast period, supported by increasing investments in digital health and a growing need for accessible mental health services. In May 2024, Fortis Healthcare collaborated with United We Care to launch Adayu Mindfulness, an AI-based mental health service offering 24/7 virtual assistance and self-assessment tools.

This initiative reflects the region’s expanding focus on AI-enabled healthcare infrastructure. Government support and rising awareness of digital health applications are expected to drive the use of medical virtual assistants, particularly in mental health, chronic disease management, and remote patient monitoring.

Emerging Trends

- Personalized Health Coaching via AI Chatbots: The adoption of AI-powered chatbots as virtual health assistants has been accelerated by their ability to deliver continuous, tailored guidance for lifestyle and chronic disease management. These systems adapt to individual health goals and contexts, offering real-time motivational support and education, thus enhancing patient engagement and self-management outcomes.

- Integration of Large Language Models for Context-Aware Interactions: Recent developments in large language models (LLMs) have enabled virtual assistants to understand complex medical queries more accurately and maintain conversational context over multiple exchanges. This capability supports more nuanced health information delivery and reduces the risk of miscommunication in patient–assistant dialogues.

- Domain-Specific Virtual Assistants for Clinical Triage: The emergence of specialized virtual assistants for areas such as emergency neurology triage has been validated in clinical studies. For example, an AI-powered assistant achieved neurologist agreement in 98.5% of syndromic diagnoses and consistently included the correct diagnosis within its top five suggestions.

Use Cases

- Emergency Neurological Triage: An AI virtual assistant was evaluated for triaging urgent neurological conditions. In expert review, it matched neurologist diagnoses 98.5% of the time and guided patients through an average of 16.5 questions in 5.5 minutes, demonstrating both efficiency and high diagnostic concordance.

- AI-Driven Appointment Scheduling: Machine learning–based scheduling systems have significantly reduced no-show rates. In one hospital initiative analyzing over 32,000 outpatient MRI appointments, an AI model achieved an ROC AUC of 0.746 for no-show prediction and, when combined with targeted telephone reminders, lowered the no-show rate from 19.3% to 15.9% over six months.

- Patient Navigation and Self-Scheduling Support: Health care chatbots can guide patients through complex care pathways by identifying appropriate providers and facilitating appointment bookings. Implementations have reported improved access to care and reduced administrative burden by automating routine scheduling tasks.

Conclusion

In conclusion, the Medical Virtual Assistant (MVA) market is poised for transformative growth, driven by advancements in AI, NLP, and healthcare digitalization. With a projected CAGR of 28.1%, the market is expected to expand from US$ 0.5 billion in 2023 to US$ 5.9 billion by 2033.

MVAs are reshaping patient-provider interactions through enhanced accessibility, administrative automation, and personalized care delivery. Regional leadership by North America and rapid adoption in Asia Pacific underscore global momentum. As use cases expand into clinical triage, mental health, and chronic disease management, MVAs are set to become an integral component of modern healthcare systems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)