Table of Contents

- Introduction

- Editor’s Choice

- Global Meat Substitutes Market Overview

- Production Volume of Meat Substitutes Statistics

- Price of Meat Substitutes Statistics

- Leading Meat Substitute Brands Ranked by Brand Awareness

- Demographics of Plant-Based Meat Alternatives

- Consumption Pattern of Plant-Based Meat Alternatives

- Advances in Meat Substitute Production Technologies

- Challenges Faced by the Meat Substitutes Industry Statistics

- Recent Development

- Conclusion

- FAQs

Introduction

Meat Substitutes Statistics: Meat substitutes, made from plant proteins, fungi, or cultured cells, mimic the flavor and texture of traditional meats. Offered in diverse formats like burgers and sausages, they cater to dietary and ethical concerns.

Created through methods like extrusion and fermentation, these substitutes frequently tout better nutritional compositions with lower saturated fat and cholesterol levels.

Propelled by the growing demand for sustainable food choices. The meat substitute market garners investments from established players and up-and-coming businesses. Their versatility and environmentally friendly characteristics could revolutionize the food sector.

Editor’s Choice

- By 2033, the global meat substitutes market is forecasted to attain a revenue of USD 29 billion.

- In the distribution of meat substitutes. The food service sector dominates with a commanding market share of 76%. While the retail segment holds a notable but comparatively smaller share of 24%.

- The average revenue per capita of meat substitutes will rise to $2.09 in 2028.

- China leads the global meat substitutes market with a substantial revenue of USD 2.371 billion, followed closely by the United States at USD 2.06 billion.

- By 2028, the production volume of meat substitutes is expected to reach 0.98 billion kilograms.

- Beginning at $15.06 in 2018, the price of meat substitutes slightly decreased to $14.16 in 2019 before remaining relatively stable at $14.10 in 2020.

- In 2023, MorningStar Farms and Beyond Meat emerged as the leading meat substitute brands in the United States. 56% and 54% of respondents indicated awareness of these brands, respectively.

Global Meat Substitutes Market Overview

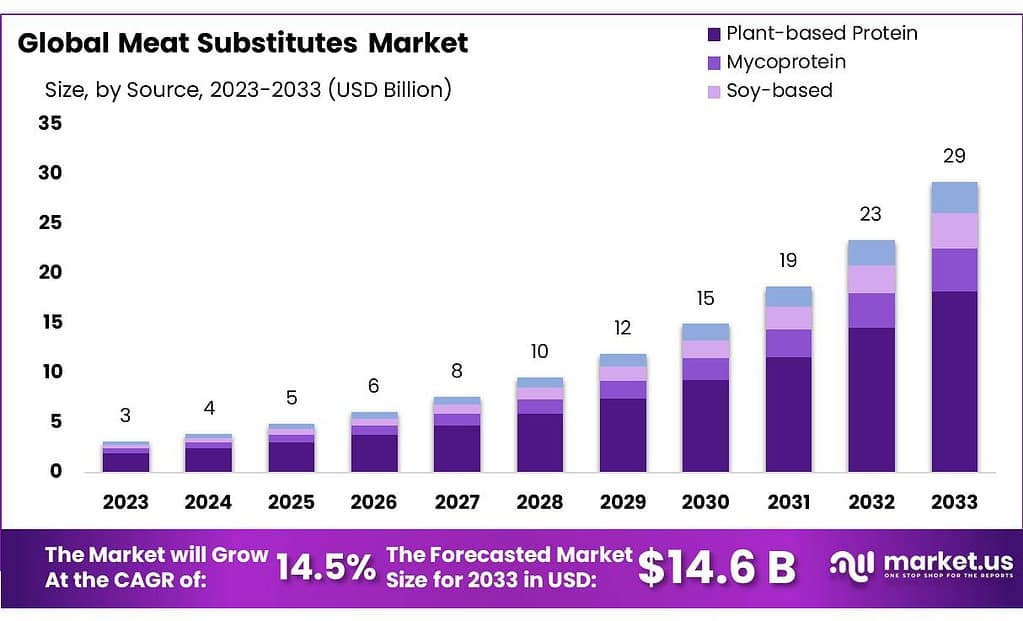

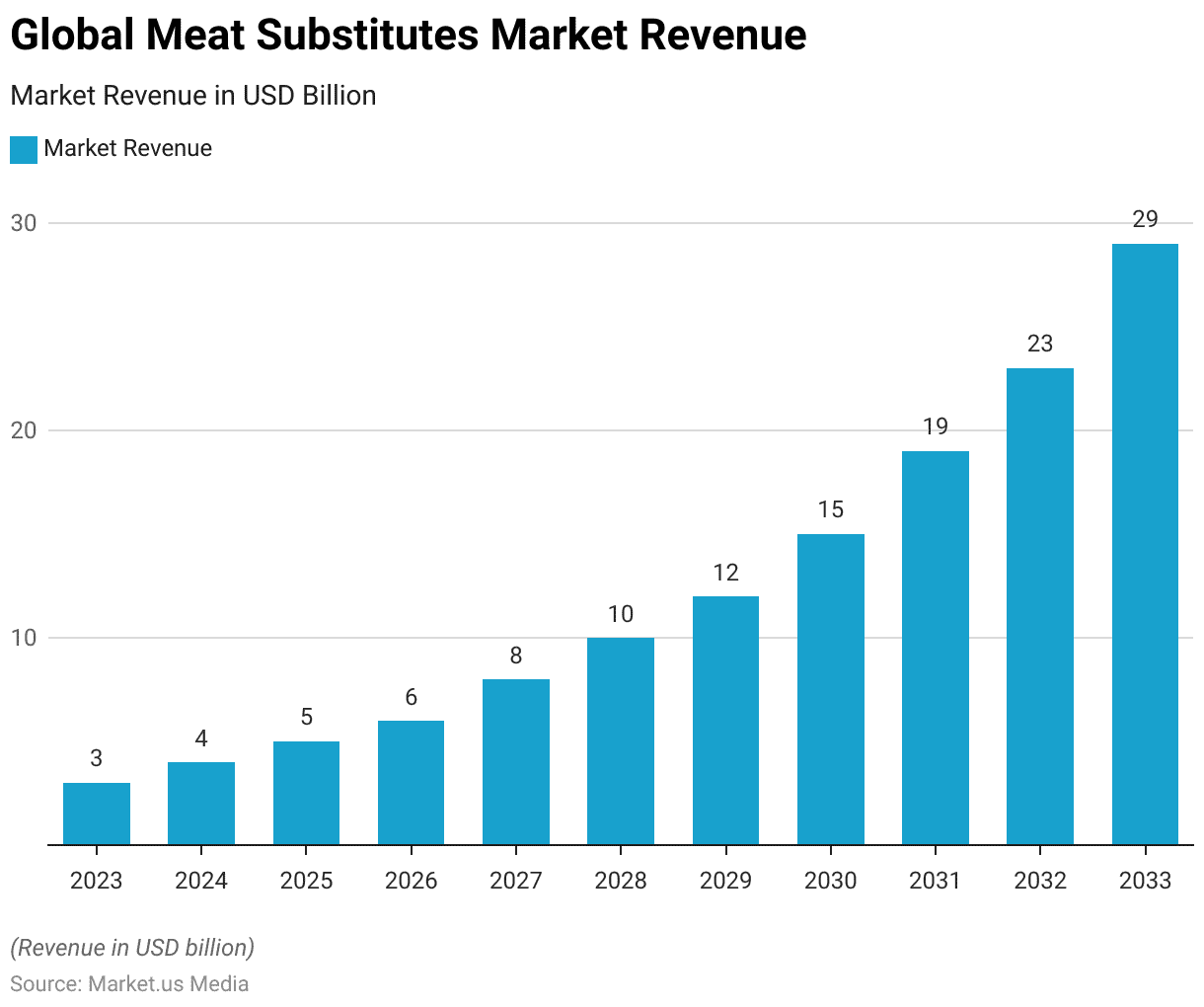

Global Meat Substitutes Market Size Statistics

- The revenue generated by the global meat substitutes market is anticipated to witness significant growth over the forecast period from 2023 to 2033 at a CAGR of 14.5%.

- Beginning at USD 3 billion in 2023, the market revenue is projected to increase steadily. Reaching USD 4 billion in 2024 and USD 5 billion in 2025.

- The upward trajectory continues with anticipated revenues of USD 6 billion in 2026 and USD 8 billion in 2027.

- Subsequently, the market is expected to grow, with revenues reaching USD 10 billion in 2028 and USD 12 billion in 2029.

- By 2030, the market is forecasted to attain a revenue of USD 15 billion. Followed by further substantial growth to USD 19 billion in 2031 and USD 23 billion in 2032.

- The upward trend persists, culminating in a projected revenue of USD 29 billion by 2033.

- This robust growth trajectory reflects a growing consumer preference for meat substitutes. Driven by health consciousness, environmental concerns, and the expanding availability of innovative plant-based protein products in the global market.

(Source: Market.us)

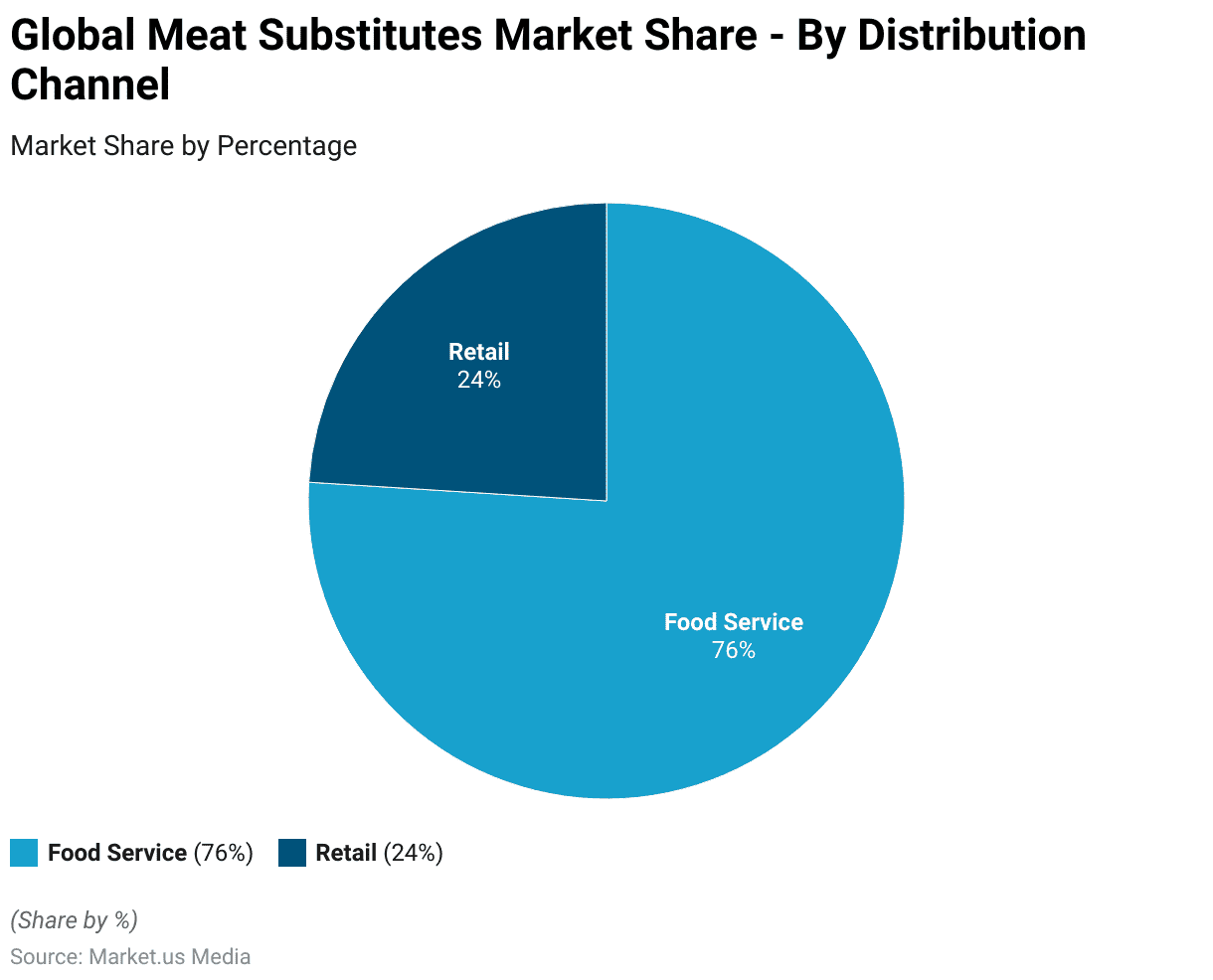

Global Meat Substitutes Market Share – By Distribution Channel Statistics

- In the distribution of meat substitutes, the food service sector dominates with a commanding market share of 76%. While the retail segment holds a notable but comparatively smaller share of 24%.

- This distribution underscores the significant presence of meat substitutes within the food service industry. Which includes restaurants, cafeterias, catering services, and other establishments providing prepared meals to consumers.

- The substantial majority share held by food service channels indicates a strong demand for meat substitutes within the food service sector. Likely driven by changing dietary preferences, and increased awareness of sustainability. The growing availability of plant-based menu options in restaurants and food outlets worldwide.

- Meanwhile, the retail segment, encompasses supermarkets, grocery stores, specialty food stores, and online retailers. Also plays a significant role in providing consumers with access to meat substitute products for home consumption. Albeit with a relatively minor market share compared to the food service sector.

(Source: Market.us)

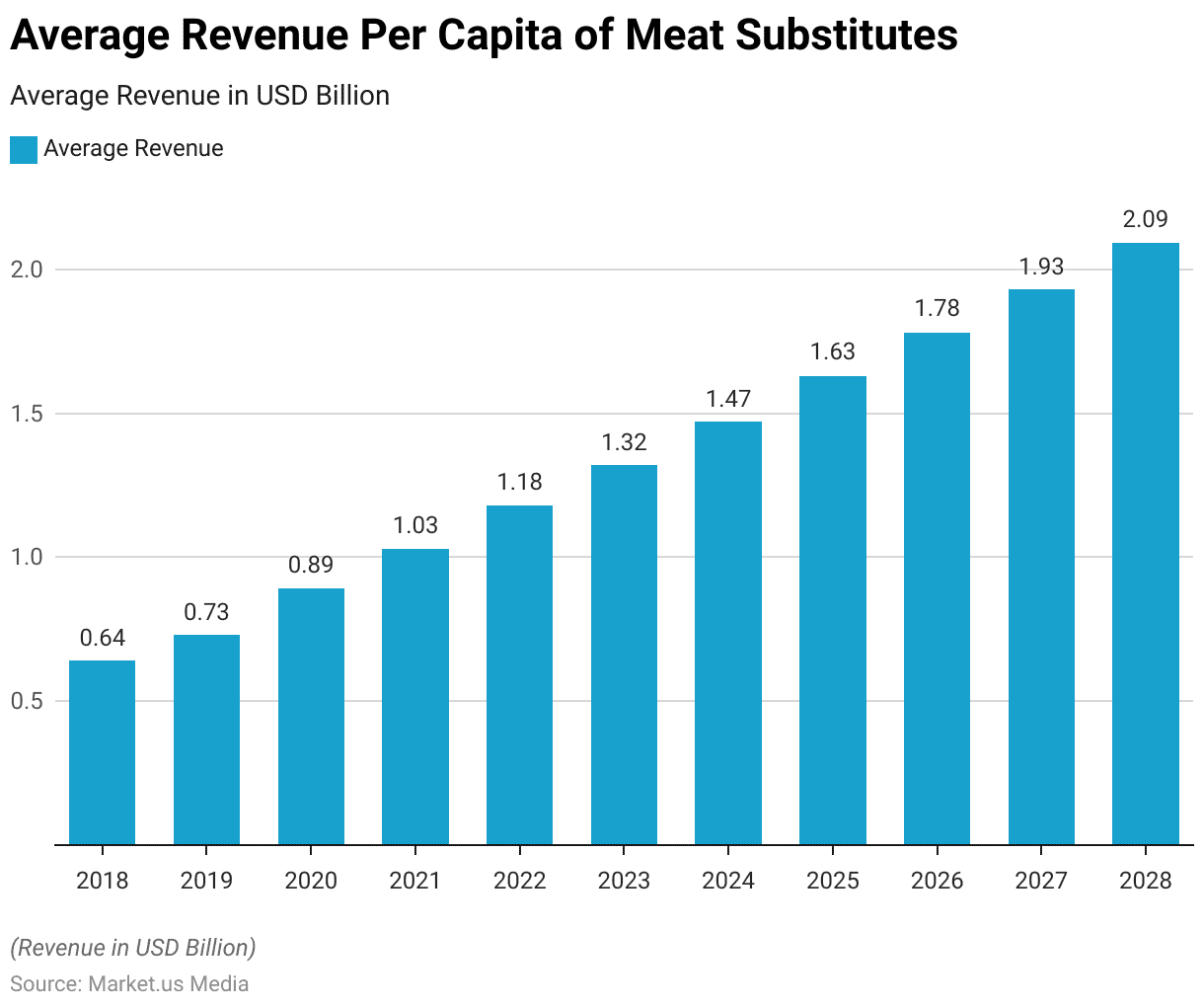

Average Revenue Per Capita

- The average revenue per capita of meat substitutes, denoted in USD, has consistently grown over the specified period.

- Beginning at $0.64 in 2018, the figure increased steadily to $0.73 in 2019 and $0.89 in 2020.

- This upward trend continued, with average revenues reaching $1.03 in 2021 and $1.18 in 2022.

- Subsequently, significant growth is observed. With average revenue per capita rising to $1.32 in 2023, $1.47 in 2024, and $1.63 in 2025.

- This trend persists, with average revenues of $1.78 in 2026, $1.93 in 2027, and $2.09 in 2028.

- The consistent average revenue per capita increase reflects growing consumer acceptance and adoption of meat substitutes. Driven by health awareness, environmental concerns, and a broader range of innovative plant-based protein products.

(Source: Statista)

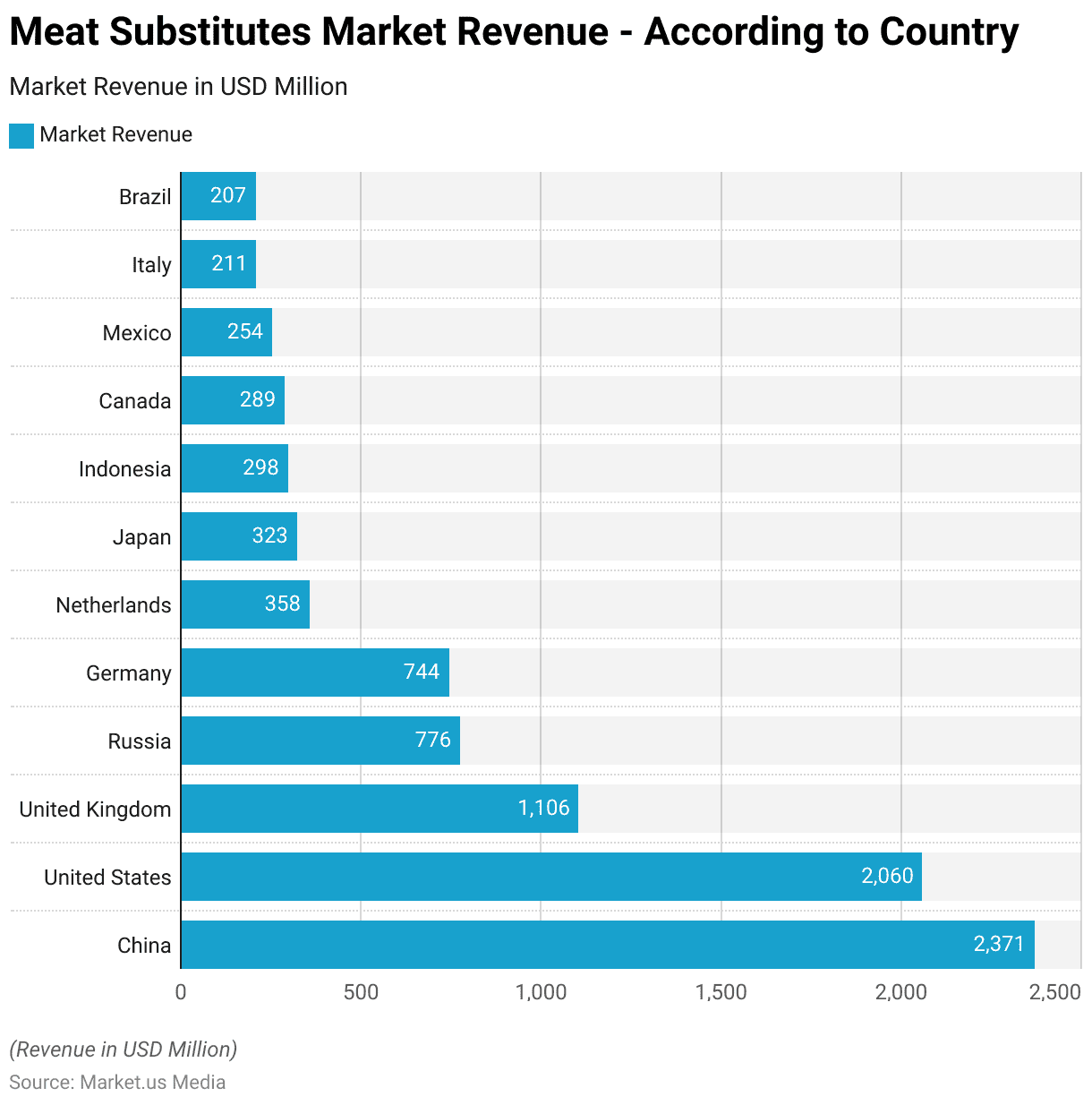

Regional Analysis of the Global Meat Substitutes Market Statistics

- The market for meat substitutes exhibits varying degrees of revenue across different countries, reflecting diverse consumer preferences and market dynamics.

- China leads the global market with a substantial revenue of USD 2.371 billion. Followed closely by the United States at USD 2.06 billion.

- The United Kingdom emerged as another significant market, with revenue totaling USD 1.106 billion.

- Russia and Germany follow with revenues of USD 776 million and USD 744 million. Respectively, this indicates a notable presence of meat substitutes in these European markets.

- The Netherlands and Japan contribute moderately to the global market with revenues of USD 358 million and USD 323 million, respectively.

- Meanwhile, Indonesia, Canada, Mexico, Italy, and Brazil exhibit varying levels of market uptake. With revenues ranging from USD 298 million to USD 207 million.

- This distribution highlights the global appeal of meat substitutes, driven by factors such as dietary preferences, health consciousness, and environmental concerns. The availability of innovative plant-based protein products tailored to diverse consumer markets worldwide.

(Source: Statista)

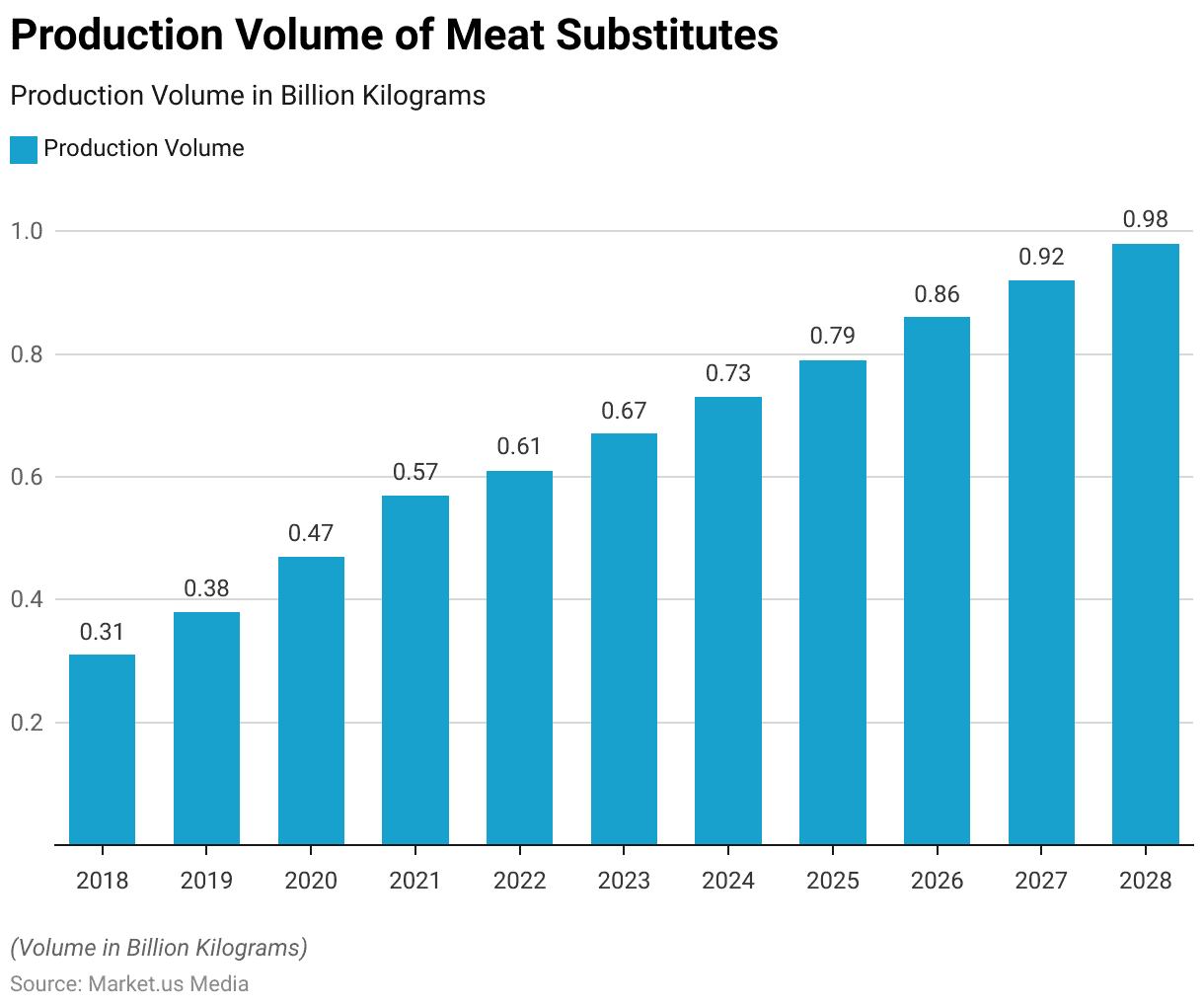

Production Volume of Meat Substitutes Statistics

- The production volume of meat substitutes has shown a consistent upward trend over the years. Reflecting increasing consumer demand and technological advancements in plant-based protein manufacturing.

- Starting at 0.31 billion kilograms in 2018, the production volume has steadily risen yearly. Reaching 0.38 billion kilograms in 2019 and 0.47 billion kilograms in 2020.

- This growth trajectory continued with production volumes of 0.57 billion kilograms in 2021 and 0.61 billion kilograms in 2022.

- Anticipated consumer adoption and market penetration expansion have led to further increases. With production volumes projected to reach 0.67 billion kilograms in 2023 and 0.73 billion kilograms in 2024.

- The trend of growth persists, with forecasted production volumes of 0.79 billion kilograms in 2025, 0.86 billion kilograms in 2026, and 0.92 billion kilograms in 2027.

- By 2028, production is expected to reach 0.98 billion kilograms.

- This upward trajectory underscores the growing popularity and acceptance of meat substitutes as viable alternatives to traditional meat products, driven by health consciousness. The sustainability concerns, and the expanding variety and availability of plant-based protein options in the global market.

(Source: Statista)

Price of Meat Substitutes Statistics

- The price of meat substitutes, denoted in USD, has experienced fluctuations over the observed years.

- Beginning at $15.06 in 2018, the price slightly decreased to $14.16 in 2019 before remaining relatively stable at $14.10 in 2020.

- A slight decline continued in 2021 with a price of $13.77, followed by a modest increase to $14.66 in 2022.

- From 2023 onwards, a gradual uptrend is observed, with prices rising to $15.23 in 2023, $15.64 in 2024, and $16.00 in 2025.

- This trend persists with $16.36 in 2026, $16.72 in 2027, and $17.09 in 2028.

- These fluctuations reflect various factors influencing the market, including changes in production costs, demand-supply dynamics, technological advancements, and consumer preferences.

- Despite these fluctuations, the overall trajectory indicates a gradual increase in the price of meat substitutes over the observed period.

(Source: Statista)

Leading Meat Substitute Brands Ranked by Brand Awareness

- In 2023, MorningStar Farms and Beyond Meat emerged as the leading meat substitute brands in the United States, with 56% and 54% of respondents indicating awareness of these brands, respectively.

- Impossible Foods, Amy’s Kitchen, and Gardein followed closely behind, each with significant brand awareness scores of 49%, 41%, and 41%, respectively.

- Other notable brands in the market included Boca (39%), Garden Gourmet (36%), and Tofurky (33%).

- While these brands commanded considerable consumer recognition, others such as Meatless Farm, Lightlife, and Sweet Earth Natural Food garnered attention, with awareness scores ranging from 30% to 29%.

- Field Roast, Quorn, Loma Linda, Before the Butcher, and Daring rounded out the list, with awareness scores ranging from 27% to 23%.

- This data highlights the competitive landscape within the meat substitute industry and the diverse range of brands vying for consumer attention and loyalty in the United States market.

(Source: Statista)

Demographics of Plant-Based Meat Alternatives

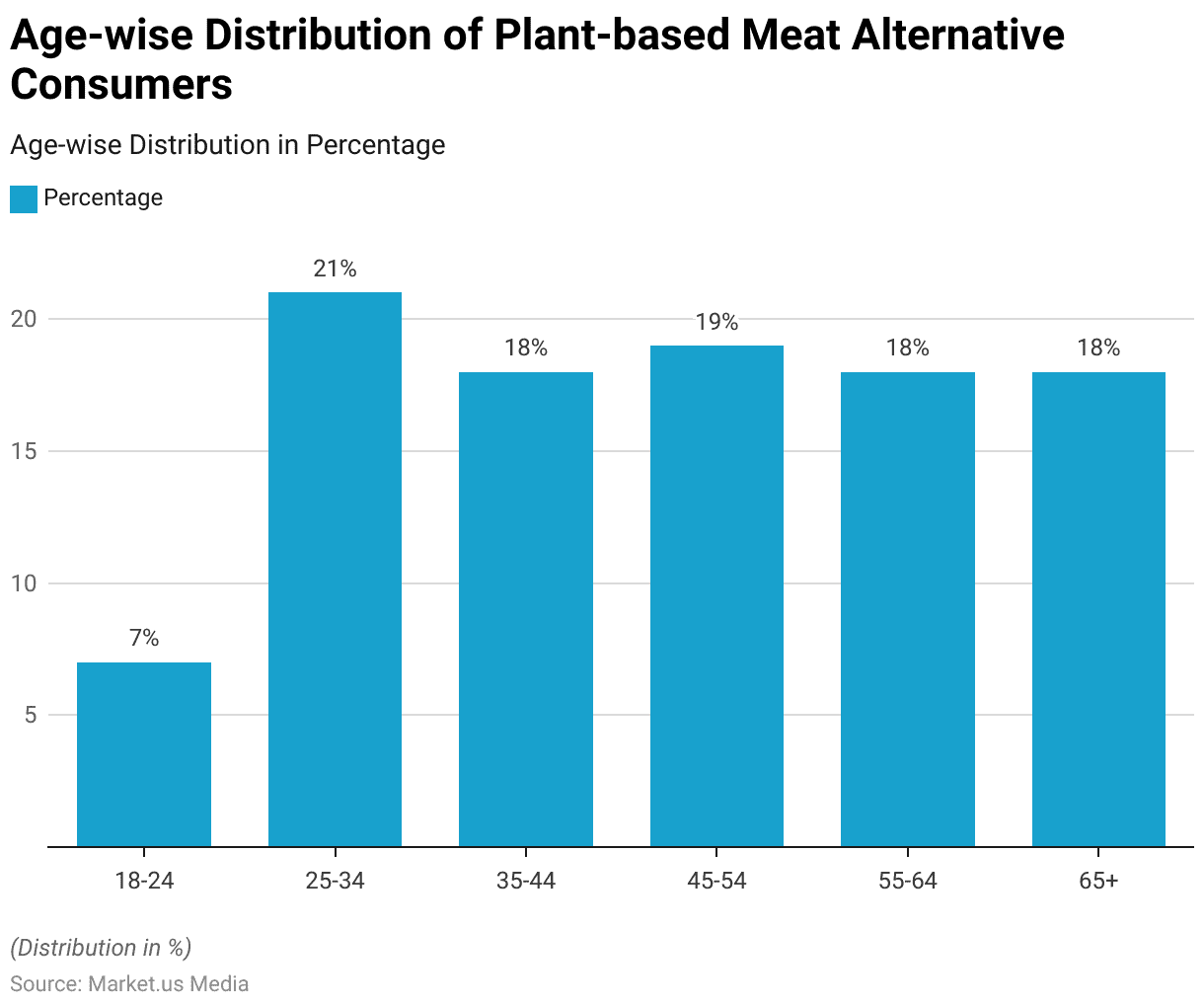

According to Age

- Plant-based meat alternatives appeal to a diverse range of age groups, as evidenced by the distribution of consumption across various demographics.

- In 2023, individuals between the ages of 25 and 34 exhibited the highest level of engagement with plant-based meat alternatives, comprising 21% of consumers.

- Following closely behind were those aged 35 to 44, representing 18% of consumers, and individuals aged 45 to 54 and 55 to 64, each constituting 19% and 18% of the demographic, respectively.

- Furthermore, the age group of 65 and older displayed a notable interest in plant-based meat alternatives, accounting for 18% of consumers.

- Although individuals aged 18 to 24 showed the lowest level of engagement, at 7%, the overall data underscores the widespread appeal of plant-based meat alternatives across different age cohorts, reflecting a growing trend towards healthier and more sustainable dietary choices among consumers of varying ages.

(Source: International Food Information Council)

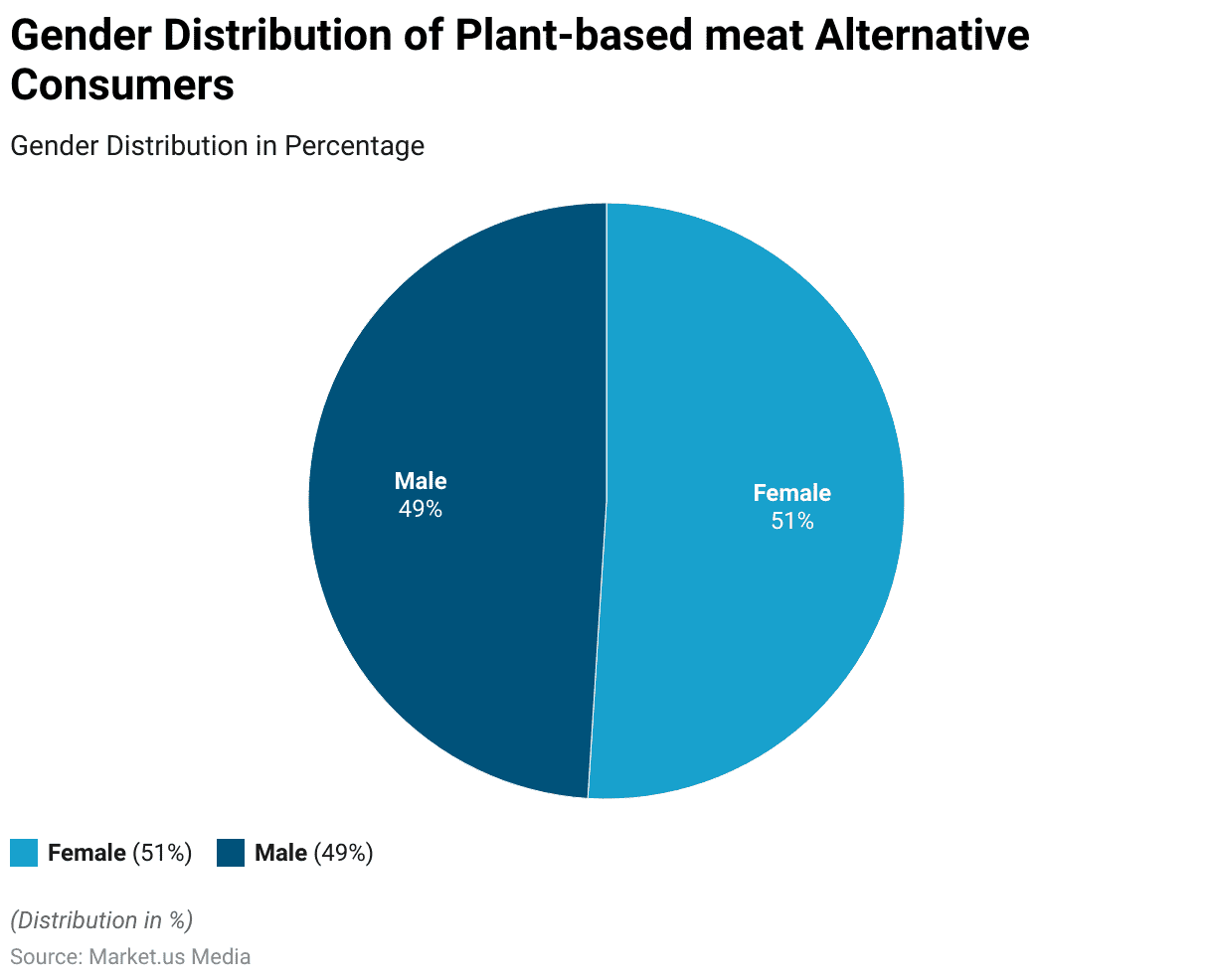

According to Gender

- Plant-based meat alternatives exhibit a balanced distribution across gender demographics, with females and males showing nearly equal levels of engagement.

- In 2023, females accounted for 51% of consumers of plant-based meat alternatives, while males comprised 49%.

- This parity suggests that plant-based meat alternatives resonate equally with both genders. Reflecting a broad appeal and adoption of these products across the population.

- The data underscores plant-based foods’ growing acceptance and integration into diverse dietary preferences and consumption habits, regardless of gender identity.

(Source: International Food Information Council)

According to Education

- Plant-based meat alternatives exhibit varying levels of adoption across different education demographics.

- In 2023, individuals with a high school diploma represented the largest cohort of consumers, constituting 21% of the demographic.

- Close behind were those who had attended some college but did not attain a degree, comprising 20% of consumers.

- Additionally, individuals with an associate’s degree or technical/vocational school background accounted for 13% of consumers.

- Conversely, those with less than a high school education constituted the smallest group, representing only 1% of consumers.

- This data suggests that plant-based meat alternatives are embraced across various educational backgrounds. Individuals with higher levels of education may exhibit slightly higher adoption rates.

(Source: International Food Information Council)

Consumption Pattern of Plant-Based Meat Alternatives

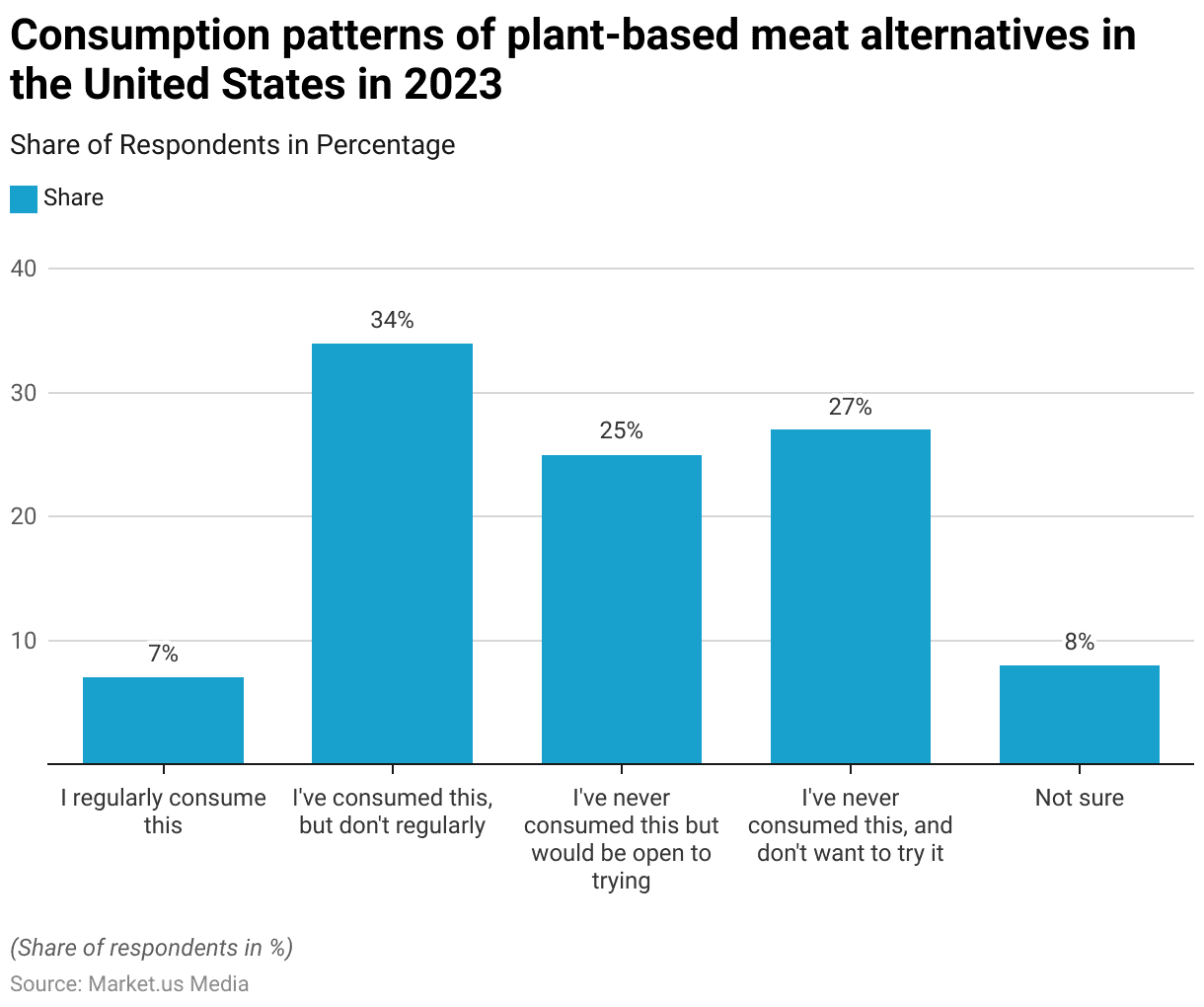

- In the United States in 2023, the consumption patterns of plant-based meat alternatives varied among respondents. Reflecting a spectrum of attitudes and behaviors towards these products.

- A small percentage, 7% of respondents, reported regularly consuming plant-based meat alternatives, indicating a consistent preference for these products.

- A more significant segment, comprising 34% of respondents, reported consuming plant-based meat alternatives in the past but not regularly.

- Additionally, 25% of respondents were open to plant-based meat alternatives despite never consuming them.

- However, a notable portion, 27% of respondents, indicated that they had never consumed plant-based meat alternatives and were not interested in trying them.

- Finally, 8% of respondents were unsure about their stance on plant-based meat alternatives. Highlighting a degree of uncertainty or indecision among some consumers.

- These findings illustrate the diverse range of attitudes and behaviors surrounding the consumption of plant-based meat alternatives in the United States.

(Source: Statista)

Advances in Meat Substitute Production Technologies

- Start-ups Redefine Meat and NovaMeat are pioneering 3D printing technology to craft intricate plant-based meat products, aiming to replicate the texture and appearance of traditional meats like steak and bacon.

- Although widespread adoption of cost-effective 3D printing in the food industry may be some time away, both companies are optimistic about its potential for consumer products.

- On the other hand, Atlast Food Co. and Meati are exploring an alternative method. Utilizing mycelia to produce structured vegan meat analogs.

- Mycelia, the multicellular structures found in mushrooms, offer a sustainable and affordable option for mimicking the fibrous texture of meats like steaks and chicken breasts.

- At last, Food Co. cultivates large mycelial slabs for shaping into products like MyBacon. While Meati focuses on creating vegan “steaks” using mycelial.

- With mycelia cultivation’s low production costs and scalability, this approach could soon revolutionize the creation of realistic meat substitutes.

(Source: PR Newswire)

Challenges Faced by the Meat Substitutes Industry Statistics

- According to survey findings, 40% of participants expressed reluctance to try cultivated meat, while 29% indicated a willingness to do so.

- Further analysis uncovered diverse perspectives on cultivated meats among various demographic segments.

- For instance, most baby boomers, account for 60% of respondents in this age group. Stated their unwillingness to sample cultivated meat, contrasting sharply with only 27% of Gen Z individuals expressing a similar sentiment.

- These findings highlight variations in acceptance levels towards cultivated meat across different age cohorts. Suggesting a generational divide in attitudes towards this emerging food technology.

(Source: FSA Survey)

Recent Development

Acquisitions and Mergers:

- Acquisition of a leading plant-based meat company by a major food conglomerate in September 2023, for an estimated $500 million, expanding their presence in the alternative protein market.

- The merger between two meat substitute startups specializing in innovative protein formulations in December 2023, created a stronger player in the plant-based food industry.

- In 2024, Impossible Foods acquired a plant-based dairy company, Further Farms, to expand its product offerings beyond meat substitutes.

- Kellogg’s subsidiary, MorningStar Farms, collaborated with Disney to launch a new range of plant-based meat substitutes, targeting families and children.

New Product Launches:

- Introduction of next-generation meat analogs with improved texture and flavor by plant-based meat brands in January 2024, resulting in a 30% increase in sales compared to traditional products.

- Launch of plant-based seafood alternatives, such as tuna and shrimp substitutes, by alternative protein companies in March 2024, tapping into the growing demand for sustainable seafood options.

- Nestlé launched its “Incredible Burger” in Europe, expanding its portfolio of plant-based meat substitutes to cater to the growing demand for alternative protein sources.

- Beyond Meat introduced its Beyond Breakfast Sausage Links, tapping into the breakfast segment of the plant-based meat market.

Funding Rounds:

- Series C funding round for a cultured meat startup in February 2024, raising $75 million to scale up production and bring lab-grown meat products to market.

- Seed funding for a novel ingredient company developing plant-based fat mimics for meat substitutes in April 2024, securing $15 million for research and development efforts.

Partnerships and Collaborations:

- Collaboration between a fast-food chain and a plant-based meat supplier in November 2023 to launch a plant-based burger menu nationwide, resulting in a 40% increase in foot traffic.

- The partnership between a meat substitute brand and a celebrity chef in March 2024 to develop signature plant-based recipes and promote sustainable cooking practices.

Investor Interest and Funding Rounds:

- In 2024, Meatless Farm raised $31 million in a funding round led by European investors. Signaling growing investor confidence in the plant-based meat industry.

- Impossible Foods secured $500 million in funding to support its global expansion efforts and further research and development of its plant-based products.

- Venture capital investments in meat substitute startups totaled $4.8 billion in 2023. With a focus on companies developing innovative plant-based and cultured meat technologies.

- Strategic partnerships and acquisitions between food manufacturers, retail chains, and agricultural companies accounted for 65% of total investment activity in the meat substitutes market in 2023. Reflecting industry efforts to capitalize on the growing consumer demand for sustainable and ethical protein alternatives.

Conclusion

Meat Substitutes Statistics – In brief, the meat substitutes industry is witnessing swift expansion driven by evolving consumer demands for healthier and eco-friendly food options.

Offering a range of choices, including plant-based proteins and cultured meat, the sector addresses various dietary requirements and ethical considerations.

Despite obstacles such as flavor and affordability, meat substitutes are gaining global traction, drawing investment and regulatory backing.

Ongoing innovation and growing consumer favorability are forecasted to propel the market’s growth. Positioning meat substitutes as crucial elements of a sustainable food ecosystem.

FAQs

Meat substitutes replicate conventional meat’s taste, texture, and appearance using non-animal ingredients such as plant proteins, fungi, or cultured cells.

Meat substitutes offer several benefits, including reducing environmental impact, promoting animal welfare, and providing healthier dietary options with lower saturated fat and cholesterol levels.

While meat substitutes aim to mimic the taste and texture of conventional meat, they often have different nutritional profiles and may vary in taste and texture. However, they provide a viable alternative for individuals looking to reduce their meat consumption or transition to a plant-based diet.

Common meat substitutes include plant-based burgers, sausages, chicken nuggets, and meatballs made from soy, wheat gluten, pea protein, or mycoprotein.

Meat substitutes generally have a lower environmental footprint than conventional meat production, requiring fewer natural resources and producing fewer greenhouse gas emissions.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)