Table of Contents

Overview

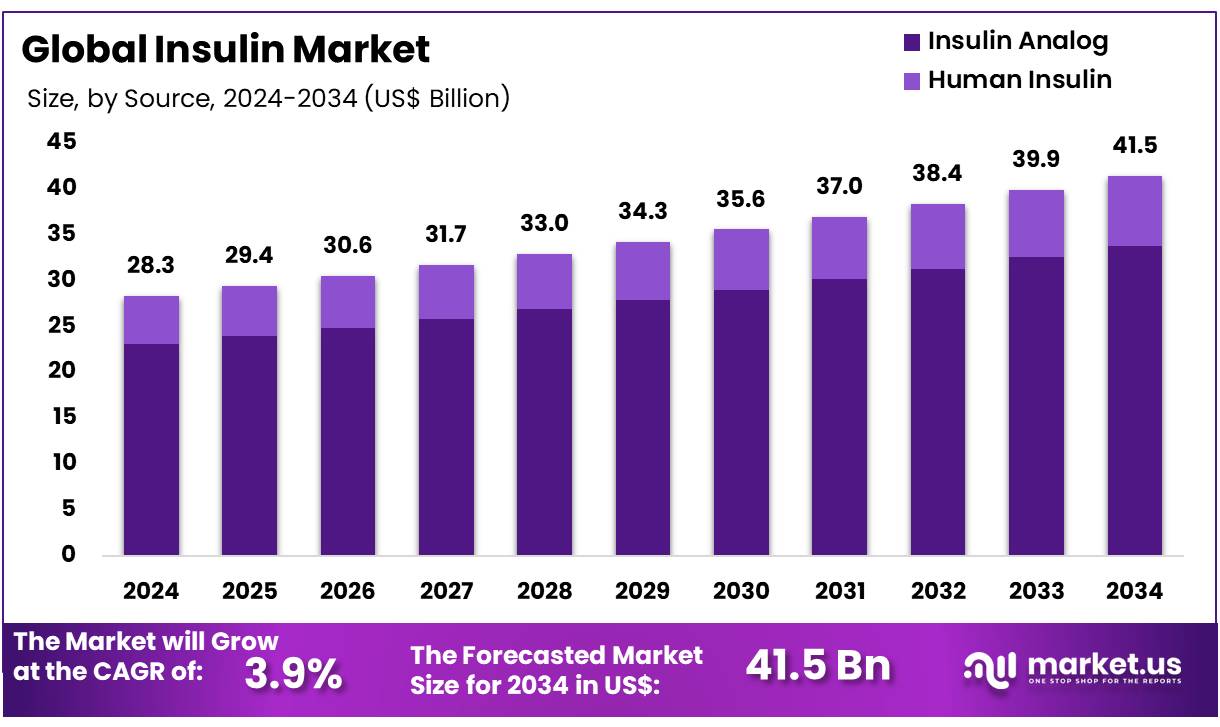

New York, NY – Dec 17, 2025 – Global Insulin Market size is forecasted to be valued at US$ 41.5 Billion by 2034 from US$ 28.3 Billion in 2024, growing at a CAGR of 3.9% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 43.1% share with a revenue of US$ 12.2 Billion.

The field of veterinary infectious disease diagnostics plays a critical role in safeguarding animal health, improving livestock productivity, and supporting public health outcomes. These diagnostic solutions are designed to detect, identify, and monitor infectious pathogens affecting companion animals, livestock, and wildlife with high accuracy and reliability.

Veterinary infectious disease diagnostics include a broad range of technologies such as immunoassays, molecular diagnostics, clinical chemistry, and hematology-based testing. These tools enable early detection of bacterial, viral, parasitic, and fungal infections, allowing timely clinical intervention and effective disease management. The adoption of advanced diagnostic platforms has been supported by rising awareness of zoonotic diseases, increasing pet ownership, and the growing need for food safety and biosecurity across animal production systems.

The demand for rapid and point-of-care diagnostic solutions has been increasing, particularly in veterinary clinics, reference laboratories, and research institutions. Molecular diagnostic techniques, including PCR-based assays, are being widely utilized due to their high sensitivity and specificity. Additionally, continuous investment in research and development has led to the introduction of innovative diagnostic kits and automated systems, enhancing testing efficiency and diagnostic accuracy.

Veterinary infectious disease diagnostics are expected to remain an essential component of global animal healthcare infrastructure. Their role in disease prevention, surveillance, and outbreak control supports sustainable animal health practices and contributes to improved animal welfare standards. As regulatory frameworks and disease monitoring programs continue to evolve, the importance of reliable veterinary diagnostic solutions is anticipated to grow steadily in the coming years.

Key Takeaways

- In 2024, the fertility supplements market generated revenue of US$ 28.3 billion and expanded at a CAGR of 3.9%, with the market projected to reach US$ 41.5 billion by 2034.

- Within the product type segment, long-acting insulin emerged as the leading category, accounting for 47.3% of the total market share in 2024.

- Based on source, insulin analogs represented the dominant revenue contributor, capturing 81.5% of the market share in 2024.

- Type 1 Diabetes Mellitus held the largest share by indication, accounting for 58.2% of the market in 2024.

- By delivery device, insulin pens led the segment, securing a 40.6% share of the global market in 2024.

- Among distribution channels, retail pharmacies dominated the market, representing 77.1% of total sales in 2024.

- Regionally, North America accounted for the highest market share, contributing 43.1% of global revenue in 2024.

Regional Analysis

North America led the global insulin market in 2024, accounting for a substantial 43.1% share of total revenue. The region’s dominance is primarily supported by the high prevalence of diabetes and a well-developed healthcare infrastructure, particularly in the United States. According to the Centers for Disease Control and Prevention (CDC), more than 38 million Americans are living with diabetes, while nearly 98 million have prediabetes. This large patient base has driven consistent demand for insulin therapies across the country.

The strong presence of major insulin manufacturers, including Novo Nordisk, Eli Lilly, and Sanofi, has further strengthened market growth by ensuring product availability and continuous innovation. In addition, widespread adoption of advanced insulin delivery technologies, such as insulin pens, pumps, and continuous glucose monitoring (CGM) systems, has improved treatment adherence and patient outcomes.

Despite these advantages, the U.S. market continues to face challenges related to insulin affordability. Rising insulin prices have raised concerns over accessibility, prompting government interventions such as caps on out-of-pocket costs for Medicare beneficiaries. Recent pricing initiatives by manufacturers are expected to partially ease this burden.

Meanwhile, the Asia Pacific region is projected to register the highest CAGR during the forecast period. Market growth is being driven by the rapidly increasing diabetes population in countries such as China and India, along with urbanization and lifestyle changes. The growing adoption of biosimilar insulins, offering cost-effective treatment options, has significantly expanded access to diabetes care across the region.

Insulin Statistics

- Ultra-rapid-acting insulin is characterized by a very fast onset of action, occurring within 2–15 minutes. Peak activity is observed between 30–60 minutes, with an overall duration of approximately 4 hours. Administration is generally done with the first bite of a meal and is commonly used in combination with long-acting insulin to support basal insulin needs.

- Rapid-acting insulin typically begins to act within 15 minutes, reaches peak effectiveness at around 1 hour, and remains active for 2–4 hours. It is usually administered immediately before meals and is frequently paired with long-acting insulin for comprehensive glycemic control.

- Rapid-acting inhaled insulin demonstrates an onset of action within 10–15 minutes, peaks at approximately 30 minutes, and maintains effectiveness for up to 3 hours. It is generally taken just prior to meals and is used alongside injectable long-acting insulin.

- Regular (short-acting) insulin has an onset of action of about 30 minutes, peaks between 2–3 hours, and has a duration ranging from 3–6 hours. This insulin is typically administered 30–60 minutes before meals to align with postprandial glucose increases.

- Intermediate-acting insulin begins to work within 2–4 hours, reaches peak activity between 4–12 hours, and provides coverage for approximately 12–18 hours. It is commonly administered once or twice daily to address insulin requirements for part of the day or overnight.

- Long-acting insulin starts exerting its effect approximately 2 hours after administration and is designed to provide peak-less, steady insulin release for up to 24 hours. It is usually taken once daily and may be combined with rapid- or short-acting insulin when additional mealtime coverage is required.

- Ultra-long-acting insulin has a delayed onset of around 6 hours, exhibits no pronounced peak, and offers an extended duration of action of 36 hours or longer. It is administered once daily and can be used in combination with faster-acting insulin formulations.

- Premixed insulin formulations show a variable onset ranging from 5–60 minutes, with multiple or variable peaks, and a duration of approximately 10–16 hours. These products are typically administered twice daily, usually 10–30 minutes before breakfast and dinner, to simplify insulin regimens.

Emerging Trends

- Once-Weekly Insulin Formulations: Recent pharmaceutical advancements have enabled the development of long-acting, once-weekly insulin analogs, including insulin icodec and insulin efsitora alfa. These formulations are designed to significantly reduce injection frequency, which is expected to improve patient adherence and long-term glycemic control. Clinical studies indicate that insulin icodec demonstrates a plasma half-life of more than eight days, supporting a stable weekly dosing regimen.

- Smart Insulin Technologies: Progress is being observed in glucose-responsive insulin (GRI) technologies, which are engineered to activate in the presence of elevated blood glucose levels and reduce activity as glucose levels normalize. Compounds such as NNC2215 aim to replicate physiological insulin secretion, thereby minimizing glycemic variability and lowering the risk of hypoglycemia.

- Artificial Pancreas Systems: The adoption of hybrid closed-loop systems, commonly referred to as artificial pancreas technologies, is increasing. These systems integrate continuous glucose monitoring (CGM) with automated insulin delivery to dynamically adjust insulin dosing in real time. The approach has been associated with improved glycemic outcomes, reduced hypoglycemic events, and lower treatment burden for patients.

- Oral Insulin Development: Ongoing research efforts are focused on the development of oral insulin formulations, including insulin tregopil and ORMD-0801. These products aim to offer a non-injectable alternative to traditional insulin therapies, with the potential to enhance patient compliance, convenience, and overall quality of life.

- Cost Reduction Initiatives: Affordability initiatives across the insulin market have resulted in measurable price declines. In the United States, the average price per insulin unit declined by approximately 42%, decreasing from USD 0.33 in 2019 to USD 0.19 by mid-2024, improving patient access and easing financial burden.

Use Cases

- Management of Type 1 Diabetes: Insulin therapy remains the cornerstone of treatment for individuals with type 1 diabetes, as endogenous insulin production is absent or minimal. In the United States, an estimated 304,000 individuals under the age of 20 are living with type 1 diabetes, requiring lifelong and consistent insulin administration.

- Treatment of Type 2 Diabetes: For patients with type 2 diabetes, insulin therapy is typically introduced when lifestyle interventions and oral antidiabetic agents fail to maintain adequate glycemic control. As of 2024, the global adult diabetic population reached approximately 589 million, underscoring the substantial and growing demand for insulin-based therapies.

- Hospital and Emergency Care Applications: Insulin is widely used in inpatient and emergency care settings to manage acute hyperglycemia, including in patients without a prior diagnosis of diabetes. Effective inpatient glycemic management has been associated with reduced complication rates, shorter hospital stays, and improved clinical outcomes.

- Gestational Diabetes Management: In cases of gestational diabetes where blood glucose targets cannot be achieved through dietary measures alone, insulin therapy is commonly prescribed. Insulin is considered safe during pregnancy, as it does not cross the placental barrier, supporting maternal and fetal health.

- Use in Insulin Delivery Devices: Advancements in insulin delivery systems, including insulin pumps and smart insulin pens, have enhanced dosing accuracy and treatment convenience. These devices enable precise insulin administration and improved integration with glucose monitoring technologies, contributing to better overall diabetes management.

Frequently Asked Questions on Insulin

- How does insulin work in the human body?

Insulin facilitates the movement of glucose from the bloodstream into muscle, fat, and liver cells. This process helps reduce blood sugar levels and supports energy storage, particularly after food consumption. - Who requires insulin therapy?

Insulin therapy is required by individuals with type 1 diabetes and some patients with advanced type 2 diabetes. It is prescribed when the body produces insufficient insulin or cannot effectively utilize it. - What are the main types of insulin available?

Insulin is classified into rapid-acting, short-acting, intermediate-acting, long-acting, and ultra-long-acting types. Each type differs in onset, peak time, and duration, allowing tailored treatment for patient-specific glycemic control. - What factors are driving the growth of the insulin market?

Market growth is driven by the rising prevalence of diabetes, increasing geriatric populations, sedentary lifestyles, and improved access to diabetes care. Technological advancements in insulin delivery devices further support market expansion. - Which regions dominate the global insulin market?

North America dominates the insulin market due to high diabetes prevalence, strong healthcare infrastructure, and favorable reimbursement policies. Europe follows closely, while Asia-Pacific is experiencing the fastest growth due to rising awareness and diagnosis rates. - What role do biosimilar insulins play in the market?

Biosimilar insulins are increasing market competition by offering cost-effective alternatives to branded products. Their adoption is expanding due to pricing pressures, patent expirations, and efforts to improve insulin affordability across developing and developed markets.

Conclusion

The global insulin market continues to demonstrate steady and resilient growth, supported by the rising prevalence of diabetes, expanding patient populations, and continuous innovation in insulin formulations and delivery technologies. Market expansion is being reinforced by the dominance of long-acting insulin, widespread adoption of insulin pens, and strong retail pharmacy distribution networks.

North America remains the leading regional market, while Asia Pacific is emerging as the fastest-growing region due to increasing diagnosis rates and access to biosimilars. Ongoing advancements such as once-weekly insulin, smart delivery systems, and affordability initiatives are expected to strengthen long-term market sustainability and patient outcomes.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)