Table of Contents

Overview

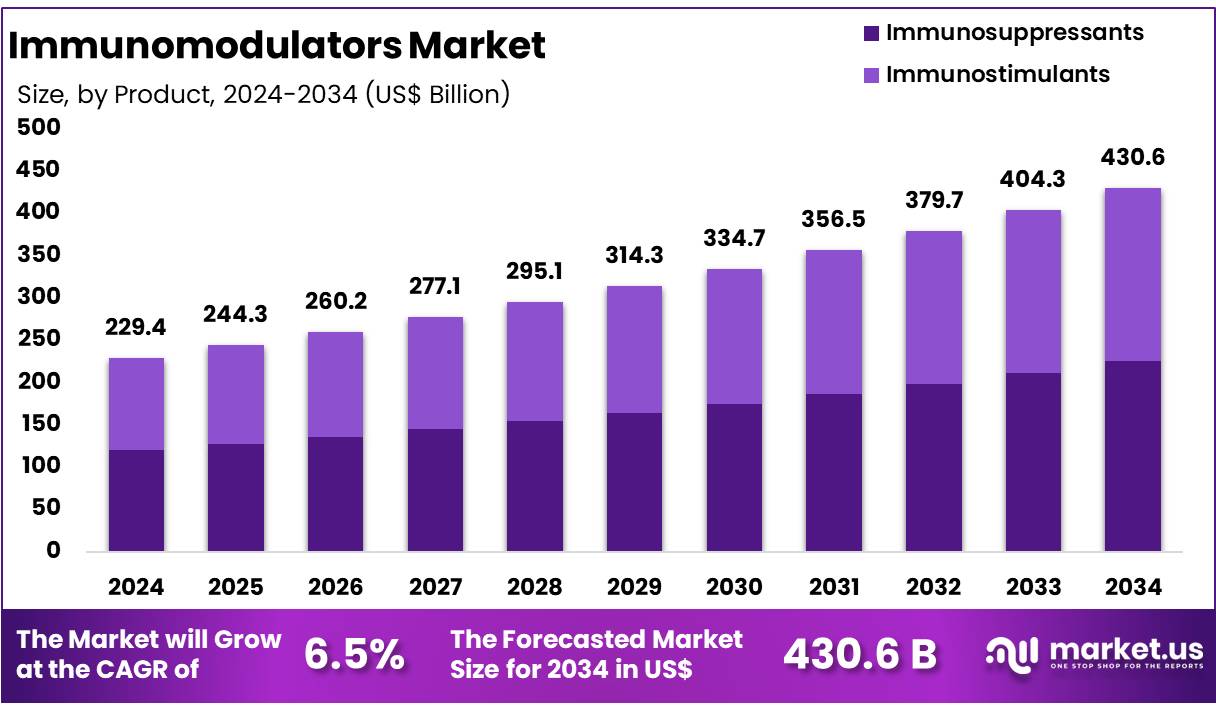

New York, NY – Dec 09, 2025 – Global Immunomodulators Market size is forecasted to be valued at US$ 430.6 Billion by 2034 from US$ 229.4 Billion in 2024, growing at a CAGR of 6.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.0% share with a revenue of US$ 89.5 Billion.

The global demand for immunomodulators has been increasing as healthcare systems prioritize advanced therapeutic solutions capable of regulating immune responses with precision. Immunomodulators are being adopted to support the management of autoimmune disorders, chronic inflammatory conditions, and certain infectious diseases. Their use has also expanded due to heightened emphasis on strengthening immune resilience across diverse patient populations.

The growth of the immunomodulators market has been attributed to rising disease prevalence, continued research investments, and the development of next-generation biologics. Biologic immunomodulators, including monoclonal antibodies and cytokine-based agents, have demonstrated strong efficacy in targeting specific immune pathways. These innovations have been supported by advancements in molecular engineering and clinical trial frameworks, enabling improved treatment outcomes and broader therapeutic applications.

The market has further benefited from increased awareness of immune health following global public health events. A steady rise in product approvals and regulatory support for novel therapies has reinforced investor confidence and accelerated commercial activity. Strategic collaborations between pharmaceutical manufacturers and research organizations continue to strengthen the pipeline of new immunomodulatory compounds.

Future growth is expected to be driven by expanding applications in oncology, personalized medicine, and preventive care. The integration of data-driven diagnostics and biomarker-based treatment selection is anticipated to enhance clinical precision and patient response rates. As the healthcare landscape evolves, immunomodulators are positioned to play a critical role in supporting targeted, safe, and effective immune regulation across global markets.

Key Takeaways

- In 2024, the Immunofluorescence Assay market generated revenue of US$ 229.4 billion, recorded a 6.5% CAGR, and is projected to reach US$ 430.6 billion by 2034.

- The immunosuppressants product segment led the market, accounting for 52.3% share in 2024.

- The oral route of administration held a dominant position with 52.1% share in 2024.

- The cancer application segment generated the highest revenue, contributing 44.7% share in 2024.

- Within the distribution channel, hospital pharmacies represented the largest share at 48.0% in 2024.

- North America dominated the global market, holding 39.0% share in 2024.

Regional Analysis

North America Leading the Immunomodulators Market

North America maintained a leading position in the global immunomodulators market, capturing 39.0% share in 2024. This dominance has been supported by the high prevalence of autoimmune disorders and cancer, which continues to increase the demand for immunomodulatory therapies. Data from the National Institute of Allergy and Infectious Diseases indicates that approximately 8% of the U.S. population is affected by autoimmune diseases.

In addition, the American Cancer Society has projected over 2 million new cancer cases in 2025, with an estimated 618,000 deaths, underscoring the substantial clinical need within the region. The presence of well-established healthcare infrastructure, significant healthcare spending, and advanced research and development capabilities further strengthens the regional market landscape. Nevertheless, the high cost associated with immunomodulatory therapies continues to pose access challenges for certain patient groups.

Asia Pacific Expected to Record the Highest CAGR

Asia Pacific has been projected to register the fastest growth in the immunomodulators market during 2025–2034. The expansion of the market can be attributed to the increasing incidence of autoimmune diseases and cancers, growing healthcare awareness, and government-led initiatives aimed at improving healthcare accessibility. GLOBOCAN estimates that cancer cases in India may rise to 2.08 million by 2040, reflecting a 57.5% increase from 2020. Countries such as India and China are making substantial investments in biotechnology and pharmaceutical research to strengthen domestic manufacturing capabilities and reduce reliance on imports.

A notable example includes the January 2025 approval by China’s NMPA of Sarclisa, an anti-CD38 monoclonal antibody, for use with pomalidomide and dexamethasone in treating multiple myeloma after prior therapy. Despite these developments, regulatory complexities, cost constraints, and infrastructure gaps continue to influence the equitable availability of immunomodulatory treatments across the region.

Emerging Trends

- Rising Approvals of Novel Therapies: The approval rate for advanced immunomodulatory therapies has continued to increase. In 2025, CARVYKTI received FDA approval for multiple myeloma, building on earlier regulatory actions from 2022 and 2023. In addition, linvoseltamab-gcpt (Lynozyfic) obtained accelerated approval on July 2, 2025, for relapsed or refractory multiple myeloma. These developments illustrate sustained innovation across CAR-T and bispecific antibody platforms.

- Expansion of Biosimilar Competition: The market has experienced a notable rise in biosimilar availability, resulting in significant reductions in the cost of immunomodulatory biologics. Pricing data indicate average decreases ranging from 21% to nearly 60%, increasing affordability for healthcare systems and improving patient access.

- Growing Use of Dietary and Vaccine Adjuvants: Immunomodulation is extending beyond prescription medicines into vaccine and nutritional applications. Vaccine adjuvants have been widely used for decades to enhance immune response, as reported by the CDC. Concurrently, the WHO has highlighted increasing interest in naturally occurring immunomodulatory compounds in foods that may support chronic disease management.

- Advances in Personalized Immune Profiling: Greater emphasis is being placed on individualized immunomodulatory strategies. The Immune Epitope Database supported by NIAID now contains over 2.2 million cataloged epitopes, providing a robust foundation for designing therapies that target specific immune pathways. This knowledge base is expected to accelerate personalized treatment development.

Use Cases

- Autoimmune Disease Management: Immunomodulators are extensively applied in the treatment of autoimmune disorders. NIAID data indicate that approximately 8% of the U.S. population—around 26 million people—live with autoimmune conditions. These therapies are used to stabilize dysregulated immune responses and improve patient outcomes.

- Protection of Immunocompromised Patients: CDC data from 2022 show that immunocompromised individuals represented 12.2% of hospitalized COVID-19 cases. Immunomodulatory agents such as monoclonal antibodies, including Pemgarda™, have been authorized to provide added protection, helping to reduce severe disease and hospitalization risk.

- Specialized Vaccination Approaches: An estimated 2.7% of U.S. adults, or roughly 7 million individuals, are considered immunocompromised. Updated COVID-19 vaccination protocols and additional doses are recommended for this group, demonstrating how immunomodulatory strategies are customized to meet the needs of at-risk populations.

- Travel Medicine for High-Risk Travelers: Immunocompromised travelers account for approximately 6% of the U.S. population and represent 1–2% of patients in travel medicine clinics. Immunomodulatory guidance including modified vaccine schedules and prophylactic measures is applied to mitigate risks from vector-borne diseases during travel.

Frequently Asked Questions on Immunomodulators

- How do immunomodulators work?

Immunomodulators function by targeting specific pathways within the immune system to alter immune cell signaling. This controlled modification supports improved disease management by preventing abnormal immune responses or strengthening immune activity when required. - What conditions are treated with immunomodulators?

Immunomodulators are commonly used for autoimmune disorders such as rheumatoid arthritis, psoriasis, and multiple sclerosis. They are also indicated for chronic inflammatory diseases, organ transplant management, and several cancer therapies requiring immune regulation. - What are the major types of immunomodulators?

The major categories include immunosuppressants, immunostimulants, and biologic agents like monoclonal antibodies. Each category operates through different mechanisms to either dampen excessive immune reactions or boost weakened immune responses. - What are the risks or side effects of immunomodulators?

Immunomodulators may cause side effects such as increased infection risk, fatigue, gastrointestinal discomfort, and organ-related complications. Continuous monitoring by healthcare professionals is essential to ensure safe and effective long-term therapy. - Which segment dominates the immunomodulators market?

The immunosuppressants segment currently dominates the due to widespread use in autoimmune disorders and transplant management. Their proven clinical effectiveness and extensive adoption across healthcare systems contribute to their strong market presence. - Which region leads the global immunomodulators market?

North America holds the leading position owing to high disease burden, advanced healthcare infrastructure, strong R&D capabilities, and significant healthcare spending. The region consistently supports rapid adoption of innovative immunomodulatory therapies. - What future opportunities exist in the immunomodulators market?

Emerging opportunities include personalized immunotherapies, expanding biologics development, and broader applications in oncology. Growth is also supported by technological advancements in diagnostics and increasing government initiatives for improved healthcare access.

Conclusion

The global immunomodulators market is positioned for sustained expansion as rising disease prevalence, advancements in biologic therapies, and increasing regulatory support continue to strengthen commercial growth. Market performance has been reinforced by innovation in monoclonal antibodies, CAR-T platforms, and biosimilars, while growing emphasis on personalized immune profiling enhances therapeutic precision.

North America maintains a dominant share due to established healthcare infrastructure, whereas Asia Pacific is expected to achieve the fastest growth driven by improving access and rising research investments. Overall, the market is expected to advance steadily as immunomodulators become integral to targeted and effective immune management.