Table of Contents

Overview

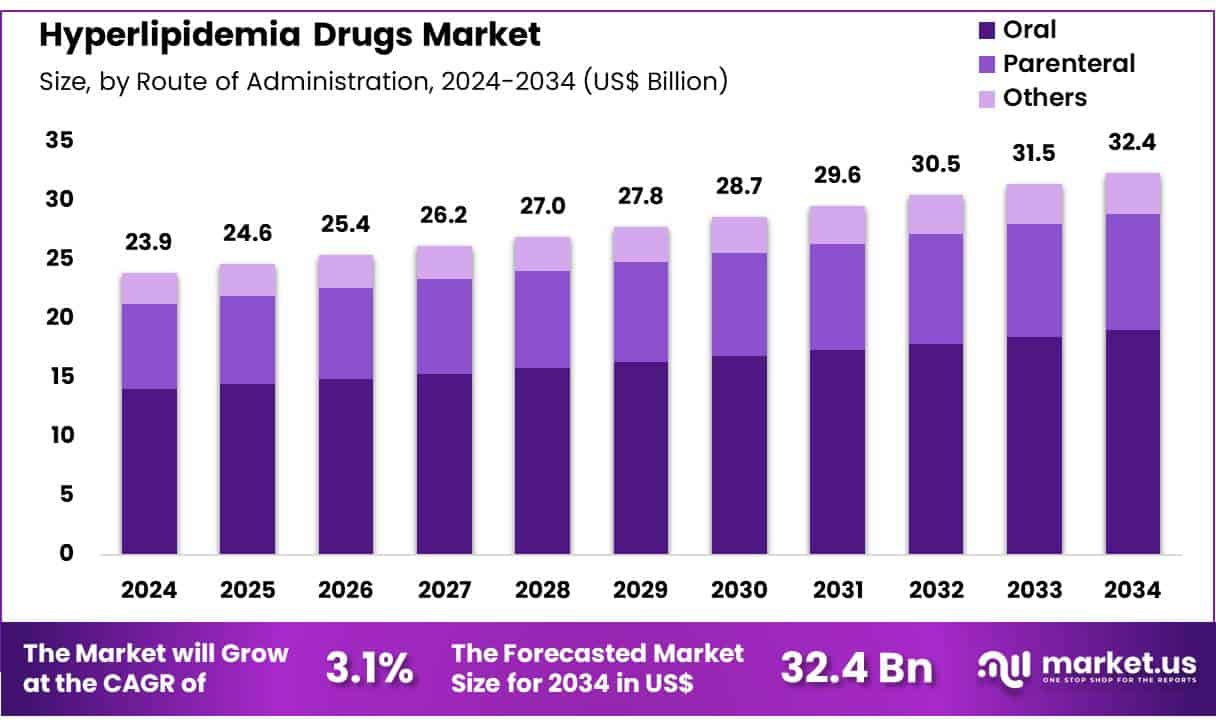

New York, NY – July 01, 2025 – Global Hyperlipidemia Drugs Market size is expected to be worth around US$ 32.4 Billion by 2034 from US$ 23.9 Billion in 2024, growing at a CAGR of 3.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.8% share with a revenue of US$ 9.5 Billion.

The global hyperlipidemia drugs market is experiencing steady expansion, driven by the increasing prevalence of lipid disorders and associated cardiovascular diseases. Hyperlipidemia, characterized by elevated levels of lipids in the blood, significantly increases the risk of coronary artery disease, stroke, and atherosclerosis. As a result, the demand for lipid-lowering therapies including statins, bile acid sequestrants, cholesterol absorption inhibitors, PCSK9 inhibitors, and fibrates has witnessed consistent growth.

The growing geriatric population, sedentary lifestyles, and dietary changes have led to a rise in hyperlipidemia cases globally. The World Health Organization (WHO) estimates that cardiovascular diseases are the leading cause of death worldwide, responsible for nearly 17.9 million deaths annually, with hyperlipidemia being a key modifiable risk factor.

Advancements in drug formulation, especially the development of biologics such as PCSK9 inhibitors and bempedoic acid, are contributing to improved patient outcomes and expanded therapeutic options. Additionally, the adoption of combination therapies is gaining momentum, particularly in high-risk populations.

North America holds a significant share of the global market due to high diagnosis rates and advanced healthcare infrastructure, while Asia-Pacific is emerging as a key growth region driven by increased screening efforts and public health initiatives. The market is poised for further growth as regulatory bodies emphasize preventive care, and pharmaceutical pipelines continue to focus on novel lipid-modifying agents.

Key Takeaways

- In 2024, the global hyperlipidemia drugs market generated a revenue of approximately US$ 23.9 billion and is projected to reach US$ 32.4 billion by 2034, expanding at a compound annual growth rate (CAGR) of 3.1% during the forecast period.

- By drug class, statins emerged as the leading segment in 2023, accounting for 48.2% of the total market share, followed by PCSK9 inhibitors, fibric acid derivatives, combination drugs, cholesterol absorption inhibitors, bile acid sequestrants, and others.

- In terms of route of administration, the oral segment dominated the market, contributing to 58.7% of total revenue, due to ease of administration and strong patient adherence.

- Regarding distribution channels, retail pharmacies held the largest share at 55.3%, reflecting widespread accessibility and consumer preference for point-of-sale purchases.

- Regionally, North America led the global market in 2023 with a 39.8% share, supported by advanced healthcare infrastructure, high diagnosis rates, and the presence of key pharmaceutical manufacturers.

Segmentation Analysis

- Drug Class Analysis: The statins segment, holding 48.2% market share, dominates due to their strong efficacy in lowering LDL cholesterol and preventing cardiovascular events. Statins remain the first-line therapy for hyperlipidemia, especially among aging populations. Their demand is further supported by increasing awareness of cholesterol control. Continued development of advanced formulations with reduced side effects and improved patient compliance is expected to sustain growth within this segment during the forecast period.

- Route of Administration Analysis: Oral formulations accounted for 58.7% of the market, reflecting strong patient preference for convenient, non-invasive therapies. These medications support higher adherence rates and eliminate the need for clinical administration. Growth is driven by innovations in drug bioavailability and tolerability, making oral routes the standard for chronic lipid-lowering therapy. As demand rises for home-based and long-term treatment options, oral hyperlipidemia drugs are expected to maintain their dominant position in the global market.

- Distribution Channel Analysis: Retail pharmacies led the distribution segment with 55.3% revenue share, owing to widespread accessibility and patient convenience. These outlets provide quick access to both prescription and over-the-counter hyperlipidemia drugs. Growth is fueled by expanding pharmacy chains, digital prescription systems, and increased patient autonomy in disease management. As local pharmacies offer reduced wait times and high availability, they are poised to remain a key channel for lipid-lowering drug distribution globally.

Market Segments

By Drug Class

- Statins

- PCSK9 Inhibitors

- Fibric Acid Derivatives

- Combination

- Cholesterol Absorption Inhibitors

- Bile Acid Sequestrants

- Others

By Route of Administration

- Oral

- Parenteral

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Regional Analysis

North America Leads the Hyperlipidemia Drugs Market

North America accounted for the largest share of the global hyperlipidemia drugs market, contributing 39.8% of total revenue. This dominance is driven by the high prevalence of elevated cholesterol levels and structured cardiovascular risk management strategies.

According to the CDC, between August 2021 and August 2023, 11.3% of U.S. adults aged 20 and above had high total cholesterol. The U.S. FDA’s continued approval of novel lipid-lowering therapies and expanded indications further strengthens treatment accessibility and supports sustained market growth across the region.

Asia Pacific to Exhibit Fastest Growth Rate

The Asia Pacific region is projected to witness the highest compound annual growth rate (CAGR) during the forecast period, driven by increasing incidences of lifestyle-related disorders and an expanding elderly population. National studies, such as those conducted in China in 2023, report rising cases of dyslipidemia.

Furthermore, growing healthcare investments across the region support enhanced access to lipid-lowering therapies. The World Bank reported that health spending in East Asia and the Pacific reached 5.43% of GDP in 2022, signaling a supportive environment for improved hyperlipidemia management and pharmaceutical uptake.

Emerging Trends

The expansion of lipid-lowering options can be attributed to the approval of PCSK9 inhibitors and novel RNA-based therapies. PCSK9 inhibitors have been shown to lower LDL-C by 45% to 60% and to confer cardiovascular benefits, supporting their increasing adoption beyond high-intensity statins. Inclisiran, a small interfering RNA targeting PCSK9, is administered only twice yearly yet delivers sustained LDL-C reductions comparable to monoclonal antibodies.

In parallel, bempedoic acid has emerged as an adjunctive therapy, producing an 18% to 19% decrease in LDL-C when added to maximally tolerated statins. Finally, combination regimens such as statin plus ezetimibe are increasingly prescribed, with ezetimibe providing an additional 12% to 20% LDL-C reduction depending on use as monotherapy or add-on.

Use Cases

Lipid-lowering drugs are routinely employed for both primary and secondary prevention of cardiovascular events. Under current U.S. guidelines, an estimated 96.2 million adults are identified for statin therapy; this includes 22.5 million for secondary atherosclerotic cardiovascular disease prevention, 4.8 million with severe hypercholesterolemia, and 20.3 million adults aged 40–75 years with diabetes.

In familial hypercholesterolemia, evolocumab demonstrated a 38.3% greater mean reduction in LDL-C versus placebo at week 24 in a trial of 153 pediatric subjects aged 10 years and older. For homozygous familial cases, evinacumab (EVKEEZA) was evaluated in 65 participants across 12 countries, illustrating targeted use in rare, severe lipid disorders.

Conclusion

The global hyperlipidemia drugs market is positioned for sustained growth, driven by rising cardiovascular disease prevalence, therapeutic innovation, and increased public health focus on lipid management. Statins continue to lead, while novel therapies like PCSK9 inhibitors and RNA-based agents are expanding treatment scope.

North America remains dominant due to advanced healthcare access, while Asia Pacific shows high potential for accelerated growth. Widespread adoption across primary and secondary prevention settings, including rare genetic disorders, underscores the market’s clinical importance. Continued regulatory support and investment in lipid-lowering research are expected to further reinforce market expansion in the coming decade.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)