Table of Contents

Overview

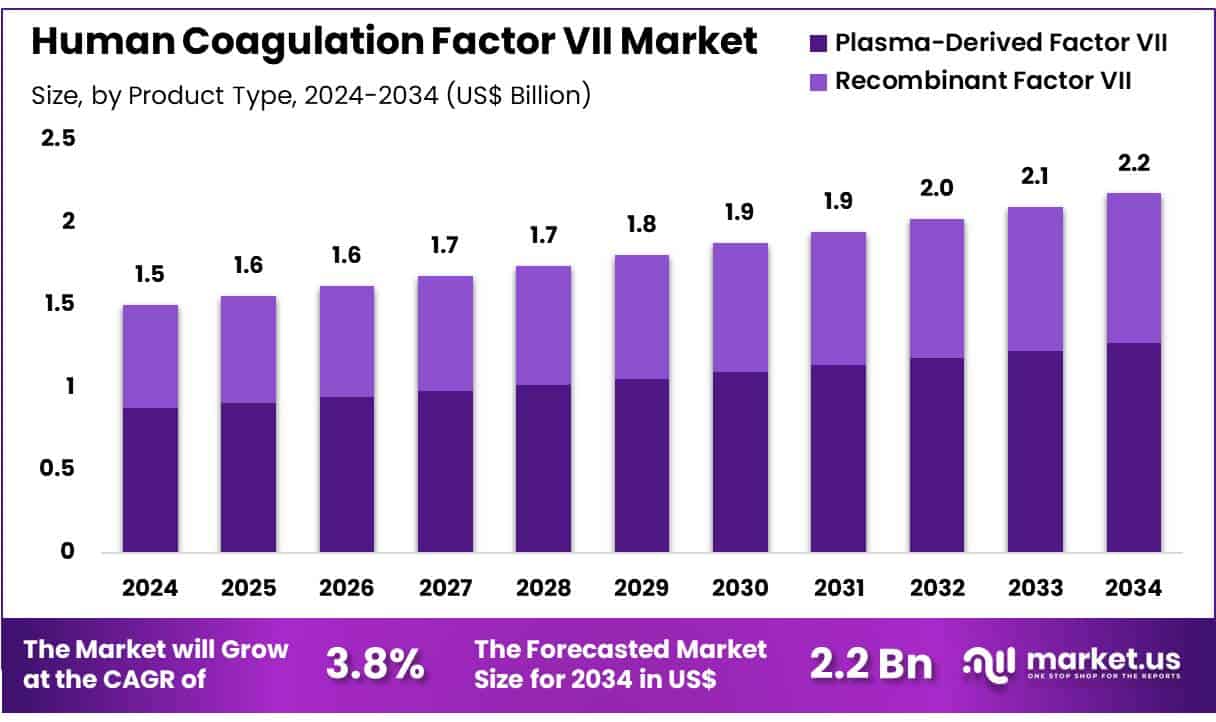

New York, NY – July 11, 2025 – Global Human Coagulation Factor VII Market size is expected to be worth around US$ 2.2 Billion by 2034 from US$ 1.5 Billion in 2024, growing at a CAGR of 3.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.2% share with a revenue of US$ 0.6 Billion.

Human Coagulation Factor VII (FVII) plays a critical role in the initiation of blood coagulation. It is a vitamin K-dependent glycoprotein produced in the liver and circulates in the bloodstream in its inactive form. Upon vascular injury, FVII binds with tissue factor (TF) exposed at the site of damage, forming a TF-FVIIa complex. This complex activates downstream clotting factors, notably Factor IX and Factor X, which are essential in generating thrombin and forming a stable fibrin clot.

Recombinant human coagulation factor VIIa (rFVIIa) has been developed as a therapeutic product for treating and preventing bleeding episodes, especially in patients with hemophilia A or B who have developed inhibitors to conventional factor replacement therapies. It is also used in patients with acquired hemophilia and certain congenital bleeding disorders.

With its fast-acting hemostatic effect, FVIIa is particularly valued during surgeries and trauma cases where rapid clot formation is essential. Recombinant formulations have demonstrated favorable safety profiles, high purity, and consistent potency. Global health authorities, including the FDA and EMA, have approved rFVIIa for specific indications.

Ongoing research continues to evaluate novel formulations and extended half-life versions to improve dosing convenience and clinical outcomes. The growing demand for effective bleeding control solutions continues to support market expansion for human coagulation factor VII products.

Key Takeaways

- In 2024, the global human coagulation factor VII market generated a revenue of approximately USD 1.5 billion and is projected to reach USD 2.2 billion by 2034, expanding at a compound annual growth rate (CAGR) of 3.8% during the forecast period.

- By product type, the market is categorized into plasma-derived factor VII and recombinant factor VII. Plasma-derived factor VII emerged as the leading segment in 2023, accounting for 58.3% of the total market share.

- Based on application, the market is segmented into hemophilia and surgery. The hemophilia segment held the dominant position, contributing 66.2% to the overall revenue in 2023, driven by increasing prevalence and ongoing treatment needs.

- In terms of end users, the market is distributed across hospitals, specialty clinics, and ambulatory surgery centers. Hospitals remained the primary end-user segment, holding a significant revenue share of 69.5%, owing to the centralized management of bleeding disorders and access to specialized care.

- Regionally, North America led the global market in 2023, capturing a 38.2% share. This leadership can be attributed to the presence of advanced healthcare infrastructure, strong regulatory support, and widespread availability of both plasma-derived and recombinant factor VII therapies.

Segmentation Analysis

- Product Type Analysis: Plasma-derived factor VII dominated the market with a 58.3% share in 2023. This segment continues to grow due to its established clinical efficacy and widespread use in treating hemophilia. Its proven safety profile, combined with increasing diagnoses of clotting disorders, supports rising demand. Regulatory approvals and its use alongside other coagulation factors further strengthen its position. As plasma-derived therapies remain the treatment standard, this segment is expected to witness sustained growth throughout the forecast period.

- Application Analysis: Hemophilia accounted for 66.2% of the total market share, making it the leading application segment. Rising global prevalence, especially in emerging regions, is driving demand for factor VII products. Advances in treatment, including gene therapies and long-acting formulations, are improving care outcomes. Increased awareness and early diagnosis contribute to higher therapy adoption. Hemophilia A and B patients, particularly those with severe conditions, will continue to rely on factor VII, supporting this segment’s continued dominance.

- End-User Analysis: Hospitals led the market with a 69.5% share, owing to their central role in managing complex coagulation therapies. As primary centers for administering both plasma-derived and recombinant factor VII, hospitals benefit from specialized staff and advanced infrastructure. Increasing clotting disorder cases in emergency and surgical care further drive demand. The expansion of hematology and surgical units globally ensures that hospitals remain key distribution and treatment points for human coagulation factor VII products.

Market Segments

By Product Type

- Plasma-Derived Factor VII

- Recombinant Factor VII

By Application

- Hemophilia

- Surgery

By End-User

- Hospitals

- Specialty Clinics

- Ambulatory Surgery Centers

Regional Analysis

North America led the human coagulation factor VII market with a 38.2% revenue share in 2023, driven by the high demand for effective hemostatic agents in patients with bleeding disorders, including hemophilia A or B with inhibitors and congenital Factor VII deficiency. According to the CDC, approximately 30,000 to 33,000 males in the U.S. were living with hemophilia between 2012 and 2018, representing a stable patient base.

The availability of recombinant Factor VIIa (rFVIIa), such as NovoSeven and SEVENFACT, has significantly improved treatment outcomes and quality of life for patients requiring bypass agents. The FDA continues to approve therapies supporting advanced care in rare bleeding disorders, further strengthening market performance. Novo Nordisk reported a 31% increase in net sales in 2023, reflecting strong demand within its Rare Disease segment.

The Asia Pacific region is projected to register the fastest CAGR during the forecast period. Growth is supported by rising awareness of bleeding disorders, improved healthcare access, and regional policy enhancements. Countries such as China and Japan have introduced updated treatment guidelines and financial support mechanisms for rare diseases. Pharmaceutical companies, including Novo Nordisk, are expanding outreach, diagnostics, and therapy accessibility, which is expected to drive significant market expansion across the Asia Pacific region.

Emerging Trends

- The approval of a second recombinant Factor VIIa product has expanded therapeutic options. In April 2020, the U.S. Food and Drug Administration approved eptacog beta (SEVENFACT), the first new bypassing agent in over two decades. This molecule has been shown to bind the endothelial protein C receptor (EPCR) with 25–30% greater affinity than the earlier product, potentially enhancing its ability to promote clot formation at bleeding sites.

- Off-label applications of rFVIIa continue to be explored in acute bleeding scenarios. In acute intracerebral hemorrhage, administration of rFVIIa within four hours of symptom onset was demonstrated to limit hematoma growth and reduce mortality in a pivotal trial, supporting further investigation in stroke settings. Ongoing studies, such as the FASTEST trial (NCT03496883), aim to enroll hundreds of participants globally to confirm these findings.

- Very-low-dose use in surgical settings has been associated with reduced blood product needs and shorter hospital stays. A matched cohort study of 362 cardiac surgery patients found that those receiving a median dose of 13 µg/kg very-low-dose rFVIIa required a median of 3 units of red blood cells versus 4 units in controls, and experienced a 1-day shorter median hospital stay without an increase in adverse thrombotic events.

- Interest in biosimilar and next-generation formulations is growing. Although the AryoSeven biosimilar of rFVIIa has been introduced, its clinical uptake remains limited. Research into long-acting or targeted delivery systems is underway, with the goal of reducing dosing frequency and improving safety profiles in bleeding disorders.

Use Cases

- Treatment of Hemophilia A and B with Inhibitors: rFVIIa is the standard bypassing agent for people with hemophilia A or B who have developed inhibitors to conventional factor replacement. In the United States, an estimated 30,000–33,000 males live with hemophilia, and up to 40% of these have the severe form requiring intensive management. Typical dosing of rFVIIa is 90 µg/kg every 2–3 hours until hemostasis is achieved.

- Management of Acquired Hemophilia: In acquired hemophilia often affecting middle-aged or elderly individuals autoantibodies neutralize native clotting factors. rFVIIa has been used successfully to control bleeding, with registry data indicating that over 85% of acute bleeding episodes are resolved after one or two doses, supporting its role as a first-line agent in this rare but serious condition.

- Control of Surgical and Trauma-Related Bleeding: Beyond congenital indications, rFVIIa has been used off-label in critical care. In trauma and major surgical settings, early administration has been linked to lower transfusion requirements. For instance, in cardiac surgery patients receiving very-low-dose rFVIIa (median 13 µg/kg), red blood cell transfusions were reduced by 25%, illustrating its utility in perioperative hemostasis.

- Investigation in Acute Intracerebral Hemorrhage: Clinical trials are evaluating rFVIIa for reducing hematoma expansion in stroke. In a landmark study, patients treated within four hours of bleed onset showed a significant reduction in hematoma growth and a trend toward lower mortality, prompting larger global trials to define its role in acute neurovascular care.

Conclusion

The global human coagulation factor VII market is poised for steady growth, driven by its critical role in managing hemophilia, surgical bleeding, and rare coagulation disorders. The rising prevalence of hemophilia, regulatory approvals of recombinant therapies, and advancements in clinical research continue to enhance treatment outcomes and expand therapeutic indications.

North America dominates due to robust infrastructure and established demand, while Asia Pacific is set to grow rapidly with improving healthcare access. Continued innovation in next-generation formulations and expanding off-label use cases are expected to further strengthen the market landscape and address significant unmet medical needs globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)