Table of Contents

Overview

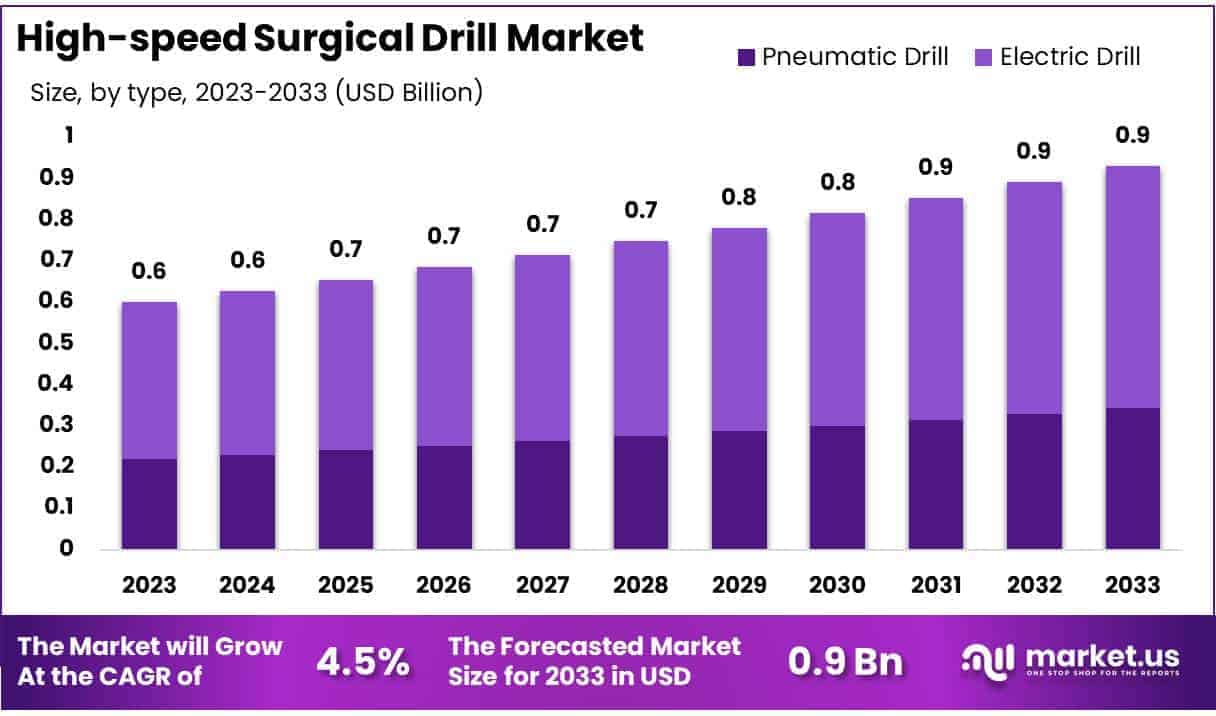

New York, NY – May 09, 2025 – Global High-speed Surgical Drill Market size is expected to be worth around USD 0.9 billion by 2033 from USD 0.6 billion in 2023, growing at a CAGR of 4.5% during the forecast period 2024 to 2033.

High-speed surgical drills are precision-engineered medical devices used to cut, shape, or remove bone and hard tissues during complex surgical procedures. These drills operate at rotational speeds ranging from 60,000 to over 100,000 RPM, enabling surgeons to perform delicate operations with enhanced accuracy and minimal tissue trauma. They are widely used across neurosurgery, orthopedic surgery, dental surgery, and otolaryngology (ENT) procedures.

Designed for ergonomic handling and minimal vibration, high-speed surgical drills contribute to better surgical outcomes by reducing operative time and improving control. The integration of pneumatic or electric-powered systems allows for consistent performance and adaptability in various clinical settings. Many models are equipped with safety features such as automatic shut-off and thermal regulation to prevent overheating and tissue damage.

Technological advancements have led to the development of cordless, lightweight, and modular drill systems that support multiple attachments and enhance intraoperative flexibility. These features make them suitable for both routine and high-risk surgical applications.

The demand for high-speed surgical drills is increasing due to the rising volume of surgical interventions, particularly in aging populations prone to orthopedic and spinal conditions. Additionally, the global shift toward minimally invasive surgeries is fueling the adoption of precision surgical instruments. Overall, high-speed surgical drills represent a critical tool in modern surgical practice, contributing to improved efficiency, safety, and patient outcomes.

Key Takeaways

- Market Size: The global high-speed surgical drill market is projected to reach approximately USD 0.9 billion by 2033, rising from USD 0.6 billion in 2023.

- Market Growth: The market is expected to expand at a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2024 to 2033.

- By Type Analysis: In 2023, the electric drill segment accounted for the largest market share at 63.2%. This dominance is attributed to its enhanced efficiency, precise performance, and ease of handling compared to pneumatic alternatives.

- By Application Analysis: The orthopedic segment held a substantial share of 48.4% in 2023. This is primarily driven by the growing prevalence of bone-related disorders and the increasing frequency of joint replacement procedures worldwide.

- By End-Use Analysis: Hospitals and clinics led the end-use segment with a 60.5% share in 2023. The high volume of complex and high-precision surgeries performed in these settings continues to drive the adoption of advanced surgical drilling systems.

- Regional Analysis: North America emerged as the leading regional market, contributing 39.8% of the total revenue in 2023. This leadership is supported by growing demand for surgical precision and efficiency across the healthcare sector.

- Competitive Landscape: The market is characterized by the presence of established medical device manufacturers who are heavily investing in research and development to enhance product innovation and expand their portfolio.

- Regulatory Impact: Stringent regulatory frameworks governing surgical devices play a significant role in shaping market trends, with a strong emphasis on ensuring product safety, reliability, and clinical efficacy.

Segmentation Analysis

- By Type Analysis: In 2023, the electric drill segment accounted for 63.2% of the market share, driven by its superior precision, adjustable speed, and low vibration compared to pneumatic models. Surgeons increasingly favor electric drills for delicate procedures in orthopedics and neurology. The development of cordless versions with extended battery life further enhances their usability. Rising surgical volumes and technological advancements are expected to sustain growth in this segment over the coming years.

- By Application Analysis: The orthopedic segment captured 48.4% of the market in 2023, supported by the rising incidence of bone-related conditions such as osteoporosis and osteoarthritis. An aging population and growing demand for joint replacement surgeries contribute significantly to this trend. High-speed surgical drills are essential in these procedures for precise bone manipulation. Moreover, the adoption of minimally invasive orthopedic techniques and ongoing investments in surgical infrastructure continue to drive demand for advanced drill systems.

- By End-use Analysis: Hospitals and clinics dominated the end-use segment in 2023 with a 60.5% revenue share, attributed to the high volume of complex surgeries performed in these settings. These facilities utilize high-speed drills across various disciplines, including orthopedics, neurology, and dental surgery. Rising trauma cases, elective procedures, and healthcare investments—especially in emerging markets—are expected to fuel further adoption. Additionally, the push to modernize surgical equipment supports continued growth in hospital-based usage of surgical drills.

Market Segments

By Type

- Pneumatic Drill

- Electric Drill

By Application

- Orthopedic

- Dental

- Neurology

- Others

By End-use

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

Regional Analysis

North America Dominates the High-speed Surgical Drill Market

North America held the leading position in the global high-speed surgical drill market in 2023, accounting for a revenue share of 39.8%. This dominance is attributed to the increasing demand for precision, efficiency, and safety in surgical procedures—particularly in orthopedic and dental applications. The rising number of complex surgeries, along with continuous advancements in surgical technology, has significantly contributed to market expansion.

Product innovation remains a key growth driver. For example, Zimmer Biomet Holdings launched the Zimmer Biomet surgical power tool system in July 2021, offering enhanced capabilities for various surgical procedures. Similarly, Stryker Corporation introduced the F1 Small Bone Power System in March 2021, a next-generation high-speed drill designed for bone surgeries. These developments support the broader adoption of minimally invasive surgical techniques and improved clinical outcomes across North America.

In addition, growing investments in surgical training and the presence of highly skilled healthcare professionals further support the demand for advanced surgical tools, reinforcing the region’s market leadership.

Asia Pacific to Register the Fastest CAGR Through 2033

The Asia Pacific region is anticipated to record the highest compound annual growth rate (CAGR) during the forecast period, driven by rapid advancements in healthcare infrastructure and a growing number of surgical interventions. Major economies such as China, India, and Japan are expected to play a pivotal role in this growth, backed by increasing healthcare spending and expanding access to surgical care.

Notable developments include the January 2024 launch of Myron Meditech’s dedicated online platform for orthopedic bone drills, which enhances product visibility and accessibility for healthcare professionals across the region. Such initiatives reflect the region’s shift toward digital engagement and informed decision-making in surgical equipment procurement.

The rising need for efficient, high-performance surgical tools to support complex procedures—combined with a growing emphasis on patient safety and outcomes—is projected to accelerate market growth across Asia Pacific. The ongoing modernization of healthcare systems and integration of advanced surgical technologies will further support long-term expansion.

Emerging Trends

- Integration with Robotic and Navigation Systems: The incorporation of high-speed drills with robotic assistance and navigation technologies has significantly improved surgical accuracy. A study involving 88 patients undergoing posterior spinal fusion demonstrated that using a navigated high-speed drill resulted in a 99.9% accuracy rate for drill paths, with 926 out of 927 paths accurately executed. This integration minimizes the risk of complications and enhances surgical outcomes.

- Advancements in Drill Design: Innovations such as shielded curved drills have been associated with improved intraoperative and clinical outcomes. In cervical corpectomy and fusion procedures, the use of these advanced drills has led to better surgical results, indicating a positive trend towards specialized drill designs tailored for specific procedures.

- Enhanced Safety Features: The development of drills with haptic feedback and penetration detection functions has enhanced surgical safety. In animal studies, drills equipped with these features detected penetration in approximately 0.015 seconds, significantly reducing the risk of inadvertent tissue damage.

- Minimally Invasive Surgical Applications: High-speed drills have facilitated the advancement of minimally invasive procedures. For instance, in transforaminal full-endoscopic spine surgery, the use of ultra-thin high-speed drills has expanded surgical options, allowing for procedures through smaller incisions and reducing patient recovery times.

Use Cases

- Neurosurgery: High-speed drills are essential in neurosurgical procedures, particularly for skull base surgeries. Their precision allows for the careful removal of bone near critical structures. However, improper use can lead to complications, emphasizing the need for proper training and technique.

- Spinal Surgery: In spinal surgeries, high-speed drills are utilized for procedures such as anterior cervical discectomy. Studies have shown that both high-speed drills and traditional curettes can be effective, with no significant differences in postoperative outcomes, suggesting that the choice of tool can be based on surgeon preference and specific case requirements.

- Orthopedic Surgery: High-speed drills are employed in orthopedic procedures for tasks like bone drilling and tissue debridement. Their use enables deeper access through bone material and efficient tissue removal, contributing to the effectiveness of orthopedic surgeries.

- Otolaryngology (ENT): In ENT surgeries, high-speed drills are used for procedures involving the removal of bone in areas like the sinuses. The development of universal consoles that accommodate both microdebriders and high-speed drills has streamlined surgical setups and improved efficiency.

Conclusion

In conclusion, the global high-speed surgical drill market is poised for steady growth, driven by rising surgical volumes, an aging population, and increasing demand for precision-based medical tools. Advancements in drill technology such as robotic integration, safety enhancements, and minimally invasive capabilities are improving surgical outcomes across specialties including orthopedics, neurosurgery, and ENT.

North America leads in market share, while Asia Pacific is projected to witness the fastest growth due to expanding healthcare infrastructure. The emphasis on efficiency, safety, and technological innovation continues to shape the market landscape, reinforcing the critical role of high-speed surgical drills in modern surgical practices.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)