Table of Contents

Overview

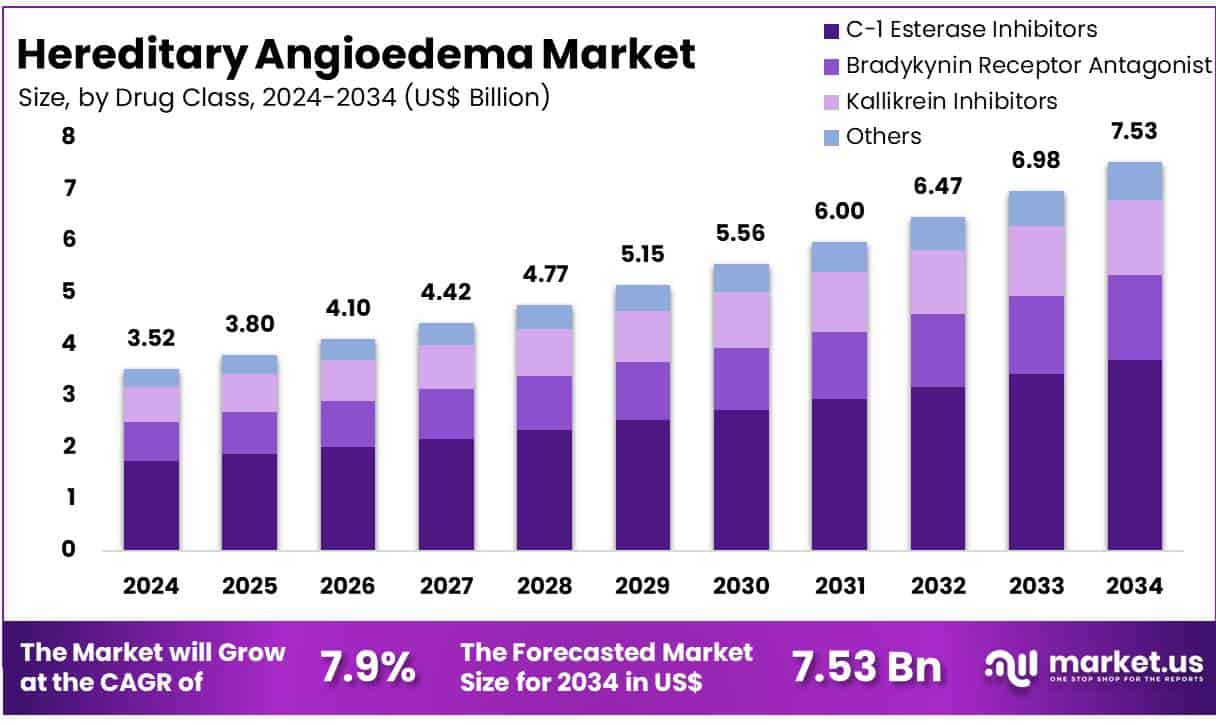

New York, NY – May 23, 2025 – The Global Hereditary Angioedema Market size is expected to be worth around US$ 7.53 billion by 2034 from US$ 3.52 billion in 2024, growing at a CAGR of 7.9% during the forecast period 2025 to 2034.

A growing emphasis on rare disease awareness and therapeutic innovation is placing Hereditary Angioedema (HAE) at the forefront of clinical and pharmaceutical developments worldwide. HAE is a rare, potentially life-threatening genetic disorder characterized by recurrent episodes of severe swelling in various parts of the body, including the limbs, face, intestinal tract, and airway.

The global burden of HAE is increasing due to improved genetic screening, heightened clinical awareness, and expanded patient advocacy initiatives. The condition is primarily caused by a deficiency or dysfunction of the C1 esterase inhibitor (C1-INH) protein, with most cases inherited in an autosomal dominant pattern.

Recent advancements in targeted therapies have significantly improved patient outcomes. Prophylactic and on-demand treatments such as C1-INH replacement, kallikrein inhibitors, and bradykinin receptor antagonists are demonstrating high efficacy in reducing the frequency and severity of attacks.

The availability of subcutaneous and oral therapies is further enhancing quality of life and treatment adherence among HAE patients. Regulatory agencies such as the U.S. FDA and EMA have granted orphan drug designations to multiple HAE therapies, accelerating innovation in this space. As precision medicine gains traction, continued investment in HAE research and diagnostic tools is anticipated to drive earlier detection and more personalized care approaches in the years ahead

Key Takeaways

- Market Size Outlook: The global Hereditary Angioedema (HAE) market is projected to reach approximately USD 7.53 billion by 2034, rising from USD 3.52 billion in 2024.

- Growth Rate: The market is anticipated to expand at a compound annual growth rate (CAGR) of 7.9% between 2025 and 2034, driven by therapeutic innovations and increasing disease awareness.

- Drug Class Analysis: The C1-esterase inhibitor segment emerged as the leading drug class in 2023, accounting for 49.2% of total market revenue, owing to its effectiveness in both acute and prophylactic treatment settings.

- Treatment Approach: Prophylactic treatment remains the dominant approach, holding a 41.0% market share, as preventive therapies gain traction for long-term disease management.

- Route of Administration: Intravenous (IV) administration continues to dominate, capturing 49.2% market share, especially in acute and emergency use cases.

- Distribution Channel: Hospital pharmacies represent the largest distribution channel, contributing 45.5% of total sales, due to their central role in dispensing acute and inpatient therapies.

- Regional Insights: North America led the global market in 2023, securing 46.8% market share with revenue exceeding USD 1.54 billion, supported by advanced healthcare infrastructure and favorable reimbursement frameworks.

Segmentation Analysis

- Drug Class Analysis: In 2023, the C1-esterase inhibitor segment led the Hereditary Angioedema (HAE) market with a 49.2% revenue share, attributed to its dual role in both on-demand and preventive treatment. Meanwhile, kallikrein inhibitors are projected to witness the highest growth during the forecast period. These therapies reduce bradykinin production by inhibiting kallikrein, effectively lowering attack frequency and offering targeted options that expand therapeutic choices for patients seeking long-term control of HAE symptoms.

- Treatment Approach Analysis: Prophylactic treatment accounted for 41.0% of the market in 2023, making it the leading therapeutic approach. Designed to prevent HAE attacks before they occur, this method is preferred for patients with frequent or severe episodes. The widespread use of approved agents like Lanadelumab (Takhzyro) and C1-INH therapies (e.g., Haegarda, Cinryze) has reinforced this trend, as these treatments significantly reduce attack rates and support long-term disease management in both clinical and home settings.

- Route of Administration Analysis: Intravenous (IV) administration dominated the HAE market with a 49.2% share in 2023, primarily used in acute care settings for rapid symptom relief. IV delivery of C1-INH therapies such as Cinryze and Berinert remains standard during emergency episodes. However, subcutaneous (SC) treatments are rapidly gaining preference for prophylactic use. Agents like Lanadelumab and Icatibant offer ease of administration and support home-based care, contributing to their expected higher growth rate during the forecast period.

- Distribution Channel Analysis: Hospital pharmacies held a dominant 45.5% market share in 2023, reflecting their critical role in managing severe HAE attacks with IV-administered therapies during emergencies. These settings are essential for immediate intervention. However, retail pharmacies are emerging as key distribution points for subcutaneous and self-administered medications, particularly those used in prophylactic care. Drugs such as Icatibant and Lanadelumab are increasingly dispensed for home use, supporting the shift toward patient-centered and preventive treatment strategies.

Market Segments

By Drug Class

- C-1 Esterase Inhibitors

- Bradykynin Receptor Antagonist

- Kallikrein Inhibitors

- Others

By Treatment Approach

- Acute Treatment

- Prophylactic (Preventive) Treatment

- On-demand (Symptom Relief) Treatment

By Route of Administration

- Intravenous

- Subcutaneous

- Oral

By Distribution channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Regional Analysis

North America represents the most mature market for Hereditary Angioedema (HAE), accounting for 46.8% of the global market share in 2023. This dominance is attributed to the region’s advanced healthcare infrastructure, widespread awareness, and robust diagnostic capabilities, particularly in the United States and Canada. Early detection and timely access to treatment options have contributed significantly to improved patient outcomes.

The region offers a comprehensive portfolio of approved therapies, including C1 esterase inhibitors, monoclonal antibodies such as Lanadelumab, and bradykinin receptor antagonists like Icatibant. These options have enhanced disease management and quality of life for HAE patients.

According to data from the National Institutes of Health (NIH), the estimated prevalence of HAE in the U.S. is approximately 1 in 50,000 individuals. However, reported prevalence can vary, ranging from 1 in 10,000 to 1 in 150,000. The condition affects individuals irrespective of sex or ethnicity, indicating a uniform distribution across demographic groups.

Emerging Trends

- A shift toward targeted prophylactic therapies has been observed, with monoclonal antibodies replacing plasma-derived C1-INH in many treatment plans. Lanadelumab, administered subcutaneously every two weeks (with some patients extending to four-week dosing after six months attack-free), has demonstrated an 87.4 % reduction in monthly attack rate and a mean of 97.7 % attack-free days during long-term studies.

- Oral prophylaxis has become available with the December 2020 FDA approval of berotralstat. In phase 3 trials, daily doses of 150 mg reduced monthly attacks by 44 % versus placebo (attack rate ratio 0.56; 95 % CI 0.41–0.77).

- Gene-silencing and mRNA-targeted agents are in development. Donidalorsen, an antisense oligonucleotide, has been shown to lower prekallikrein levels by ~70 % and reduce attack rates by ~90 % in early studies.

- Short-term oral prophylaxis (on-demand) is emerging for procedural use. Sebetralstat, dosed three times daily, is under investigation for prevention of attacks around surgeries or dental work.

Pediatric indications have expanded: lanadelumab received pediatric approval (ages 2+) in February 2023, extending its prophylactic use beyond the original 12 years and older population. - Treatment models have trended toward home-based, self-administered care, improving patient convenience and quality of life. Self-injection training and remote monitoring tools are increasingly integrated into care pathways.

Use Cases

- Routine Prophylaxis in Adolescents and Adults: Patients aged ≥ 12 years received lanadelumab 300 mg SC every two weeks, resulting in an 87.4 % mean reduction in attack rate and over 80 % of patients remaining attack-free for at least six months.

- Daily Oral Prevention: In a 24-week, placebo-controlled trial (n = 121), berotralstat 150 mg once daily reduced attacks from a baseline of ~3.0 to 1.7 per month, with a statistically significant attack rate ratio of 0.56 (P < 0.001).

- Short-Term Prophylaxis for Procedures: Sebetralstat, administered orally three times per day, is under evaluation for preventing attacks associated with surgeries or dental procedures, offering a needle-free, patient-controlled option.

- Management in C1-INH–Normal Patients (HAE-nC1INH): Oral berotralstat has stabilized or reduced attack frequency and severity in patients who switched from injectable prophylaxis, with most reporting significant clinical benefit and tolerable side effects.

- Pediatric Acute and Long-Term Care: For children aged 2–11 years, plasma-derived C1-INH products (e.g., Berinert for acute attacks; Cinryze for prophylaxis) and attenuated androgens (e.g., danazol) are used, with personalized dosing based on pharmacokinetic matching to adolescent data.

- Future One-Time Gene Therapy: CRISPR-based therapies targeting the KLKB1 gene (e.g., NTLA-2002) are in early trials, aiming for a single treatment that could reduce prekallikrein production and prevent attacks long-term.

Conclusion

The Hereditary Angioedema (HAE) market is experiencing significant transformation driven by advances in targeted therapies, improved diagnostic capabilities, and increased awareness. Prophylactic treatments and self-administered options such as lanadelumab and berotralstat are enhancing patient outcomes and adherence. The market is projected to grow at a 7.9% CAGR, reaching USD 7.53 billion by 2034.

Innovations in oral therapies, pediatric indications, and gene-silencing approaches are expanding treatment possibilities. North America remains the leading region, supported by robust healthcare systems and early diagnosis. Continued investment in R&D is expected to further refine precision care and improve quality of life for HAE patients.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)