Overview

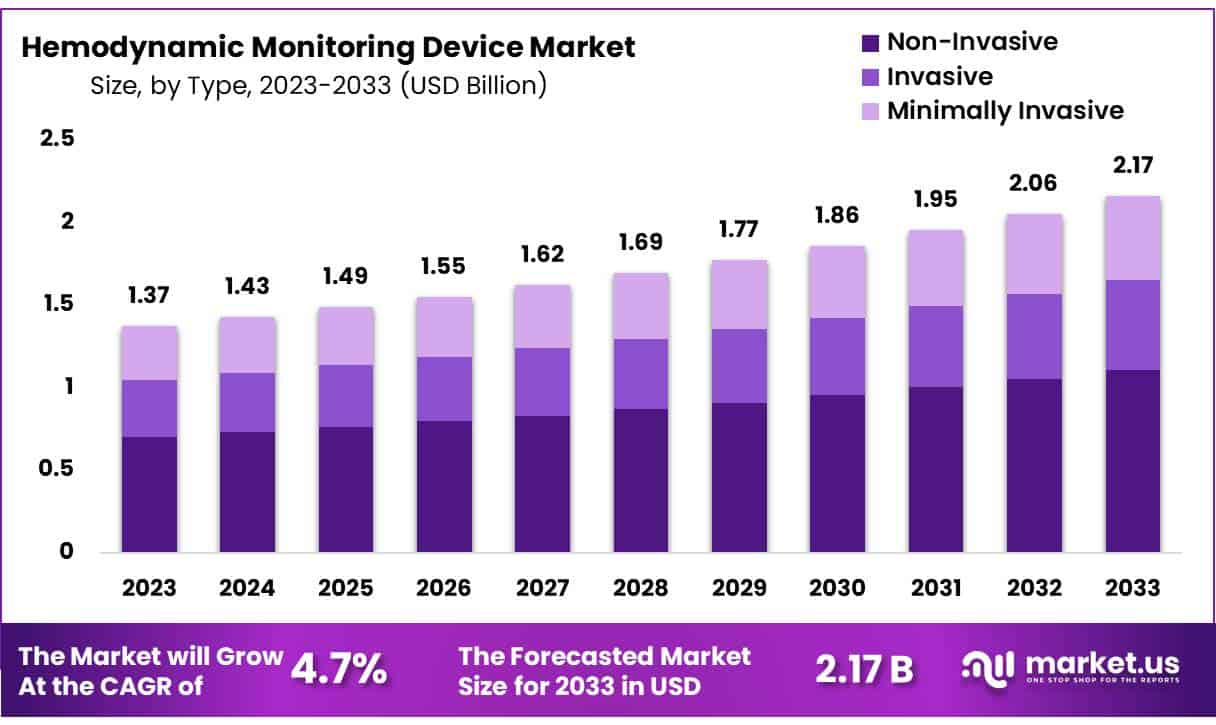

New York, NY – Jan 06, 2026 – Global Hemodynamic Monitoring Device Market size is expected to be worth around USD 2.17 Billion by 2033 from USD 1.37 Billion in 2023, growing at a CAGR of 4.7% during the forecast period from 2024 to 2033.

Hemodynamic monitoring devices are advanced medical systems designed to continuously assess cardiovascular function in critically ill and high-risk patients. These devices measure key physiological parameters such as blood pressure, cardiac output, heart rate, stroke volume, and oxygen delivery, enabling clinicians to make timely and informed treatment decisions.

The basic formation of a hemodynamic monitoring device includes sensors, monitoring hardware, data processing units, and display interfaces. Sensors are either invasive or non-invasive and are responsible for capturing real-time physiological signals from the patient. These signals are transmitted to monitoring hardware, where they are processed using validated algorithms to generate accurate hemodynamic parameters. The processed data are then displayed on user-friendly interfaces, allowing healthcare professionals to interpret trends and variations efficiently.

Hemodynamic monitoring devices are widely used in intensive care units, operating rooms, emergency departments, and cardiac care settings. Their adoption has been driven by the increasing prevalence of cardiovascular diseases, rising numbers of surgical procedures, and the growing demand for precision-based critical care. Technological advancements, including minimally invasive techniques, wireless connectivity, and integration with hospital information systems, have further enhanced device performance and clinical utility.

The market growth of hemodynamic monitoring devices can be attributed to improved patient outcomes through early detection of hemodynamic instability and optimized fluid and drug management. As healthcare systems continue to prioritize patient safety and data-driven clinical decisions, hemodynamic monitoring devices are expected to remain a core component of modern critical care infrastructure.

Key Takeaways

- Market Size: The Hemodynamic Monitoring Device Market is projected to reach approximately USD 2.17 billion by 2033, increasing from USD 1.37 billion in 2023.

- Market Growth: The market is anticipated to expand at a compound annual growth rate (CAGR) of 4.7% during the forecast period from 2024 to 2033.

- Type Analysis: Non-invasive hemodynamic monitoring devices dominate the market, accounting for a leading share of 51.27%.

- Product Analysis: In 2023, hemodynamic monitors represented the largest product segment, capturing 54.13% of the total market share.

- End-Use Analysis: Hospitals emerged as the primary end users in 2023, holding a significant market share of 41.38%.

- Regional Analysis: North America maintained a dominant position in 2023, contributing 40.5% of the global Hemodynamic Monitoring Device Market revenue.

- Technological Advancements: The integration of artificial intelligence and machine learning into real-time monitoring systems is accelerating market growth by enhancing clinical accuracy and decision-making.

- Rising Incidence of Cardiovascular Diseases: The growing prevalence of cardiovascular disorders, combined with an expanding aging population, is driving increased demand for hemodynamic monitoring devices across healthcare settings.

- Non-Invasive Monitoring Preference: A rising preference for non-invasive monitoring solutions is being observed, as these technologies reduce procedural risks and improve overall patient safety.

Regional Analysis

In 2023, North America accounted for a leading 40.5% share of the global Hemodynamic Monitoring Device Market. This dominance can be attributed to the presence of a well-established healthcare infrastructure, early adoption of advanced medical technologies, and a high prevalence of cardiovascular diseases across the region. The expanding geriatric population has further increased the need for accurate and real-time cardiovascular monitoring solutions.

Moreover, strong investments in research and development, along with rising healthcare expenditure, have supported the adoption of non-invasive and minimally invasive hemodynamic monitoring technologies. Collectively, these factors reinforce North America’s role as a major contributor to global market growth, supporting sustained innovation and long-term market expansion.

Emerging Trends

- Shift Toward Noninvasive and Minimally Invasive Technologies: A clear transition is being observed from conventional invasive techniques, such as pulmonary artery catheterization, toward noninvasive and minimally invasive monitoring solutions. Technologies including pulse contour analysis, thoracic bioimpedance, and bioreactance are being increasingly adopted, as they lower procedural risks, enhance patient safety, and improve overall comfort.

- Growing Adoption of Dynamic Hemodynamic Parameters: Clinical practice is progressively moving away from static measurements toward dynamic monitoring parameters to more accurately evaluate fluid responsiveness and cardiac performance. This shift enables more precise and timely clinical decision-making, particularly in high-acuity and critical care environments.

- Integration of Predictive Analytics and Artificial Intelligence: Modern hemodynamic monitoring systems are increasingly incorporating predictive analytics and artificial intelligence capabilities. These technologies support early identification of hemodynamic instability, facilitating proactive intervention, optimizing treatment strategies, and improving patient outcomes.

- Advancement of Wearable and Portable Monitoring Devices: The development of wearable and portable hemodynamic monitoring devices is expanding the scope of continuous patient observation beyond hospital settings. These solutions support remote patient monitoring, enhance outpatient care management, and contribute to improved continuity of care.

Key Use Cases

- Critical Care and Intensive Care Units (ICUs): Hemodynamic monitoring plays a central role in ICUs for the management of patients with severe cardiovascular and respiratory conditions. Continuous assessment of parameters such as cardiac output, blood pressure, and vascular resistance informs therapeutic adjustments and supports clinical stability.

- Perioperative Monitoring: During surgical procedures, particularly in cardiac and complex surgeries, hemodynamic monitoring is essential to ensure patient safety. Real-time physiological data enables anesthesiologists to maintain adequate perfusion, optimize oxygen delivery, and promptly address intraoperative instability.

- Emergency and Trauma Care: In emergency and trauma settings, rapid evaluation of hemodynamic status is critical for early diagnosis and treatment of conditions such as shock or acute hemorrhage. Noninvasive monitoring technologies provide immediate and actionable data, supporting timely clinical intervention.

- Management of Chronic Cardiovascular Conditions: Patients with chronic conditions, including heart failure and hypertension, increasingly benefit from ongoing hemodynamic monitoring. Wearable devices allow continuous data collection, enabling early detection of deterioration, timely therapy adjustments, and reduced hospital readmission rates.

- Clinical Research and Trials: Hemodynamic monitoring devices are widely utilized in clinical research and trials to assess the safety and effectiveness of emerging therapies. Precise and reliable measurement of cardiovascular parameters is essential to ensure data accuracy, reproducibility, and regulatory compliance.

Frequently Asked Questions on Hemodynamic Monitoring Device

- Where are hemodynamic monitoring devices commonly used?

Hemodynamic monitoring devices are primarily used in intensive care units, operating rooms, emergency departments, and cardiac care units, where continuous and accurate cardiovascular assessment is essential for timely clinical decision-making and patient stabilization. - What are the main types of hemodynamic monitoring devices?

Hemodynamic monitoring devices are broadly categorized into invasive, minimally invasive, and non-invasive systems, with non-invasive devices gaining preference due to reduced procedural risks, improved patient comfort, and advancements in monitoring accuracy. - What factors are driving the hemodynamic monitoring device market?

Market growth is driven by the rising prevalence of cardiovascular diseases, increasing surgical procedures, an aging population, and growing demand for real-time patient monitoring, supported by continuous technological advancements in healthcare systems. - Why is non-invasive monitoring gaining popularity?

Non-invasive hemodynamic monitoring is increasingly adopted as it minimizes infection risks, reduces complications, lowers healthcare costs, and enhances patient safety, while still delivering reliable and continuous cardiovascular data for clinical evaluation. - How do technological advancements impact this market?

Innovations such as artificial intelligence, machine learning, and wireless connectivity have improved data accuracy, predictive capabilities, and workflow efficiency, significantly enhancing the clinical value and adoption rate of hemodynamic monitoring devices. - Which end users dominate the hemodynamic monitoring device market?

Hospitals represent the largest end-user segment due to high patient inflow, availability of advanced infrastructure, and increased demand for continuous cardiovascular monitoring in critical care and surgical environments. - What is the future outlook for the hemodynamic monitoring device market?

The market is expected to witness steady growth, supported by expanding healthcare investments, increasing adoption of non-invasive technologies, and a global shift toward data-driven and precision-based patient care models.

Conclusion

The hemodynamic monitoring device market represents a critical component of modern critical care, driven by the growing burden of cardiovascular diseases, rising surgical volumes, and increasing demand for precision-based clinical decision-making. Continuous technological advancements, particularly in non-invasive monitoring, artificial intelligence, and wearable solutions, are enhancing clinical accuracy, patient safety, and workflow efficiency.

Strong adoption across hospitals and critical care settings, especially in North America, supports sustained market expansion. As healthcare systems increasingly prioritize early detection, data-driven treatment, and improved patient outcomes, hemodynamic monitoring devices are expected to maintain steady growth and long-term clinical relevance.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)