Table of Contents

Overview

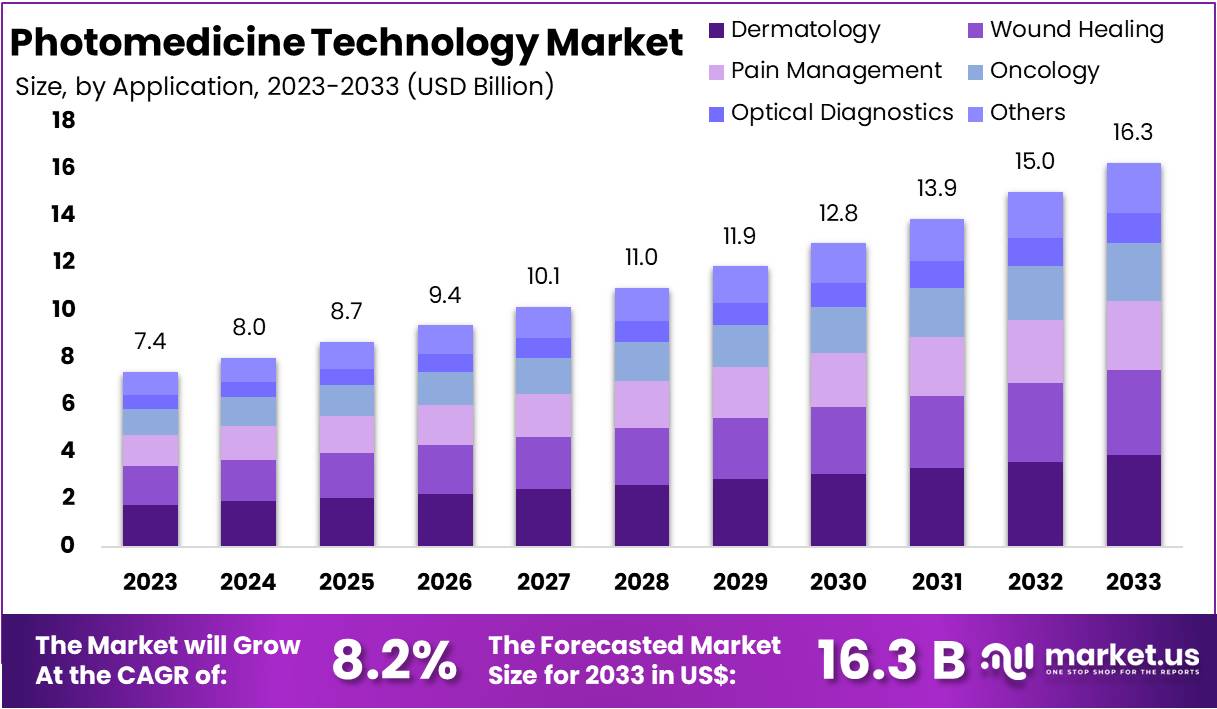

New York, NY – Feb 17, 2026 – The Global Photomedicine Technology Market size is expected to be worth around US$ 16.3 Billion by 2033, from US$ 7.4 Billion in 2023, growing at a CAGR of 8.2% during the forecast period from 2024 to 2033.

Photomedicine technology represents a specialized field within medical science focused on the therapeutic application of light for diagnostic and treatment purposes. The foundational concept is based on the interaction between specific wavelengths of light and biological tissues to stimulate, repair, or modify cellular functions. This controlled light exposure is delivered through advanced devices such as lasers, light-emitting diodes (LEDs), and broadband light systems.

The basic formation of photomedicine technology involves three core components a calibrated light source, a targeted delivery system, and tissue-specific response mechanisms. Light sources are engineered to emit precise wavelengths, typically within ultraviolet (UV), visible, or near-infrared spectra. These wavelengths penetrate tissues at varying depths, enabling targeted treatment of dermatological, oncological, ophthalmic, and musculoskeletal conditions.

The therapeutic effect is achieved through photobiomodulation, photothermal, or photochemical reactions. In photobiomodulation, cellular mitochondria absorb light energy, leading to enhanced adenosine triphosphate (ATP) production and improved cellular repair processes. Photothermal effects generate localized heat to remove or reshape tissue, while photochemical reactions activate light-sensitive compounds for targeted therapies.

Advancements in optical engineering, semiconductor technology, and clinical research have strengthened the safety and precision of these systems. As healthcare providers increasingly prioritize minimally invasive treatment modalities, photomedicine technology continues to gain adoption across hospitals, specialty clinics, and research institutions. Ongoing innovation is expected to further expand its clinical applications and commercial potential.

Key Takeaways

- The Photomedicine Technology Market is expected to attain a valuation of approximately USD 16.3 billion by 2033, rising from USD 7.4 billion in 2023, reflecting a compound annual growth rate (CAGR) of 8.2% during the forecast period.

- In 2023, the lasers category dominated the type segment, contributing more than 52% of the overall market revenue.

- Within the application segment, dermatology emerged as the leading category in 2023, accounting for over 24% of total market share.

- North America held the largest regional share in 2023 at 49%, representing a market value of approximately USD 3.6 billion.

Regional Analysis

In 2023, North America accounted for over 49% of the global Photomedicine Technology Market, representing a market value of approximately USD 3.6 billion. This leadership position has been supported by the strong adoption of advanced photomedicine solutions across healthcare facilities in the region. The presence of major industry participants and sustained investments in research and development have accelerated technological innovation and commercialization. A well-developed healthcare infrastructure has further enabled the widespread integration of photomedicine in clinical practice.

Demand for non-invasive treatment options in dermatology, oncology, and pain management has remained high, driven by growing patient preference for therapies associated with minimal side effects. Supportive regulatory frameworks have also facilitated the approval and deployment of advanced medical devices. The United States contributed the largest share within the region, supported by extensive healthcare networks and technological advancements. Canada also demonstrated steady adoption, particularly in dermatology and wound care applications, reinforcing regional market strength.

Emerging Trends in the Pharmaceutical Excipients Market

- Regulatory Facilitation for Novel Excipients: A voluntary pilot initiative, known as PRIME, has been introduced by the U.S. Food and Drug Administration through its Center for Drug Evaluation and Research (CDER) to evaluate excipients not previously utilized in approved drug products and not widely used in food applications. During the initial two-year phase, approximately four proposals (two annually) were planned for comprehensive review, focusing on toxicological and quality-related data. This structured regulatory pathway is intended to reduce uncertainty and encourage innovation in excipient development.

- Expansion of Co-Processed Excipients (CoPEs): The European Medicines Agency has issued harmonized Q&As outlining three risk categories for co-processed excipients applied in solid oral dosage forms. These materials integrate multiple functional attributes, such as binding and disintegration, within a single excipient system. Adoption has been increasing due to advantages including reduced tablet dimensions, improved manufacturability, and simplified formulation design.

- Increased Review Throughput for Excipient Suitability Petitions: Under Generic Drug User Fee Amendments (GDUFA) performance objectives, the FDA has strengthened its review capacity for excipient suitability petitions. Up to 50 petitions were targeted for review within a six-month timeframe in FY 2024, with projected increases to 70 in FY 2025 and 80 in FY 2026. This enhancement is expected to accelerate generic drug development timelines when formulation changes involving novel excipients are proposed.

- Early Regulatory Engagement on Excipient Strategy: Recent FDA guidance emphasizes proactive discussion of novel excipients during the Investigational New Drug (IND) stage. Early interaction with regulators is encouraged to address safety, compatibility, and formulation challenges before pivotal clinical development. This approach supports risk mitigation and improves development efficiency.

- Substitution of Titanium Dioxide in Oral Formulations: Following safety evaluations and regulatory reassessment, the EMA released technical guidance in July 2022 addressing the removal or substitution of titanium dioxide in oral dosage forms. As a result, research activity has intensified toward alternative whitening and opacifying agents that comply with evolving EU regulatory requirements.

Key Use Cases

- Abuse-Deterrent Opioid Formulations: Within the FDA’s PRIME framework, two novel excipient proposals designed to enhance viscosity and gel strength in opioid tablets were selected during the initial review period. These excipients are being assessed for their capacity to resist tampering and limit rapid drug release, thereby strengthening abuse-deterrent properties.

- Generic Reformulation Through Suitability Petitions: In FY 2024, up to 50 excipient suitability petitions were reviewed within the six-month performance target. This pathway enables generic manufacturers to replace an FDA-approved excipient, such as microcrystalline cellulose, with a functionally comparable alternative without submitting a full new drug application. The mechanism supports cost-effective and time-efficient product entry.

- Application of Co-Processed Excipients in Solid Oral Dosage Forms: Manufacturers of immediate-release tablets have increasingly incorporated CoPEs classified under EMA risk categories: Category I (low risk), Category II (moderate risk), and Category III (high risk), based on compositional and functional complexity. This strategy consolidates multiple excipient functions such as filler and binder into one to three materials, enhancing formulation robustness and operational efficiency.

- Formulation Optimization During IND Development: Early-stage clinical programs have benefited from regulatory engagement on novel excipient selection. In several IND submissions, discussions with the FDA occurred within approximately six weeks, facilitating improved bioavailability outcomes and reducing the extent of nonclinical testing requirements. This proactive strategy has contributed to accelerated first-in-human study initiation.

- Reformulation Without Titanium Dioxide: By mid-2022, more than 30 marketing authorization holders in the EU had submitted regulatory variations to replace titanium dioxide with alternative pigments, including calcium carbonate, in solid oral products. These modifications align with EMA technical guidance and reflect a broader industry transition toward compliant excipient alternatives.

Frequently Asked Questions on Photomedicine Technology

- How does photomedicine technology work?

Photomedicine technology works by delivering specific wavelengths of light to targeted tissues, stimulating biological responses such as cell regeneration or selective tissue destruction. The therapeutic effect depends on wavelength, intensity, and exposure time, ensuring precision and controlled treatment outcomes. - What are the major applications of photomedicine technology?

Major applications include photodynamic therapy for cancer treatment, laser surgery, skin rejuvenation, acne treatment, and ophthalmic procedures. It is also used in pain management and wound healing, where controlled light exposure supports tissue repair and reduces inflammation. - What are the benefits of photomedicine technology?

The technology offers minimally invasive procedures, reduced recovery time, limited side effects, and high precision. It allows targeted therapy with minimal damage to surrounding tissues, improving patient safety and treatment efficiency across multiple clinical specialties. - What types of devices are used in photomedicine?

Devices commonly used include lasers, LED therapy systems, intense pulsed light (IPL) devices, and fiber-optic delivery systems. These instruments are designed to provide controlled light emission suitable for various therapeutic and diagnostic medical applications. - What is the current outlook of the photomedicine technology market?

The photomedicine technology market is experiencing steady growth, supported by rising demand for minimally invasive treatments and advancements in laser technologies. Increasing adoption in dermatology and oncology segments has significantly contributed to expanding global market revenues. - Which regions dominate the photomedicine technology market?

North America holds a significant market share due to advanced healthcare infrastructure and high adoption of aesthetic procedures. Europe follows closely, while Asia-Pacific is expected to witness rapid growth owing to rising healthcare investments and patient awareness. - What are the key challenges in the photomedicine technology market?

High equipment costs, strict regulatory requirements, and limited reimbursement policies in certain regions present challenges. Additionally, the need for skilled professionals to operate advanced photomedicine systems may restrict broader adoption in developing markets. - Who are the key end-users in the photomedicine technology market?

Hospitals, specialty clinics, dermatology centers, and ambulatory surgical centers represent major end-users. Increasing demand from cosmetic and aesthetic clinics has also significantly expanded the commercial scope of photomedicine technology applications globally.

Conclusion

In conclusion, photomedicine technology has evolved into a critical component of modern therapeutic practice, driven by precise light-based interventions and continuous advancements in optical engineering. The market is projected to expand from USD 7.4 billion in 2023 to approximately USD 16.3 billion by 2033, registering a CAGR of 8.2%.

Growth has been supported by strong demand for minimally invasive treatments, particularly in dermatology and oncology, and by the dominance of laser-based systems. North America maintains leadership due to advanced healthcare infrastructure and innovation capacity. Despite regulatory and cost challenges, sustained research and rising clinical adoption are expected to reinforce long-term market expansion.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)