Table of Contents

Overview

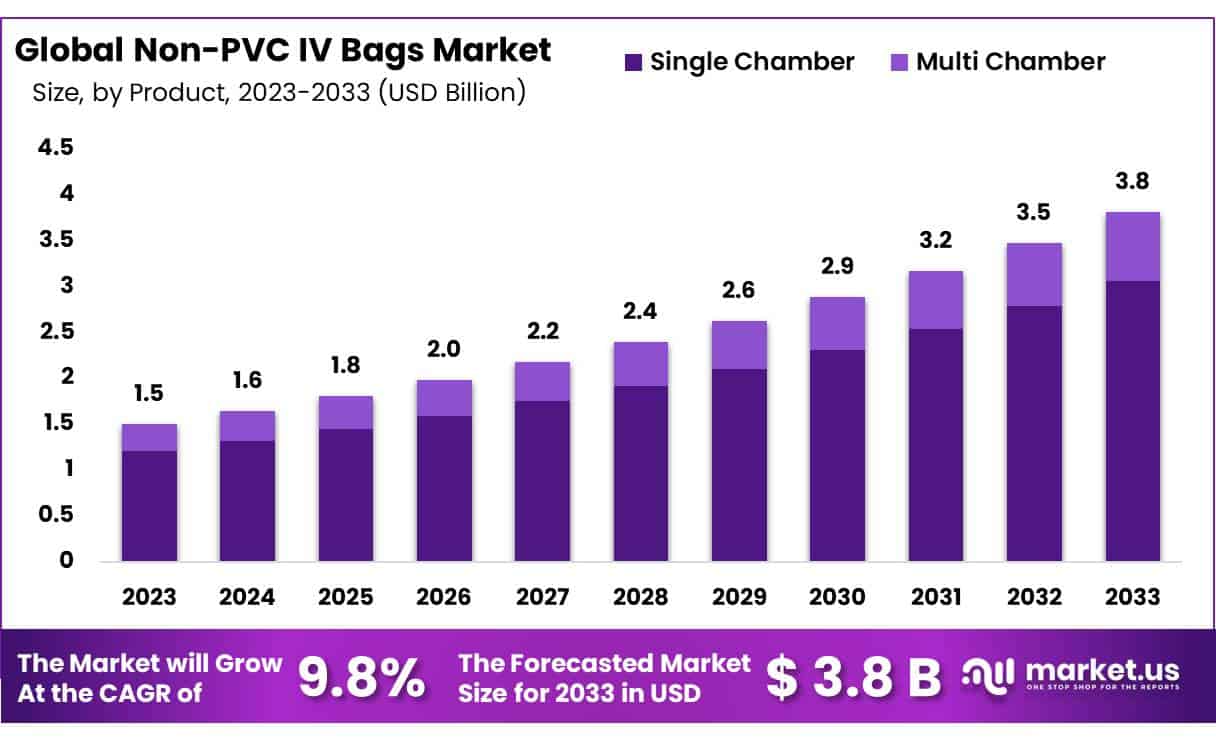

New York, NY – Jan 29, 2026 – The Global Non-PVC IV Bags Market size is expected to be worth around USD 3.8 Billion by 2033 from USD 1.5 Billion in 2023, growing at a CAGR of 9.8% during the forecast period 2024 to 2033.

The formulation of non-PVC intravenous (IV) bags has gained increasing attention across the global healthcare sector due to rising concerns over patient safety, regulatory compliance, and environmental impact. Non-PVC IV bags are primarily manufactured using alternative polymer materials such as polypropylene (PP), polyethylene (PE), and ethylene vinyl acetate (EVA). These materials are selected for their chemical stability, flexibility, and compatibility with a wide range of pharmaceutical solutions.

Unlike conventional PVC-based IV bags, non-PVC variants do not require plasticizers such as di-(2-ethylhexyl) phthalate (DEHP), which have been associated with potential health risks. The absence of DEHP improves product safety, particularly in sensitive applications including oncology, neonatal care, and long-term infusion therapies. Additionally, non-PVC materials exhibit lower drug adsorption and leaching characteristics, supporting higher drug integrity during storage and administration.

The basic formulation process involves polymer resin selection, extrusion or film-blowing, and advanced sealing technologies to ensure sterility and durability. These bags are designed to withstand terminal sterilization methods while maintaining mechanical strength and transparency.

The adoption of non-PVC IV bags is being driven by stringent regulatory standards, growing awareness of sustainable medical packaging, and increased demand from hospitals and pharmaceutical manufacturers. As healthcare systems continue to prioritize safety and environmental responsibility, non-PVC IV bags are positioned as a critical component in modern infusion therapy solutions.

Key Takeaways

- Market Size: The Non-PVC IV Bags Market is projected to reach approximately USD 3.8 billion by 2033, expanding from USD 1.5 billion in 2023.

- Market Growth: Market expansion is expected to occur at a compound annual growth rate (CAGR) of 9.8% during the forecast period 2024–2033.

- Product Analysis: In 2023, the single-chamber segment led the market, accounting for 64.7% of total revenue share.

- Application Analysis: Ethylene Vinyl Acetate (EVA) emerged as the leading material type, capturing approximately 31.8% of the market share in 2023.

- Content Analysis: The liquid mixtures segment represented the dominant content type in 2023, contributing nearly 80.2% of overall market share.

- Regional Analysis: North America maintained its leading position in the global market, holding a dominant 41.6% share in 2023.

Regional Analysis

North America accounted for the largest share of the Non-PVC IV Bags Market, holding 41.6% of total revenue in 2023. The region’s dominance is primarily driven by stringent regulatory frameworks aimed at enhancing patient safety, which have accelerated the adoption of non-PVC IV containers. These products support safe and effective patient care by minimizing the risk of harmful chemical exposure. Additionally, the high prevalence of stomach cancer in the region has contributed to increased demand for IV bags.

According to estimates from the American Cancer Society, approximately 27,600 new stomach cancer cases were diagnosed in the United States in 2020, with around 11,010 related deaths reported. Patients undergoing treatment for stomach cancer often depend on total parenteral nutrition, as oral food intake becomes limited or impossible.

This dependency is expected to drive demand for ethylene-vinyl acetate (EVA) IV bags, thereby supporting overall market growth. Furthermore, the region is witnessing increased adoption of advanced drug delivery systems and continuous technological innovations, which are expected to further strengthen market expansion.

Asia Pacific is anticipated to register the highest CAGR during the forecast period. Market growth in the region is supported by the competitive presence of local manufacturers, who offer cost-effective products that enhance international demand. Factors such as rising foreign direct investments, rapid expansion of healthcare infrastructure, and an increasing number of hospitals and clinics are collectively contributing to the strong growth outlook of the Non-PVC IV Bags Market in this region.

Emerging Trends

Non-polyvinyl chloride (non-PVC) intravenous (IV) bags are increasingly recognized as an important advancement in modern medical practice, primarily due to safety concerns associated with conventional PVC-based containers. The transition has been driven by the potential health risks linked to di(2-ethylhexyl) phthalate (DEHP), a plasticizer widely used in PVC products. DEHP has been shown to leach into IV solutions, which may affect protein stability and trigger activation of the complement system, potentially leading to adverse immune reactions during the administration of therapeutic agents.

To mitigate these risks, healthcare providers are progressively adopting non-PVC IV bags manufactured from alternative materials such as polyolefins, including polyethylene (PE) and polypropylene (PP), as well as ethylene vinyl acetate (EVA). These materials do not require phthalate plasticizers to achieve flexibility, thereby eliminating the risk of DEHP migration into infused solutions.

Despite their clinical advantages, non-PVC IV bags present certain operational challenges. Evidence suggests that some non-PVC infusion bags may experience higher leakage rates when compared with upright polypropylene containers. Leakage is commonly associated with mechanical stress during squeezing, stacking, or uneven placement, which can cause edge folding, as well as weaknesses at nozzle joints. Such issues may result in increased material wastage, higher costs, and potential procedural risks.

Nevertheless, the healthcare sector continues to prioritize the development and adoption of safer alternatives to PVC-based medical devices. The growing use of non-PVC IV bags reflects a broader commitment to improving patient safety by reducing exposure to harmful plasticizers. Continued research and material innovation are expected to address existing limitations, enhancing the durability, performance, and reliability of non-PVC IV systems in clinical environments.

Use Cases

- Chemotherapy Administration: Non-PVC IV bags are extensively used for delivering chemotherapy drugs. Their chemical stability minimizes interactions with cytotoxic agents, preserving drug efficacy and reducing the likelihood of unintended side effects.

- Parenteral Nutrition: For patients dependent on intravenous nutritional support, non-PVC IV bags provide a safer solution by reducing the risk of material–solution interactions and contamination, which is critical for long-term patient care.

- Neonatal Care: In neonatal intensive care units, the use of DEHP-free, non-PVC IV bags is particularly important. Newborns are highly susceptible to chemical exposure, and these bags support safer infusion practices for this vulnerable population.

- Blood Storage and Transfusion: Non-PVC IV bags are also employed in the storage and transfusion of blood and blood components. Their biocompatible properties help maintain blood integrity, lowering the risk of contamination and supporting safe transfusion outcomes.

Frequently Asked Questions on Non-PVC IV Bags

- Why are Non-PVC IV bags considered safer than PVC bags?

They are considered safer because they eliminate DEHP plasticizers commonly used in PVC, lowering patient exposure to toxic compounds, improving drug compatibility, and supporting stricter hospital safety and regulatory compliance requirements. - What medical applications commonly use Non-PVC IV bags?

Non-PVC IV bags are widely used for parenteral nutrition, chemotherapy, saline, glucose, and complex drug admixtures, particularly in intensive care and oncology settings where material stability and patient safety are critical. - Are Non-PVC IV bags more expensive than conventional PVC bags?

Although unit costs may be slightly higher than PVC alternatives, overall value is enhanced through reduced adverse reactions, lower regulatory risk, improved shelf stability, and long-term cost savings associated with better clinical outcomes. - What factors are driving the growth of the Non-PVC IV bags market?

The non-PVC IV bags market is driven by rising hospital admissions, growth in chronic diseases, increasing chemotherapy usage, and stringent regulations on PVC materials, resulting in steady adoption across developed and emerging healthcare systems. - What materials dominate the Non-PVC IV bags market?

Market offerings primarily include polypropylene, ethylene vinyl acetate, and multilayer polyolefin bags, with manufacturers focusing on advanced film technologies, enhanced barrier properties, and compatibility with automated compounding and infusion systems. - Which regions show the strongest demand for Non-PVC IV bags?

North America and Europe lead adoption due to strict safety regulations, while Asia-Pacific shows the fastest growth, supported by expanding healthcare infrastructure, rising medical spending, and increasing awareness of non-PVC medical packaging benefits. - How is the competitive landscape of the Non-PVC IV bags market structured?

The market is moderately consolidated, characterized by multinational medical device companies investing in capacity expansion, sustainability initiatives, and product innovation, while regional players compete through cost efficiency and hospital-focused supply agreements.

Conclusion

The Non-PVC IV bags market is experiencing sustained growth, driven by increasing emphasis on patient safety, regulatory compliance, and environmental sustainability. The shift away from DEHP-containing PVC materials toward safer alternatives such as EVA, PP, and PE has strengthened clinical outcomes, particularly in oncology, neonatal care, and long-term infusion therapies.

Strong adoption in North America, combined with rapid expansion across Asia Pacific, highlights the global acceptance of non-PVC solutions. Despite certain operational challenges, ongoing material innovation and technological advancements are expected to enhance product performance, positioning non-PVC IV bags as a critical component of modern infusion therapy systems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)