Table of Contents

Overview

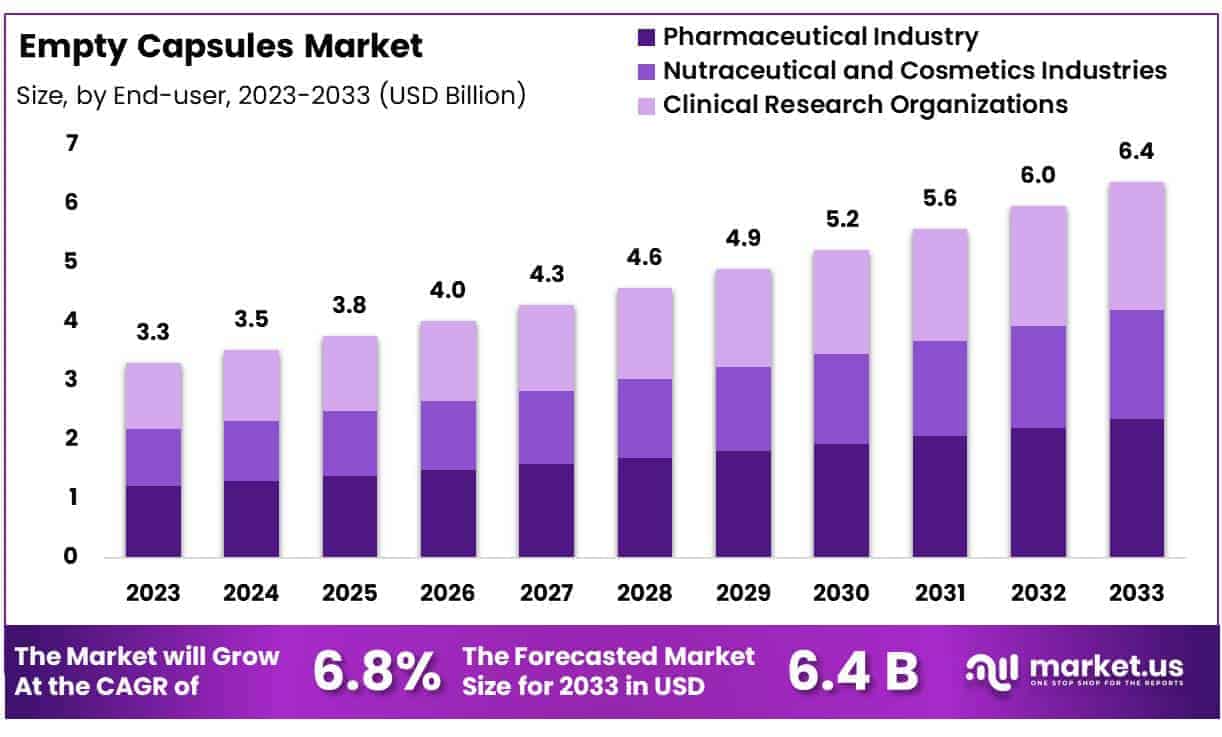

New York, NY – Oct 20, 2025 – Global Empty Capsules Market size is expected to be worth around USD 6.4 Billion by 2033 from USD 3.5 Billion in 2024, growing at a CAGR of 6.8% during the forecast period from 2025 to 2033.

The Empty Capsules Market represents a crucial segment of the pharmaceutical and nutraceutical industries, facilitating precise dosage delivery and enhanced bioavailability of active ingredients. Empty capsules, typically made of gelatin or hydroxypropyl methylcellulose (HPMC), are widely used for encapsulating powders, granules, and liquids across various therapeutic applications.

The market’s growth is driven by rising health awareness, increasing demand for dietary supplements, and the growing preference for personalized medicine. The shift toward plant-based and vegetarian capsules has further accelerated adoption among consumers seeking cleaner, non-animal-derived products. Additionally, pharmaceutical companies increasingly favor empty capsules due to their ease of formulation, faster disintegration, and improved patient compliance.

Technological advancements in capsule manufacturing, such as innovative filling machines and high-quality polymer materials, are enhancing product performance and production efficiency. Regulatory support for nutraceuticals and the expansion of contract manufacturing organizations (CMOs) are also contributing to market expansion globally.

The global Empty Capsules Market is expected to witness significant growth over the coming years, driven by increasing capsule-based drug delivery innovations and growing investments in healthcare infrastructure. As the pharmaceutical sector continues to evolve, empty capsules will remain essential in ensuring precision, safety, and consumer preference within modern drug and supplement formulations.

Key Takeaways

- Market Size: Global Empty Capsules Market size is expected to be worth around USD 6.4 Billion by 2033 from USD 3.5 Billion in 2024, growing at a CAGR of 6.8% during the forecast period from 2025 to 2033.

- By Product Type: In 2023, non-gelatin capsules dominated the market, accounting for an impressive 79% share, driven by rising consumer preference for vegetarian, plant-based, and allergen-free capsule formulations.

- By Capsule Size: The market exhibited a clear inclination toward “Size 0” capsules, which held a 23% share in 2023, reflecting their widespread use in pharmaceutical and nutraceutical dosage applications.

- By End Use: The pharmaceutical industry led the market in 2023 with a 37% share, attributed to the increasing adoption of capsule-based drug formulations for enhanced bioavailability and patient compliance.

- By Region: North America emerged as the leading regional market, contributing 40% of global revenue in 2023, supported by strong pharmaceutical manufacturing capabilities and advanced healthcare infrastructure.

- Market Dynamics: Leading players are focusing on research and development (R&D), expanding global distribution networks, and pursuing strategic mergers and acquisitions to strengthen market presence and sustain long-term growth.

- Regulatory Environment: Stringent regulatory frameworks in regions such as North America and Europe ensure product safety and quality, presenting both operational challenges and growth opportunities for market participants.

Segmentation Analysis

Product Analysis:

In 2023, non-gelatin capsules accounted for 79% of the global empty capsules market, reflecting the growing consumer inclination toward plant-based and allergen-free alternatives. These capsules, primarily produced from hydroxypropyl methylcellulose (HPMC), cater to vegan and vegetarian preferences and align with the increasing demand for clean-label and sustainable formulations.

The gradual decline in gelatin capsule usage is largely influenced by ethical, dietary, and health-related considerations. This shift highlights a significant transformation within the pharmaceutical and nutraceutical industries, driving continuous innovation in non-gelatin capsule technologies and environmentally responsible production methods.

Capsule Analysis:

The “Size 0” capsules led the market in 2023, capturing a 23% share, owing to their optimal fill capacity, convenience, and ease of ingestion. Larger variants such as “Size 000” are preferred for high-dose supplement formulations, while “Size 00” remains a staple for daily nutritional intake.

Smaller capsule sizes, ranging from “Size 1” to “Size 5,” serve specialized applications, including pediatric and therapeutic uses. This wide range of capsule sizes allows manufacturers to cater effectively to diverse dosage requirements and consumer preferences, enhancing flexibility across both pharmaceutical and nutraceutical product lines.

End-Use Analysis:

The pharmaceutical industry dominated the market in 2023 with a 37% share, driven by the widespread use of capsules in efficient and controlled drug delivery systems. The nutraceutical sector also demonstrated strong growth, supported by increasing consumer awareness of preventive healthcare and dietary supplementation.

Beyond these, the cosmetics industry leverages capsule technology to encapsulate and protect active ingredients in skincare and beauty formulations. Furthermore, Clinical Research Organizations (CROs) utilize capsules extensively in clinical trials to ensure precise dosing, compliance, and reliability, reinforcing their critical role in drug development and regulatory validation.

Regional Analysis

In 2023, North America emerged as the dominant region in the global empty capsules market, accounting for a notable 40% share. This leadership is primarily driven by the region’s advanced healthcare infrastructure, high per capita healthcare expenditure, and the strong presence of major pharmaceutical and nutraceutical manufacturers.

Market growth across North America is further supported by rising consumer demand for dietary supplements and an increasing emphasis on preventive healthcare practices. Moreover, the region’s strict regulatory framework ensures superior product quality, safety, and compliance, reinforcing its competitive advantage. These factors collectively strengthen North America’s position as a key hub for innovation and development within the global empty capsules market.

Frequently Asked Questions on Empty Capsules

- What are empty capsules?

Empty capsules are small, shell-like containers used to encase powders, granules, or liquids for oral consumption. They are made from gelatin or plant-based materials and serve as an efficient drug and supplement delivery system. - What materials are used to make empty capsules?

Empty capsules are typically made from gelatin, derived from animal collagen, or non-gelatin materials such as hydroxypropyl methylcellulose (HPMC) and pullulan, which cater to vegetarian and vegan consumers seeking plant-based alternatives. - What are the main types of empty capsules?

The two primary types of empty capsules are hard capsules, used for dry powders and granules, and soft capsules, designed for oils and liquids. Hard capsules are widely preferred for pharmaceuticals and dietary supplements. - Which industries use empty capsules the most?

The pharmaceutical and nutraceutical industries are the largest users of empty capsules, followed by cosmetics and functional food sectors. They are utilized to ensure accurate dosage, improved bioavailability, and enhanced patient compliance. - Which type of capsule dominates the market?

In 2023, non-gelatin capsules held a dominant 79% market share, reflecting the growing consumer shift toward plant-based and allergen-free formulations, particularly in nutraceutical and health supplement applications. - What capsule size is most commonly used?

The “Size 0” capsules are the most widely used, accounting for 23% of the market in 2023, due to their balanced capacity, easy swallowing, and suitability for both pharmaceutical and dietary supplement formulations. - Which region leads the global empty capsules market?

North America leads the global market with a 40% share in 2023, supported by strong pharmaceutical manufacturing, advanced R&D facilities, and increasing demand for high-quality health and wellness products. - How do regulations impact the empty capsules industry?

Regulatory authorities such as the FDA and EMA enforce strict standards to ensure capsule safety, quality, and consistency. Compliance with these standards enhances consumer trust but increases production and testing costs for manufacturers.

Conclusion

The global Empty Capsules Market continues to gain momentum, driven by the rising demand for dietary supplements, advanced drug delivery systems, and increasing preference for plant-based formulations. Technological advancements, strong R&D initiatives, and expanding healthcare infrastructure are enhancing product innovation and market penetration.

North America remains a dominant force due to its robust pharmaceutical base and stringent regulatory standards. As the industry moves toward personalized and preventive healthcare, empty capsules are expected to remain integral in ensuring precision, safety, and efficiency in modern drug formulation and nutraceutical applications, supporting sustainable long-term market growth.