Table of Contents

Overview

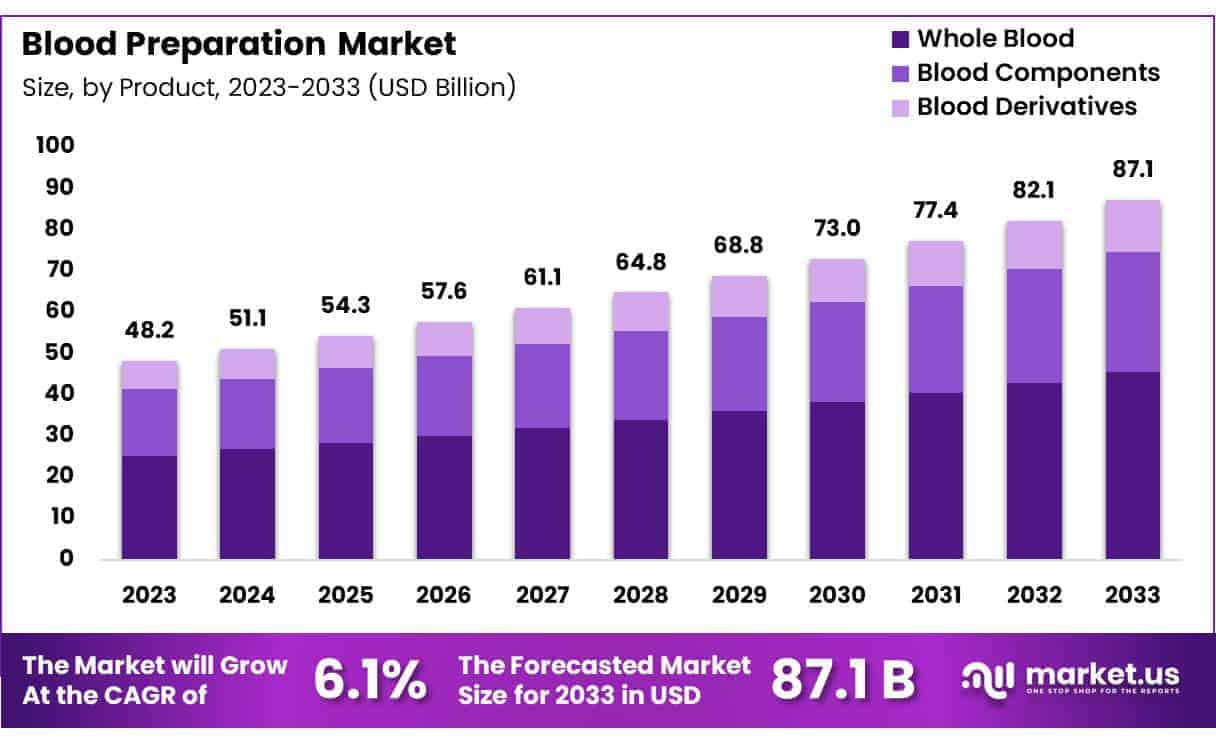

New York, NY – May 12, 2025 – Global Blood Preparation Market size is expected to be worth around US$ 87.1 billion by 2033 from US$ 48.2 billion in 2023, growing at a CAGR of 6.1% during the forecast period 2024 to 2033.

The blood preparation market plays a crucial role in supporting a wide range of medical procedures, emergency care, and chronic disease management. Blood products such as whole blood, red blood cells, plasma, and platelets are essential for transfusions in surgeries, trauma care, and the treatment of various hematological conditions.

The growing demand for effective blood management has led to increased focus on safe collection, processing, and storage techniques. Whole blood is commonly used in hospitals for immediate transfusions, while individual components are often separated to treat specific conditions more efficiently.

Anticoagulants and antithrombotic agents are widely used in the preparation of blood to prevent clotting during storage and transfusion. These agents also support therapeutic applications in managing blood clot-related disorders.

Hospitals and clinics represent the primary end-users of blood preparation products, with ongoing efforts to maintain adequate blood supplies and improve transfusion safety. Advancements in storage technologies, blood screening methods, and public awareness campaigns about blood donation are further strengthening the reliability of blood services.

Regionally, demand for blood preparation is growing across both developed and developing healthcare systems, driven by improvements in emergency medical care, surgical capacity, and public health initiatives. The market continues to evolve with the ongoing development of innovative preservation methods and regulatory standards aimed at ensuring quality and safety.

Key Takeaways

- Market Overview: The global blood preparation market is projected to reach approximately USD 87.1 billion by 2033, rising from USD 48.2 billion in 2023, and expanding at a compound annual growth rate (CAGR) of 6.1% during the forecast period from 2024 to 2033.

- Product Segment Insights: In 2023, the whole blood segment accounted for the largest share at 52.3%, primarily driven by the rising demand for blood transfusions in emergency and critical care settings.

- Therapeutic Class Analysis: Among antithrombotic and anticoagulant products, the anticoagulants segment held a dominant share of 54.8%, supported by the increasing global burden of thromboembolic disorders such as deep vein thrombosis and pulmonary embolism.

- Application Analysis: The thrombocytosis segment demonstrated robust growth, capturing a 40.8% revenue share in 2023, due to higher detection rates and treatment demand for elevated platelet conditions.

- End-Use Analysis: Hospitals emerged as the leading end-use segment, contributing 60.7% of total market revenue, attributed to the widespread administration of blood components and therapies in inpatient settings.

- Regional Outlook: North America led the global market, accounting for a 39.2% revenue share in 2023. This dominance is supported by advanced healthcare infrastructure, high procedural volume, and increased awareness of blood-related therapies.

Segmentation Analysis

- By Product Analysis: In 2023, the whole blood segment led the market with a 52.3% share, driven by its essential use in surgeries, trauma care, and hematological treatments. Increasing road accidents and chronic illnesses have elevated the demand for transfusions. Technological advancements in collection and storage have enhanced safety and availability. Moreover, rising awareness about emergency blood supply needs and expanding hospital donation drives are expected to further support the growth of the whole blood segment.

- By Antithrombotic and Anticoagulants Type Analysis: Anticoagulants dominated with a 54.8% share in 2023, fueled by the rising prevalence of thromboembolic conditions such as stroke, DVT, and pulmonary embolism. Their increasing use in preventive care and clinical protocols, especially among elderly populations, has contributed to robust demand. The emergence of newer, safer anticoagulant therapies and ongoing R\&D aimed at efficacy improvement are likely to strengthen the segment’s growth and reinforce its role in proactive blood-related disorder management.

- By Application Analysis: The thrombocytosis segment recorded a 40.8% revenue share in 2023, driven by growing awareness of complications linked to elevated platelet levels, including cardiovascular risks and pulmonary embolism. The rise in obesity and sedentary lifestyles, key risk factors for thrombocytosis, supports this trend. Additionally, improved diagnostic capabilities have enabled early detection and treatment, encouraging demand for specialized blood preparation solutions. This segment is expected to remain a critical area of focus in thrombotic disease management.

- By End-user Analysis: Hospitals accounted for 60.7% of the market in 2023 due to their central role in providing transfusion services for surgeries, trauma, and chronic disease care. Increasing cases of conditions requiring regular blood transfusions have accelerated demand. The push for better patient outcomes and safer transfusion practices is prompting hospitals to upgrade protocols. Strengthened partnerships with blood banks are also expected to ensure supply continuity, solidifying hospitals as the primary users of blood preparation products.

Market Segments

By Product

- Blood Components

- Whole Blood

- Blood Derivatives

By Antithrombotic Anticoagulants Type

- Fibrinolytics

- Platelet Aggregation Inhibitors

- Anticoagulants

By Application

- Thrombocytosis

- Pulmonary Embolism

- Renal Impairment

- Angina Blood Vessel Complications

- Others

By End-user

- Hospitals

- Research Labs

- Diagnostic Centers

- Blood Banks

Regional Analysis

North America Leads the Blood Preparation Market

North America holds a leading position in the global blood preparation market, supported by robust healthcare infrastructure and a high demand for blood products. The region faces a growing burden of chronic diseases, trauma cases, and surgical interventions, all of which contribute to the increasing need for blood transfusions. Data from the American National Red Cross highlights the ongoing urgency, with blood or platelets needed every few seconds across the United States.

This high demand has spurred the development and adoption of advanced blood processing technologies, which have significantly enhanced the safety, storage, and usability of blood components. Public awareness campaigns and organized donation drives have also played a key role in maintaining adequate blood supplies. Moreover, ongoing research into blood substitutes and regenerative medicine is expected to further strengthen the region’s position in the market.

Asia Pacific Projected to Register the Fastest Growth

The Asia Pacific region is anticipated to witness the highest growth in the blood preparation market over the coming years. A rising population, coupled with increasing cases of chronic illnesses and accidents, has intensified the demand for blood products. According to the Indian Health Ministry, millions of blood units are needed annually to meet the healthcare needs of the population.

Efforts to expand healthcare access, improve blood donation rates, and modernize blood processing techniques are expected to support market growth. Government-led initiatives and investments in healthcare infrastructure are also contributing to the development of more efficient blood collection and preparation systems across the region. As a result, the Asia Pacific market is set to emerge as a key growth engine in the global landscape.

Emerging Trends

- Patient Blood Management (PBM): PBM is an evidence-based approach aiming to optimize the care of patients who might need transfusions. It focuses on minimizing unnecessary transfusions, thereby reducing risks associated with transfusion-related complications and conserving blood resources.

- Pathogen Reduction Technologies (PRTs): To enhance the safety of blood products, PRTs are employed to inactivate a broad spectrum of pathogens in blood components, thereby reducing the risk of transfusion-transmitted infections.

- Cold-Stored Platelets: Traditionally, platelets are stored at room temperature for up to 5 days. However, storing platelets at colder temperatures has been shown to extend their shelf life and improve hemostatic function, particularly beneficial in trauma care settings.

- Digital Platforms for Donor Engagement: The integration of mobile applications and online platforms has streamlined the process of blood donation by facilitating donor recruitment, appointment scheduling, and retention, thereby enhancing the efficiency of blood collection systems.

Use Cases

- Surgical Procedures: Blood transfusions are critical during surgeries to compensate for blood loss. In the United States, approximately 15 million units of whole blood and red blood cells are transfused annually, with a significant portion utilized in surgical settings.

- Trauma Care: Immediate availability of blood components is vital for trauma patients experiencing significant blood loss. Timely transfusions can be life-saving in such emergencies.

- Chronic Anemia Management: Patients with conditions like sickle cell disease or thalassemia often require regular blood transfusions to manage anemia and maintain adequate hemoglobin levels.

- Cancer Treatment: Chemotherapy can lead to decreased blood cell counts, necessitating transfusions of red blood cells or platelets to manage anemia and prevent bleeding complications.

- Obstetric Care: Postpartum hemorrhage is a leading cause of maternal mortality. Access to safe blood transfusions is essential in managing severe bleeding during or after childbirth.

Conclusion

In conclusion, the global blood preparation market is poised for steady growth, driven by the rising demand for transfusions across surgical, trauma, chronic disease, and cancer care settings. Technological advancements in blood processing, improved storage methods, and increased awareness of blood donation are enhancing the safety and efficiency of transfusion practices.

North America leads the market due to its advanced infrastructure, while Asia Pacific is emerging as a high-growth region. With ongoing innovations such as pathogen reduction technologies and patient blood management programs, the market is expected to evolve further, ensuring safer, more effective blood preparation and utilization worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)