Table of Contents

- Introduction

- Editor’s Choice

- Sports Apparel Market Size

- Athleisure Market Size

- Activewear Market Size

- Sports & Swimwear Industry Statistics

- Global Yoga Wear Market Size

- Global Women’s Sportswear Market Size

- Athleisure Sales Statistics

- Athleisure Companies Statistics

- Sports and Swimwear Price Trends

- Demographic Dynamics of Athleisure Consumers

- Consumer Preferences

- Key Investment Trends

- Regulations for Athleisure Products

- Athleisure Product Innovations

- Recent Developments

- Conclusion

- FAQs

Introduction

Athleisure Industry Statistics: The athleisure industry has experienced significant growth due to rising health and fitness trends, the influence of fashion icons, and the expansion of e-commerce.

This sector combines athletic apparel with casual wear, appealing to a diverse demographic that prioritizes comfort and style.

Key product categories include leggings, joggers, sports bras, and sneakers, with major players like Lululemon, Nike, and Adidas leading the market.

Challenges such as sustainability demands, market saturation, and changing consumer preferences necessitate innovation and differentiation strategies.

The future outlook indicates continued growth, particularly in emerging markets. Driven by advancements in fabric technology and the potential integration of smart textiles.

Editor’s Choice

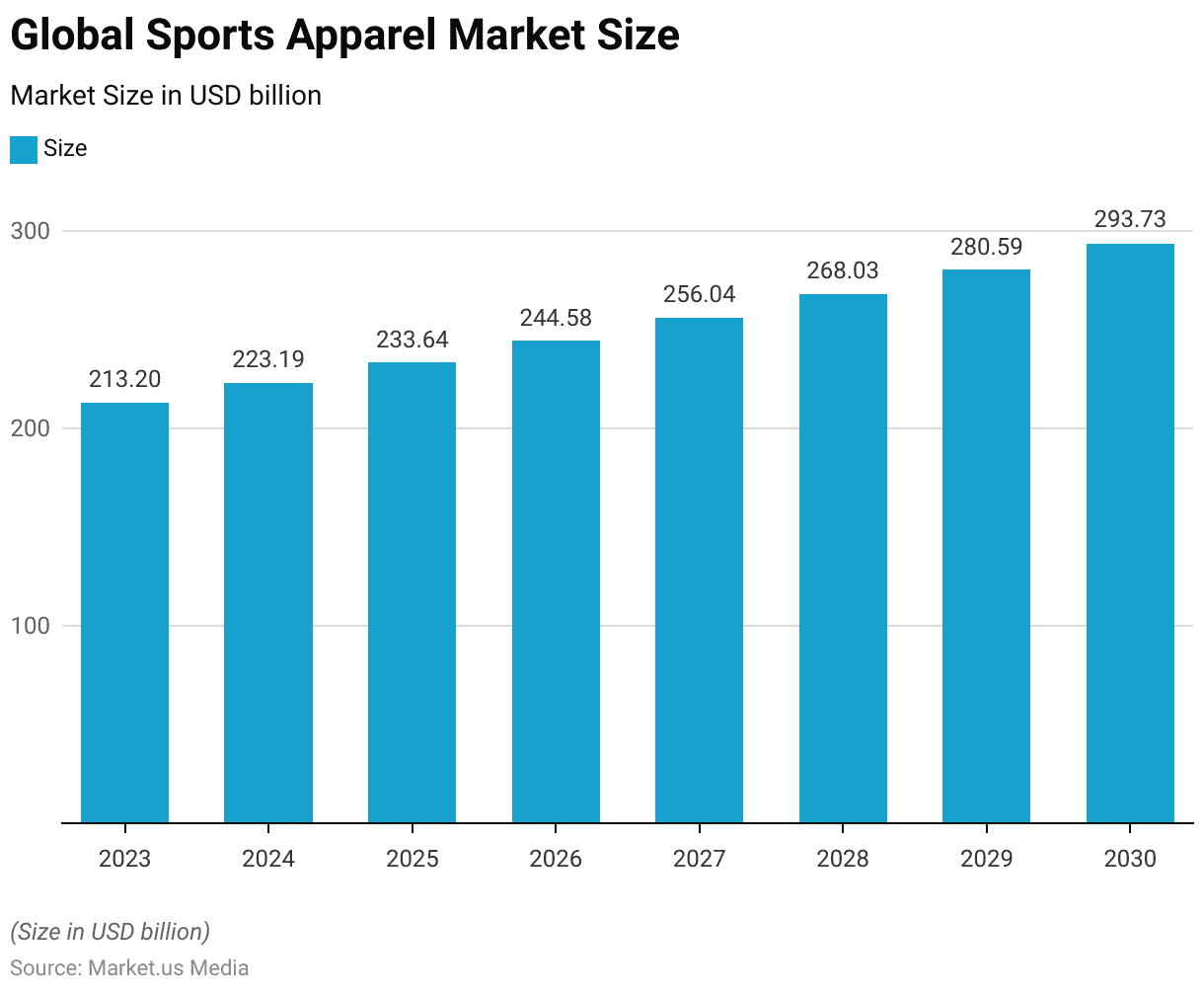

- The global sports apparel market revenue is projected to reach USD 293.73 billion by 2030.

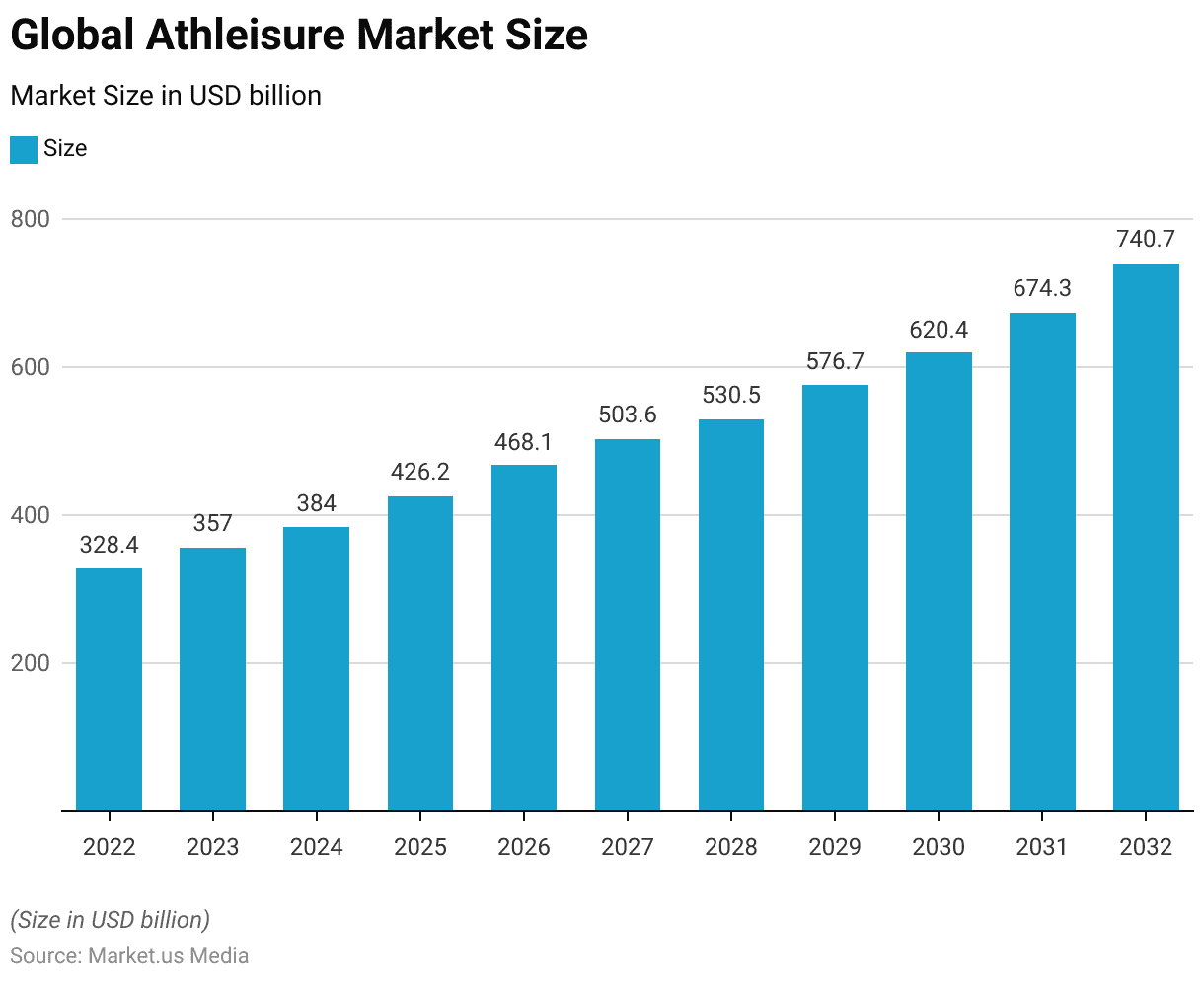

- By 2032, the global athleisure market revenue is expected to reach USD 740.7 billion.

- The global activewear market revenue is projected to reach USD 451.1 billion by 2028.

- By 2028, the global yoga wear market is forecasted to reach a value of USD 39,910 million.

- In 2023, sales figures for the largest athletic apparel, accessories, and footwear companies worldwide showed significant variance, reflecting their market positions and scale. Nike Inc. dominated the industry with the highest sales, amounting to USD 51,542 million.

- In 2023, consumer preferences for athleisure wear brands in the United States showed distinct patterns. Lululemon led the market, with a significant 50% of consumers indicating it as their preferred brand for athleisure purchases.

- In 2016, a survey focusing on the preferences of French women regarding sportswear revealed a distinct hierarchy of criteria they consider when making purchases. Comfort was overwhelmingly the most valued aspect, with 99% of respondents highlighting it as crucial, emphasizing its paramount importance in sportswear selection.

Sports Apparel Market Size

- The global sports apparel market is projected to see a continuous rise in revenue from 2023 through 2030.

- Starting with a market size of USD 213.2 billion in 2023, the sector is expected to grow steadily each year, reaching USD 223.19 billion in 2024.

- By 2025, the market size is anticipated to increase to USD 233.64 billion, followed by a rise to USD 244.58 billion in 2026.

- The growth momentum is expected to be sustained, with the market size reaching USD 256.04 billion in 2027 and USD 268.03 billion by 2028.

- The upward trend is projected to continue, with market sizes of USD 280.59 billion in 2029 and USD 293.73 billion by 2030.

- This consistent growth highlights the increasing consumer interest and investment in sports apparel globally.

(Source: Statista)

Athleisure Market Size

- The global athleisure market has experienced significant growth in recent years at a CAGR of 8.70%, with the market size reaching USD 328.4 billion in 2022.

- This upward trend continued in 2023, with the market expanding to USD 357.0 billion.

- Projections indicate sustained growth in the coming years, with the market expected to reach USD 384.0 billion in 2024, followed by an increase to USD 426.2 billion in 2025.

- By 2026, the market is anticipated to grow to USD 468.1 billion, and by 2027, it will likely reach USD 503.6 billion.

- The market is forecasted to surpass USD 530.5 billion in 2028 and climb to USD 576.7 billion by 2029.

- Moving into the next decade, the market is projected to continue its upward trajectory, reaching USD 620.4 billion in 2030 and further expanding to USD 674.3 billion in 2031.

- By 2032, the global athleisure market is expected to reach an impressive USD 740.7 billion.

(Source: market.us)

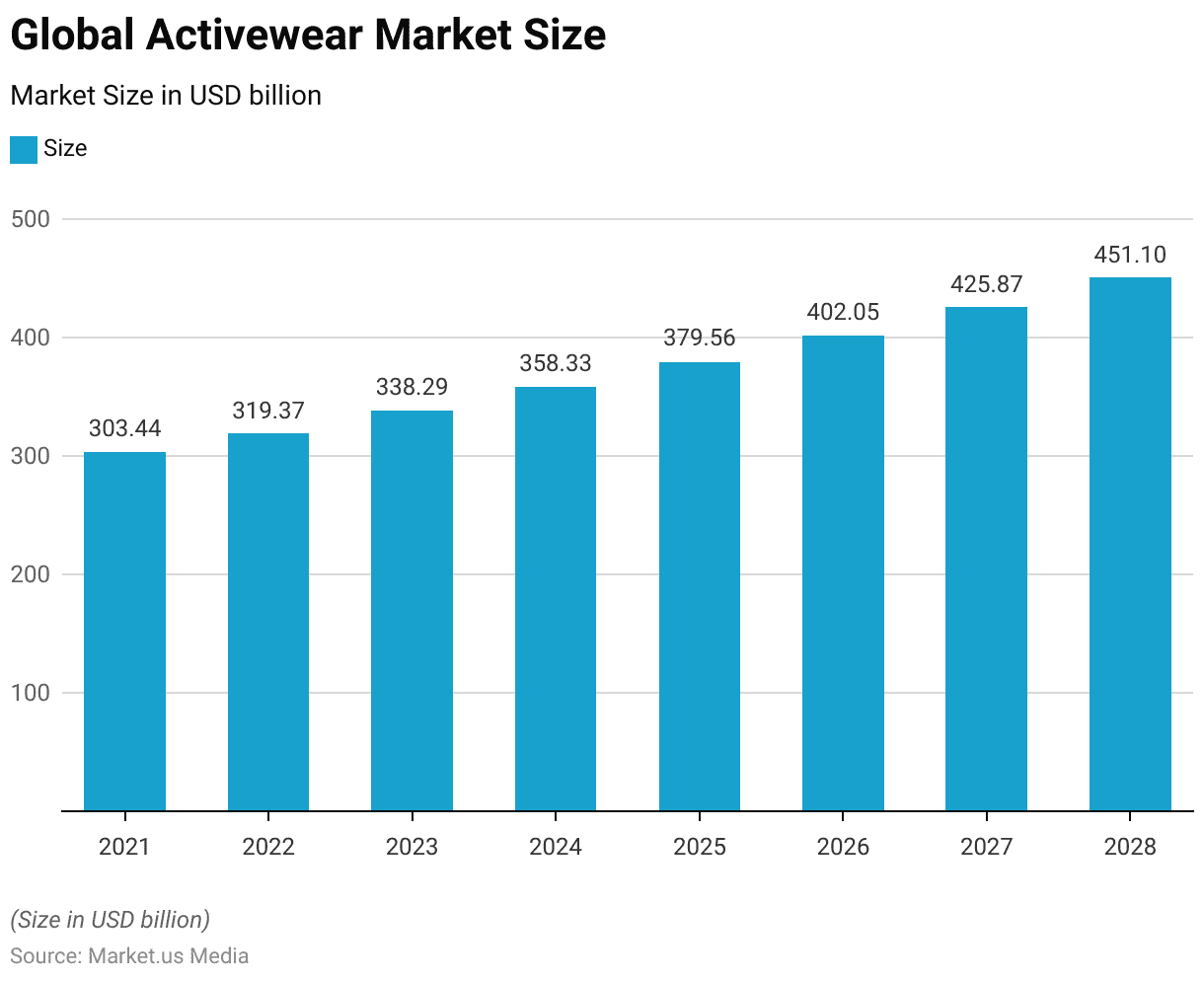

Activewear Market Size

- The global activewear market has shown a steady upward trajectory from 2021 to 2028.

- In 2021, the market was valued at USD 303.44 billion, and it grew to USD 319.37 billion in 2022.

- The trend of growth continued, with the market size reaching USD 338.29 billion in 2023, and it is projected to expand to USD 358.33 billion by 2024.

- By 2025, the market is expected to further increase to USD 379.56 billion.

- The upward trend is set to continue, with market values projected at USD 402.05 billion in 2026, USD 425.87 billion in 2027, and ultimately reaching USD 451.1 billion by 2028.

- This sustained growth underscores the increasing consumer demand and broadening acceptance of activewear products globally.

(Source: Statista)

Sports & Swimwear Industry Statistics

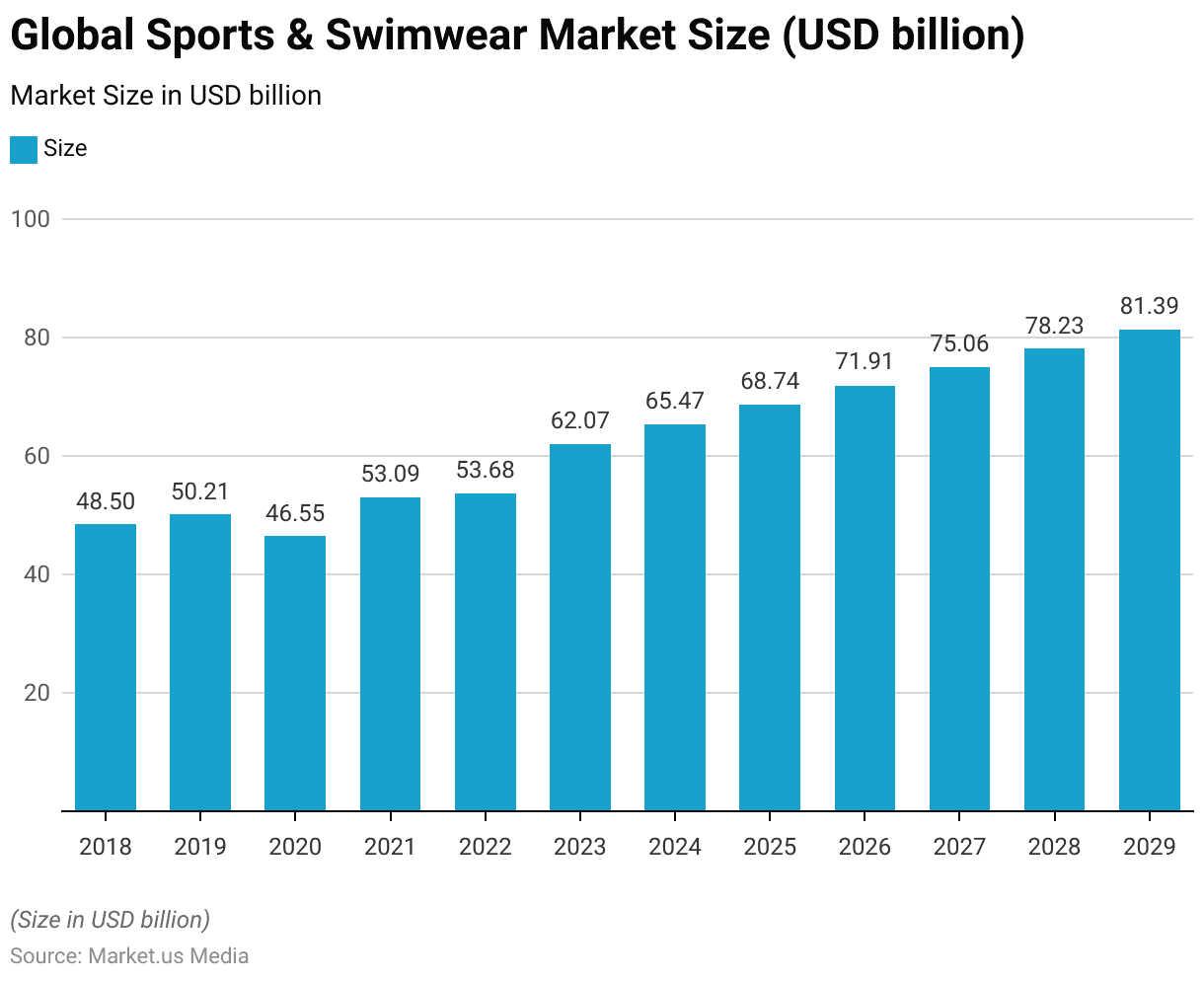

Global Sports & Swimwear Market Size

- The global sports and swimwear market has demonstrated a fluctuating yet overall upward trend in market size from 2018 through 2029.

- In 2018, the market was valued at USD 48.50 billion. It experienced growth in 2019, reaching USD 50.21 billion, before declining in 2020 to USD 46.55 billion, likely impacted by global economic challenges.

- A strong recovery was observed in 2021, with the market size increasing to USD 53.09 billion, followed by a slight rise to USD 53.68 billion in 2022.

- Substantial growth occurred in 2023, with the market size escalating to USD 62.07 billion.

- This growth trajectory is expected to continue, with the market projected to reach USD 65.47 billion in 2024, USD 68.74 billion in 2025, USD 71.91 billion in 2026, USD 75.06 billion in 2027, USD 78.23 billion in 2028, and USD 81.39 billion by 2029.

- This progression highlights the enduring appeal and increasing market demand for sports and swimwear globally.

(Source: Statista)

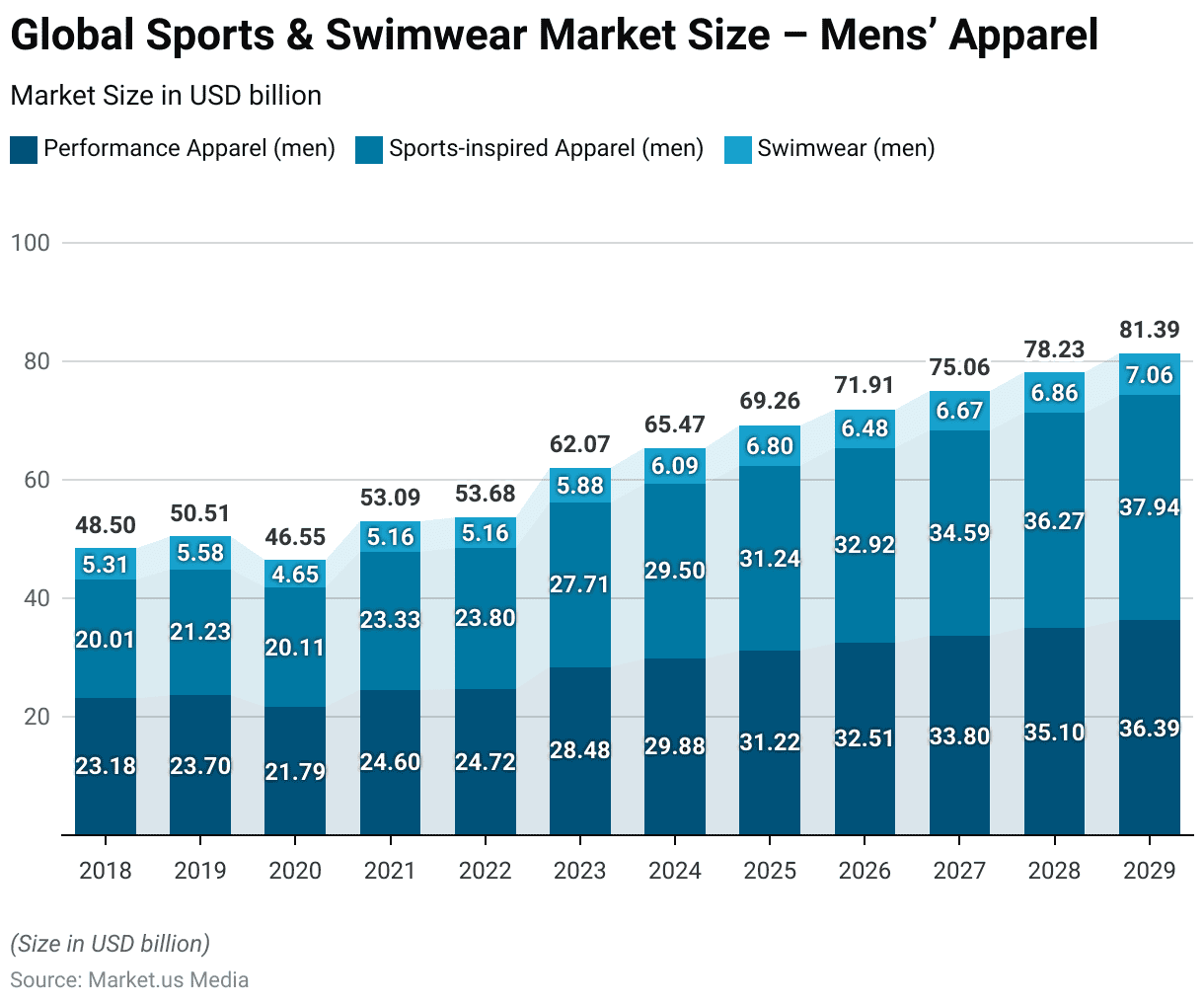

Global Sports & Swimwear Market Size – Men’s Apparel

2018-2022

- The global sports and swimwear market, segmented by type into performance apparel, sports-inspired apparel, and swimwear for men, has seen varied growth from 2018 to 2022.

- In 2018, the performance apparel segment stood at USD 23.18 billion, sports-inspired apparel at USD 20.01 billion, and swimwear at USD 5.31 billion.

- By 2019, these segments had slightly increased to USD 23.70 billion, USD 21.23 billion, and USD 5.58 billion, respectively.

- A decrease was observed in 2020, with performance apparel falling to USD 21.79 billion, sports-inspired apparel to USD 20.11 billion, and swimwear to USD 4.65 billion.

- The market rebounded in 2021, with performance apparel reaching USD 24.60 billion, sports-inspired apparel climbing to USD 23.33 billion, and swimwear recovering to USD 5.16 billion.

- This recovery trend continued through 2022, maintaining similar levels.

2023-2029

- Substantial growth was recorded in 2023, with performance apparel reaching USD 28.48 billion, sports-inspired apparel reaching USD 27.71 billion, and swimwear increasing to USD 5.88 billion.

- From 2024 onwards, consistent growth is projected across all segments.

- By 2024, performance apparel is expected to reach USD 29.88 billion, sports-inspired apparel USD 29.50 billion, and swimwear USD 6.09 billion.

- This upward trend is anticipated to continue, with performance apparel projected to reach USD 36.39 billion, sports-inspired apparel USD 37.94 billion, and swimwear USD 7.06 billion by 2029.

- The data indicates a robust expansion in all categories, emphasizing the growing market demand for men’s sports and swimwear products.

(Source: Statista)

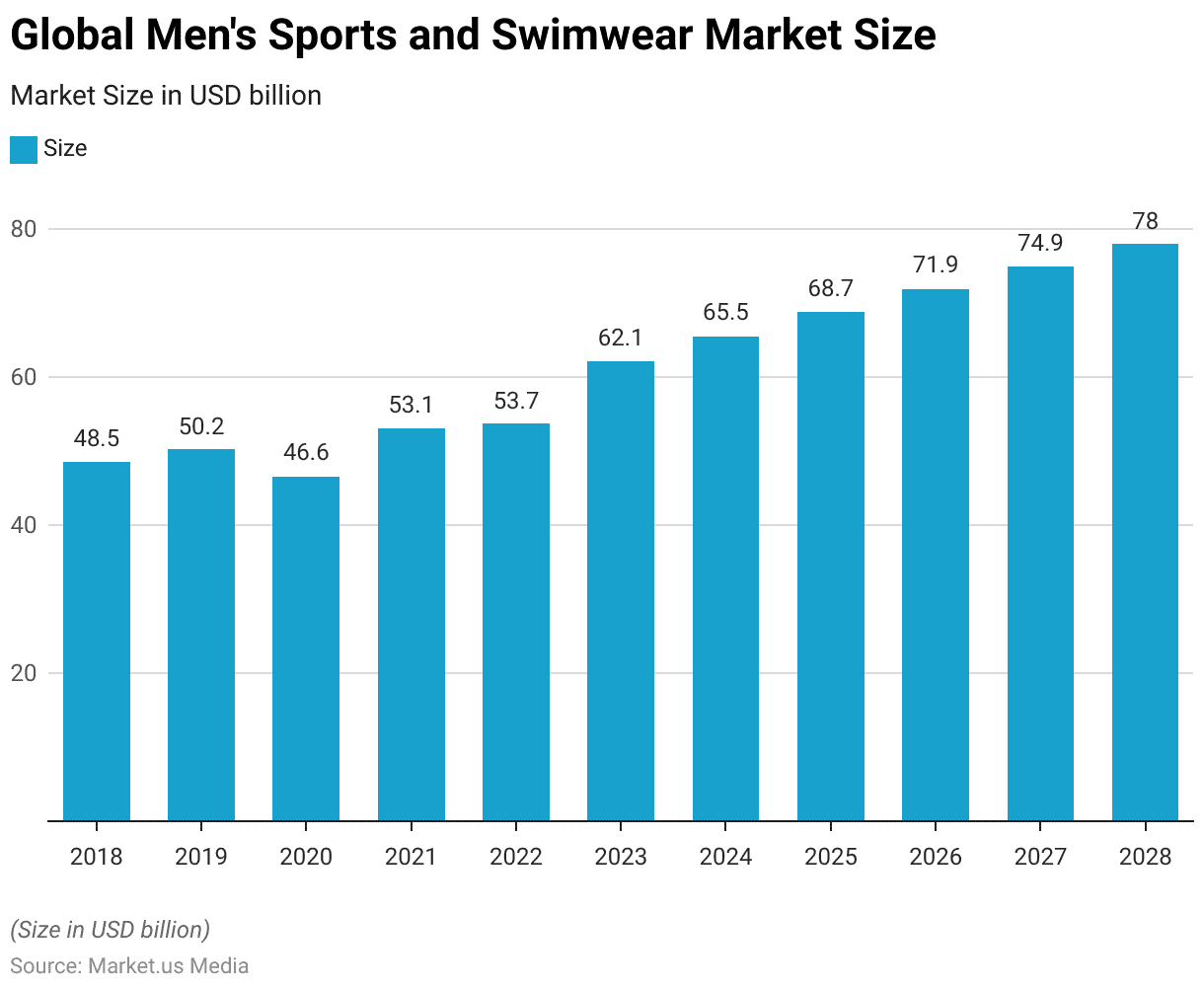

Global Men’s Sports and Swimwear Market Size

- The global men’s sports and swimwear market has exhibited fluctuating yet generally upward-moving revenue trends from 2018 to 2028.

- Starting with a revenue of USD 48.5 billion in 2018, the market experienced a slight increase to USD 50.21 billion in 2019.

- However, in 2020, revenue dipped to USD 46.55 billion, likely due to external market disruptions.

- A recovery was evident in 2021 as revenues rose to USD 53.1 billion and slightly increased to USD 53.67 billion in 2022.

- A significant growth trajectory began in 2023, with revenue jumping to USD 62.07 billion, followed by further growth to USD 65.46 billion in 2024.

- The upward trend continued, with revenues reaching USD 68.74 billion in 2025, USD 71.9 billion in 2026, and USD 74.91 billion in 2027, and projections indicate it will reach USD 77.97 billion by 2028.

- This pattern underscores a resilient and expanding market segment, with increasing consumer interest and investment in men’s sports and swimwear products.

(Source: Statista)

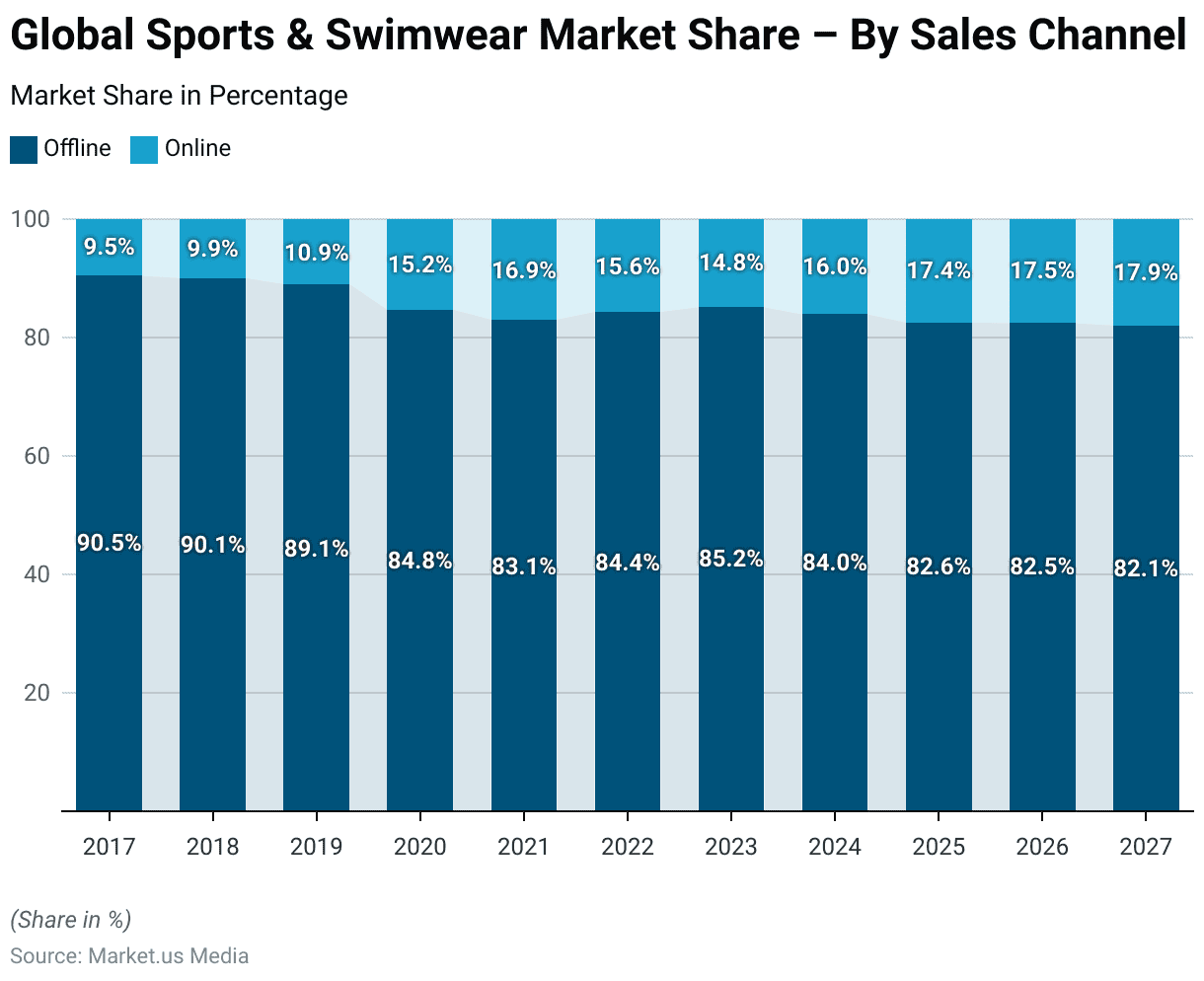

Global Sports & Swimwear Market Share – By Sales Channel

2017-2022

- The distribution of market share between offline and online sales channels in the global sports and swimwear market has shown a noticeable trend towards increased online purchases from 2017 to 2022.

- In 2017, the market was heavily dominated by offline sales, accounting for 90.5% of the total, with online sales making up only 9.5%.

- This dynamic began shifting gradually; by 2018, offline sales decreased slightly to 90.1%, while online sales increased to 9.9%.

- The trend continued in 2019, with offline sales decreasing further to 89.1% and online sales climbing to 10.9%.

- A significant shift occurred in 2020 when the offline market share dropped to 84.8%, accompanied by a rise in online sales to 15.2%, likely influenced by global events that year.

- By 2021, offline sales decreased to 83.1%, and online sales increased to 16.9%.

- There was a slight rebound in offline sales in 2022 to 84.4%, with online sales adjusting to 15.6%.

2023-2027

- However, in 2023, offline sales slightly increased again to 85.2%, with online sales decreasing to 14.8%.

- The trend towards increased online sales resumed in 2024, when online sales were projected to increase to 16%, with offline sales at 84%.

- By 2025, online sales were expected to rise to 17.4%, while offline sales were projected to drop to 82.6%.

- This pattern was anticipated to continue, with online sales reaching 17.5% in 2026 and further rising to 17.9% by 2027, while offline sales were expected to decrease correspondingly.

- This shift illustrates a growing consumer preference for online shopping in the sports and swimwear market, reflecting broader digital transformation trends in retail.

(Source: Statista)

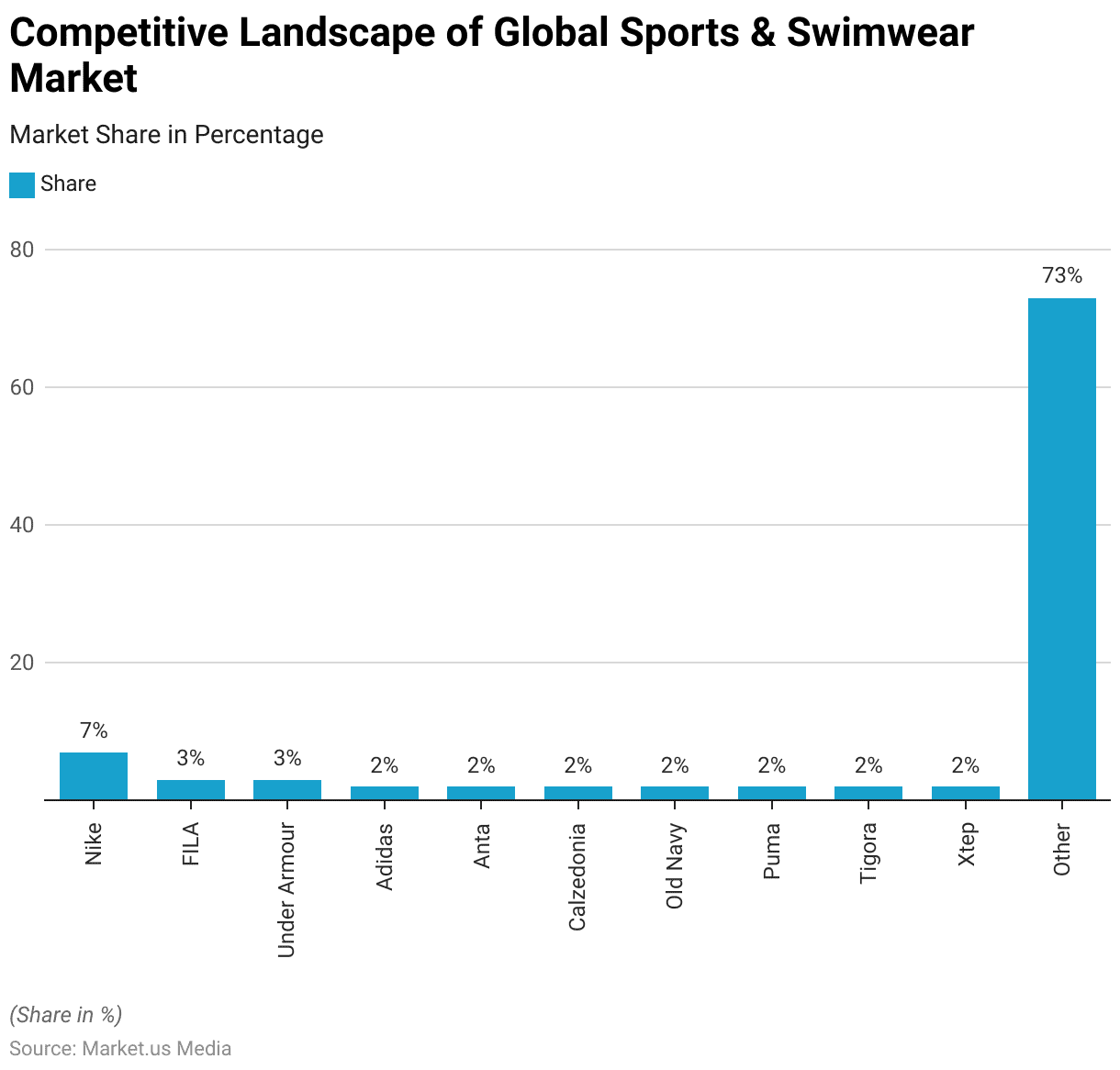

Competitive Landscape of Global Sports & Swimwear Market

- The competitive landscape of the global sports and swimwear market is characterized by a significant diversity of participants, with a large portion of the market composed of various smaller companies.

- Nike leads the market with a 7% share, indicating its dominant position in the industry.

- Following Nike, FILA and Under Armour each hold a 3% market share, reflecting their strong presence in the market. Adidas, Anta, Calzedonia, Old Navy, Puma, Tigora, and Xtep each have a 2% share, showcasing a fairly fragmented market with several players competing closely.

- The “Other” category, which includes numerous smaller and niche companies, collectively holds a substantial majority of the market, accounting for 73%.

- This high percentage highlights the extensive fragmentation and competition within the global sports and swimwear market, where no single company commands overwhelming market control.

(Source: Statista)

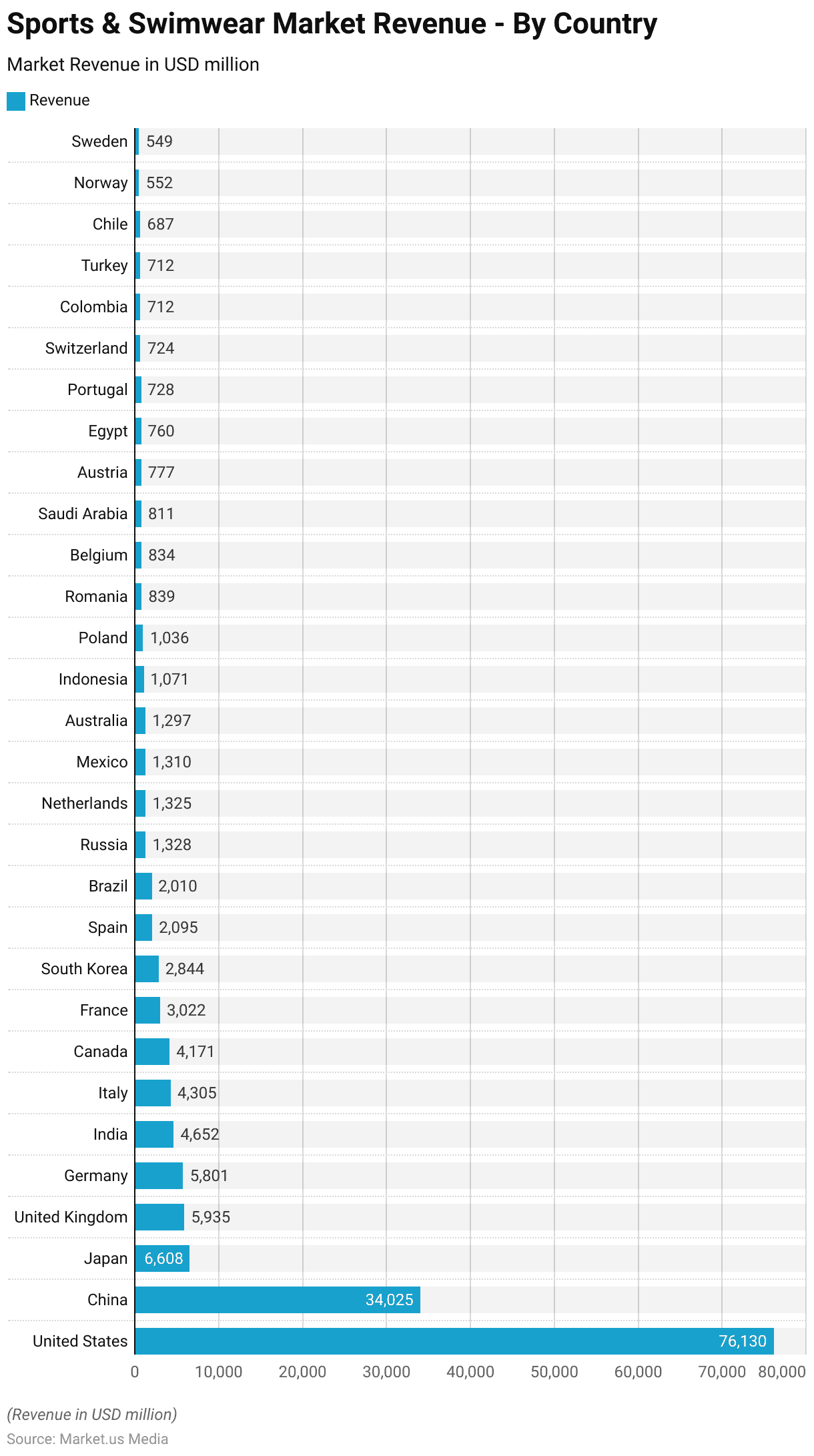

Sports & Swimwear Market Revenue – By Country

- In 2023, the revenue of the global sports and swimwear market displayed significant geographical disparities. The United States led with a substantial revenue of USD 76,130 million, underscoring its dominant market position.

- China followed as the second largest market, generating USD 34,025 million. Japan and the United Kingdom also held significant shares, with revenues of USD 6,608 million and USD 5,935 million, respectively.

- Germany contributed USD 5,801 million, closely aligning with the market sizes of other major European economies.

- India’s market size stood at USD 4,652 million, followed by Italy with USD 4,305 million, and Canada at USD 4,171 million.

- France and South Korea further exemplified robust markets in Europe and Asia with revenues of USD 3,022 million and USD 2,844 million, respectively.

- Spain and Brazil also showed notable market sizes of USD 2,095 million and USD 2,010 million, respectively.

- Countries like Russia, the Netherlands, Mexico, and Australia showed smaller yet substantial market revenues ranging from USD 1,328 million to USD 1,297 million. Emerging markets such as Indonesia and Poland contributed over USD 1,000 million each.

- Other countries, including Romania, Belgium, Saudi Arabia, Austria, Egypt, Portugal, Switzerland, Colombia, Turkey, Chile, Norway, and Sweden, though smaller in market size, demonstrated the widespread global reach and consumer interest in sports and swimwear, each contributing under USD 1,000 million to the market in 2023.

- This diverse revenue distribution highlights varying consumer behaviors and market penetration across different regions.

(Source: Statista)

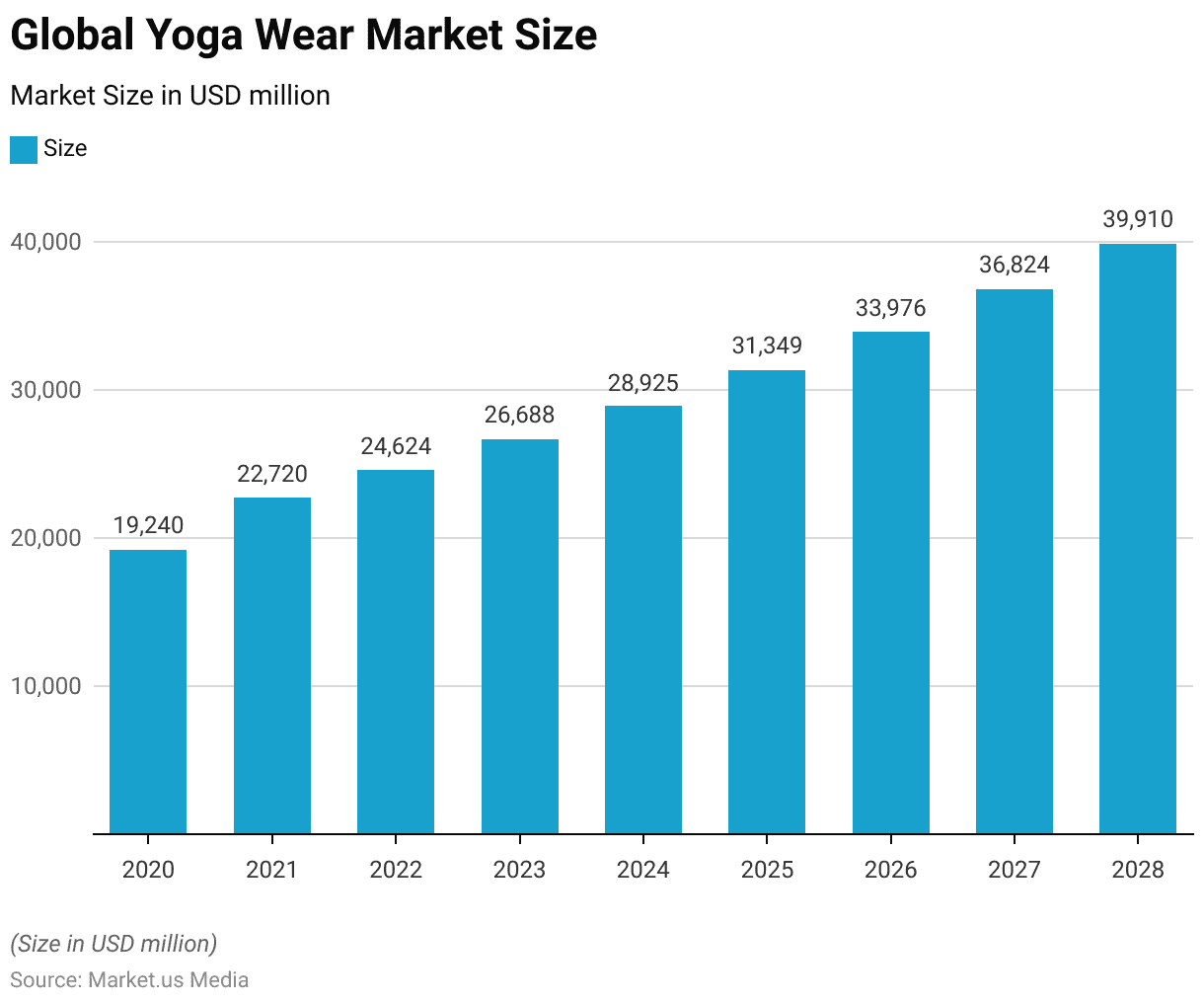

Global Yoga Wear Market Size

- The global yoga wear market has seen a notable increase in value from 2020 to 2028.

- In 2020, the market was valued at USD 19,240 million.

- By 2021, it had grown significantly to USD 22,720 million, reflecting the rising popularity of yoga and increased consumer interest in yoga apparel.

- The upward trend continued, with the market size reaching USD 24,624 million in 2022.

- Further growth was observed in 2023, with the market size expanding to USD 26,688 million.

- The market is projected to maintain this growth momentum, increasing to USD 28,925 million in 2024 and then to USD 31,349 million in 2025.

- By 2026, the market is expected to grow to USD 33,976 million, followed by an increase to USD 36,824 million in 2027.

- By 2028, the global yoga wear market is forecasted to reach a value of USD 39,910 million.

- This steady growth trajectory highlights the enduring appeal of yoga as a wellness activity and the corresponding consumer demand for specialized apparel.

(Source: Statista)

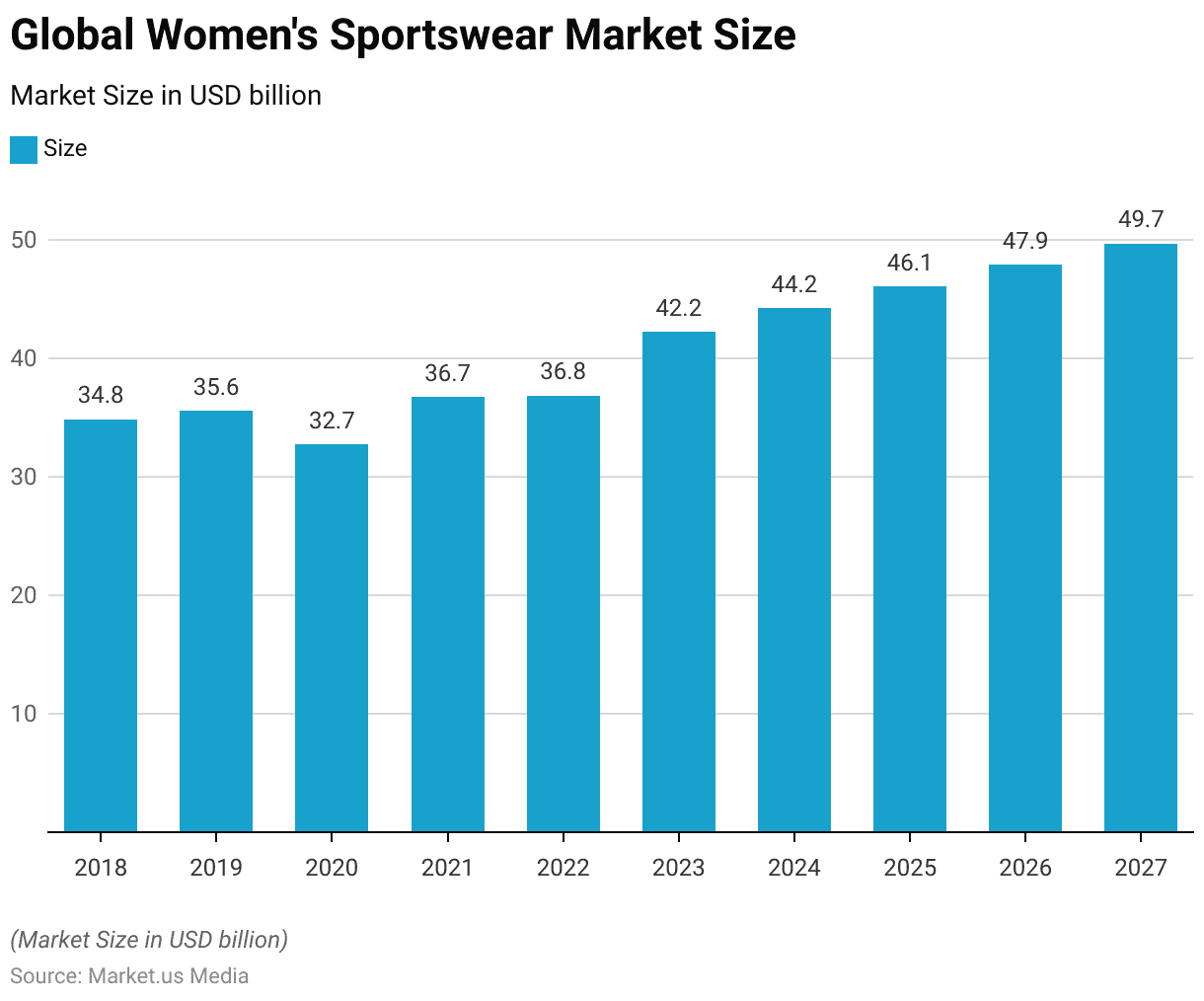

Global Women’s Sportswear Market Size

- The global women’s performance sports apparel market has displayed notable trends over the period from 2018 to 2027.

- Initially, the market size stood at USD 34.82 billion in 2018 and saw a modest increase to USD 35.55 billion in 2019.

- A downturn occurred in 2020 when the market size decreased to USD 32.73 billion, likely affected by global economic conditions.

- However, the market rebounded to USD 36.7 billion in 2021 and maintained a similar level at USD 36.81 billion in 2022.

- From 2023 onwards, significant growth was observed as the market size escalated to USD 42.24 billion, and it is projected to continue its upward trajectory, reaching USD 44.21 billion in 2024.

- Further increments are expected, with the market size growing to USD 46.1 billion in 2025, USD 47.92 billion in 2026, and culminating at USD 49.67 billion by 2027.

- This consistent growth underscores the increasing demand and popularity of women’s performance sports apparel globally.

(Source: Statista)

Athleisure Sales Statistics

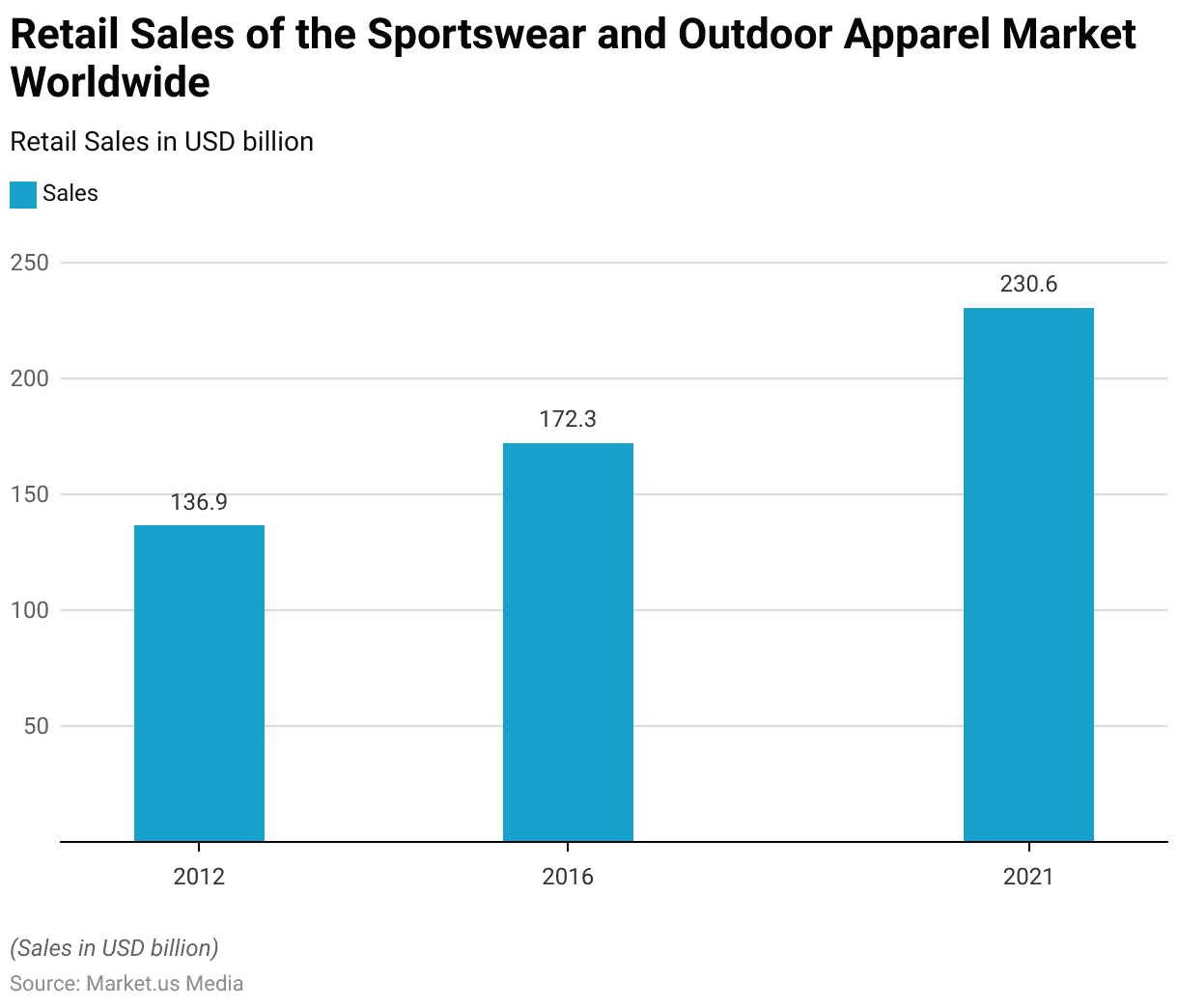

Retail Sales of the Sportswear and Outdoor Apparel Market Worldwide

- From 2012 to 2021, the retail sales of the sportswear and outdoor apparel market worldwide exhibited a substantial growth trajectory.

- In 2012, the market’s retail sales were valued at USD 136.9 billion.

- Over the following four years, the market experienced notable growth, culminating in retail sales of USD 172.3 billion by 2016.

- This upward trend persisted, and by 2021, the market had further expanded to reach a value of USD 230.6 billion.

- This significant increase over nearly a decade highlights the growing consumer demand and expanding market presence of sportswear and outdoor apparel globally.

(Source: Statista)

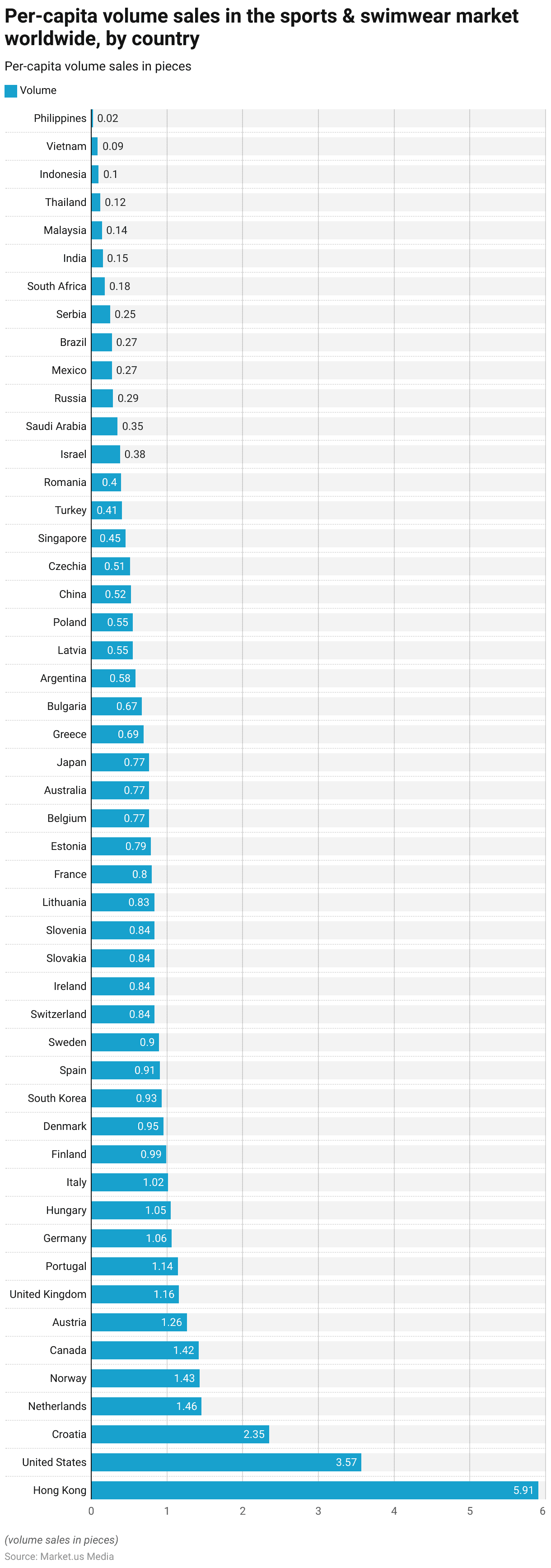

Per-capita Volume Sales in The Sports & Swimwear Market Worldwide – By Country

- In 2023, per-capita volume sales in the sports and swimwear market displayed considerable variation across different countries. Hong Kong led the way with the highest per-capita volume at 5.91 pieces, significantly ahead of other regions.

- The United States followed with a per-capita volume of 3.57 pieces. In Europe, Croatia reported a notable figure of 2.35 pieces, while the Netherlands and Norway had per-capita sales of 1.46 and 1.43 pieces, respectively. Canada was close behind with 1.42 pieces per capita.

- In Western Europe, countries like Austria, the United Kingdom, Portugal, Germany, and Italy showed per-capita volumes ranging from 1.26 pieces in Austria to 1.02 pieces in Italy.

- Other European nations, including Hungary, Finland, Denmark, and Spain, also reported per-capita volumes close to one piece, reflecting moderate consumption rates.

- Lower down the scale, countries like Sweden, Switzerland, Ireland, Slovakia, Slovenia, and Lithuania had per-capita volumes ranging from 0.84 to 0.9 pieces. France, Estonia, Belgium, Australia, and Japan reported even lower figures, all below 0.8 pieces per capita.

- Eastern European and Mediterranean countries like Greece and Bulgaria, along with Argentina and Latvia in other regions, showed per-capita volumes under 0.7 pieces.

- Major Asian markets such as China, Singapore, and Japan reported relatively low per-capita sales, ranging from 0.45 to 0.77 pieces, indicating varying degrees of market penetration.

- The lowest per-capita volumes were observed in countries with emerging markets or lower sports and swimwear adoption rates, such as India, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines, all of which reported per-capita sales significantly below 0.2 pieces.

- This wide range of per-capita sales volumes highlights diverse consumer behaviors and market maturity levels across the globe.

(Source: Statista)

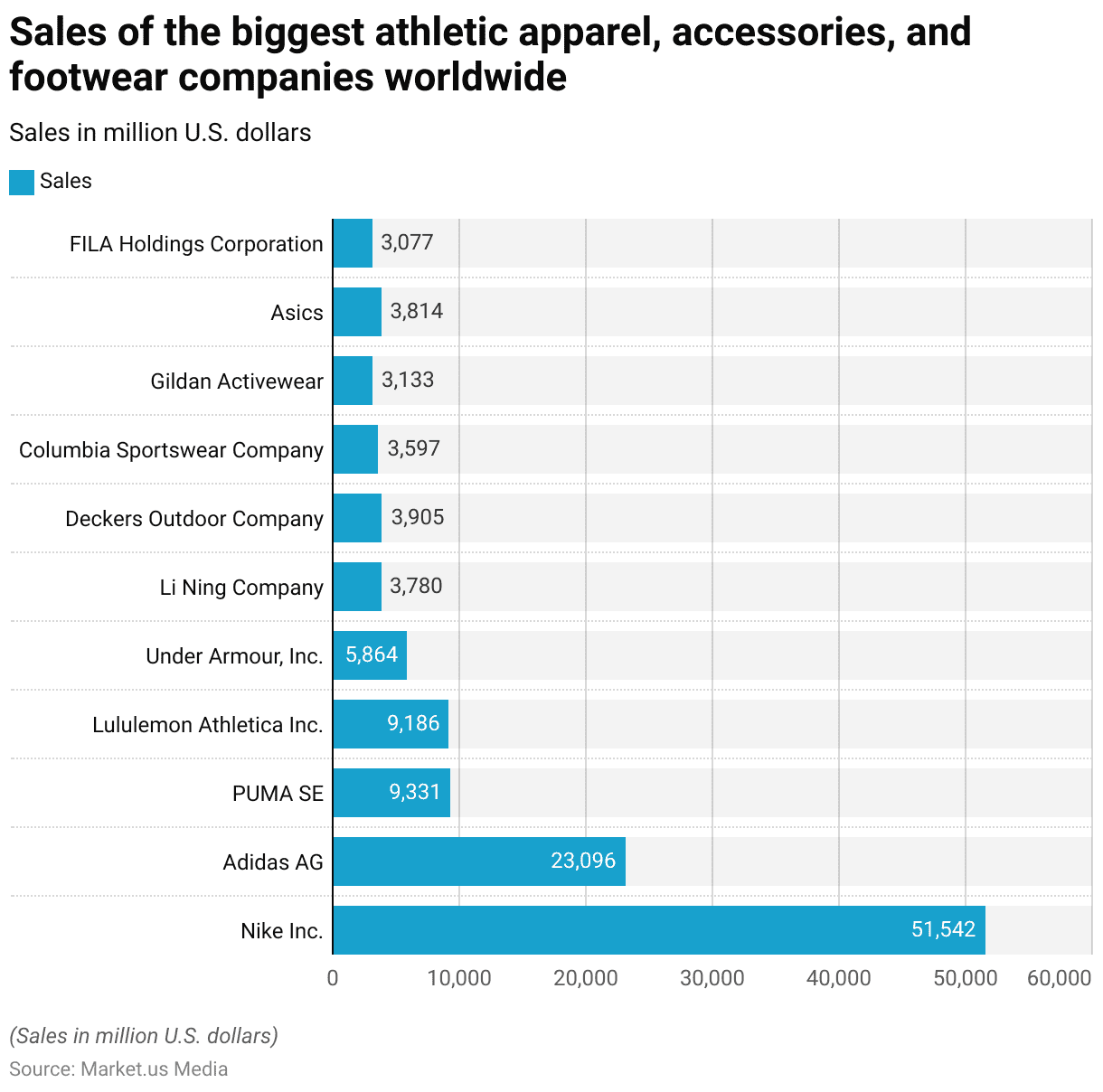

Global Sales of the Top Performance Apparel, Accessories, and Footwear Companies

- In 2023, sales figures for the largest athletic apparel, accessories, and footwear companies worldwide showed significant variance, reflecting their market positions and scale.

- Nike Inc. dominated the industry with the highest sales, amounting to USD 51,542 million, substantially ahead of its nearest competitor, Adidas AG, which reported sales of USD 23,096 million.

- PUMA SE and Lululemon Athletica Inc. also held substantial market shares, with sales of USD 9,331 million and USD 9,186 million, respectively.

- Under Armour, Inc. followed with sales reaching USD 5,864 million.

- Other key players included Li Ning Company with USD 3,780 million, Deckers Outdoor Company with USD 3,905 million, and Columbia Sportswear Company, which posted sales of USD 3,597 million.

- Gildan Activewear and Asics reported sales of USD 3,133 million and USD 3,814 million, respectively.

- FILA Holdings Corporation recorded sales of USD 3,077 million, highlighting its position among leading brands.

- These figures demonstrate the competitive landscape and varying scales of operations within the global athletic apparel market.

(Source: Statista)

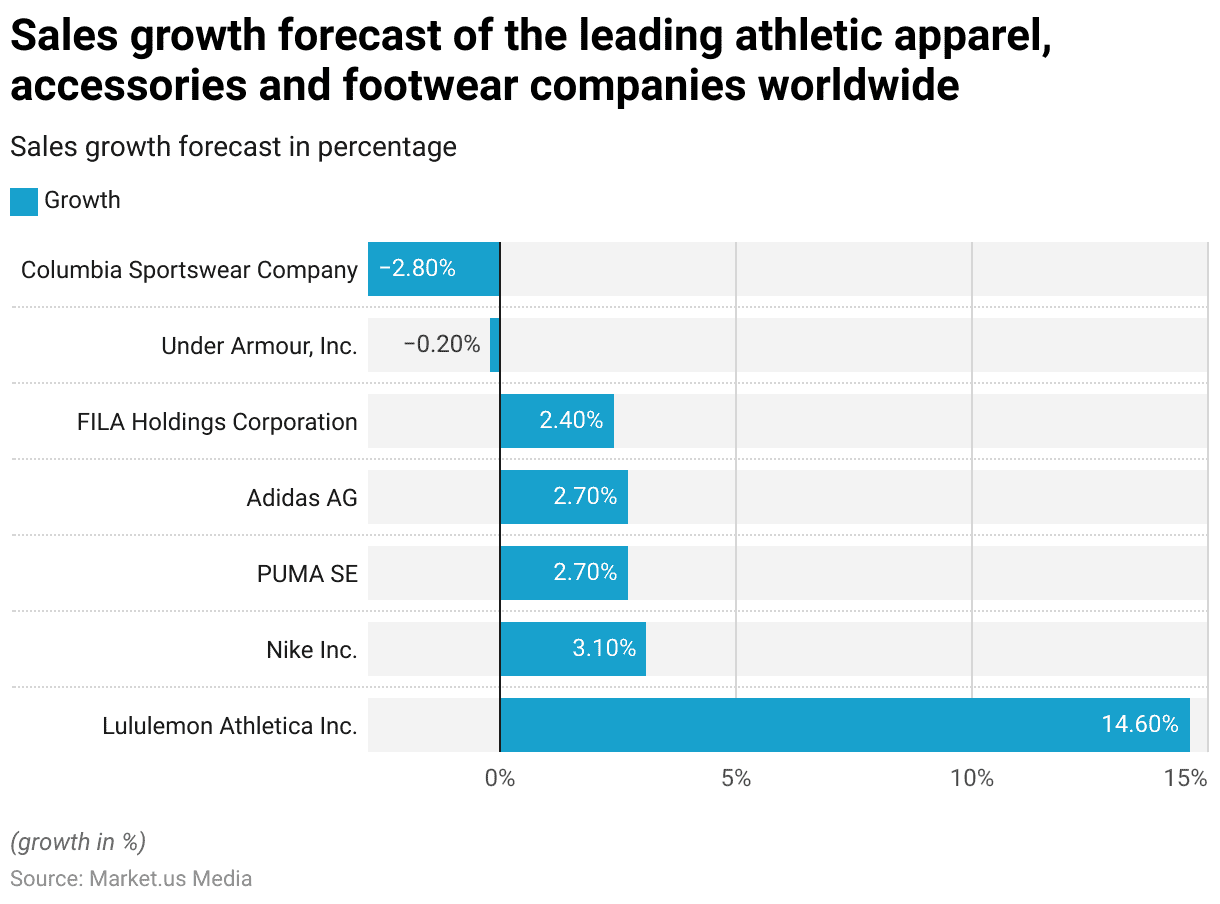

Global Sales Growth Forecast of Top Athletic Wear Companies

- In 2024, the sales growth forecast for leading athletic apparel, accessories, and footwear companies varies significantly.

- Lululemon Athletica Inc. is projected to lead the growth with a remarkable increase of 14.60%, far outpacing its competitors.

- Nike Inc. follows with a moderate growth rate of 3.10%.

- PUMA SE and Adidas AG are both expected to see their sales rise by 2.70%, indicating steady, albeit more conservative, growth.

- FILA Holdings Corporation’s growth forecast is slightly lower at 2.40%.

- In contrast, some companies are expected to experience a decline in sales. Under Armour, Inc. is projected to see a slight decrease of 0.20%, while Columbia Sportswear Company faces a more substantial decline of 2.80%.

- This diverse range of growth forecasts highlights the varied strategic positions and market dynamics affecting these prominent players in the athletic apparel industry.

(Source: Statista)

Athleisure Companies Statistics

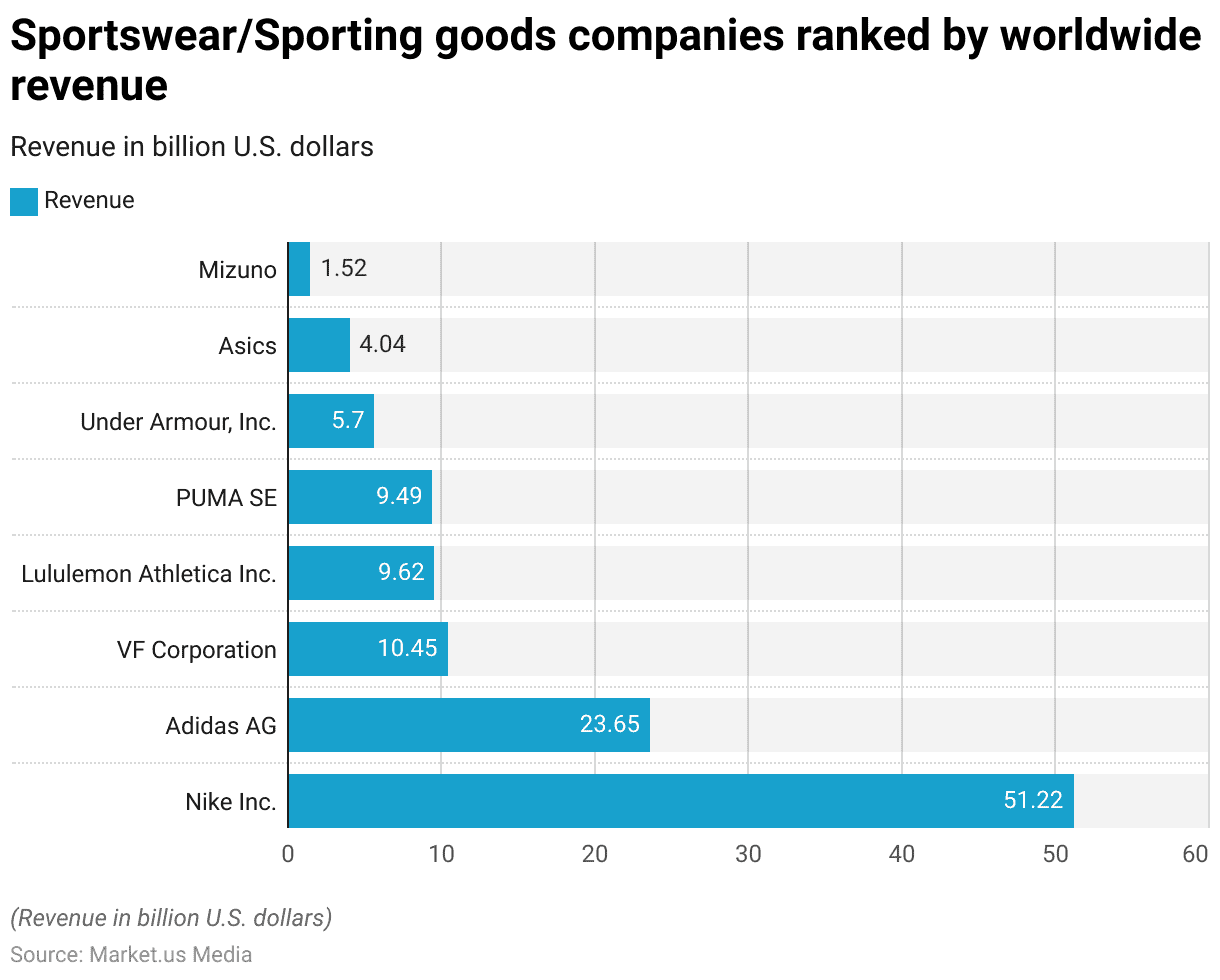

Largest Sporting Goods Companies Worldwide

- In fiscal 2023, the revenue rankings of sportswear and sporting goods companies highlighted significant disparities in their financial performance.

- Nike Inc. led the pack with a substantial revenue of USD 51.22 billion, far exceeding its closest competitor.

- Adidas AG followed with a revenue of USD 23.65 billion, establishing itself as another major player in the industry.

- VF Corporation, which owns a variety of apparel brands, generated a considerable revenue of USD 10.45 billion.

- Lululemon Athletica Inc. and PUMA SE were not far behind, posting revenues of USD 9.62 billion and USD 9.49 billion, respectively, indicating their strong market presence and consumer appeal.

- Under Armour, Inc. also maintained a significant share of the market with revenue totaling USD 5.7 billion.

- Asics and Mizuno, while smaller in comparison to the industry leaders, still held notable positions with revenues of USD 4.04 billion and USD 1.52 billion, respectively.

- These figures demonstrate the varying levels of market penetration and consumer demand among leading brands in the global sportswear and sporting goods market.

(Source: Statista)

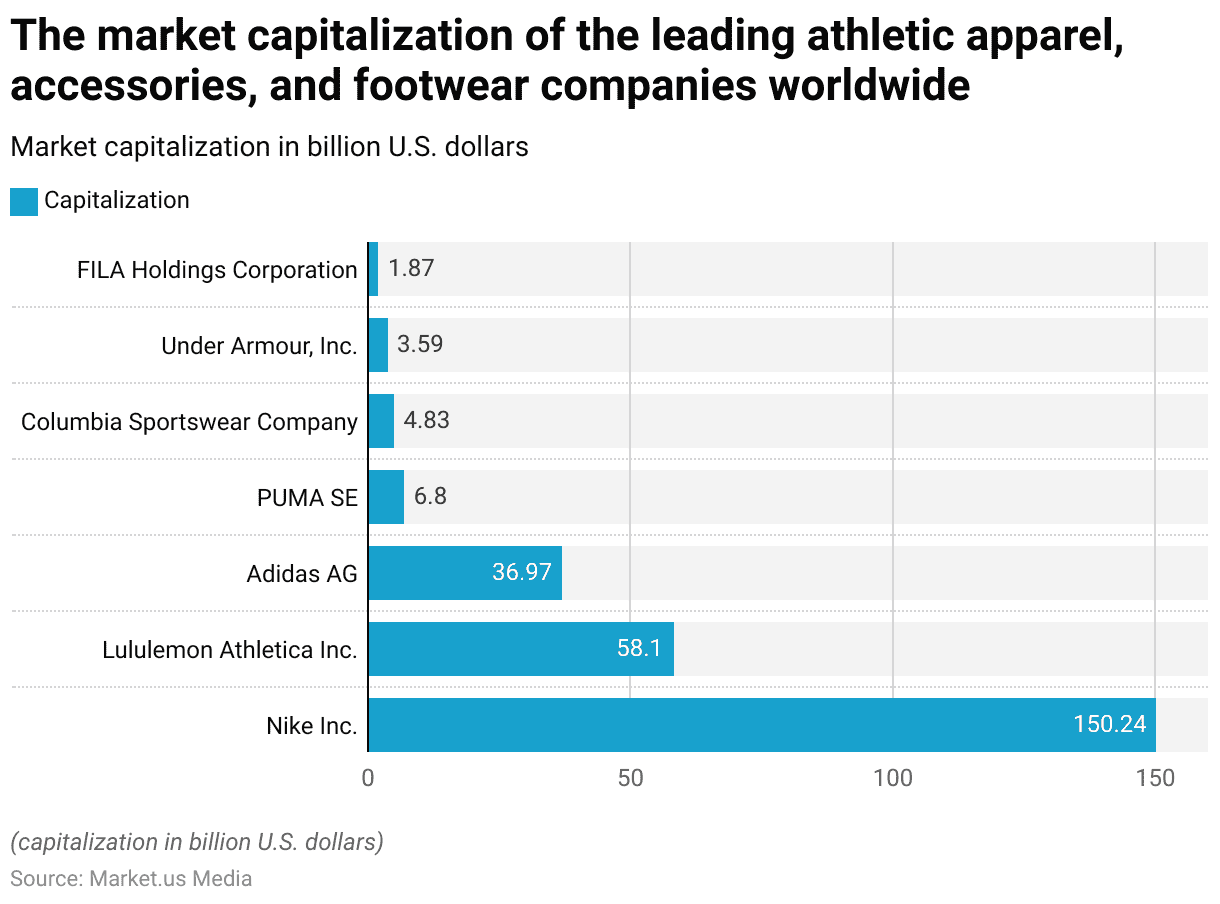

Market Capitalization of the Top Performance Apparel, Accessories and Footwear Companies

- In 2024, the market capitalization of leading athletic apparel, accessories, and footwear companies showcased significant differences in scale and financial valuation.

- Nike Inc. led the industry with a substantial market capitalization of USD 150.24 billion, indicating its dominant position within the sector.

- Lululemon Athletica Inc. held a strong second position with a market capitalization of USD 58.1 billion, reflecting its robust growth and premium brand positioning.

- Adidas AG also maintained a considerable presence with a market capitalization of USD 36.97 billion.

- Smaller yet significant players included PUMA SE, which was valued at USD 6.8 billion, and Columbia Sportswear Company, with a market cap of USD 4.83 billion.

- Under Armour, Inc., known for its innovative performance wear, had a market capitalization of USD 3.59 billion.

- FILA Holdings Corporation, while smaller in comparison to its peers, still held a substantial market cap of USD 1.87 billion.

- These figures demonstrate the varying degrees of market influence and financial standing among the top companies in the global athletic apparel market.

(Source: Statista)

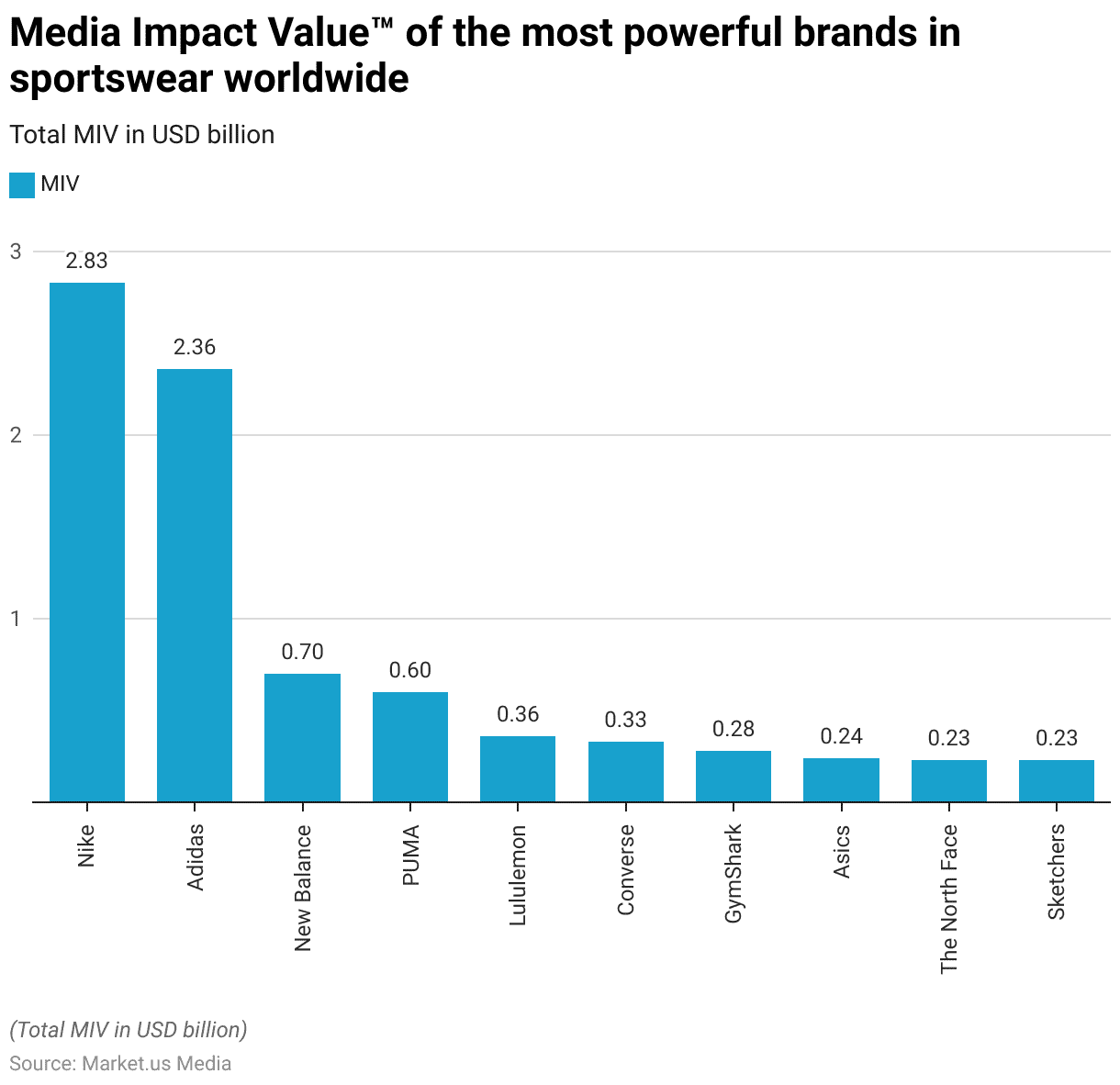

Media Impact Value of the Most Powerful Brands in Sportswear Worldwide

- In 2023, the Media Impact Value™ (MIV) of the most powerful brands in the sportswear industry showcased Nike and Adidas leading the pack with significant figures.

- Nike topped the chart with an MIV of USD 2.83 billion, reflecting its dominant brand influence and market penetration.

- Adidas followed closely with an MIV of USD 2.36 billion, underscoring its strong global presence and marketing effectiveness.

- New Balance, PUMA, and Lululemon also demonstrated noteworthy media impacts with MIVs of USD 0.7 billion, USD 0.6 billion, and USD 0.36 billion, respectively, indicating their successful branding and consumer engagement strategies.

- Converse and GymShark further highlighted their media traction with MIVs of USD 0.33 billion and USD 0.28 billion, respectively.

- Asics, The North Face, and Skechers, though smaller in comparison, still maintained significant media visibility with MIVs of USD 0.24 billion, USD 0.23 billion, and USD 0.23 billion, respectively.

- These figures represent the effective media strategies and the resultant brand value generated by these companies in the competitive sportswear market of 2023.

(Source: Statista)

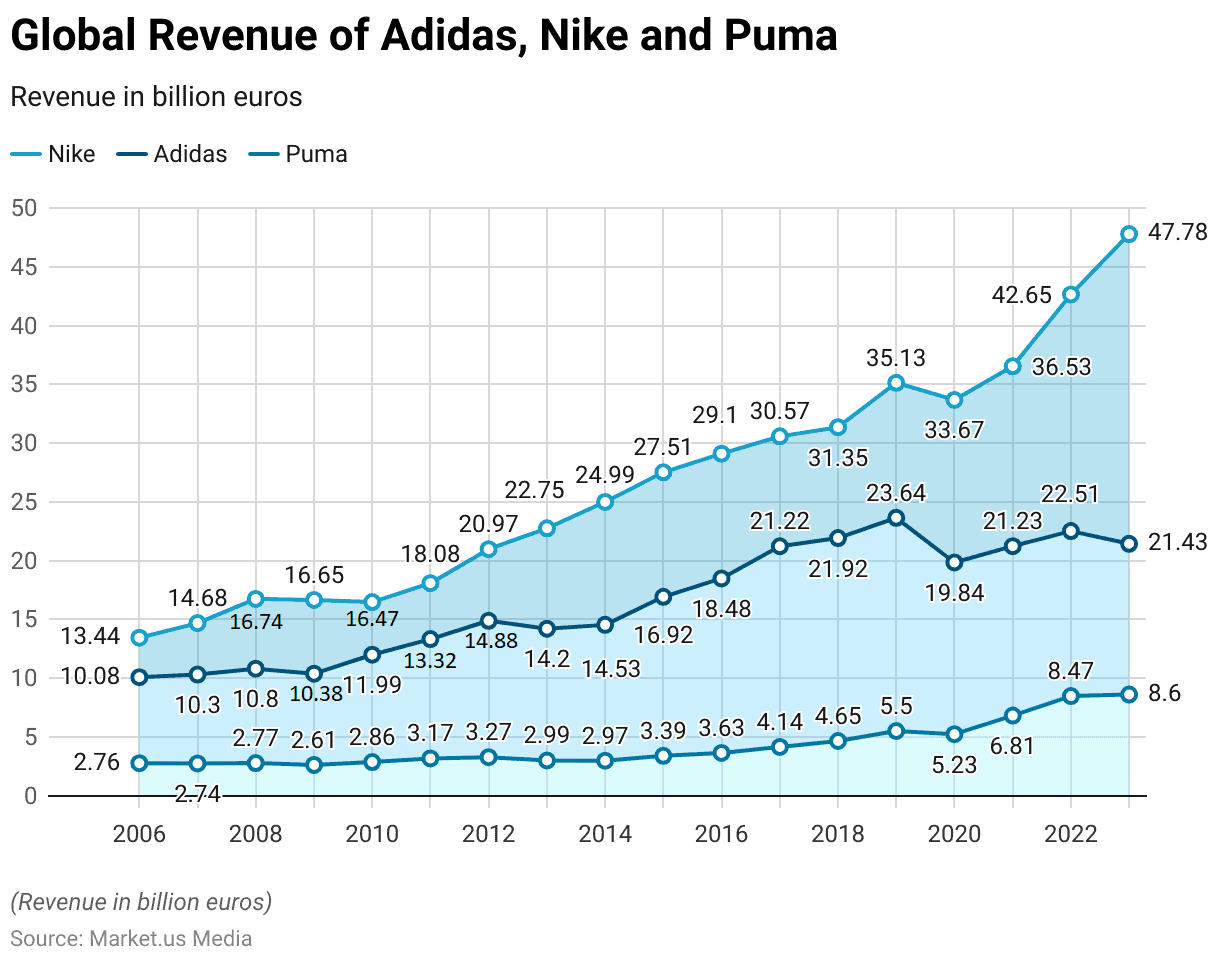

Adidas, Nike & Puma Revenue Comparison

- From 2006 to 2023, the global revenues of Nike, Adidas, and Puma exhibited varied growth trajectories.

- In 2006, Nike reported a revenue of €13.44 billion, with Adidas at €10.08 billion and Puma at €2.76 billion. Over the next few years, all three companies saw fluctuations but generally upward trends in their revenue figures.

- By 2007, Nike’s revenue increased to €14.68 billion, and Adidas slightly rose to €10.3 billion, while Puma experienced a slight dip to €2.74 billion.

- A significant growth spurt occurred for Nike in 2008, reaching €16.74 billion, as Adidas climbed to €10.8 billion, and Puma slightly increased to €2.77 billion.

- The following years up to 2011 saw Nike’s revenues hover around €16 billion, then jump to €18.08 billion in 2011, while Adidas experienced a steadier increase, reaching €13.32 billion in the same year, and Puma growing to €3.17 billion.

- The period from 2012 onwards marked a robust growth phase, especially for Nike, which saw its revenues skyrocket to €42.65 billion by 2022.

- Adidas also grew substantially during this period, peaking at €22.51 billion in 2022 before slightly declining to €21.43 billion in 2023. Puma’s revenue followed a similar upward trend, peaking at €8.6 billion in 2023.

- This progression illustrates significant revenue increases for all three companies, with Nike consistently leading in terms of revenue generation, followed by Adidas and Puma.

- Each brand showed resilience and the ability to grow amidst varying market conditions over nearly two decades.

(Source: Statista)

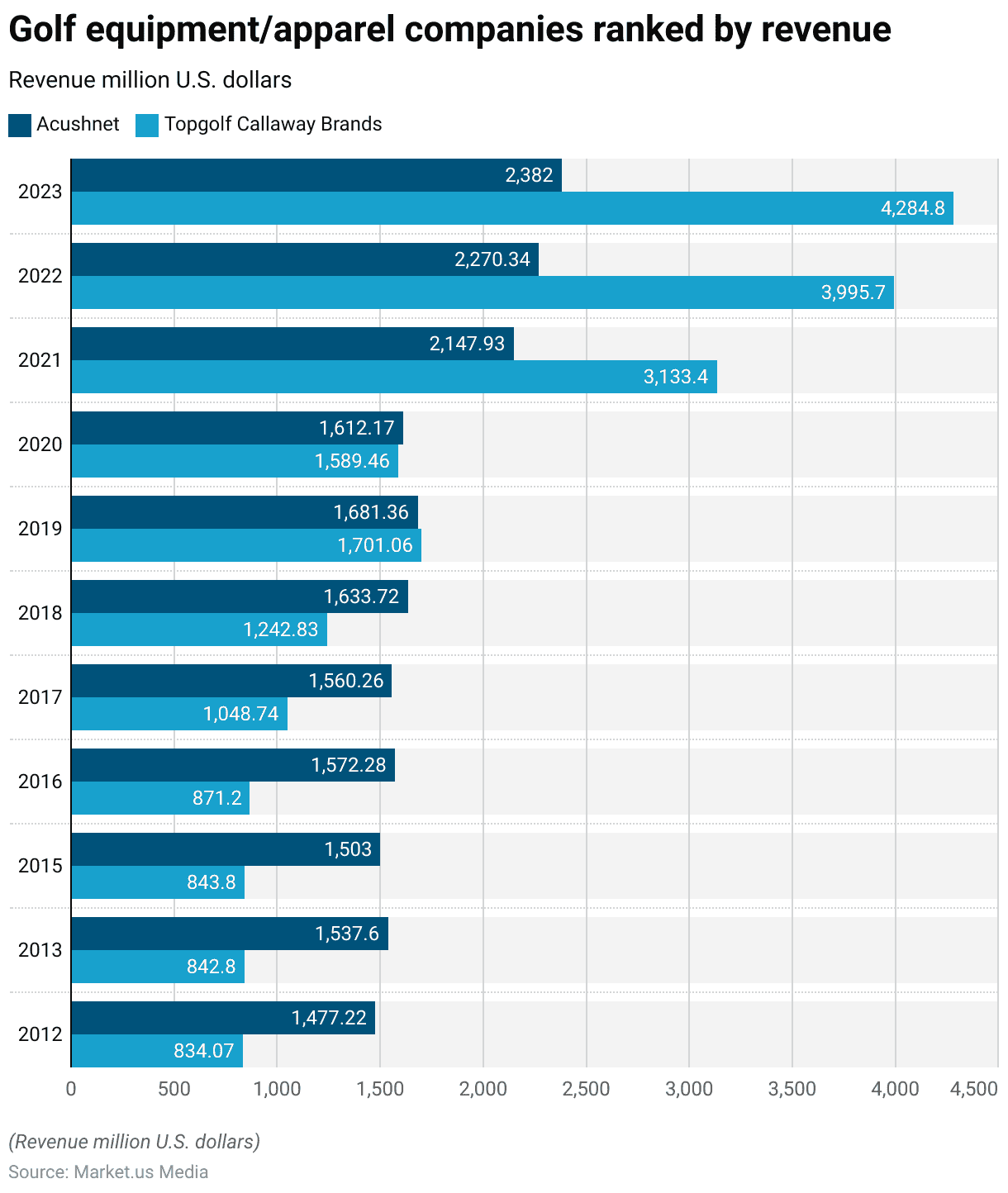

Revenue of Golf Equipment/Apparel Companies Worldwide

- From 2012 to 2023, the revenue trajectories of Acushnet and Topgolf Callaway Brands, two prominent companies in the golf equipment and apparel industry, reflected notable growth and significant market shifts.

- Acushnet started the period in 2012 with revenues of $1,477.22 million, experiencing gradual increases over the years, with a mild drop in 2015 to $1,503.0 million before rising steadily to reach $1,681.36 million in 2019.

- A slight decrease occurred in 2020, dropping to $1,612.17 million, likely influenced by market conditions.

- However, a sharp increase followed in 2021, with revenues soaring to $2,147.93 million, and continued growth led to $2,382.0 million by 2023.

- Topgolf Callaway Brands demonstrated a more dramatic growth pattern, starting from $834.07 million in 2012.

- The revenues saw a modest increase initially, reaching $843.8 million in 2015 and $871.20 million in 2016.

- The revenue then significantly jumped in 2017 to $1,048.74 million, and more robust growth ensued, peaking at $4,284.80 million in 2023 after substantial annual increases from 2019 onwards.

- This remarkable growth trajectory highlights Topgolf Callaway Brands’ aggressive expansion and increasing market presence compared to the steadier growth of Acushnet.

(Source: Statista)

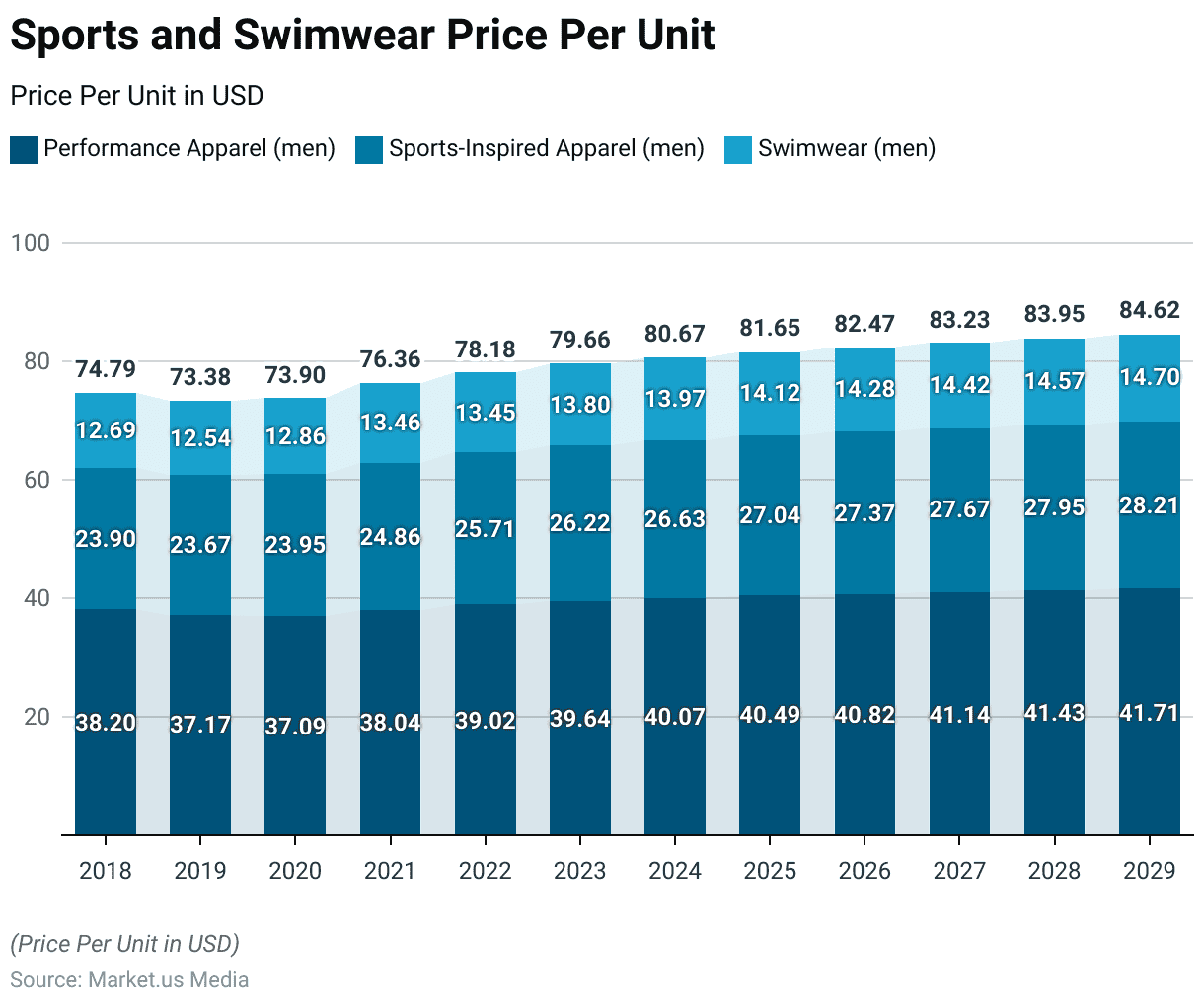

Sports and Swimwear Price Trends

- From 2018 to 2029, the pricing trends for men’s sports and swimwear, encompassing performance apparel, sports-inspired apparel, and swimwear, indicate a consistent upward trajectory in unit prices across all categories.

- Initially, in 2018, performance apparel was priced at $38.20 per unit.

- This category experienced a slight decrease in 2019 to $37.17, followed by a minor dip in 2020 to $37.09, before embarking on a steady annual increase, reaching $41.71 by 2029.

- Sports-inspired apparel began at $23.90 per unit in 2018, dipped slightly in 2019 to $23.67, and then gradually increased each year, achieving $28.21 per unit by 2029.

- Similarly, swimwear started at $12.69 per unit in 2018, saw a slight decrease in 2019 to $12.54, but subsequently rose each year, culminating at $14.70 per unit in 2029.

- These incremental increases reflect a steady rise in the cost or perceived value of these products over the period.

- The overall upward trend across the categories suggests that the market conditions for men’s sports and swimwear remain robust, with growing consumer demand likely driving the increases in unit prices year over year.

(Source: Statista)

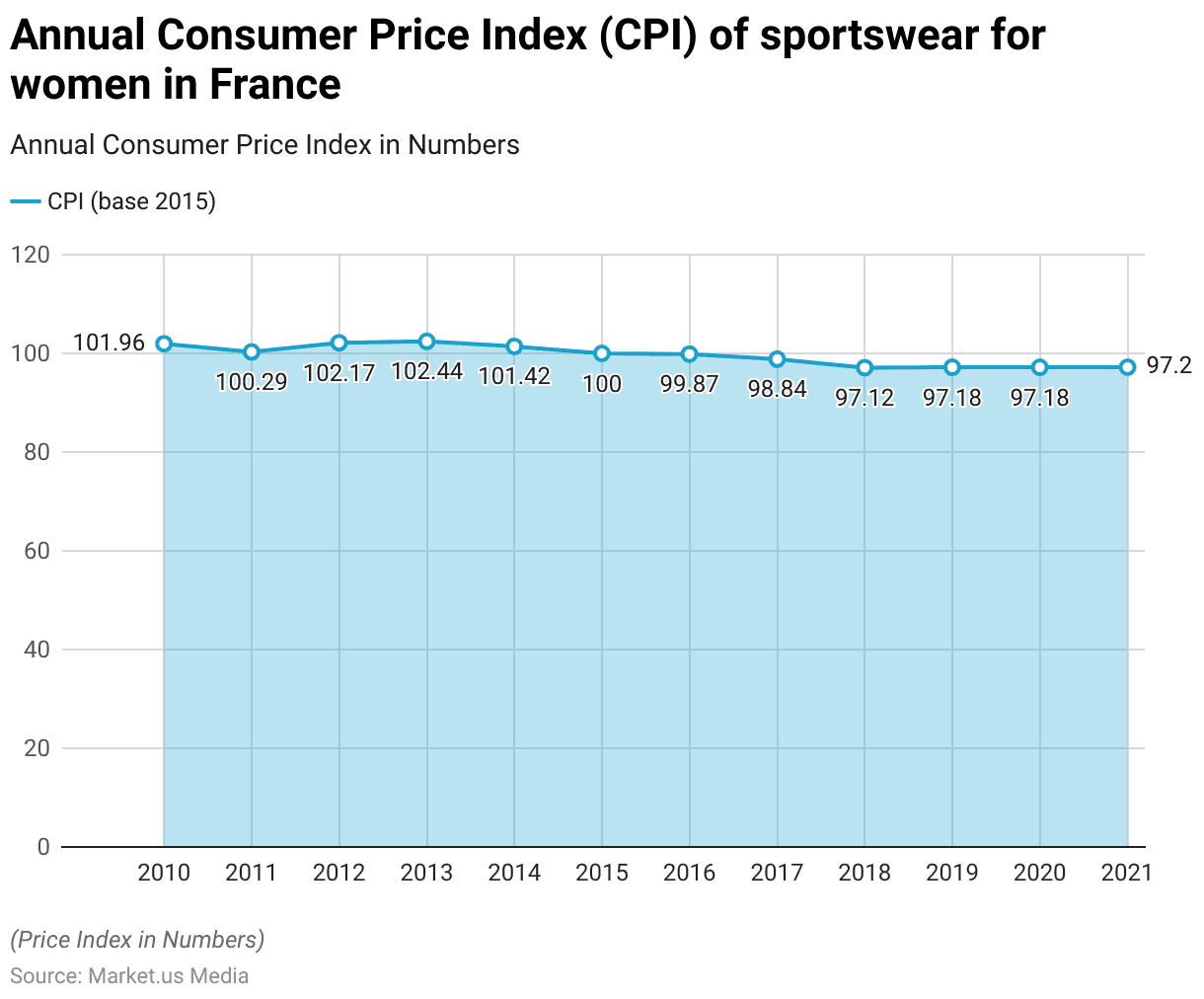

Consumer Price Index (CPI) of Sportswear for Women

- Between 2010 and 2021, the Consumer Price Index (CPI) for women’s sportswear in France exhibited a noticeable trend, fluctuating initially and then showing a gradual decline over the years, using 2015 as the base year (indexed at 100).

- In 2010, the CPI stood slightly above the base at 101.96, indicating higher prices relative to the base year.

- It slightly decreased to 100.29 in 2011 and then rose to its peak at 102.44 in 2013, suggesting an increase in sportswear prices during this period.

- After 2013, the CPI began a consistent downward trend, reflecting a decrease in prices.

- By 2014, it had dropped to 101.42, and by 2015, it normalized to the base index of 100.

- This downward trend continued post-2015; in 2016, the index slightly decreased to 99.87 and further declined to 98.84 in 2017.

- The trend of declining prices persisted, reaching 97.12 in 2018 and stabilizing around 97.18 in 2019 and 2020.

- In 2021, the CPI marginally increased to 97.2, indicating a slight stabilization but overall remaining below the level of 2015.

- This overall decrease in the CPI from 2015 onwards suggests that the cost of women’s sportswear in France became more affordable over the latter part of the observed period.

(Source: Statista)

Demographic Dynamics of Athleisure Consumers

Age

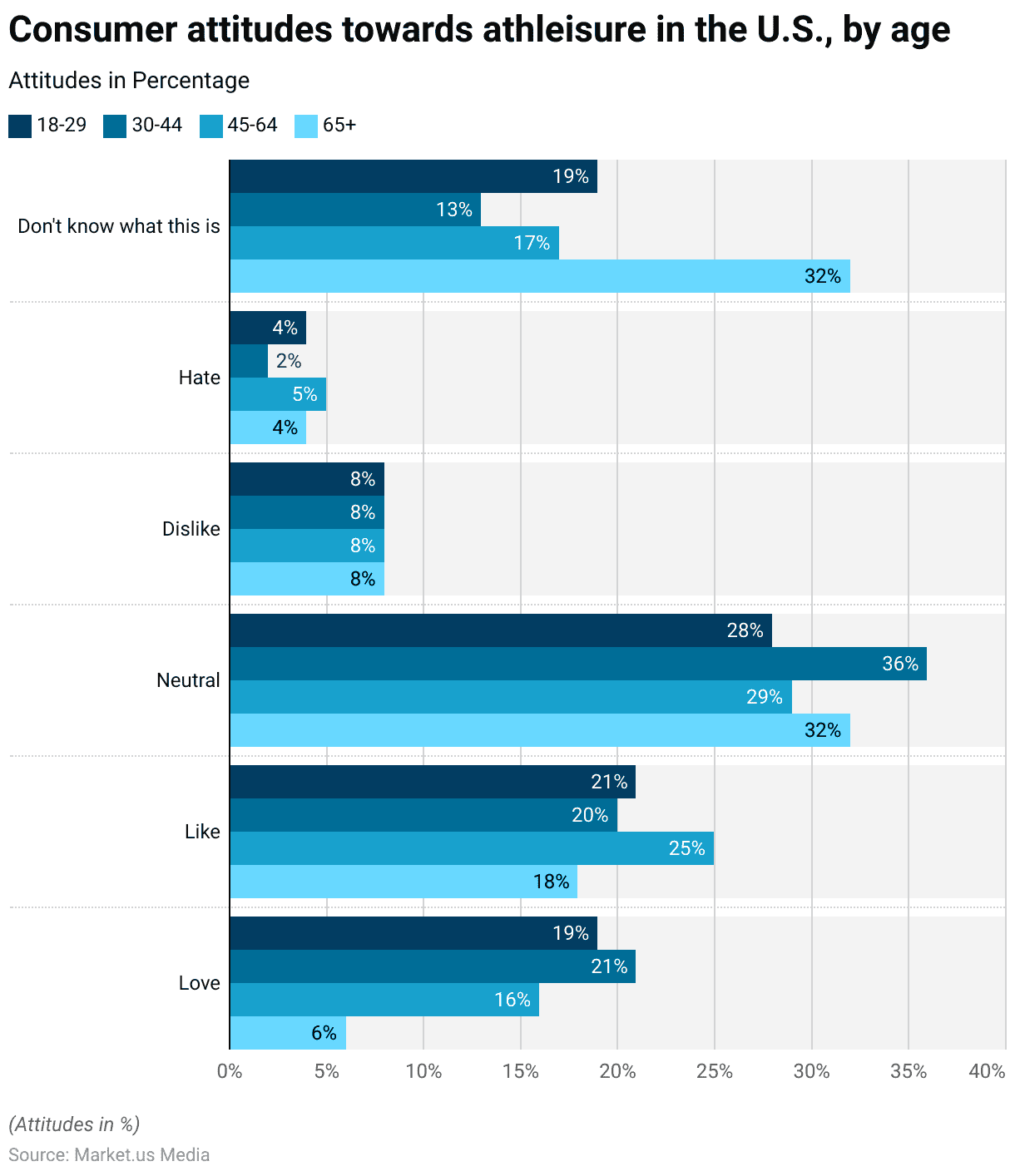

- In the United States in 2023, consumer attitudes towards the athleisure fashion trend varied significantly across different age groups.

- Among the youngest demographic, aged 18-29, 19% expressed a strong affinity for the trend (“Love”), closely followed by 21% of those aged 30-44.

- This affection was less pronounced in the older age brackets, with 16% of those aged 45-64 and only 6% of those 65 and older sharing the sentiment.

- The trend was “Liked” by a larger portion of the 45-64 age group, at 25%, compared to 21% of 18-29-year-olds and 20% of 30-44-year-olds, with older adults (65+) showing an 18% approval rate.

- “Neutral” responses were highest among the 30-44 age group at 36%, while 28% of the youngest group, 29% of the 45-64 group, and 32% of those 65 and older felt the same.

- Dislike and hate towards athleisure were relatively consistent across all age groups, with about 8% disliking and 2-5% hating the trend.

- However, significant uncertainty or lack of awareness about athleisure was evident, especially among older adults (65+), with 32% indicating they didn’t know what the trend was, compared to 19% of the 18-29 group, 13% of the 30-44 group, and 17% of the 45-64 group.

- This illustrates a clear generational gap in both awareness and acceptance of the athleisure trend.

(Source: Statista)

Generation

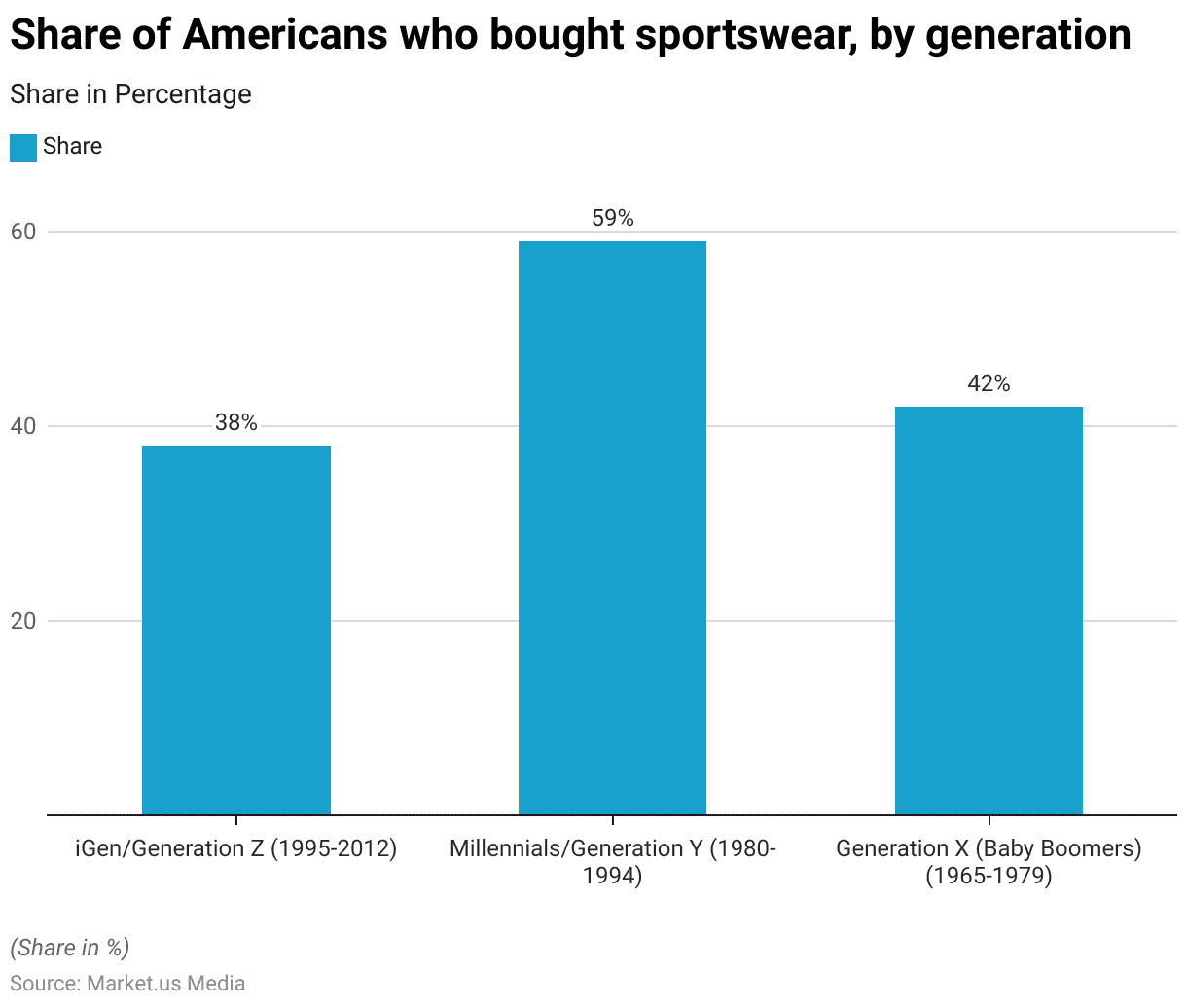

- In 2021, the purchasing behavior of Americans regarding sportswear varied notably across different generational cohorts.

- Millennials, or Generation Y (born 1980-1994), demonstrated the highest engagement with sportswear, with 59% of respondents indicating they had purchased sportswear within the last 24 months.

- This high level of participation highlights the strong connection between Millennials and active lifestyle trends.

- Generation X (born 1965-1979) also showed significant interest, with 42% reporting sportswear purchases, reflecting their ongoing involvement in personal health and fitness.

- In contrast, iGen, or Generation Z (born 1995-2012), had a lower participation rate at 38%, suggesting a varied set of interests or financial priorities among the youngest demographic.

- This data underscores the marked differences in sportswear consumption habits among the generations, with Millennials leading the trend.

(Source: Statista)

Gender

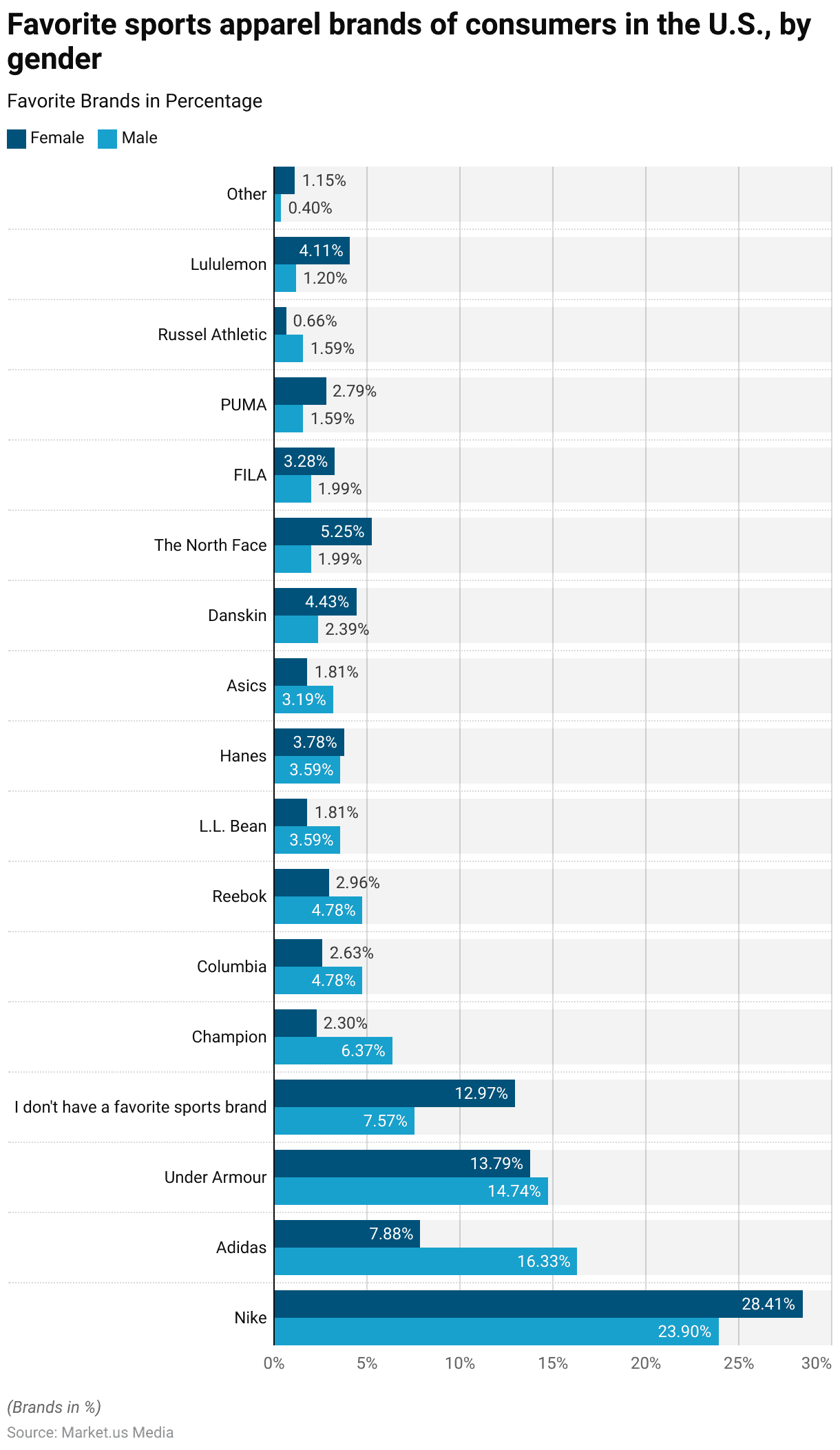

- In a 2018 survey focusing on U.S. consumers’ favorite sports apparel brands by gender, Nike emerged as the clear leader among both females and males, capturing 28.41% and 23.90% of preferences, respectively.

- Adidas was more favored by males (16.33%) compared to females (7.88%). Under Armour also held significant appeal, with 13.79% of females and 14.74% of males regarding it as their favorite.

- A notable percentage of respondents did not have a specific favorite sports brand, with 12.97% of females and 7.57% of males expressing no particular preference.

- Among other brands, Champion was preferred by 6.37% of males and 2.30% of females, showing a greater inclination among men. Columbia and Reebok each gathered around 2.63% to 4.78% across genders.

- Less mainstream but still significant, The North Face and Danskin were notably more favored by females, gathering 5.25% and 4.43%, respectively, compared to under 2.39% from males.

- Lululemon was also more popular among females at 4.11% compared to just 1.20% among males.

- Other brands like FILA, PUMA, and Asics showed smaller but still notable gender-based differences in preference.

- This data illustrates the diverse preferences in sportswear, with certain brands showing marked differences in popularity between genders.

(Source: Statista)

Income Group

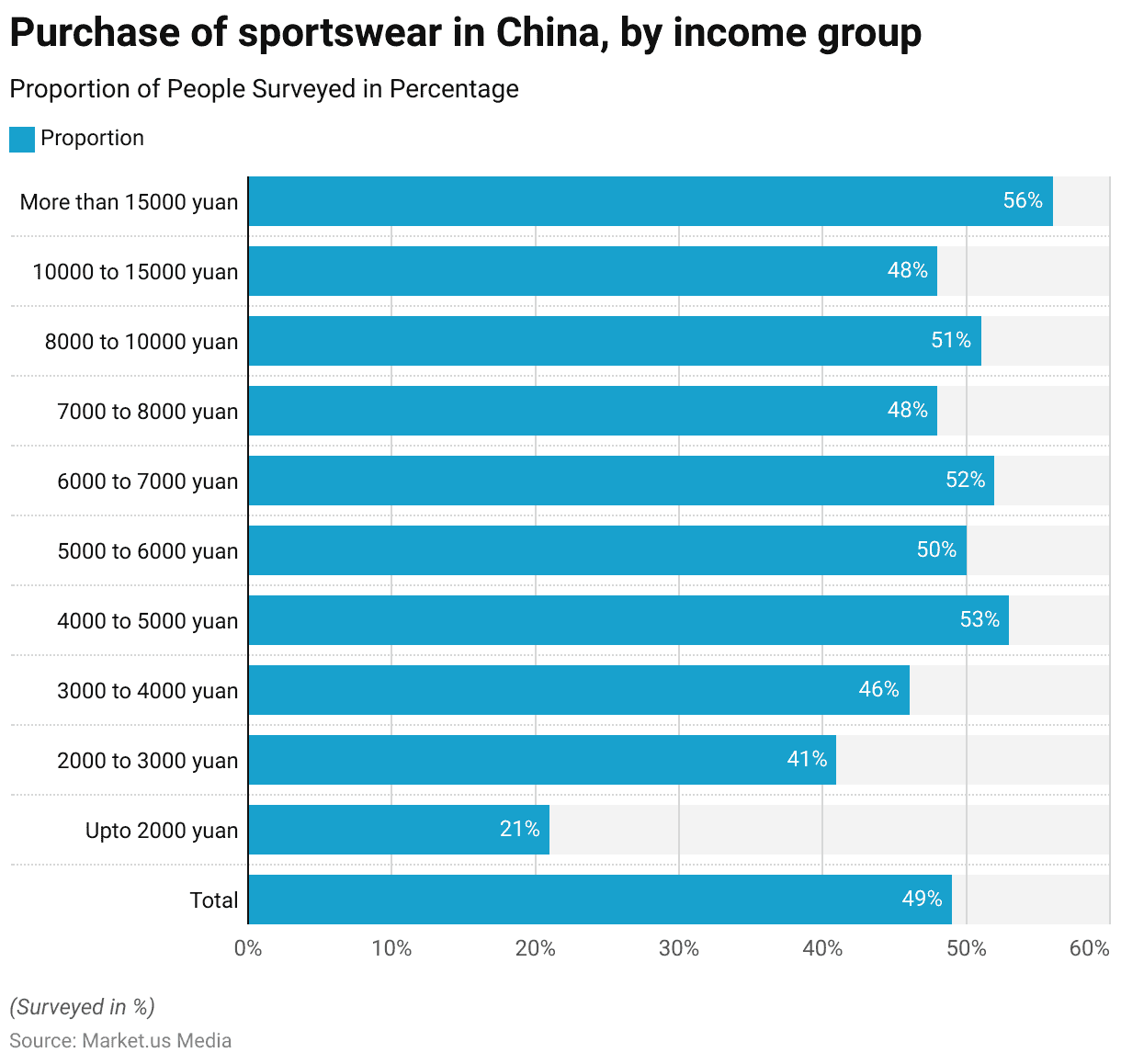

- In 2012, a survey on the purchase of sportswear in China revealed varied buying patterns across different income groups.

- Overall, 49% of the surveyed population reported purchasing sportswear. Those earning up to 2,000 yuan were the least likely to buy sportswear, with only 21% reporting purchases.

- The propensity to purchase sportswear increased with income: 41% of those earning between 2,000 to 3,000 yuan and 46% of those with incomes from 3,000 to 4,000 yuan bought sportswear.

- The highest purchase rates were observed in higher income brackets. For instance, 53% of individuals earning between 4,000 to 5,000 yuan and 50% of those making between 5,000 to 6,000 yuan purchased sportswear.

- Similarly, 52% of the group earning between 6,000 to 7,000 yuan, and 51% of those with incomes from 8,000 to 10,000 yuan reported buying sportswear.

- Those earning between 7,000 to 8,000 yuan and between 10,000 to 15,000 yuan had slightly lower purchase proportions at 48%.

- However, individuals earning more than 15,000 yuan showed the highest sportswear purchasing rate at 56%.

- These findings indicate a clear correlation between higher income levels and the likelihood of purchasing sportswear in China during 2012.

(Source: Statista)

Consumer Preferences

Athleisure Brand Purchases

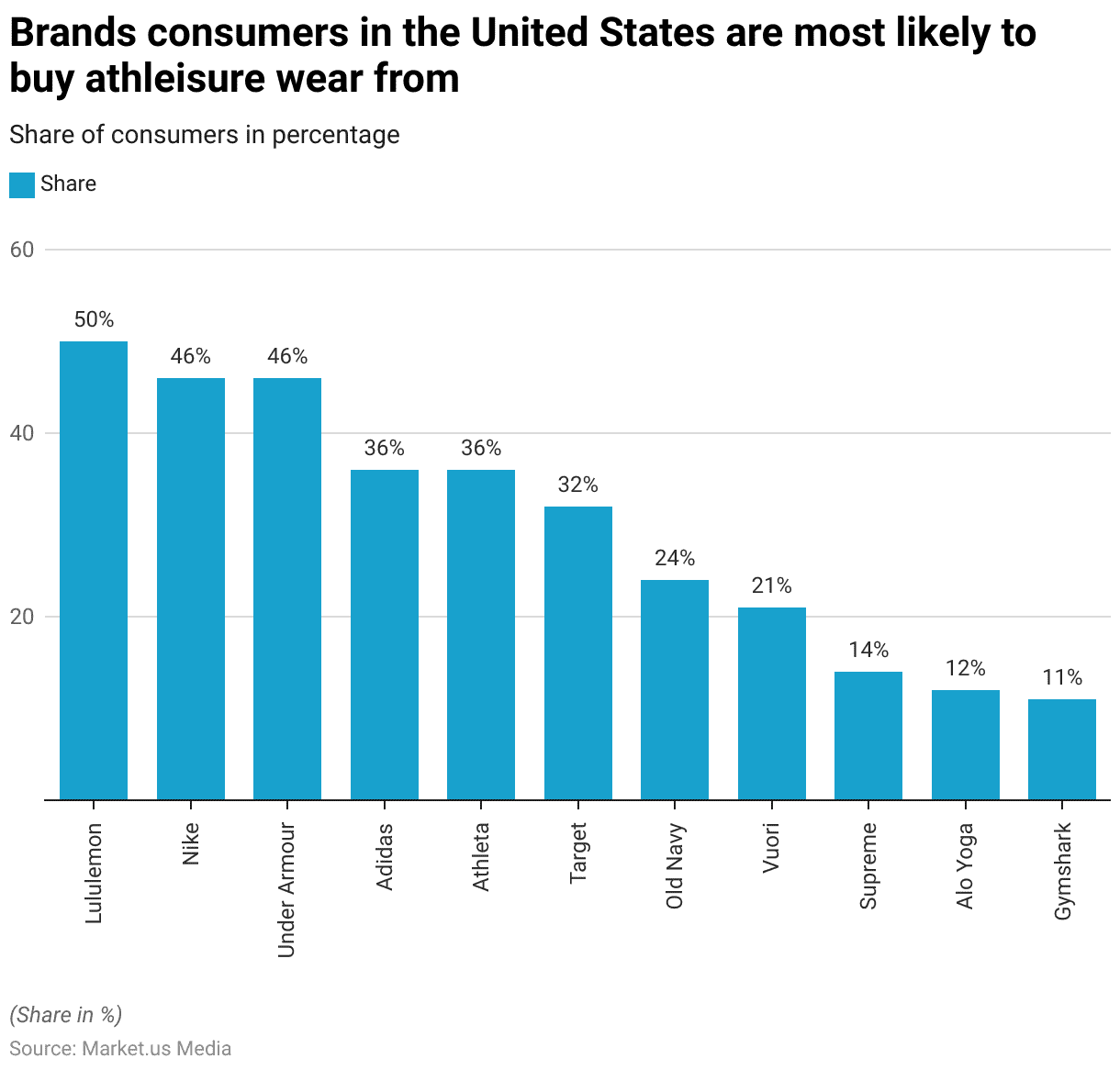

- In 2023, consumer preferences for athleisure wear brands in the United States showed distinct patterns.

- Lululemon led the market, with a significant 50% of consumers indicating it as their preferred brand for athleisure purchases.

- Nike and Under Armour were also highly favored, each capturing 46% of consumer preferences, demonstrating their strong market presence.

- Adidas and Athleta each held a solid position as well, with 36% of consumers likely to buy their products.

- Target followed, attracting 32% of consumers and showcasing its appeal in the athleisure sector, perhaps due to its accessible pricing and wide distribution.

- Old Navy, known for affordable clothing options, was preferred by 24% of the consumers. Vuori, a newer brand in the market, managed to capture 21% of consumer interest, reflecting its growing popularity.

- More niche brands like Supreme, Alo Yoga, and Gymshark had smaller but noteworthy shares of consumer preferences at 14%, 12%, and 11%, respectively.

- This distribution underscores the varied consumer choices and brand loyalty in the U.S. athleisure market, highlighting a strong inclination towards established brands as well as emerging labels.

(Source: Statista)

Motivation for Consumers to Buy Sports Apparel, Shoes & Equipment

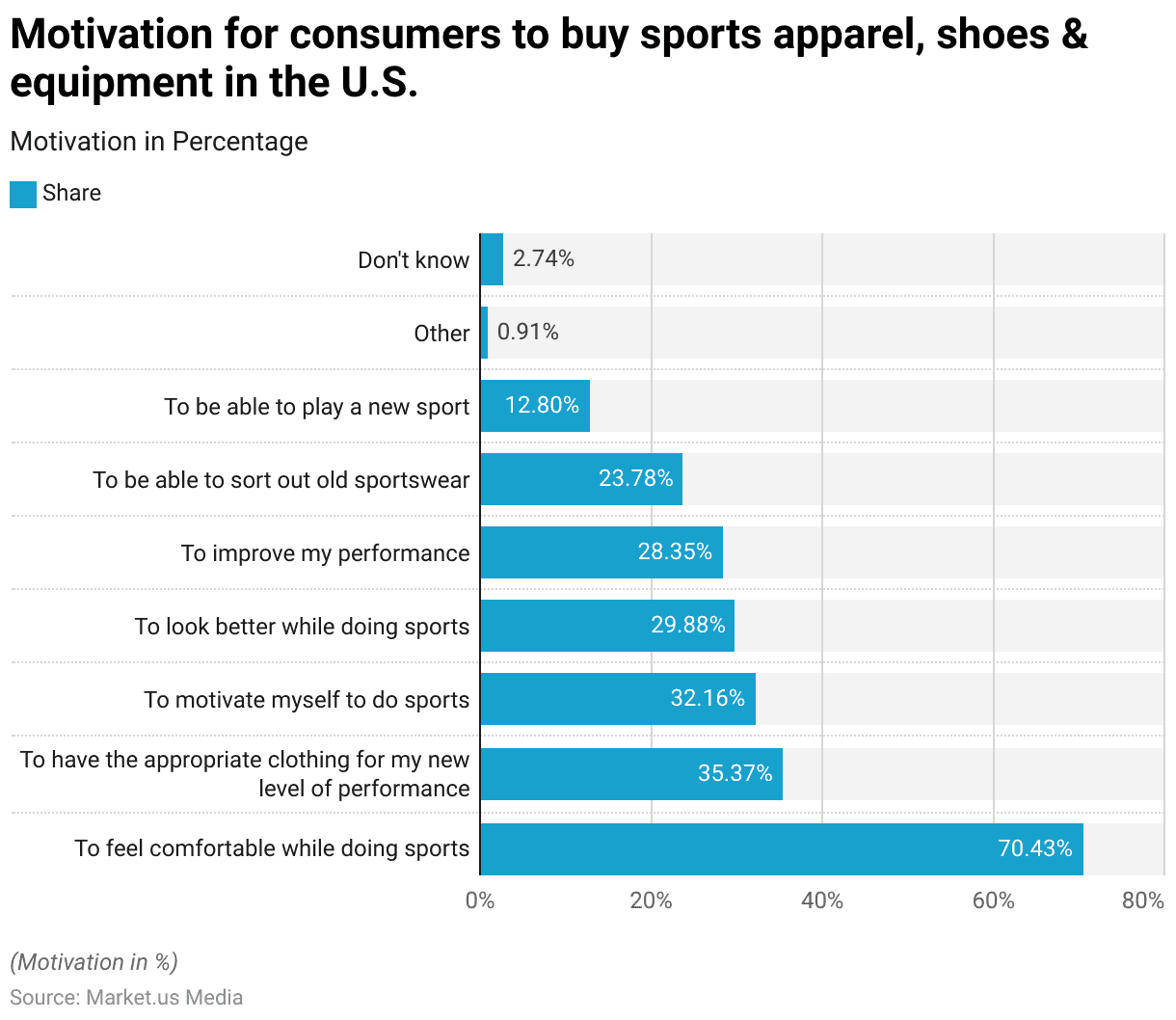

- In 2018, a survey on consumer motivations for purchasing sports apparel, shoes, and equipment in the U.S. revealed a variety of reasons influencing their buying decisions.

- A significant majority, 70.43% of respondents, cited comfort while engaging in sports as the primary aim. This emphasis on comfort underscores its importance in sports-related purchases.

- Additionally, 35.37% of consumers stated that obtaining apparel suitable for their new level of performance was a key motivation, indicating that many are looking to support their athletic progression with appropriate gear.

- Motivating oneself to engage in sports activities was another notable reason, with 32.16% of respondents choosing this, suggesting that new sports gear serves as an inspiration for some.

- Looking better while participating in sports was important for 29.88% of the respondents, while 28.35% purchased new items to improve their performance, highlighting the role of aesthetics and functionality in sportswear choices.

- About 23.78% mentioned replacing old sportswear as their motivation and 12.80% were gearing up to play a new sport. Only a small fraction, 0.91%, had other unspecified reasons, and 2.74% were unsure about their motivations.

- This distribution reflects a diverse set of goals that consumers consider when investing in new sports equipment and apparel.

(Source: Statista)

Purchase Frequency of Sportswear

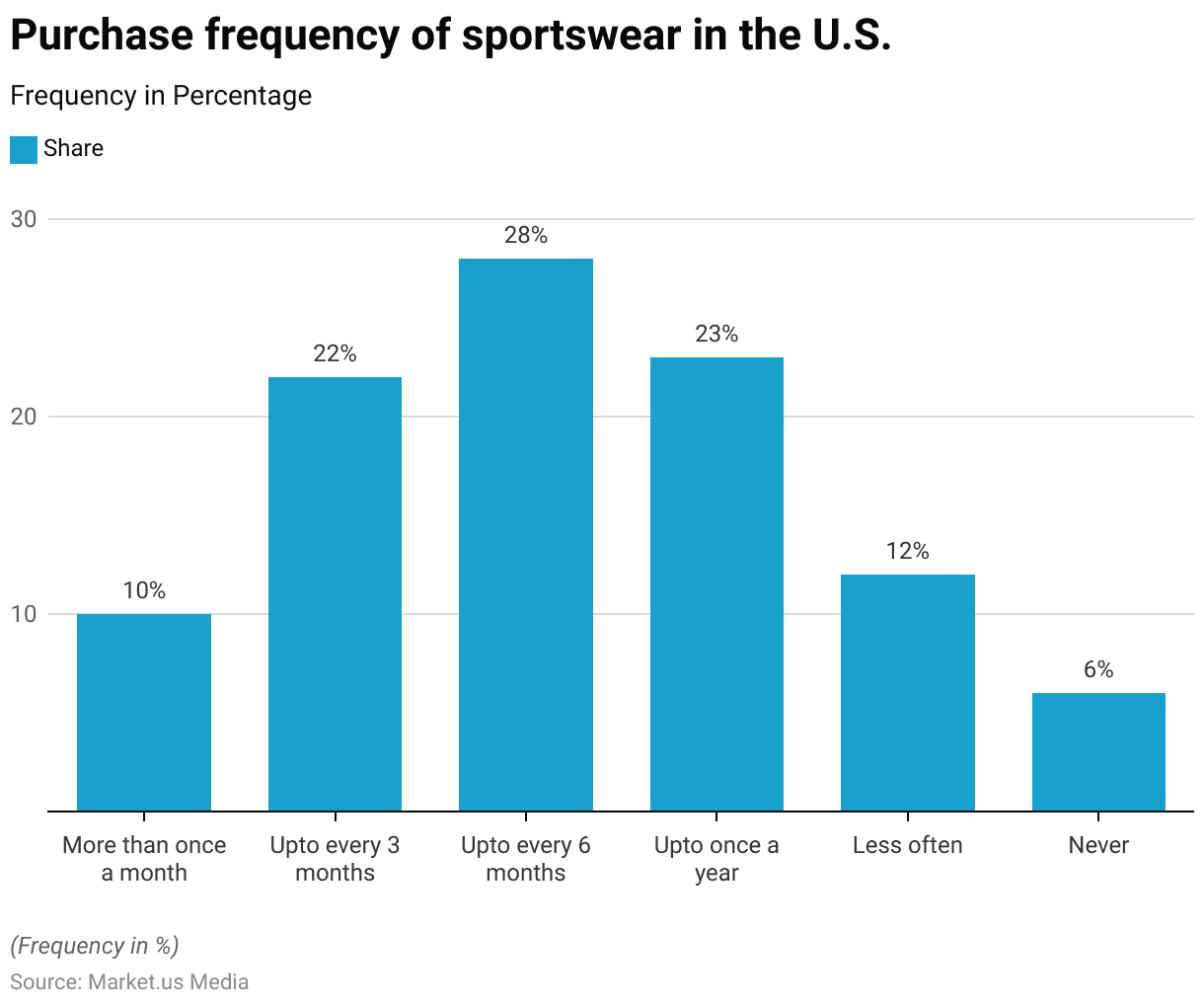

- In 2018, a survey analyzing the purchase frequency of sportswear among U.S. consumers revealed varied shopping habits.

- A small percentage, 10% of respondents, reported purchasing sportswear more than once a month, indicating a high level of engagement with active lifestyles or a strong preference for frequently updating their athletic wardrobe.

- The majority preferred less frequent shopping intervals: 22% purchased up to every three months, and 28%, the largest group, bought new sportswear up to every six months.

- About 23% of those surveyed chose to buy sportswear up to once a year, while 12% did so even less often.

- Notably, a minimal 6% of respondents stated they never buy sportswear.

- This data underscores a spectrum of consumer behaviors in sportswear shopping, ranging from those who frequently update their gear to support an active lifestyle to those who seldom feel the need to make such purchases.

(Source: Statista)

Popularity Growth Index of Leading Women’s Athletic Apparel Brands Among Generation Z

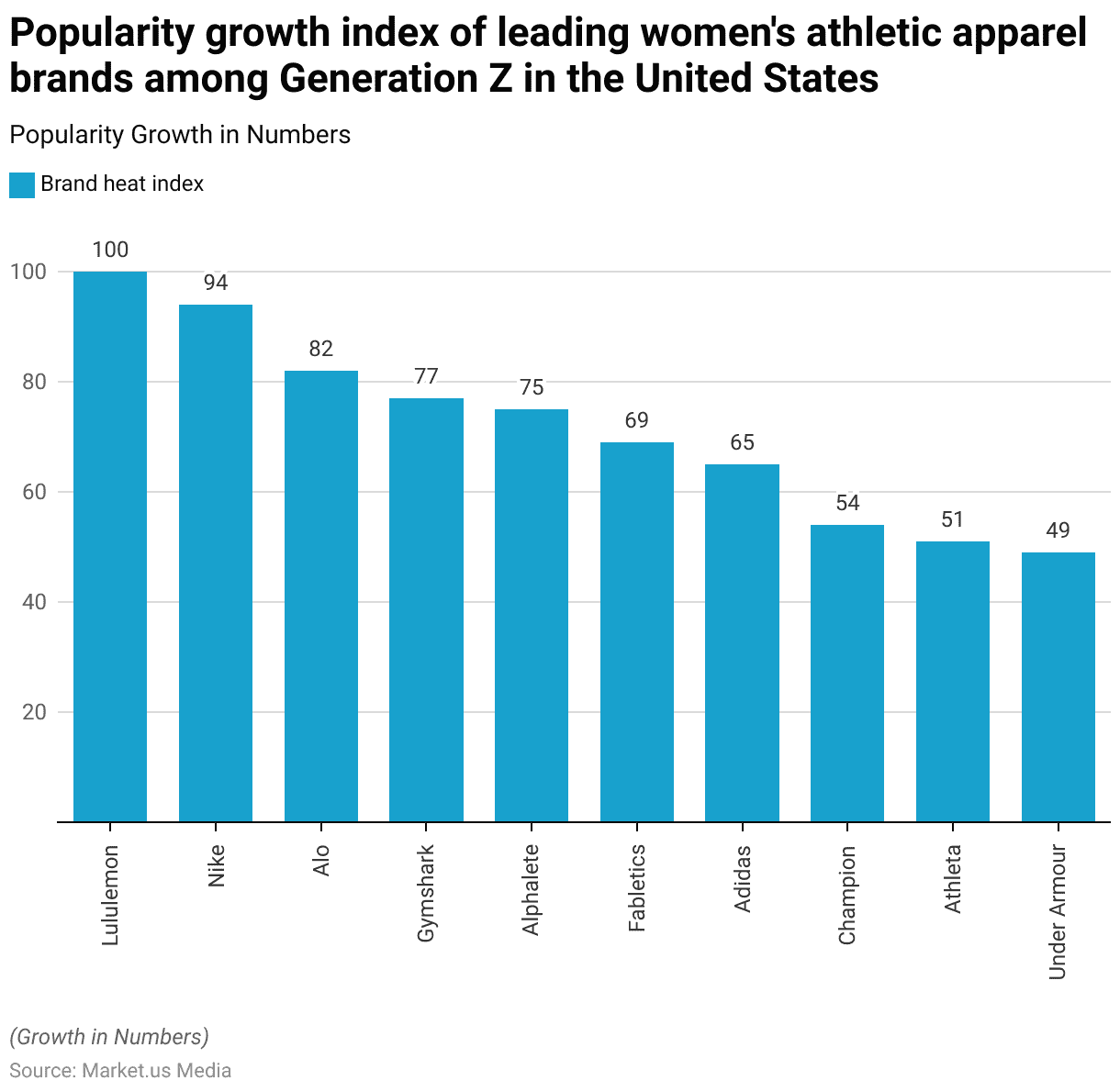

- In 2024, among Generation Z in the United States, the popularity of leading women’s athletic apparel brands was quantified through a ‘Brand Heat Index’, highlighting the preferences and trends within this demographic.

- Lululemon topped the chart with a perfect score of 100, affirming its premier status and strong appeal among young consumers. Nike closely followed with a score of 94, underscoring its enduring popularity and significant influence in the athletic apparel market.

- Alo and Gymshark also demonstrated substantial popularity, with scores of 82 and 77, respectively, indicating their successful resonance with the Gen Z audience, likely due to their trendy designs and marketing strategies.

- Alphalete and Fabletics, with scores of 75 and 69, reflected a solid preference among the younger crowd, suggesting that their targeted marketing and product offerings were well-received.

- Adidas, with a score of 65, and Champion, at 54, showed moderate popularity. Both brands have a long-standing presence in the market, and their scores reflect a stable but less pronounced appeal among Gen Z consumers.

- Athleta and Under Armour rounded out the list with scores of 51 and 49, respectively, indicating a need to potentially revamp their strategies to better connect with this dynamic and influential demographic.

- This index serves as a crucial indicator of brand performance and perception among one of the most trend-sensitive and purchasing-powerful age groups.

(Source: Statista)

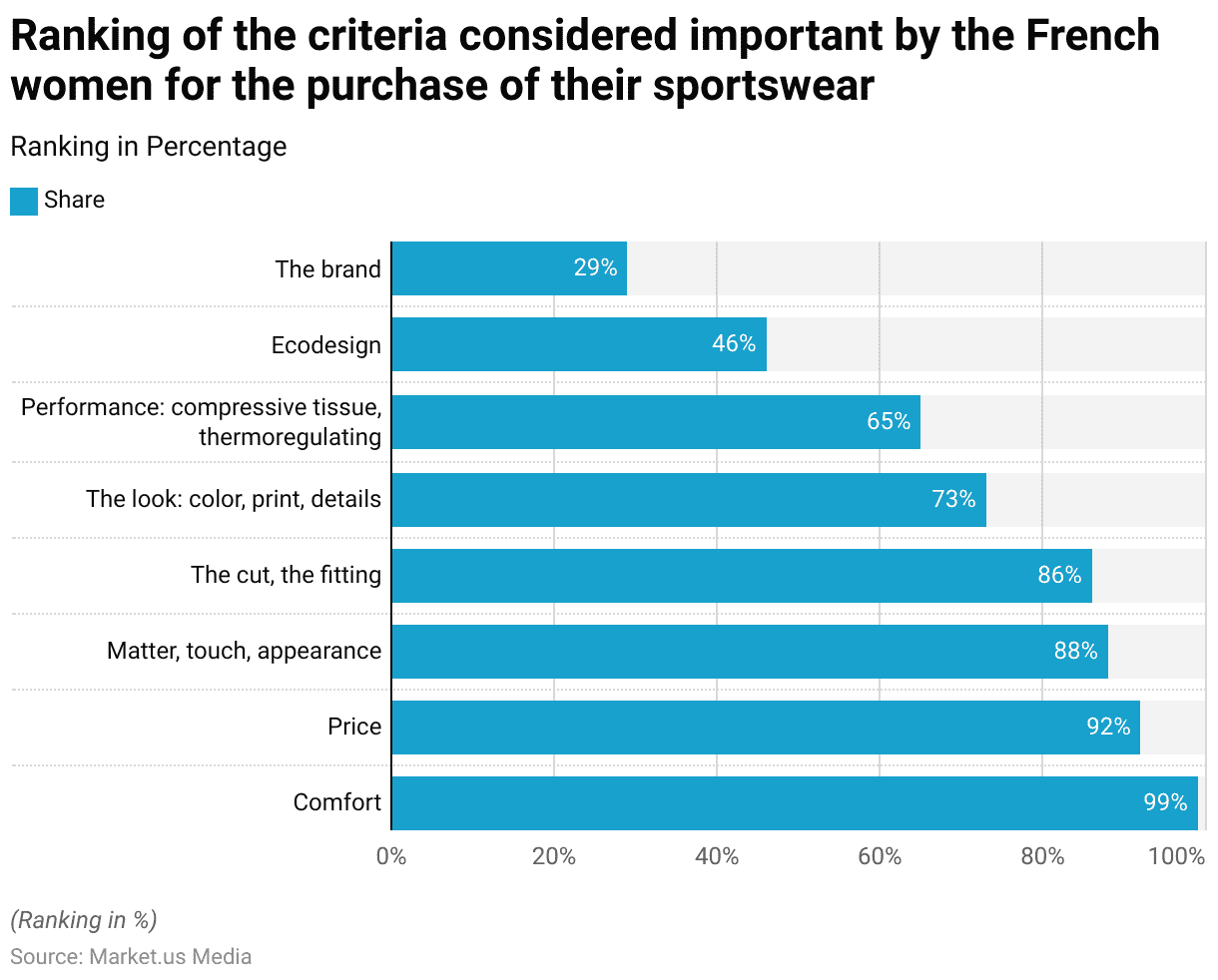

Sportswear: The Most Important Criteria for Women

- In 2016, a survey focusing on the preferences of French women regarding sportswear revealed a distinct hierarchy of criteria they consider when making purchases.

- Comfort was overwhelmingly the most valued aspect, with 99% of respondents highlighting it as crucial, emphasizing its paramount importance in sportswear selection.

- Price was a significant consideration for 92% of the participants, indicating a strong preference for finding a balance between cost and quality.

- Material quality, including touch and appearance, was important for 88% of the women, closely followed by the fit and cut of the sportswear, which was important for 86% of respondents. This suggests that aesthetic details and comfort in wear are nearly as vital as the overall feel of the material.

- The visual appeal, including color, print, and other design details, was prioritized by 73% of the respondents, showing a substantial interest in the stylistic elements of sportswear.

- Performance features such as compressive tissues and thermoregulation were considered important by 65% of the respondents, indicating that functionality also plays a significant role in their purchasing decisions.

- Eco-design was important to 46%, reflecting a growing awareness and preference for sustainability in clothing choices.

- Lastly, brand name was the least important factor, with only 29% considering it a significant criterion, which shows that brand identity holds less sway over practical factors like comfort, price, and material quality.

(Source: Statista)

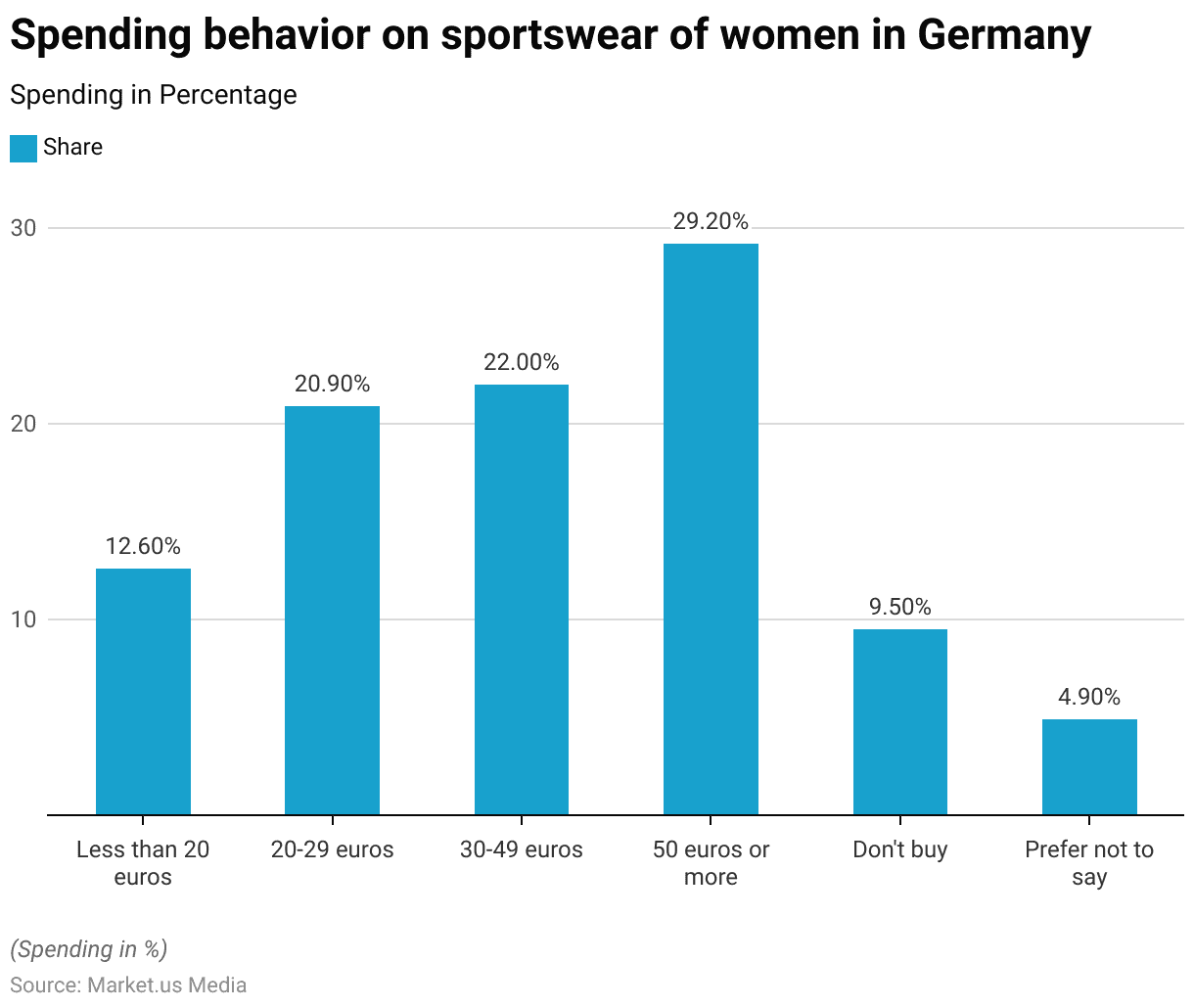

Spending Behavior on Sportswear of Women

- In 2011, a survey examining the spending behavior of women in Germany on sportswear revealed varied patterns.

- The largest share of respondents, 29.20%, reported spending 50 euros or more on sportswear, indicating a willingness to invest in higher-priced items, possibly due to perceived quality or brand preference.

- The next largest group, 22.00%, spent between 30 to 49 euros, showing a preference for mid-range priced sportswear, which could reflect a balance between quality and affordability.

- Furthermore, 20.90% of women spent between 20 and 29 euros, and a smaller portion, 12.60%, spent less than 20 euros.

- These figures suggest that while a significant number of consumers are looking for affordability, a considerable amount of consumers still prioritize more substantial spending on sportswear.

- Additionally, 9.50% of respondents indicated they do not buy sportswear at all, which could be due to a lack of interest or need.

- Meanwhile, 4.90% preferred not to disclose their spending habits. This data provides insight into the diverse financial commitments German women are willing to make regarding their sportswear purchases.

(Source: Statista)

Key Investment Trends

R&D Spending by Sportswear Players

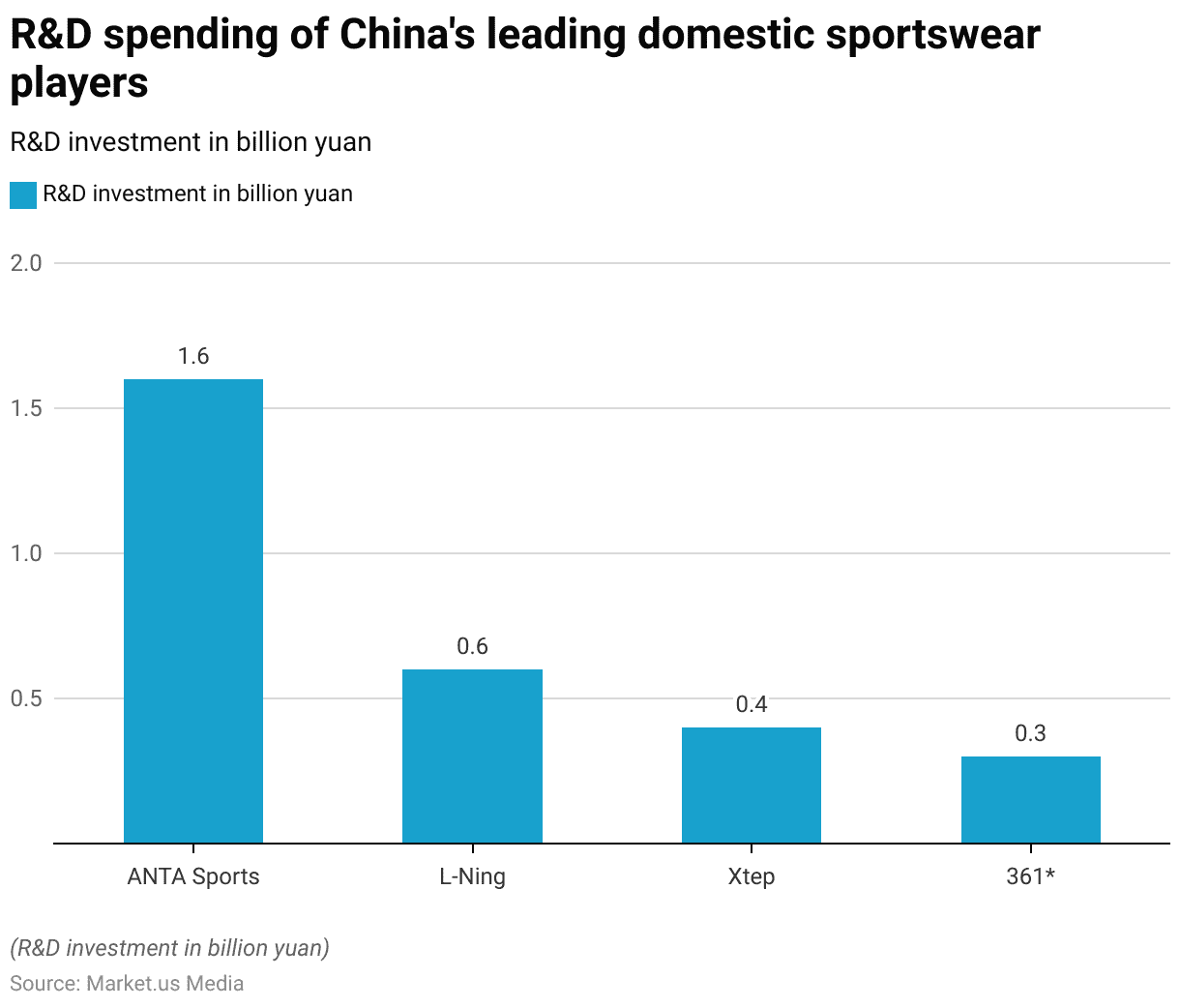

- In 2023, China’s major domestic sportswear brands demonstrated varying levels of investment in research and development (R&D), reflecting their commitment to innovation and product development.

- ANTA Sports led the pack with a substantial R&D investment of 1.6 billion yuan, underscoring its position as a leader in advancing sportswear technology and design.

- L-Ning followed with a significant but lower investment of 0.6 billion yuan, indicating a strong but more conservative approach to R&D compared to ANTA.

- Xtep also made notable investments in R&D, allocating 0.4 billion yuan, which reflects its efforts to enhance product offerings and compete effectively in the market.

- Meanwhile, 361 invested the least among the noted brands, with an R&D expenditure of 0.3 billion yuan.

- This investment strategy highlights different priorities and resources available to each brand to enhance its competitiveness through innovation.

(Source: Statista)

YoY R&D Investment Growth of Sportswear Players

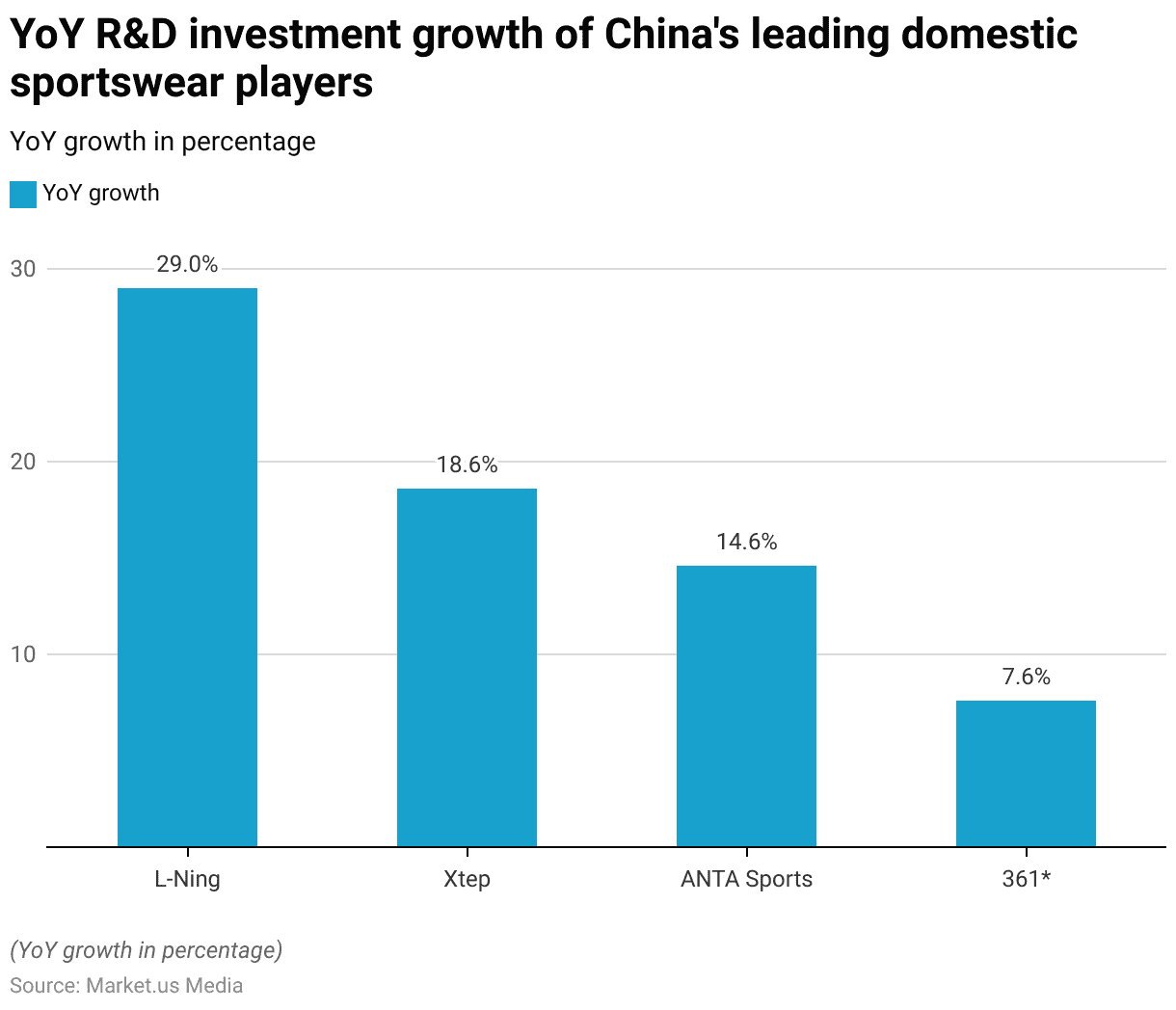

- In 2022, the annual growth rates in research and development (R&D) investments among China’s major domestic sportswear brands showcased diverse commitments to innovation.

- L-Ning led the charge with an impressive year-over-year (YoY) growth of 29% in its R&D investments, indicating a strong focus on enhancing its product lines and technological capabilities.

- Xtep also demonstrated a significant investment in innovation, recording an 18.60% increase in its R&D spending, reflecting its strategic intent to bolster product development.

- ANTA Sports followed with a solid 14.60% growth in R&D investments, suggesting a steady commitment to advancing its sports technology and materials.

- On the other hand, 361 displayed the most modest increase, with only a 7.60% growth in R&D spending, pointing to a more cautious approach to investment in new developments compared to its competitors.

- This range of investment growth rates highlights the varying strategies and priorities within the competitive landscape of Chinese sportswear manufacturers.

(Source: Statista)

Regulations for Athleisure Products

- In the market research analysis of global regulations impacting athleisure products, various legal frameworks are evident across different countries, shaping the industry’s operational dynamics significantly.

- In the European Union, athleisure products must adhere to REACH regulations that restrict hazardous substances, and the General Product Safety Directive (GPSD) mandates risk assessments for all products to ensure consumer safety.

- Moreover, new regulations like the Sustainable Product Initiative and the Digital Product Passport are set to transform design and supply chain processes to enhance sustainability and digitalization.

- In the United States, athleisure wear is subjected to rigorous standards, including ASTM testing for textile products and California Proposition 65, which requires warning labels for products containing harmful chemicals.

- There is also an emphasis on energy efficiency and radiofrequency compliance for fitness equipment under the FCC regulations and the Energy Conservation Program.

- Asia, particularly China, focuses on patent protection with its distinct system for utility and invention patent applications, highlighting the importance of IP in athleisure product development and positioning.

- Collectively, these regulations necessitate a robust compliance strategy for manufacturers and importers in the athleisure sector to mitigate risks associated with non-compliance, thus ensuring market access and consumer safety globally.

(Source: Compliance Gate, FashionUnited, Finnegan, Leading IP+ Law Firm)

Athleisure Product Innovations

- In recent developments within the athleisure industry, a strong emphasis on merging functionality with high-fashion trends is evident.

- Innovations include the introduction of Omorpho‘s micro-weighted training gear, which caters to a growing interest in strength training and outdoor activities.

- This gear, which includes vests, shorts, leggings, and shirts, incorporates small weights to enhance workout efficiency.

- Another noteworthy innovation comes from Tighties, a brand leveraging the BOA Fit System to offer precision-fit sportswear that aids in pain relief, muscle strengthening, and active recovery. These resistance leggings and other specialized apparel support athletic performance while ensuring comfort.

- Moreover, the luxury sector is also converging with athleisure, with high-profile collaborations between luxury fashion brands and traditional sports brands, such as Gucci’s partnership with Adidas. These collaborations are tailoring athleisure items that deliver both comfort and style, aiming to make luxury brands more accessible and appealing to daily consumers.

- This trend highlights the shift towards lifestyle-oriented sportswear that promises both aesthetic appeal and practicality, reshaping how luxury and leisurewear intersect in today’s fashion market.

- These innovations reflect a broader industry trend towards garments that serve dual purposes, satisfying the demands for style, comfort, and functionality in various consumer segments.

(Sources: Athletech News, Mintel)

Recent Developments

Acquisitions and Mergers:

- Nike acquires RTFKT Studios: In 2023, Nike acquired RTFKT Studios, a company specializing in virtual sneakers and digital apparel, for $200 million. This acquisition aims to strengthen Nike’s digital and athleisure offerings by merging the physical and virtual worlds, targeting the growing demand for wearable tech and digital fashion.

- Lululemon acquires Mirror: In 2023, Lululemon completed the acquisition of Mirror, an at-home fitness company, for $500 million. This move is intended to diversify Lululemon’s athleisure portfolio by integrating digital fitness offerings with its apparel business, offering a complete fitness lifestyle solution.

New Product Launches:

- Adidas launches “Made to Be Remade” line: In early 2024, Adidas introduced its new “Made to Be Remade” athleisure collection. The line features 100% recyclable materials, allowing customers to return used products for new items. This sustainable approach reflects Adidas’ commitment to eco-friendly athleisure, with the collection expected to account for 10% of sales by 2025.

- Puma launches Exhale Yoga Collection: In mid-2023, Puma launched the Exhale Yoga Collection, designed in collaboration with celebrity ambassador Cara Delevingne. The collection focuses on comfortable, eco-conscious materials and is part of Puma’s broader push into the wellness and athleisure segment.

Funding:

- Vuori raises $400 million from SoftBank: In 2023, Vuori, a California-based athleisure brand, secured $400 million in funding from SoftBank’s Vision Fund to expand globally. The funding will be used to open new retail locations and expand its e-commerce platform in Asia and Europe.

- Outdoor Voices raises $60 million: In early 2024, Outdoor Voices, an athleisure brand focusing on recreational apparel, raised $60 million in Series C funding. The investment will be used to enhance their direct-to-consumer sales model and further develop their sustainable athleisure product line.

Technological Advancements:

- Wearable technology integration: By 2025, 30% of athleisure apparel is expected to feature integrated wearable technology, such as fitness tracking and performance monitoring sensors, reflecting the merging of fitness technology with fashion.

- Sustainable fabric innovations: Eco-friendly materials are driving growth in athleisure. By 2026, 35% of athleisure products are projected to be made from recycled or sustainable materials, in response to increasing consumer demand for environmentally conscious fashion.

Conclusion

Athleisure Industry Statistics – The athleisure industry has boomed over the last decade, transforming from a niche to a major fashion trend due to shifts toward casual, versatile clothing suitable for both fitness and daily wear.

Driven by growing health awareness and more relaxed work environments, the sector has seen rapid expansion, outpacing traditional apparel markets and fueling innovation across brands.

Both established sportswear giants and newer fashion brands have broadened their ranges, incorporating advanced, sustainable materials and technologies like smart fabrics.

With its solid economic performance and alignment with contemporary lifestyles, the athleisure market is set to continue its growth, especially as remote work influences dress codes, ensuring fashion and functionality remain intertwined.

FAQs

Athleisure refers to clothing designed for workouts and other athletic activities that are also worn in other settings, such as during work, casual, or social occasions.

Athleisure has grown in popularity due to a shift in lifestyle towards health and fitness, coupled with the rise of more casual dress codes in workplaces and social settings. Its comfort and style make it a versatile choice for everyday wear.

Key drivers include increased health consciousness, the integration of fitness into daily life, advancements in fabric technology, and a blending of fashion and function that appeals to a broad consumer base.

While specific numbers can fluctuate, the athleisure market has seen significant growth globally. It continues to expand as more brands enter the space and existing brands increase their offerings.

Major players include traditional sportswear brands like Nike, Adidas, and Under Armour, as well as specialized athleisure brands like Lululemon and newer entrants like Gymshark.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)