Table of Contents

Overview

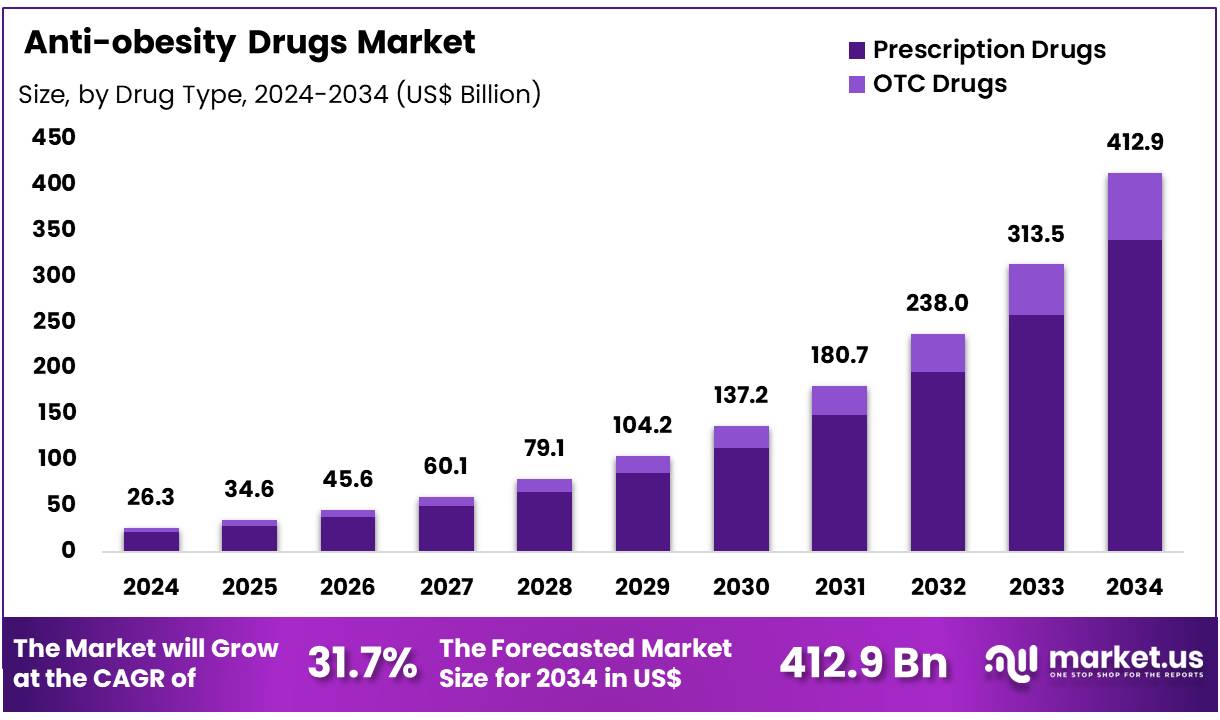

New York, NY – Dec 09, 2025 – Global Anti-obesity Drugs Market size is forecasted to be valued at US$ 412.9 Billion by 2034 from US$ 26.3 Billion in 2024, growing at a CAGR of 31.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 46.40% share with a revenue of US$ 12.2 Billion.

The anti-obesity drugs market is experiencing accelerated expansion as the global prevalence of obesity continues to rise. The market value has been supported by increasing awareness regarding weight management, a growing emphasis on preventive healthcare, and the strong clinical performance of next-generation therapeutic agents. The demand for safe and effective pharmacological interventions has gained momentum as obesity has been associated with diabetes, cardiovascular disease, and other chronic conditions.

The market growth has been further strengthened by the development of GLP-1 receptor agonists, which have demonstrated significant weight-reduction outcomes in clinical trials. Rising healthcare expenditure, improved reimbursement structures, and expanding access to innovative drugs across emerging economies have contributed to widespread adoption. Regulatory approvals for novel formulations have continued to shape the competitive landscape, while major pharmaceutical companies have been investing in research initiatives aimed at improving efficacy and minimizing adverse effects.

Strategic collaborations, pipeline advancements, and increasing physician recommendations are anticipated to support market penetration over the forecast period. The shift toward personalized treatment and the growing use of digital health platforms for obesity management have introduced new opportunities for industry stakeholders. The market outlook remains positive as clinical innovation and patient demand continue to align.

The anti-obesity drugs market is expected to record sustained growth, driven by rising obesity rates and the strong performance of breakthrough therapies. Continued investment in R&D and supportive regulatory pathways are likely to reinforce the market’s long-term development.

Key Takeaways

- In 2024, the anti-obesity drugs market generated US$ 26.3 billion in revenue, registered a CAGR of 31.7%, and is projected to reach US$ 412.9 billion by 2034.

- Prescription drugs dominated the drug type segment, accounting for 82.3% of the market in 2024.

- By mechanism of action, Peripherally Acting Drugs contributed the largest share at 58.5% in 2024.

- The injectable route of administration generated the highest revenue, holding 75.9% of the market in 2024.

- By patient type, Adults accounted for the majority share at 95.3% in 2024.

- Among distribution channels, Retail Pharmacies represented the leading segment with 56.70% share in 2024.

- North America held the largest regional share, capturing 46.40% of the global market in 2024.

Segmentation Analysis

- Drug Type Analysis: Prescription anti-obesity drugs held 82.3% of the 2024 market, supported by demand for validated therapies. GLP-1 agonists like semaglutide and liraglutide enable 15–20% weight loss, reinforcing obesity’s recognition as a chronic disease, especially among high-BMI patients with comorbidities.

- Mechanism of Action Analysis: Peripherally acting drugs captured 58.5% of the 2024 market. Agents like orlistat inhibit gastrointestinal fat absorption, offering favorable safety with minimal central effects. Their tolerability broadens patient adoption, although gastrointestinal reactions persist as common adverse events.

- Route of Administration Analysis: Injectable formulations generated 75.9% of 2024 revenue due to strong clinical outcomes of GLP-1 therapies such as semaglutide and tirzepatide. Wider availability, including launches in emerging markets, and superior efficacy over oral options strengthen preference for sustained-delivery injectable products.

- Patient Type Analysis: Adults accounted for 95.3% of the market in 2024, driven by high obesity prevalence and associated comorbidities. Evidence linking GLP-1 drugs with reduced dementia risk in diabetic adults, particularly older women, reinforces their expanding role in chronic disease management.

- Distribution Channel Analysis: Retail pharmacies held 56.7% of the 2024 market, supported by broad accessibility, counseling services, and digital integration. Strong presence of retail chains and home-delivery options enhances adherence, positioning pharmacies as the primary access point for prescription and OTC obesity treatments.

Regional Analysis

North America maintained its leadership in the anti-obesity drugs market in 2024, capturing a 46.4% share. This position has been driven by high obesity prevalence, well-established healthcare systems, and substantial healthcare expenditure. The United States, in particular, reported strong uptake of GLP-1 receptor agonists such as semaglutide and tirzepatide.

According to the latest KFF Health Tracking Poll, 12% of adults have used a GLP-1 agonist, with 6% currently using one. Usage was significantly higher among individuals with chronic conditions, reaching 43% among adults with diabetes, 25% among those with heart disease, and 22% among those recently diagnosed as overweight or obese. Public awareness has increased steadily, with 32% of adults reporting high awareness in 2024, up from 19% in mid-2023.

The Asia Pacific region is expected to register the highest CAGR over the forecast period. Rising obesity rates in China, India, and Japan have elevated demand for effective weight-management therapies. A Novotech report indicated that China is now the second-most-active country for obesity clinical trials after the United States, despite a lower national obesity rate. The launch of Wegovy in India and the anticipated entry of generic semaglutide after 2026 are expected to further accelerate market expansion across the region.

Use Cases

- Adolescent Obesity Management: In 2024, semaglutide use among U.S. adolescents increased notably, with first-time prescriptions rising from 9.9 to 14.8 per 100,000. Utilization among obese teens without diabetes reached 0.9%, reflecting a near-doubling from the previous year.

- Chronic Disease Prevention in Adults: Semaglutide (Wegovy) demonstrated measurable cardiovascular protection, reducing major adverse cardiovascular events to 6.5% compared with 8% in the placebo group, based on evidence from a large 17,600-patient clinical investigation.

- Weight Loss in Non-Diabetic Adults: Clinical findings indicated that GLP-1 receptor agonists produced 6.1–7.4% weight reduction in overweight adults without diabetes, a higher response compared with the 4–6.2% weight loss observed among adults living with diabetes.

- Long-Term Adherence Patterns: One-year treatment persistence showed clear variation, with semaglutide (Ozempic) achieving 47.1% adherence compared with 19.2% for liraglutide (Saxenda). These adherence trends directly influence real-world therapeutic effectiveness.

- Population-Level Obesity Impact: U.S. adult obesity prevalence declined by approximately 2% between 2020 and 2023, coinciding with rising GLP-1 drug uptake, which reached nearly 6% of the national adult population.

Frequently Asked Questions on Anti-obesity Drugs

- How do anti-obesity drugs work?

These drugs operate through mechanisms that influence appetite pathways, metabolic regulation, or fat absorption. Appetite suppression, delayed gastric emptying, and reduced caloric uptake are commonly observed effects, contributing to progressive weight loss in clinically supervised treatment conditions. - Who is eligible to use anti-obesity drugs?

Eligibility is typically defined for adults with obesity or individuals with overweight conditions accompanied by comorbidities. Prescription decisions are based on body mass index thresholds and clinical assessments conducted by qualified healthcare professionals. - Are anti-obesity drugs safe for long-term use?

Long-term safety is evaluated through controlled clinical studies, and approved drugs demonstrate acceptable benefit-risk profiles. Regular medical supervision is recommended because consistent monitoring assists in managing potential side effects and optimizing treatment adherence and effectiveness. - Can anti-obesity drugs be used alongside lifestyle interventions?

These drugs are typically prescribed as part of a combined management plan that includes dietary adjustments and physical activity. Clinical outcomes indicate that pharmacotherapy produces stronger weight-loss results when accompanied by structured behavioral and nutritional interventions. - Which drug classes dominate the anti-obesity drugs market?

Glucagon-like peptide-1 receptor agonists and combination appetite-regulating therapies currently dominate due to their strong efficacy profiles. Their increasing prescription rates have significantly influenced overall revenue growth and shaped competitive dynamics within the global market. - Which regions lead in market share?

North America maintains the largest market share because of high obesity rates, strong reimbursement systems, and rapid uptake of innovative pharmacotherapies. Europe follows, while Asia-Pacific exhibits accelerated growth driven by expanding healthcare access and rising awareness. - How is demand changing among consumers and healthcare providers?

Demand has been increasing due to heightened awareness of obesity-related risks, growing confidence in pharmacotherapy outcomes, and physician preference for evidence-based treatment options. Broader acceptance of newer agents has strengthened prescription volumes across multiple markets.

Conclusion

The anti-obesity drugs market has been characterized by robust expansion, supported by rising obesity prevalence, strong clinical outcomes of GLP-1 therapies, and increasing healthcare awareness. The dominance of prescription drugs, particularly injectable formulations, has reinforced the market’s clinical strength and commercial performance.

Regional growth has been led by North America, while Asia Pacific is projected to accelerate due to expanding access and rising trial activity. Broadening therapeutic applications, improved adherence trends, and supportive regulatory pathways are expected to sustain long-term development. Continued R&D investment and growing patient acceptance are likely to reinforce a positive market trajectory over the forecast period.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)