Table of Contents

Overview

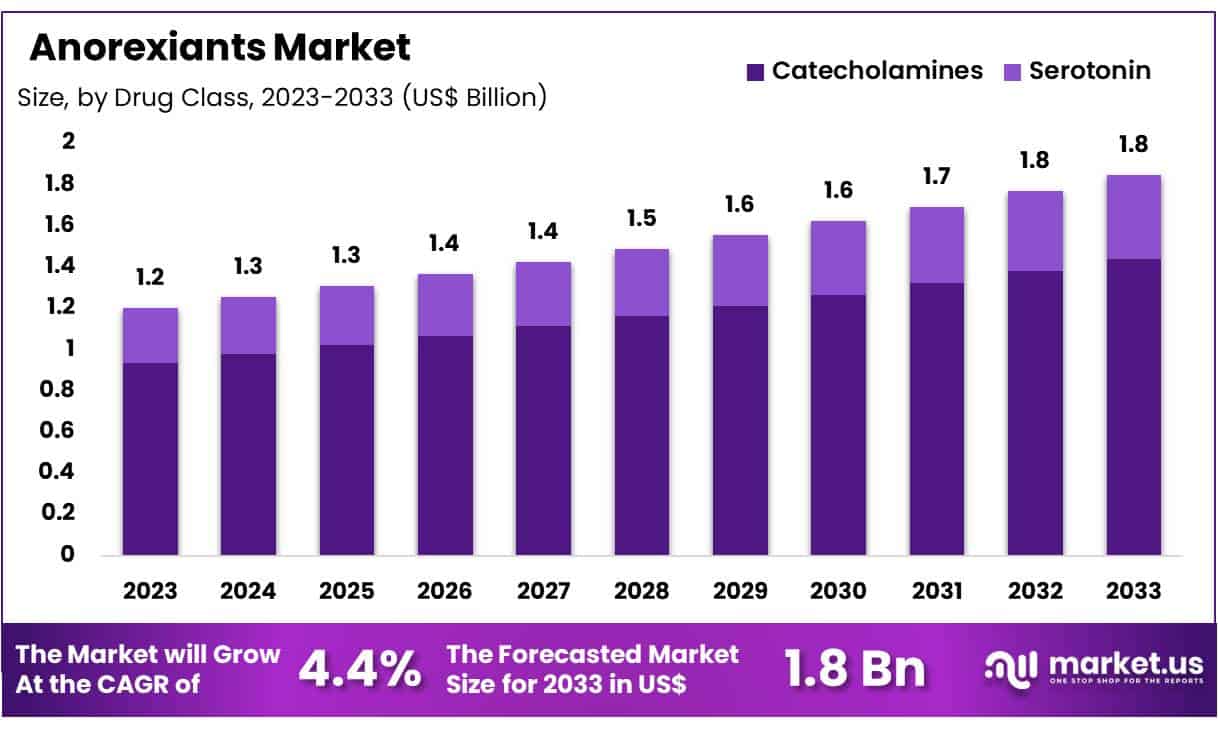

New York, NY – May 19, 2025 – Global Anorexiants Market size is expected to be worth around US$ 1.8 Billion by 2033 from US$ 1.2 Billion in 2023, growing at a CAGR of 4.4% during the forecast period from 2024 to 2033.

The global anorexiants market is experiencing steady growth, driven by rising obesity rates and increasing awareness of weight management solutions. Anorexiants, also known as appetite suppressants, are pharmacological agents that reduce appetite and food intake. These medications are commonly prescribed as part of a comprehensive weight-loss plan for individuals struggling with obesity and overweight conditions, especially when diet and exercise alone are insufficient.

The rising prevalence of obesity-related comorbidities such as type 2 diabetes, cardiovascular disorders, and metabolic syndrome has further accelerated the demand for effective anti-obesity therapies. According to the World Health Organization (WHO), worldwide obesity has nearly tripled since 1975, with over 1.9 billion adults categorized as overweight in 2022, of which more than 650 million were obese.

Prescription anorexiants, such as phentermine and diethylpropion, are regulated due to potential side effects and the risk of dependence, requiring careful medical supervision. Recent advancements in drug development have introduced newer formulations with improved safety profiles and reduced side effects, which are likely to support market expansion.

North America currently leads the market due to high obesity rates, a favorable reimbursement landscape, and ongoing clinical research. Meanwhile, Asia-Pacific is expected to witness significant growth, fueled by urbanization, changing dietary habits, and increasing healthcare access. The anorexiants market is projected to expand further as regulatory bodies approve new weight management drugs and global health initiatives promote obesity prevention and treatment.

Key Takeaways

- Market Size: The global anorexiants market is projected to increase from approximately USD 1.2 billion in 2023 to around USD 1.8 billion by 2033.

- Market Growth: The market is anticipated to expand at a compound annual growth rate (CAGR) of 4.4% between 2024 and 2033.

- Drug Class Analysis: Catecholamines, including key stimulants such as phentermine and phentermine/topiramate ER, account for the largest share, representing 78% of the market in 2023.

- Route of Administration Analysis: Oral formulations continue to dominate the market, capturing 86% of the total share due to ease of administration and patient preference.

- End-Use Analysis: Hospitals and clinics emerged as the leading end-users, contributing to 29% of the total market revenue in 2023.

- Regional Analysis: North America led the global anorexiants market in 2023, holding a dominant share of 42%, supported by high obesity prevalence and advanced healthcare infrastructure.

Segmentation Analysis

- Drug Class Analysis: The anorexiants market is classified into catecholamines, serotonin-based drugs, and other appetite suppressants. Catecholamines lead the segment with a 78% market share, owing to their high efficacy, affordability, and CNS-stimulating effects. Serotonin-based drugs like lorcaserin are gaining traction for their appetite-suppressing properties, particularly among patients who cannot tolerate stimulants. Rising obesity prevalence and ongoing drug development are expected to support sustained growth across all segments, reinforcing the market’s clinical and commercial potential.

- Route of Administration Analysis: Oral administration dominates the anorexiants market with an 86% share, attributed to its ease of use, accessibility, and cost-effectiveness. Tablets and capsules remain preferred by both patients and providers, enabling daily compliance and wide adoption. Subcutaneous injections, such as liraglutide, serve as a niche but expanding segment, especially among patients requiring enhanced efficacy. While oral drugs maintain strong preference, injectable formulations are gaining momentum in chronic obesity treatment plans, supporting dual-segment market growth.

- End-Use Analysis: Hospitals and clinics account for 29% of the anorexiants market, driven by their role in obesity diagnosis and prescription-based therapy. Institutional sales follow, supported by bulk purchases in specialized centers. Retail sales remain vital due to consistent demand for ongoing treatment. Online pharmacies are rapidly expanding, fueled by digital access and competitive pricing. Together with smaller channels like wellness centers, these end-use segments reflect growing adoption of anorexiants in both clinical and consumer-directed settings.

Market Segments

By Drug Class

- Catecholamines

- Serotonin

By Route of Administration

- Oral

- Subcutaneous

By End User

- Institutional Sales

- Hospitals & Clinics

- Retail Sales

- Online Pharmacies

- Others

Regional Analysis

North America accounted for a leading 42% share of the global anorexiants market in 2023, primarily driven by a high obesity prevalence and related comorbidities. Data from the CDC indicates that over 40% of U.S. adults are classified as obese, fueling strong demand for pharmacological weight management solutions. The region’s well-established healthcare infrastructure, easy access to FDA-approved anorexiant drugs, and active public health awareness initiatives further support market expansion.

In addition, substantial investments in obesity research and treatment programs continue to enhance therapeutic options. The rising adoption of non-stimulant anorexiants and advanced weight-loss medications in both the U.S. and Canada reinforces the region’s market leadership. These combined factors are expected to ensure continued dominance and consistent growth of the North American anorexiants market.

Emerging Trends

- Severe Obesity Increase Despite Stable Obesity Rates: While overall adult obesity prevalence in the United States stabilized at approximately 40.3% from August 2021 to August 2023, the rate of severe obesity rose from 7.7% to 9.7% over the same period. This indicates a shift toward higher-risk patient populations requiring more intensive interventions.

- Rising Prescriptions of Anorexiant Medications: Prescriptions for obesity drugs, including phentermine, semaglutide, and tirzepatide, grew at an average annual rate of 5.3% between 2017 and 2024. The number of prescriptions increased from 760,000 in July 2017 to 1.51 million by February 2024, reflecting broader clinical adoption of pharmacologic weight-management therapies.

- Expansion of FDA Approvals Beyond Weight Loss: In March 2024, semaglutide 2.4 mg (Wegovy) received FDA approval not only for weight management but also for reducing cardiovascular risk in adults with obesity or overweight and preexisting cardiovascular disease. This represents a trend toward positioning anorexiants as multi-benefit therapies in chronic disease management.

- Growth of Telehealth and Compounded Formulations: Following the end of official shortages of branded GLP-1 anorexiants, compounding pharmacies and telehealth providers have continued to supply alternative formulations. Between January and April 2025, the FDA received over 520 adverse-event reports related to compounded semaglutide and 480 for compounded tirzepatide, underscoring both the scale of off-label use and emerging safety considerations.

Use Cases

- Adult Weight-Management Therapy: Anorexiants are prescribed as first-line pharmacologic treatments for adults with obesity (BMI ≥ 30 kg/m²) or overweight (BMI ≥ 27 kg/m²) with comorbidities. The marked increase to 1.51 million obesity-drug prescriptions by February 2024 highlights widespread clinical uptake for long-term weight-control strategies.

- Management of Severe Obesity: Patients with severe obesity (BMI ≥ 40 kg/m²) have increasingly been targeted for anorexiant therapy, given their higher risk of cardiometabolic complications. With severe obesity prevalence now at 9.7% of U.S. adults, these drugs are critical for reducing morbidity in this high-risk cohort.

- Cardiovascular Risk Reduction in Obese Patients: Since March 2024, semaglutide 2.4 mg has been formally indicated to lower major adverse cardiovascular events in adults with obesity or overweight and established cardiovascular disease. This use case extends anorexiants beyond weight loss to direct heart-protection roles in approximately 40% of obese patients with CVD.

- Telehealth-Enabled Personalized Dosing: The proliferation of telemedicine platforms has enabled tailored anorexiant regimens, often via compounded formulations when commercial products are inaccessible or unaffordable. However, the FDA’s receipt of over 1,000 adverse-event reports for compounded semaglutide and tirzepatide through April 2025 signals the need for careful monitoring in these remote-prescribing models.

Conclusion

The global anorexiants market is poised for sustained growth, driven by rising obesity prevalence, expanded therapeutic applications, and evolving treatment delivery models. Advancements in drug formulations, FDA approvals for broader health benefits, and increasing adoption of telehealth are reshaping the landscape of pharmacologic weight management.

North America remains the dominant region due to robust healthcare infrastructure and high demand. Meanwhile, emerging markets offer new growth avenues. As awareness increases and treatment accessibility improves, anorexiants are expected to play an increasingly central role in addressing obesity and related health conditions across diverse patient populations worldwide.