Table of Contents

Overview

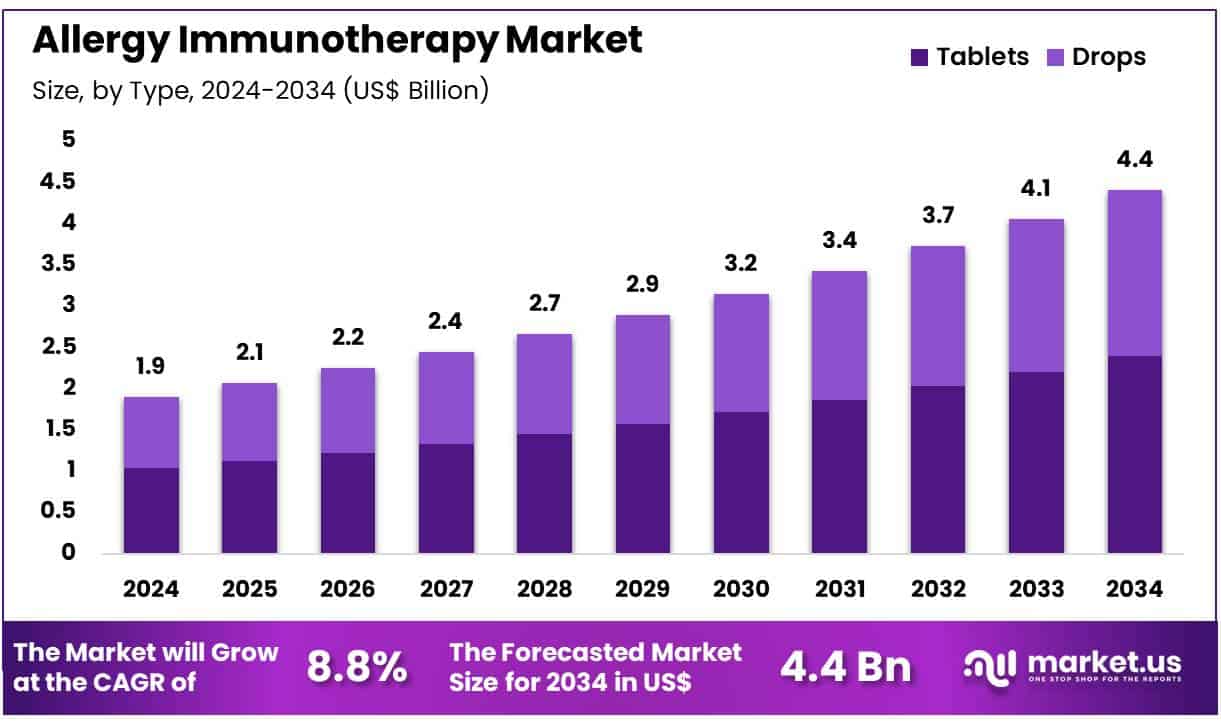

New York, NY – July 08, 2025 – Global Allergy Immunotherapy Market size is expected to be worth around US$ 4.4 Billion by 2034 from US$ 1.9 Billion in 2024, growing at a CAGR of 8.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.5% share with a revenue of US$ 0.8 Billion.

The global Allergy Immunotherapy Market is poised for significant growth over the coming decade, driven by the increasing prevalence of allergic disorders and growing awareness of long-term treatment solutions. Allergy immunotherapy, also known as desensitization or hypo-sensitization, works by gradually reducing the immune system’s sensitivity to specific allergens. It offers long-term relief from allergic symptoms such as hay fever, allergic asthma, and insect sting allergies, making it a preferred option over conventional pharmacotherapy.

Subcutaneous Immunotherapy (SCIT) and Sublingual Immunotherapy (SLIT) are the two primary delivery methods, with SLIT gaining considerable traction due to its convenience and safety profile. North America and Europe remain the dominant regions, attributed to well-established healthcare systems, high allergy diagnosis rates, and increasing R&D investments. Meanwhile, the Asia-Pacific region is projected to grow rapidly, fueled by urbanization, lifestyle changes, and rising healthcare expenditures.

The market is also witnessing innovation in allergen extracts and biologics, with several pipeline candidates under clinical trials. Moreover, regulatory support from agencies such as the FDA and EMA for allergen-specific immunotherapy products continues to foster industry growth.

Overall, the allergy immunotherapy market is expected to expand steadily, providing sustainable and cost-effective treatment solutions for millions affected by allergic diseases globally.

Key Takeaways

- In 2024, the global allergy immunotherapy market generated an estimated revenue of US$ 1.9 billion, and it is projected to reach approximately US$ 4.4 billion by 2034, expanding at a compound annual growth rate (CAGR) of 8.8% during the forecast period.

- By treatment type, subcutaneous immunotherapy (SCIT) emerged as the leading segment in 2023, accounting for 66.4% of the total market share, driven by its established clinical efficacy in long-term allergy management.

- In terms of formulation type, the market is categorized into tablets and drops, with tablets dominating the segment and capturing a 54.4% share owing to patient convenience and higher compliance.

- The allergy type segmentation highlights allergic rhinitis as the most prevalent condition treated through immunotherapy, commanding a 71.6% share of the total market in 2024, followed by allergic asthma and other allergic conditions.

- Based on distribution channel, hospital pharmacies led the market, contributing to 39.4% of the overall revenue, supported by strong clinical infrastructure and physician-led therapy administration.

- Regionally, North America maintained its dominant position in 2024, securing a 39.5% share of the global market, attributed to advanced healthcare systems, high awareness levels, and favorable reimbursement frameworks for allergy treatments.

Segmentation Analysis

- Treatment Type Analysis: Subcutaneous Immunotherapy (SCIT) remains the leading treatment approach, capturing 66.4% of the allergy immunotherapy market. Its strong clinical efficacy and long-term benefits in managing allergic rhinitis and asthma reinforce its gold-standard status. SCIT’s ability to target multiple allergens such as pollen, pet dander, and dust mites enhances its applicability. Familiarity among healthcare providers, combined with its disease-modifying potential, continues to support widespread adoption across clinical settings globally.

- Type Analysis: Tablets account for 54.4% of the market, favored for their non-invasive administration and at-home convenience. These sublingual tablets dissolve easily under the tongue, eliminating the need for frequent clinical supervision. Increased awareness about Sublingual Immunotherapy (SLIT) and patient preference for user-friendly treatment options have accelerated uptake. The availability of SLIT tablets for allergens like grass pollen and house dust mites has broadened the treatment landscape, contributing significantly to segment growth.

- Allergy Type Analysis: Allergic rhinitis dominates the allergy type segment, comprising 71.6% of market share. Its rising global incidence driven by urbanization, pollution, and climate change has increased demand for long-term treatment solutions. Symptoms such as sneezing, nasal congestion, and itchy eyes prompt patients to seek effective care. Both SCIT and SLIT therapies offer targeted options for allergic rhinitis, making immunotherapy a reliable choice for improved symptom control and enhanced patient quality of life.

- Distribution Channel Analysis: Hospital pharmacies lead the distribution channel segment with a 39.4% market share. Their infrastructure, availability of trained allergists, and capacity for personalized patient monitoring make hospitals the preferred setting for SCIT administration. Hospital-based pharmacies ensure a steady supply of approved immunotherapy products through established procurement systems. As specialized allergy care becomes more prominent, hospital pharmacies are expected to retain their pivotal role in facilitating the delivery and oversight of immunotherapy treatments.

Market Segments

By Treatment Type

- Subcutaneous Immunotherapy (SCIT)

- Sublingual Immunotherapy (SLIT)

By Type

- Tablets

- Drops

By Allergy Type

- Allergic Rhinitis

- Allergic Asthma

- Others

By Distribution Channel

- Hospital Pharmacy

- Online Pharmacy

- Retail Pharmacy

Regional Analysis

In 2024, North America led the global allergy immunotherapy market, accounting for 39.5% of total revenue. This dominance is primarily attributed to the high prevalence of allergic conditions and progressive regulatory initiatives. According to the Centers for Disease Control and Prevention (CDC), nearly 1 in 3 U.S. adults and more than 1 in 4 children reported experiencing seasonal allergies, eczema, or food allergies in 2021.

This substantial disease burden fuels the demand for long-term therapeutic solutions. Further boosting market growth, the U.S. Food and Drug Administration (FDA) expanded approvals in 2024 for certain allergy immunotherapy products, allowing broader patient access and earlier intervention. These regulatory developments, combined with robust healthcare infrastructure, continue to support the region’s market leadership.

The Asia Pacific region is projected to record the fastest CAGR during the forecast period, driven by the increasing incidence of allergies and rising healthcare expenditures. As outlined in the “Health at a Glance: Asia/Pacific 2024” report by the OECD and WHO, healthcare spending is steadily rising across the region, enabling greater investment in advanced therapies. Growing public awareness, government-led health initiatives, and improved diagnostic capabilities are expected to enhance adoption of allergy immunotherapies, reinforcing the region’s potential for sustained market growth.

Emerging Trends

- Expansion of Oral and Sublingual Therapies: The range of immunotherapy products has broadened beyond traditional injections. In July 2024, the FDA approved PALFORZIA, the first oral peanut immunotherapy for patients aged 1–17 years, to reduce the risk of severe reactions after accidental peanut exposure . Similarly, sublingual tablets for house dust mite allergy (ODACTRA) have received extended indications, allowing daily at-home dosing for adolescents and adults aged 12–65 years.

- Broader Pediatric Indications: Pediatric use of immunotherapy is growing. In 2023, clinical trials supported extending the house dust mite SLIT tablet to children aged 5–11 years, marking the final commitment trial in the US Pediatric Study Plan . This shift enables earlier intervention, which is associated with improved long-term tolerance development.

- Rising Insurance Coverage: Coverage of allergy immunotherapy has improved substantially. As of 2023, 42 out of 50 Medicaid programs offered benefits for immunotherapy under guidelines-based asthma care, up from fewer than 30 programs in 2016–2017 . This trend reduces out-of-pocket costs and supports wider patient access.

- Increasing Allergy Burden Driving Demand: The global burden of allergic rhinitis is significant, affecting an estimated 500 million people worldwide. In the US, adult asthma prevalence stands at 8.0% and 8.3% in children, with pollen exposures rising over multi-decade records. This growing patient population underpins the steady uptake of immunotherapy solutions.

Use Cases

- Peanut Allergy (Oral Immunotherapy): PALFORZIA is indicated for patients 1–17 years with a confirmed peanut allergy. It is administered in two phases—initial escalation under medical supervision, followed by home dosing—to lower the severity of reactions upon accidental exposure.

- House Dust Mite–Induced Allergic Rhinitis (Sublingual Tablets): Odactra tablets, used daily under the tongue, are approved for patients aged 12–65 years to relieve rhinitis symptoms confirmed by IgE testing to Dermatophagoides species. Pediatric extension trials for ages 5–11 are complete, poised to broaden use.

- Grass Pollen–Induced Allergic Rhinitis (Sublingual Tablets): GRASTEK® is approved for persons aged 5–65 years with Timothy grass pollen allergy. Daily sublingual dosing has been shown to reduce nasal and eye symptoms during grass pollen season.

- Long-Term Desensitization: Studies have demonstrated that multi-year subcutaneous immunotherapy (SCIT) achieves sustained symptom relief. For example, wheat-flour–sensitized workers receiving SCIT for at least four years showed significant reductions in bronchial responsiveness and skin test sensitivity.

Conclusion

The global allergy immunotherapy market is on a strong growth trajectory, driven by increasing allergy prevalence, expanding therapeutic innovations, and supportive regulatory actions. With a projected CAGR of 8.8% and expected market value of US$ 4.4 billion by 2034, the sector is witnessing greater adoption of both SCIT and SLIT therapies.

Regional growth is led by North America, while Asia Pacific shows strong potential due to rising healthcare investment. Innovations such as oral immunotherapy, broader pediatric approvals, and improved insurance coverage are enhancing treatment accessibility, making allergy immunotherapy a cost-effective, long-term solution for millions affected by allergic conditions worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)