Table of Contents

Overview

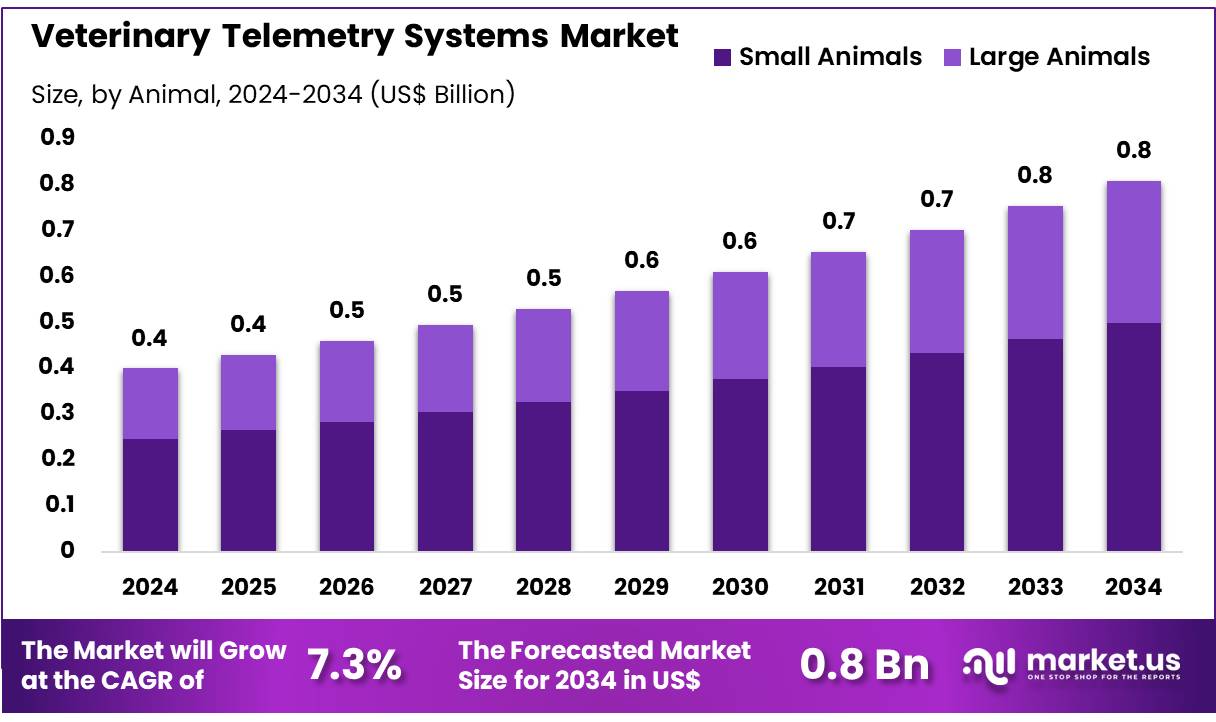

New York, NY – Dec 04, 2025 – Global Veterinary Telemetry Systems Market size is expected to be worth around US$ 0.8 Billion by 2034 from US$ 0.4 Billion in 2024, growing at a CAGR of 7.3% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.9% share with a revenue of US$ 0.2 Billion.

The global veterinary telemetry systems market has been characterized by steady expansion as advanced monitoring technologies are increasingly integrated into animal health practices. Growth has been supported by rising adoption of wireless and real-time monitoring solutions across veterinary clinics, livestock management facilities, and research institutions. The increasing incidence of chronic animal diseases and the growing emphasis on precision livestock farming have further contributed to sustained market demand.

Veterinary telemetry systems are utilized to capture physiological data such as heart rate, temperature, respiration, activity, and other critical parameters. The demand for remote and continuous monitoring has been reinforced by operational advantages, including improved diagnostic accuracy, reduced manual intervention, and enhanced animal welfare outcomes. The deployment of sensor-based devices and cloud-enabled data platforms has broadened commercial opportunities for technology providers.

North America has been observed as a leading regional market due to established veterinary infrastructure and high technology adoption. Asia–Pacific is projected to witness accelerated growth driven by expanding livestock populations, increasing pet ownership, and investments in smart farming solutions. The market has also benefited from advancements in wearable devices and telemetry-integrated diagnostic tools.

Overall, the expansion of veterinary telemetry systems has been supported by increasing digitalization in veterinary care, rising awareness of real-time health monitoring, and continuous innovation by industry stakeholders. Continued development of compact, cost-efficient, and high-accuracy telemetry solutions is expected to create favorable growth prospects for the global market.

Key Takeaways

- In 2024, the veterinary telemetry systems market generated revenue of US$ 0.4 billion, expanding at a CAGR of 7.3%, and is projected to reach US$ 0.8 billion by 2034.

- By product type, the market is segmented into vital signs monitors, wearables, ECG/EKG monitors, anesthesia machines, accessories, and others, with vital signs monitors leading at 31.3% market share in 2024.

- Based on technology, the market is categorized into compact/tabletop, floor standing, and portable systems, where compact/tabletop technology accounted for a dominant 43.1% share.

- In terms of application, the market is divided into respiratory, neurology, cardiology, and others, with the respiratory segment holding the largest share at 36.4%.

- By animal type, segmentation includes small animals and large animals, with the small animals segment leading at 61.7% revenue share.

- Under end-user segmentation, the market consists of veterinary hospitals/clinics and others, where veterinary hospitals/clinics captured 68.9% of the market.

- Regionally, North America emerged as the leading market, securing 38.9% share in 2024.

Regional Analysis

North America Leads the Veterinary Telemetry Systems Market

North America accounted for the largest revenue share of 38.9% in the veterinary telemetry systems market, supported by a heightened emphasis on comprehensive animal healthcare. The American Veterinary Medical Association (AVMA) has emphasized the importance of integrating technological advancements into veterinary practices. Findings from a 2023 AVMA survey indicated an increasing interest among veterinary professionals in remote patient monitoring to enhance care quality and streamline workflow efficiency.

Regulatory support also contributes to the region’s leadership. The U.S. FDA’s Center for Veterinary Medicine (CVM) oversees veterinary device regulation, ensuring the safety and effectiveness of telemetry systems used for animal health monitoring. This regulatory framework strengthens confidence among veterinary practitioners regarding the reliability and benefits of advanced monitoring technologies.

Asia Pacific Poised for the Highest CAGR During the Forecast Period

The Asia Pacific region is projected to record the fastest CAGR, driven by rising attention to animal health and increasing adoption of technological solutions across veterinary practices. Insights from the Asia-Pacific Veterinary Federation reflect a growing shift toward advanced digital tools in animal healthcare.

Expanding digital infrastructure further supports this trend. Mobile internet penetration continues to rise across the region. According to the Telecom Regulatory Authority of India, wireless internet subscriptions in India increased to 927.86 million in September 2024, up from 777.60 million in March 2020. This growing connectivity base enhances accessibility to remote monitoring solutions, thereby fostering greater adoption of veterinary telemetry systems across Asia Pacific.

Emerging Trends

- Rise of Wearable Biosensors: The increasing use of wearable technologies such as accelerometers, ECG electrodes, and temperature loggers has strengthened real-time monitoring in veterinary care. Recent assessments indicate that 31.6% of welfare-monitoring studies rely on wearable devices, enabling continuous physiological and behavioral data collection for early health issue detection and optimized treatment planning.

- Growth of Implantable Telemetry Devices: The adoption of implantable transmitters capable of measuring internal physiological parameters including heart rate and core temperature has accelerated across multiple species. Continued refinement of surgical implantation methods has reduced tissue damage and procedural risks, supporting high-quality physiological research and improving accuracy in veterinary clinical investigations.

- Expansion of GPS and Satellite Tracking: GPS- and satellite-enabled telemetry systems are increasingly applied beyond wildlife ecology and now support large-scale livestock management. These technologies provide real-time location and movement insights, improving grazing efficiency, biosecurity monitoring, and early disease detection across extensive production environments.

- Regulatory Support for Advanced Telemetry Technologies: The FDA’s Center for Veterinary Medicine has emphasized a science-driven, risk-based approach for evaluating emerging telemetry solutions. This regulatory endorsement is accelerating development of AI-enhanced analytics and connected monitoring platforms, facilitating smoother adoption within clinical and research domains.

Use Cases

- National-Level Health Monitoring Initiatives: The USDA’s NAHMS program is preparing its “Sheep 2024” initiative, which intends to deploy telemetry-enabled collars across a representative national flock sample. These devices will collect movement, feedlot entry, and health event data throughout early to mid-2024, supporting population-level health assessments.

- Animal Welfare Evaluation: Systematic assessments of monitoring technologies show that 52% of welfare-focused studies utilize camera-based systems, while 31.6% deploy wearable sensors. These telemetry tools enable non-invasive, near-continuous 24-hour monitoring, strengthening the identification of behavioral deviations and welfare risks in research and clinical applications.

- Heat-Stress Prediction in Swine Production: The USDA’s HotHog application integrates telemetry-style weather inputs and species-specific physiological thresholds to forecast heat stress in pigs. Developed through a five-year collaboration between ARS and academic partners, the tool provides farm-level predictions that help producers mitigate welfare and productivity losses.

- AMR Surveillance in Veterinary Environments: APHIS’s Antimicrobial Resistance Pilot Project applies telemetry-linked sample logging to monitor resistance patterns in livestock pathogens. Data collected from hundreds of isolates each quarter supports near real-time detection of emerging antimicrobial resistance trends, improving surveillance and response capabilities across veterinary settings.

Frequently Asked Questions on Veterinary Telemetry Systems

- How do veterinary telemetry systems work?

These systems operate through sensors or implanted devices that capture vital parameters and transmit encrypted signals to a monitoring platform. The process enables continuous observation without physical restraint, improving welfare conditions and enhancing accuracy of recorded physiological data. - What parameters can be monitored using these systems?

Key parameters include heart rate, blood pressure, body temperature, respiration rate, and physical activity. Advanced systems also monitor ECG, EEG, and metabolic indicators, supporting comprehensive assessments required in veterinary medicine, animal research, and pharmaceutical safety evaluations. - What benefits do telemetry systems provide to veterinarians and researchers?

These systems provide continuous, stress-free monitoring that reduces animal handling, improves data reliability, and supports early detection of physiological changes. Enhanced accuracy enables better treatment planning, welfare compliance, and scientific validity in regulated testing environments. - What types of veterinary telemetry systems exist?

Systems typically include wireless external sensors, implantable telemetry devices, wearable collars, and patch-based monitors. Each category is developed to address specific monitoring requirements, such as chronic studies, mobility allowances, environmental suitability, and data precision standards. - Which regions dominate the veterinary telemetry systems market?

North America holds a leading position due to advanced veterinary infrastructure, significant R&D activities, and strong technology adoption. Europe follows closely, while Asia-Pacific is exhibiting accelerated growth driven by expanding animal healthcare expenditure and research investments. - What are the major end-users in this market?

Primary end-users include veterinary clinics, research laboratories, academic institutions, animal hospitals, and pharmaceutical companies. These stakeholders rely on telemetry technologies to enhance diagnostic accuracy, improve welfare standards, and generate reliable data for scientific and clinical evaluations. - Which technology trends are shaping the market?

Key trends include adoption of IoT-enabled platforms, miniaturized sensors, cloud-based analytics, and AI-supported monitoring systems. These innovations improve data precision, enable predictive insights, and support seamless integration across clinical and research workflows.

Conclusion

The veterinary telemetry systems market is expected to advance steadily as digital monitoring becomes integral to animal health management. Market expansion has been supported by increased adoption of wireless sensors, rising emphasis on precision livestock farming, and the growing burden of chronic diseases in animals.

North America continues to lead due to strong technological readiness, while Asia–Pacific is projected to record the fastest growth. The development of compact, high-accuracy devices and broader use of AI-enabled platforms is anticipated to strengthen future adoption. Overall, sustained innovation and expanding applications across clinical, research, and livestock environments are expected to reinforce long-term market growth.