Table of Contents

Overview

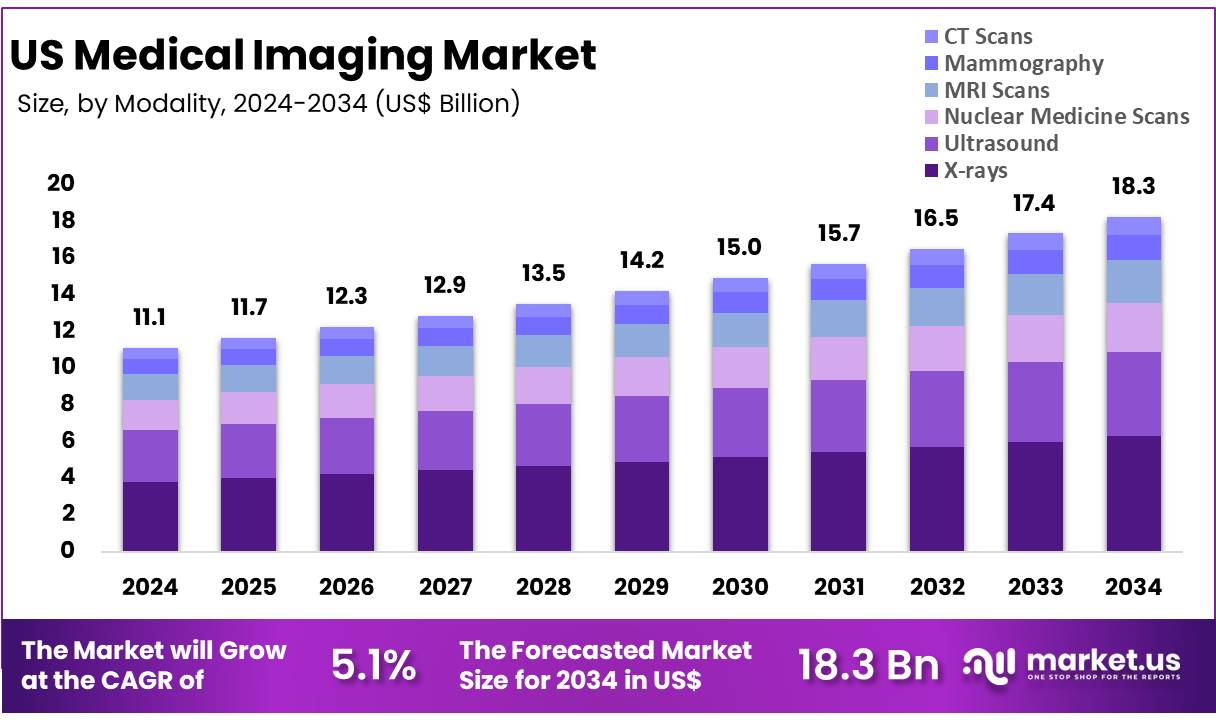

New York, NY – Dec 08, 2025 – The US Medical Imaging Market size is expected to be worth around US$ 18.3 Billion by 2034 from US$ 11.1 Billion in 2024, growing at a CAGR of 5.1% during the forecast period 2025 to 2034.

The U.S. medical imaging market has been experiencing consistent growth as healthcare providers continue to adopt advanced diagnostic technologies. The expansion of this market can be attributed to increasing demand for early disease detection, rising prevalence of chronic disorders, and continued investments in imaging infrastructure across hospitals and diagnostic centers.

Significant progress in modalities such as MRI, CT, ultrasound, and nuclear imaging has strengthened diagnostic accuracy and enhanced clinical workflows. The integration of artificial intelligence has improved image interpretation, reduced scan times, and supported physicians in delivering timely and precise diagnoses. The adoption of minimally invasive procedures has further contributed to the growing application of imaging systems in treatment planning and surgical navigation.

Growth in the market has also been supported by favorable reimbursement structures, expanded government focus on preventive care, and rising penetration of ambulatory imaging services. The high preference for technologically advanced equipment has encouraged continuous product innovation by industry leaders.

Strong demand from cardiology, oncology, neurology, and orthopedic applications is expected to sustain market momentum. The sector is positioned for continued advancement as imaging providers prioritize digital transformation, equipment modernization, and enhanced patient-care efficiency.

Key Takeaways

- In 2024, the U.S. medical imaging market generated revenue of US$ 11.1 billion, and a CAGR of 5.1% has been projected for the forecast period, with the market expected to reach US$ 18.3 billion by 2033.

- The modality landscape comprises X-rays, ultrasound, nuclear medicine scans, MRI scans, mammography, and CT scans, with X-rays leading the segment in 2024, accounting for 34.5% of total market share.

- Based on end-use, the market is segmented into hospitals, diagnostic imaging centers, and others, with hospitals dominating the market in 2024 by capturing a 62.4% share.

Market Segments

- Modality Analysis: In 2023, the X-ray segment accounted for 34.5% of the U.S. medical imaging market, supported by continuous innovation in digital X-ray and fluoroscopy systems. The rising prevalence of chronic illnesses, including cardiovascular diseases and cancer, reinforced its essential diagnostic role. Broader adoption across urban and rural healthcare settings, increasing utilization in outpatient and emergency care, and the emergence of portable imaging technologies contributed to the segment’s sustained expansion.

- End-use Analysis: Hospitals held 62.4% of the end-use market in 2023, reflecting substantial investments in advanced MRI, CT, and X-ray systems to improve diagnostic precision. Growth in patient volumes, heightened focus on early disease detection, and increasing preference for outpatient-based procedures supported hospital leadership in imaging services. The expanding integration of artificial intelligence in diagnostic workflows is expected to further elevate imaging performance and operational efficiency across hospital environments.

Emerging Trends

The adoption of artificial intelligence and machine learning within medical imaging workflows has advanced rapidly across the United States. Increasing FDA clearances for AI-driven software are supporting automated image interpretation, lesion detection, and workflow optimization, particularly in CT, MRI, and mammography. Expansion of software-as-a-medical-device solutions is expected to enhance diagnostic precision and ease radiologist workload in high-volume settings.

Standardization of health data has progressed through the U.S. Core Data for Interoperability and proposed Health IT regulations. These initiatives require the use of common data elements and FHIR-based interfaces, enabling consistent exchange of imaging reports and metadata. This development has supported broader adoption of structured reporting and real-time access to historical imaging across electronic health record platforms.

Patient safety considerations have driven stronger emphasis on radiation-dose management. National guidelines encourage low-dose CT approaches, more stringent justification of ionizing procedures, and active monitoring of cumulative exposure. Dose-tracking registries at major healthcare centers are being used to ensure compliance and reduce long-term cancer risk.

Imaging utilization in ambulatory care has continued to increase, particularly among older adults. Between 1996 and 2006, ultrasound, MRI, CT, and PET use in outpatient visits for individuals aged 55–64 grew significantly. Broader reimbursement coverage and expansion of outpatient imaging centers have supported this shift beyond traditional hospital-based diagnostic environments.

Use Cases

- Emergency Department Diagnostics: Imaging played a critical role in emergency care in 2018, with X-rays performed in 46,642 visits, CT scans in 25,437 visits, ultrasound in 7,119 visits, and MRI in 1,322 visits. These modalities enabled rapid assessment of trauma, stroke, and acute abdominal disorders, supporting timely clinical intervention.

- Ambulatory Monitoring and Follow-Up: Outpatient clinics increasingly rely on advanced imaging to support long-term disease management. Between 1996 and 2006, utilization of ultrasound, MRI, CT, and PET among patients aged 55–64 rose sharply. This adoption strengthened monitoring of cardiovascular conditions, cancer recurrence, and musculoskeletal disorders outside hospital settings.

- Vision and Eye Health Screening: Through national surveillance systems, a growing share of Medicare beneficiaries is receiving routine imaging such as optical coherence tomography and fundus photography. These tests support early identification of glaucoma and diabetic retinopathy, with claims and EHR data enabling population-level monitoring of vision health trends.

- AI-Driven Teleradiology: AI-enabled teleradiology platforms are being deployed to expand diagnostic access in underserved areas. Under FDA digital health pilot programs, deep-learning systems have been validated for stroke detection on CT scans, reducing time to diagnosis by up to 30 percent. These solutions allow expert interpretation where on-site radiologists are limited.

Frequently Asked Questions on US Medical Imaging

- Which imaging modalities are most commonly used in the United States?

The US market is dominated by X-ray, ultrasound, CT, and MRI, which are preferred due to broad clinical applications. Their adoption is supported by established healthcare infrastructure, high diagnostic demand, and continuous technological improvements that enhance accuracy and workflow efficiency. - What conditions are most frequently diagnosed through medical imaging?

Medical imaging is routinely applied for cardiovascular diseases, cancer detection, neurological disorders, musculoskeletal injuries, and abdominal conditions. These modalities support early diagnosis, guide therapeutic decisions, and enable continuous monitoring to improve patient outcomes across various clinical settings. - How is artificial intelligence used in medical imaging?

Artificial intelligence is increasingly used to automate image interpretation, reduce diagnostic errors, and optimize radiology workflows. AI-driven tools support earlier disease detection, structured reporting, and improved operational efficiency, which enhances clinical productivity within hospitals and diagnostic centers. - What factors drive demand for medical imaging services in the US?

Demand is driven by an aging population, increased prevalence of chronic diseases, widening clinical applications, and advancements in imaging technologies. Higher utilization of preventive diagnostics and improved reimbursement frameworks also contribute to sustained expansion across outpatient and inpatient settings. - How is radiation exposure managed in medical imaging?

Radiation exposure is controlled through standardized protocols, optimized equipment settings, and low-dose imaging technologies. Regulatory guidelines require providers to minimize patient risk while maintaining image quality, and continuous quality assurance processes support safety across all diagnostic environments. - Which segments dominate the US medical imaging market?

MRI, CT, and ultrasound remain dominant due to widespread clinical applications and strong reimbursement support. Equipment sales, diagnostic services, and related software solutions represent major revenue contributors, as hospitals and imaging centers invest in upgraded and efficient systems. - What trends are shaping the future of the US medical imaging market?

Key trends include AI-assisted diagnostics, portable imaging, value-based care adoption, and rising demand for minimally invasive procedures. Continued investment in high-precision modalities and patient-centric solutions is expected to reshape service delivery across hospitals and independent centers.

Conclusion

The U.S. medical imaging market is positioned for sustained expansion as healthcare providers continue to prioritize early diagnosis, technological advancement, and improved patient management. Growing demand for advanced modalities, increasing adoption of AI, and strong investment in hospital and ambulatory imaging infrastructure are reinforcing market momentum.

Favorable reimbursement policies, rising chronic disease burdens, and expanding outpatient diagnostic services further strengthen long-term growth prospects. As imaging systems become more integrated, digitalized, and patient-centric, the sector is expected to maintain steady progress, supported by ongoing innovation, improved operational efficiency, and widening clinical applications across diverse medical specialties.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)