Table of Contents

Overview

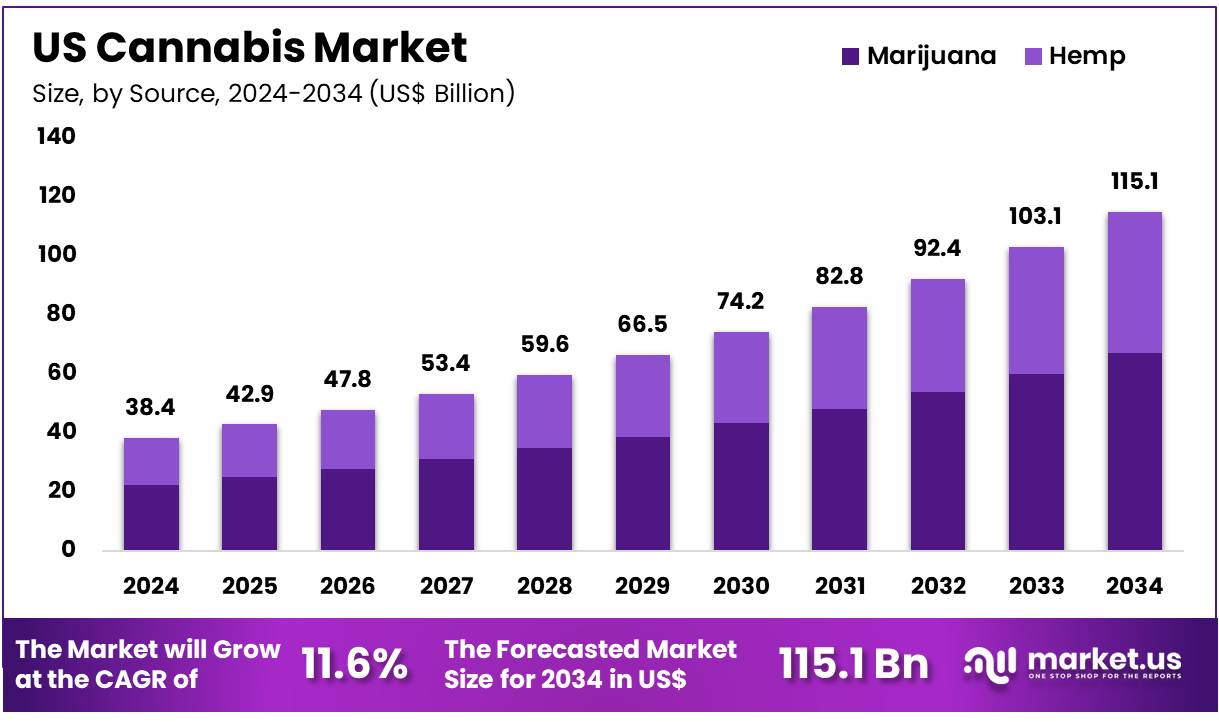

New York, NY – Dec 08, 2025 – The US Cannabis Market size is expected to be worth around US$ 115.1 Billion by 2034 from US$ 38.4 Billion in 2024, growing at a CAGR of 11.6% during the forecast period 2025 to 2034.

The expansion of the U.S. cannabis industry has been driven by steady regulatory progress, increasing consumer acceptance, and the widening availability of advanced product formats. Market performance has strengthened as legalization has broadened across key states, creating a structured environment for medical and adult-use applications. Demand growth has been supported by rising utilization in wellness, pain management, and recreational segments, establishing cannabis as a mainstream consumer category.

The market value has been estimated to exceed significant multibillion-dollar levels, and sustained growth has been anticipated over the forecast period. This momentum has been attributed to the introduction of innovative product lines, including edibles, concentrates, and infused wellness products. Retail infrastructure expansion has further contributed to enhanced accessibility, while improvements in supply-chain efficiency and cultivation technology have supported consistent product quality.

Policy developments at the federal level continue to be monitored closely, as reforms related to banking access, taxation, and interstate commerce are expected to influence long-term industry stability. State-level legalization initiatives have demonstrated strong voter support, reinforcing the trajectory toward broader regulatory alignment.

Market competition has intensified as leading operators pursue strategic partnerships, acquisitions, and geographic expansion to strengthen their positions. Investment activity remains cautiously optimistic, supported by improving transparency and compliance standards across the sector.

The U.S. cannabis market is positioned for continued advancement as consumers, regulators, and industry stakeholders adopt a more structured and mature approach to cannabis commercialization.

Key Takeaways

- In 2024, the U.S. cannabis market generated revenue of US$ 38.4 billion, and with a CAGR of 11.6%, the market is expected to reach US$ 115.1 billion by 2033.

- The source segment is categorized into hemp and marijuana, with marijuana accounting for 58.3% of the market share in 2024.

- Based on derivatives, the market is segmented into CBD, THC, and others, and CBD represented the largest share at 63.4%.

- Within the cultivation segment, the market is divided into indoor, greenhouse, and outdoor cultivation, with indoor cultivation holding the leading revenue share of 52.5%.

- Regarding end-use, the market is classified into industrial, medical, and recreational applications, and the recreational segment dominated with a 55.7% revenue share.

Segmentation Analysis

- Source Analysis: The marijuana segment accounted for 58.3% of the U.S. cannabis market in 2024, supported by rising demand across recreational and medicinal categories. Growth has been influenced by broader legalization initiatives, increasing societal acceptance, and the expanding development of marijuana-based therapeutic solutions targeting conditions such as pain and anxiety. Advancements in cultivation methods and a widening range of product formats are expected to reinforce the segment’s leadership over the forecast period.

- Derivatives Analysis: CBD represented 63.4% of the U.S. cannabis derivatives market, driven by its extensive adoption in wellness, pharmaceutical, and cosmetic applications. Demand has been underpinned by strong consumer interest in CBD’s therapeutic attributes, including analgesic, anxiolytic, and anti-inflammatory effects. Greater regulatory clarity, expanding legalization, and rising consumer awareness are projected to stimulate further growth in CBD-based tinctures, oils, edibles, and other formulations, particularly among health-conscious users seeking natural alternatives to conventional drug therapies.

- Cultivation Analysis: Indoor cultivation held a 52.5% revenue share, supported by the ability to maintain precise control over environmental variables. This approach enables consistent, high-quality cannabis production and facilitates year-round cultivation, making it highly suitable for premium and medicinal-grade products. Continued adoption of advanced technologies such as automated climate systems and hydroponics is expected to contribute to the expansion of indoor cultivation as demand increases for standardized, high-yield output.

- End-use Analysis: The recreational segment led the market with a 55.7% revenue share, driven by wider legalization and evolving consumer attitudes. Growing interest in edibles, concentrates, and other recreational formats has accelerated market expansion. As cannabis becomes more integrated into mainstream consumer behavior, enhanced retail distribution, delivery services, and broader product accessibility are expected to further strengthen the recreational segment’s dominance in the U.S. cannabis market.

Emerging Trends

- Rising Prevalence of Use: The prevalence of cannabis consumption in the United States has increased steadily. In 2021, an estimated 52.5 million adults, representing approximately 19 percent of the population, were reported to have used cannabis at least once. By 2022, this figure had risen to about 61.9 million adults, or roughly 19.5 percent. The expansion of legal access, shifting public attitudes, and wider product availability have been identified as key drivers behind this upward trajectory.

- Diversification of Consumption Methods: Although smoking remained the dominant mode of use in 2022, accounting for 79.4 percent of current consumers, alternative routes gained substantial traction. Edible products were used by 41.6 percent of consumers, vaping devices by 30.3 percent, and dabbing concentrates by 14.6 percent. Nearly half of all consumers (46.7 percent) employed two or more consumption methods, indicating a transition toward personalized dosing preferences and more tailored consumer experiences.

- Youth and Young Adult Patterns: Cannabis use among adolescents and young adults continues to present public health concerns. In 2022, approximately 30.7 percent of U.S. 12th-grade students reported past-year use, while 6.3 percent reported daily consumption. Among adults aged 18–24, roughly one in four individuals reported current use, and approximately one in eight reported daily use. These usage levels highlight persistent challenges associated with early initiation and potential implications for neurodevelopment.

- Federal Policy Developments: Federal rescheduling efforts are progressing. In January 2024, the U.S. Department of Health and Human Services recommended moving cannabis from Schedule I to Schedule III of the Controlled Substances Act following a comprehensive review. A related public hearing scheduled for January 21, 2025, was postponed pending procedural adjustments. The proposed rescheduling is expected to influence scientific research, financial services access, and interstate commerce frameworks.

Use Cases

- Medical Treatment of Epilepsy: Epidiolex, the first FDA-approved cannabis-derived pharmaceutical product, has been in use since June 25, 2018, for treating seizures associated with Lennox–Gastaut and Dravet syndromes in patients aged two years and older. Clinical evidence indicates that about 80 percent of patients receiving Epidiolex achieved a reduction in seizure frequency, compared with approximately 50 percent of patients in placebo groups.

- Management of Chemotherapy-Induced Nausea and AIDS-Related Anorexia: Synthetic THC formulations including Marinol and Syndros are approved for managing nausea and vomiting linked to cancer chemotherapy as well as appetite loss associated with AIDS. Cesamet (nabilone), another synthetic analogue, is also authorized for chemotherapy-related nausea. Collectively, these therapies support tens of thousands of patients each year who show limited response to conventional antiemetic treatments.

- Recreational and Wellness Applications: Cannabis continues to be utilized widely for recreational and wellness purposes. In 2022, approximately 15.3 percent of adults around 40 million people reported current use, with 8.2% consuming cannabis daily or near-daily. Product formats such as smokable flower, infused edibles, vape cartridges, and concentrated extracts are selected based on preferred onset characteristics, effect profiles, and duration.

- Public Health Surveillance and Safety Monitoring: From December 2018 to January 2023, a total of 539,106 cannabis-involved emergency department visits were recorded among individuals aged 24 years and younger. During peak periods, weekly visits among 15–24 year-olds reached up to 2,813. These data underscore the importance of surveillance mechanisms and educational initiatives aimed at mitigating risks associated with high-potency products and novel formulations.

Frequently Asked Questions on US Cannabis

- What is cannabis and how is it regulated in the United States?

Cannabis refers to plants used for medical and recreational purposes, regulated at the state level due to federal restrictions. States determine cultivation, distribution, and consumer access, creating a varied regulatory framework nationwide. - What are the main types of cannabis products available in the U.S.?

Cannabis products include flower, edibles, concentrates, oils, tinctures, and topicals. Availability depends on state laws, but product diversification has increased as consumer demand, innovation, and legalization support broader access across different usage categories. - How is medical cannabis used in the country?

Medical cannabis is used for managing conditions such as chronic pain, anxiety, and neurological disorders. Access generally requires physician approval and enrollment in a state medical program, ensuring controlled usage guided by established clinical recommendations. - What is the legal status of recreational cannabis in the U.S.?

Recreational cannabis is legal in several states, allowing adults to purchase and possess regulated products. However, federal prohibition limits interstate commerce and banking access, creating operational challenges despite growing consumer acceptance and expanding state-level legalization. - What cultivation method holds the largest share in the U.S. cannabis market?

Indoor cultivation captured 52.5% of market revenue due to its controlled growing environment. This method ensures consistent quality, optimized yields, and enhanced regulatory compliance, making it the preferred approach for commercial producers.

Conclusion

The U.S. cannabis market has entered a phase of structured expansion driven by regulatory progress, growing consumer acceptance, and sustained investment activity. Market performance has been supported by strong demand across recreational, medical, and wellness segments, while innovations in product formats and cultivation technologies have enhanced accessibility and quality.

State-level legalization momentum and anticipated federal reforms are expected to reinforce long-term stability. With rising usage prevalence, diversified consumption patterns, and improving industry standards, the sector is positioned for continued advancement. Overall, the market is projected to maintain robust growth as commercialization becomes increasingly mature and widely integrated.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)